Enabling Public Goods Funding to Extend Beyond Our Immediate Circles

TechFlow Selected TechFlow Selected

Enabling Public Goods Funding to Extend Beyond Our Immediate Circles

Exploring how to create truly effective public goods funding systems.

Author: Carl Cervone

Translator: Elsa

Translator's Preface

In this article, the author uses the concept of "circles" as a starting point to progressively reveal how we often focus only on our immediate circle in daily life and tend to neglect funding public goods beyond it—using distance as an excuse. The article further explores how to extend mechanisms for funding public goods into broader domains, transcending the circles we directly interact with, to build truly effective public goods funding systems. Through such expansion, we can construct a "diverse, civilization-scale public goods funding infrastructure."

Main Content

This article was inspired by the work and thought leadership of organizations explicitly mentioned (such as Gitcoin, Optimism, Drips, Superfluid, Hypercerts, etc.), as well as multiple conversations with Juan Benet and Raymond Cheng about network capital versus private capital.

Every funding ecosystem has core areas, along with important but peripheral ones

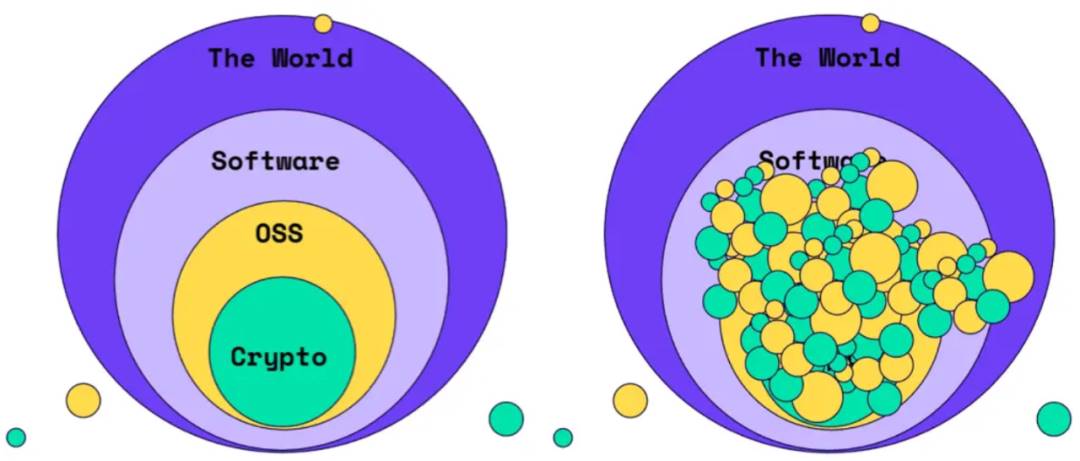

A 2021 blog post from Gitcoin effectively visualized the concept of nested scopes. It described a series of impact funding mechanisms that initially focused on the innermost circle ("crypto"), then expanded outward to the next layer ("open-source software"), and eventually influenced the entire world.

Owocki’s illustration shows the evolution of crypto-native impact funding—from “crypto funding crypto” to gradually affecting the whole world.

This is a solid approach: start by solving problems close to home, then scale outward.

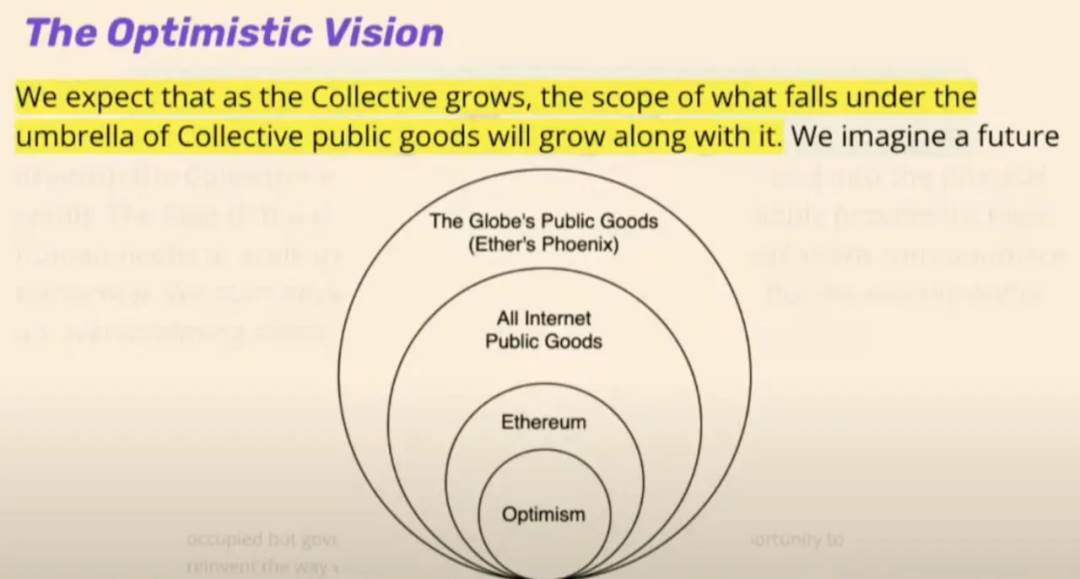

Optimism also uses a similar perspective to explain its vision for retroactive public goods funding.

Optimism aims to expand the scope of its supported public goods through retroactive funding.

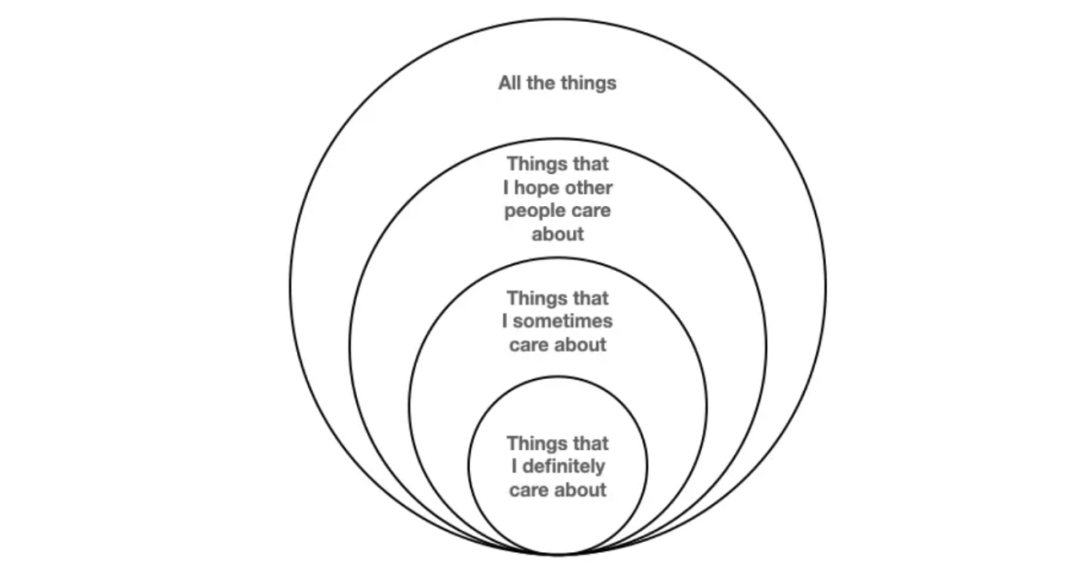

Optimism sits within Ethereum, which is contained within “all internet public goods,” which in turn is part of “global public goods.” Each outer layer is a superset of the one inside it.

Below is my simplified version of this four-circle meme.

I care about “everything,” but I don’t want to worry about how everything gets funded.

While I personally may not spend time thinking about deep-sea biodiversity or noise pollution in Kolkata, many people do care about these issues. Simply being aware of something often shifts it from the category of “everything” into “things I hope others care about.”

Most of us lack the ability to evaluate what matters outside our immediate circles

We’re generally capable of reasonably assessing things closely tied to our daily lives. This is our inner circle—the things we genuinely care about.

Within an organization, someone’s inner circle might include teammates, projects they collaborate on, tools they use regularly, and so on.

We can also assess some (though likely not all) things one degree upstream or downstream from our everyday circle. These are things we sometimes care about.

In the case of a software package, upstream could be your dependencies, while downstream would be projects that depend on your package. In an educational course, upstream might include valuable prerequisite courses or resources, while downstream includes students recommending the course to friends.

Software developers or educators can reach even further upstream—to research and institutions behind those resources. Now we enter the realm of caring about “everything.”

However, most rational individuals stop investing significant concern at this point. Beyond one degree, things become hazy. These are the things we hope others will care about.

The risk is that we may use distance as an excuse not to fund them, thereby exacerbating free-rider problems

It’s true that everything in our inner circle depends on strong funding in outer layers. Yet it’s difficult to contribute more than our “fair share” toward things one layer removed—even if someone attempts to calculate that share. There are valid reasons for this.

First, categorization within broad domains is hard. Categories like “all internet public goods” are so expansive that, viewed differently, almost anything could arguably belong and deserve funding.

Second, it’s difficult to incentivize stakeholders to care about funding beyond their immediate circles because impacts are so diffuse. I’d rather fund an entire team I know than a small, unknown portion of a team I don’t know.

Finally, there’s no direct consequence for not funding these projects—as long as we assume others continue funding them and won’t drop out.

Thus, we face a classic free-rider problem.

Beyond governments—which can print money, tax, and issue bonds to pay for long-term public goods—we as a society lack good mechanisms to fund things beyond our closest circles. Most capital flows toward things with short-term returns and closer proximity.

One way to address this is to let people focus on funding things close to them (i.e., things they can personally evaluate), while building mechanisms that consistently push portions of funds outward to peripheral layers.

Incidentally, this mirrors how private capital flows. We should try to emulate some characteristics of private capital.

Venture capital models work for things without short- or medium-term returns because private capital is composable and easily divisible

There’s a model for funding hard tech over 5–10+ year horizons: venture capital (VC). Of course, annual funding levels for long-term projects are more influenced by interest rates than final value. But given that VC has mobilized trillions of dollars over recent decades, it’s a proven model.

This model works largely because venture capital (and other sources of investment capital) is composable and easily divisible.

By composable, I mean you can take VC funding while also doing an IPO, securing bank loans, issuing bonds, or raising capital through more exotic mechanisms. In fact, this is expected—these financing methods are interoperable.

They compose well because ownership and cash distribution are clearly defined. Most companies use a sequence of financing instruments throughout their lifecycle.

Investment capital is also easily divisible. Many people contribute to the same pension fund. Many pension funds (and other investors) act as limited partners (LPs) in the same VC fund. Many VC funds invest in the same company. All these divisions occur upstream of the company and its day-to-day operations.

These traits make private capital highly efficient in flowing through complex network graphs. When a VC-backed company has a liquidity event (IPO, acquisition, etc.), proceeds flow efficiently—from the company to VCs, from VCs to LPs, from pension funds to retirees, even from retirees to their children.

This is not how public goods funding flows through networks. Compared to numerous irrigation channels, we have relatively few large water towers (governments, major foundations, high-net-worth individuals, etc.).

Private Capital vs. Public Capital Flow

To clarify, I’m not advocating that public goods should receive VC funding. I’m simply pointing out two key features of private capital that currently lack equivalents in public capital.

How can we enable more public goods funding to flow beyond our direct circles?

Optimism recently announced a new program for retroactive funding within its ecosystem.

In past rounds, the range of eligible projects was very broad. Going forward, funding will be much narrower, focusing on closer upstream and downstream links in its value chain.

How Optimism currently thinks about upstream and downstream impact

Unsurprisingly, feedback has been mixed—many projects previously within scope are now excluded from upcoming rounds.

In the newly announced first round, 10 million tokens were allocated to “on-chain builders.” By the third round, on-chain builders received a disproportionately small share—only about 1.5 million out of 30 million tokens available. What could these projects do with 2–5x the current level of retroactive funding?

One thing they could do is reinvest part of their tokens into their own retroactive funding or grant rounds.

For example, if Optimism funds DeFi apps that drive network transaction volume, those apps could fund front-ends, portfolio trackers, and other tools serving their own impact focus.

If Optimism funds core OP Stack dependencies, those teams could fund their own dependencies or research contributors.

What if projects used what they deemed their deserved portion and cycled the rest forward?

This is already happening in various forms. The Ethereum Attestation Service (EAS) now runs a scholarship program for teams building on its protocol. Pokt just announced its own retroactive funding round, pooling all tokens received from Optimism (and Arbitrum) into this initiative. Even Kiwi News, which received below-median funding in Round 3, implemented its own version of retroactive funding for community contributors.

Meanwhile, Degen Chain pioneered a more radical idea: giving community members token allocations with the requirement to gift them as “tips” to other members.

All these experiments redirect public goods funding from central pools (like OP or Degen treasuries) to the edges, expanding their reach.

The next step is making these commitments explicit and verifiable.

One possible mechanism: let projects define a floor value and a percentage above the floor they’re willing to allocate to their own funding pool. For instance, my floor might be 50 tokens, with 20% allocated above that. If I receive 100 tokens total, I’d allocate 10 tokens (20% of the 50 above floor) to fund edge projects in my network. If I receive only 40 tokens, I keep all 40.

(Incidentally, my project did something similar in the last Optimism round.)

Beyond pushing more funds outward, this plays a crucial role in helping public goods projects establish cost bases. Long-term, for projects consistently receiving less than expected, the message becomes clear: they’re either mispricing their work or undervalued within the funding ecosystem.

In future rounds, projects with surpluses will be evaluated not only on their direct impact but also on the broader influence created through smart capital allocation. Projects unwilling to run their own funding programs could park surplus in productive places—like the Gitcoin matching pool, Protocol Guild—or even burn it!

In my view, these two values should remain confidential until after funding. If a project receives 100 tokens and donates 10, others shouldn’t know whether its parameters were (50, 20%) or (90, 100%).

The final step is connecting these systems.

The examples of EAS, Pokt, and Kiwi News are encouraging, but each requires setting up new projects, applying/exchanging/transferring grant tokens to new wallets, and manually sending funds to new recipients.

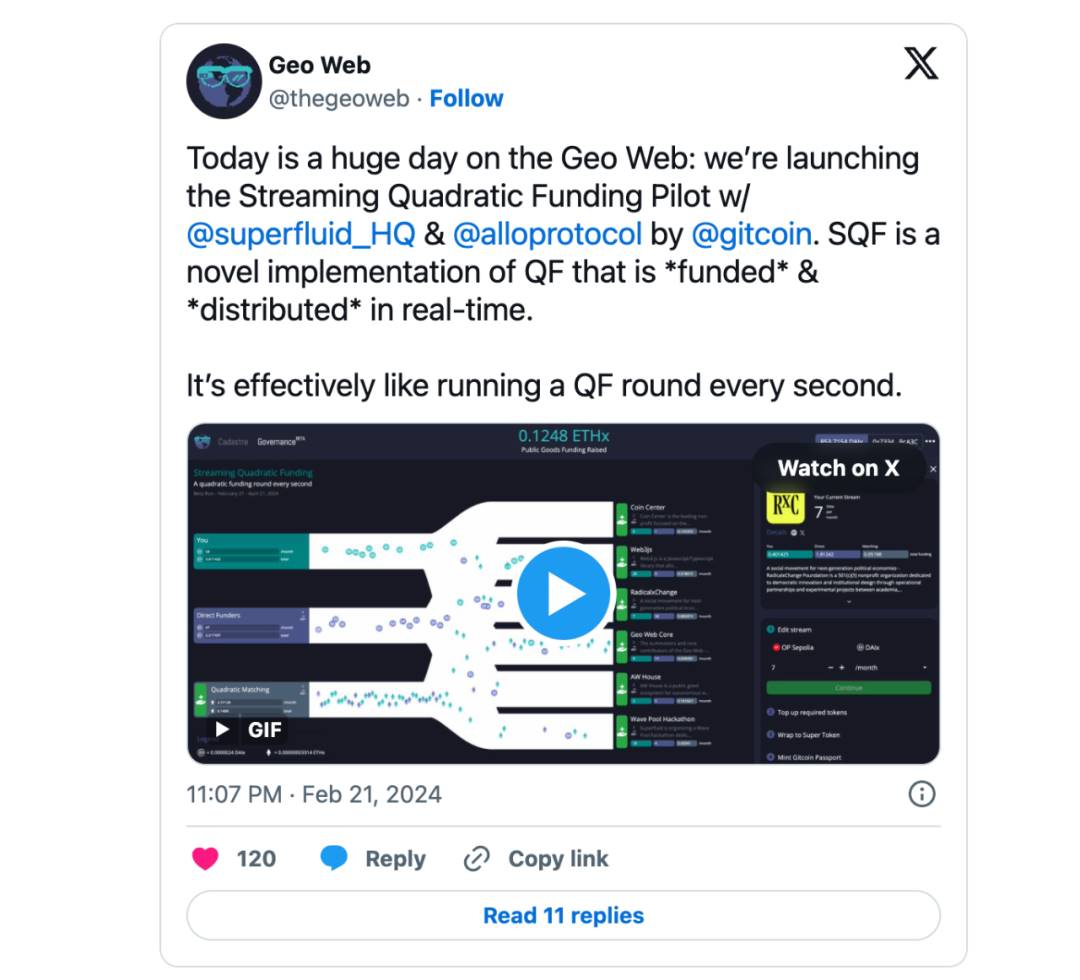

Protocols like Drips, Allo, Superfluid, and Hypercerts provide the underlying infrastructure for more composable funding flows—now we need to connect these pipes, just like Geo Web’s pilot project.

The mission of this cycle is to create truly effective public goods funding systems. Then, we begin scaling them

In crypto, we’re still experimenting with mechanisms to decide which projects get funded and how capital is distributed. Compared to decentralized finance (DeFi), public goods funding infrastructure remains immature, poorly composable, and unproven in practice.

To move beyond experimentation and achieve scale, we must solve two problems:

1. Measurement—not just proving these mechanisms work, but showing they outperform traditional public goods funding models (see [1] for why this is a meaningful challenge worth pursuing, and [2] for analysis of Gitcoin’s long-term impact);

2. Explicit commitments: clear promises about how “profits” or surplus funds flow to outer circles.

In venture capital, there’s always another investor behind every investor—ultimately, it might be your grandmother (more accurately, all of our grandmothers). Every such investor is incentivized to allocate capital effectively to earn trust and access larger pools in the future.

For public goods, there’s always a tightly connected group—upstream or downstream—that you depend on. But currently, there is no commitment to share surpluses with these entities. Until such commitments become standard, public goods funding will struggle to scale beyond our immediate circles.

We haven’t yet reached a stage superior to traditional models (image from Gitcoin whitepaper)

I believe it’s insufficient to merely promise, “Once we reach a certain scale, we’ll fund these projects.” That’s too easy to change. Instead, these commitments must be established early, embedded as foundational elements in funding mechanisms and grant programs.

I find it unreasonable to expect a few whales’ treasuries to fund everything. That’s the water tower model used by traditional governments and large foundations.

But the earlier and more explicitly we commit to funding our dependencies while still small, the more we demonstrate a real market for public goods—expanding the total addressable market (TAM) and shifting incentives.

Only then will we possess something truly worth promoting—something that builds momentum and creates the “diverse, civilization-scale public goods funding infrastructure” we dream of.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News