A Major Comparison Between Established and New VC Coins: These New Tokens Have "Fallen Into Value"

TechFlow Selected TechFlow Selected

A Major Comparison Between Established and New VC Coins: These New Tokens Have "Fallen Into Value"

In the short term, L2, cross-chain, and restaking sectors have declined to relatively better valuations; in the long term, new tokens from various VC-backed projects still have 68% downside potential.

Author: Nan Zhi, Odaily Planet Daily

During the underperforming second and third quarters in the crypto market, newly launched "VC coins" have come under widespread criticism. These tokens typically exhibit characteristics of "low circulation, high FDV," and tend to decline continuously as tokens are released. Now, most of these tokens have completed several unlock cycles and have dropped significantly amid multiple market downturns—so have any of them already "fallen into value territory"?

In this article, Odaily compares mainstream new projects from the past year with previous bull cycle "VC coins" using funding data and circulating market cap to explore the answer.

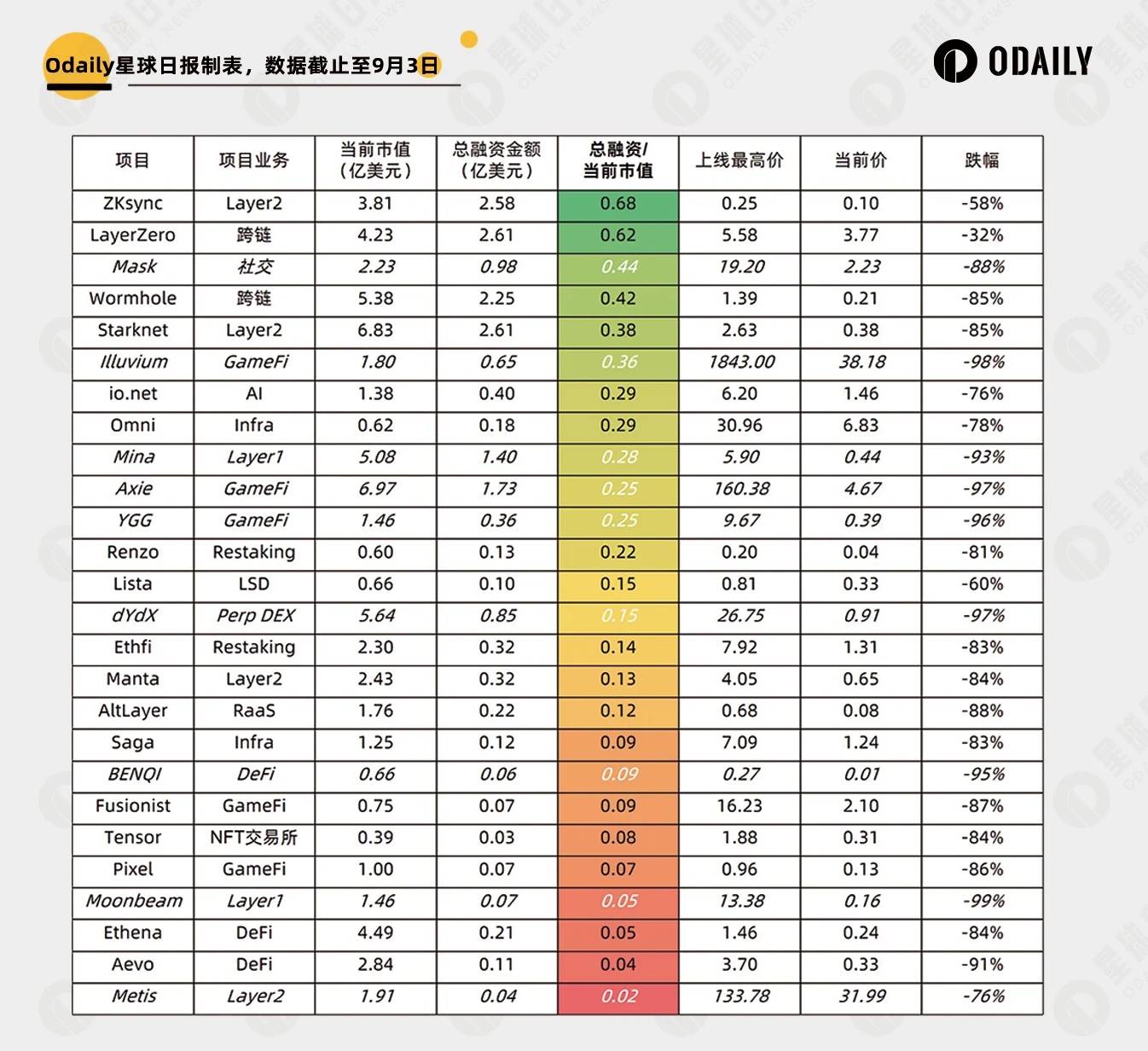

Top-Tier VC Coins & Binance New Listings

-

Sample: This section analyzes top-tier tokens such as STRK (Starknet), W (Wormhole), along with new tokens from Binance Launchpool, totaling 21 tokens.

-

Data sources: Circulating market cap, funding amounts, and current prices are sourced from Rootdata. For projects that did not disclose funding, only disclosed valuation figures are shown. "All-time high price" refers to the highest 4H closing price on Binance candlestick charts since listing, excluding brief spike highs.

-

Evaluation method: Value-for-money is measured by total funding ÷ current market cap—the higher the ratio, the better the relative value.

The results are shown in the chart below. It’s clear that major airdrop-driven projects, despite large funding rounds, now offer relatively high value after falling 60%–80%.

In terms of sectors, Layer 2, cross-chain, and LSD & Restaking show the best value. In contrast, GameFi and DeFi rank lowest in value efficiency.

If we instead evaluate value based on drawdown magnitude, GameFi occupies four of the top ten spots (Xai being a Layer 3 dedicated to gaming).

If a game project demonstrates strong fundamentals and its token has a direct cash flow linkage to the ecosystem, it may be considered as having fallen into value territory.

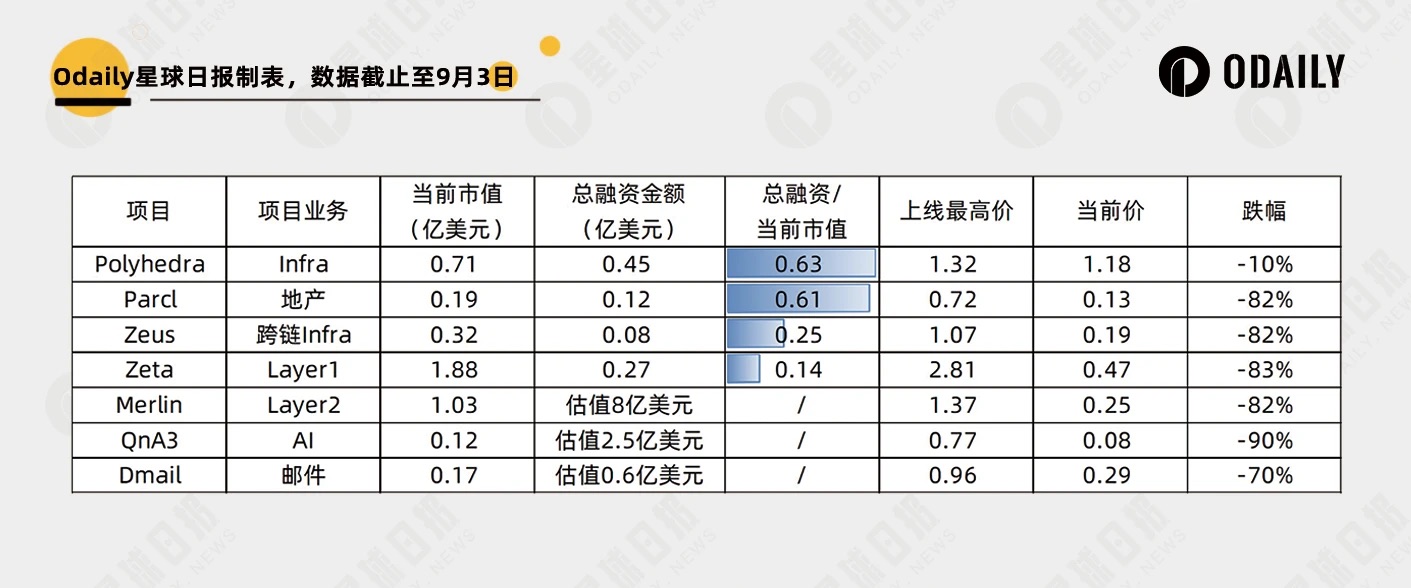

OKX New Listings

Using the same evaluation methodology but focusing on projects first listed on OKX, we obtain the following data.

ZKJ (Polyhedra) and PRCL (Parcl) maintain strong value metrics comparable to the top tier from the prior section. Zeus and Zeta fall into the mid-tier range.

Comparison with Legacy "VC Coins"

During the last bull cycle, many heavily funded tokens emerged. We consider those projects that have survived multiple years of token unlocks and bear market pressure as having undergone sufficient market testing, making them solid benchmarks for comparison.

New vs. Old: Layer 2 and LSD

As noted earlier, Layer 2 and Restaking stand out among new launches in terms of value. How do they compare against established Layer 2 and LSD projects? Odaily's analysis is shown below.

It’s evident that, after multiple price corrections, the newer projects in these sectors now match or even exceed legacy projects in value efficiency. Before the next major unlock events, there may be some early bottom-fishing opportunities.

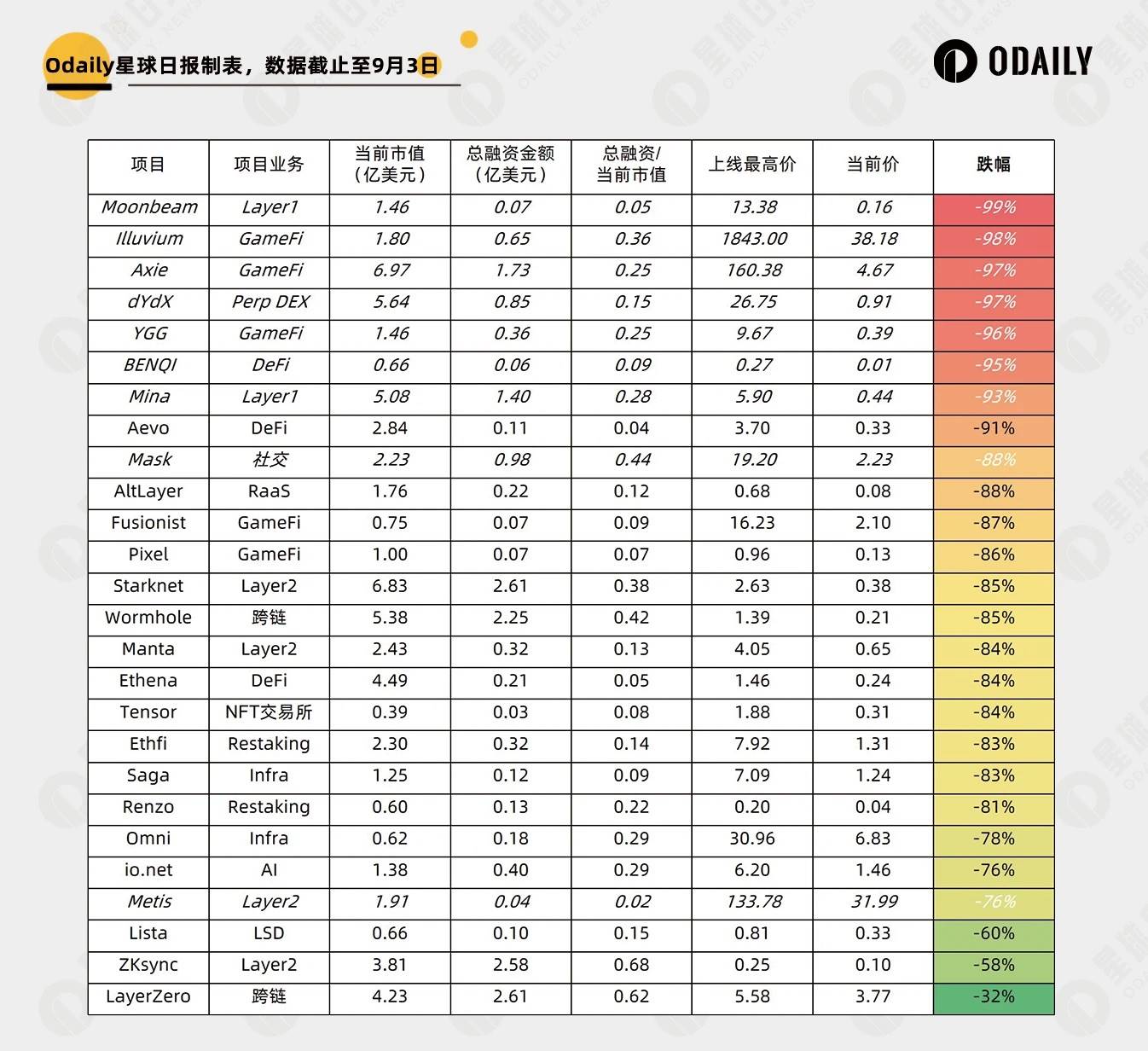

Broad-Spectrum Comparison

We further selected projects that raised funds and launched in the first half of 2021, such as dYdX, Mask, and Axie Infinity, marked in italics and white in the chart below.

Overall, legacy projects still hold slightly better relative value than new ones, suggesting most new tokens still have meaningful downside potential.

A clearer picture emerges when comparing drawdown depth. The chart below shows that top VC-backed tokens from the last bull run ultimately fell over 95% from their peaks (average drawdown: 93%), while new tokens have only averaged a 78% decline so far.

Falling from 78% to 93% implies an additional 68% drop (1–(1–93%)/(1–78%)). However, this level of depreciation may require prolonged vesting schedules and extended bear market conditions to materialize.

Conclusion

In summary, tokens in the Layer 2, cross-chain, and LSD & Restaking sectors may have reached short-term value territory, but in the long run, most VC-backed new tokens still face substantial downside risks.

Readers are advised to make further decisions by evaluating project revenue, whether tokenomics are tied to revenue streams, and upcoming token release schedules. Short-term bottom fishing or long-term shorting of low-value-efficiency tokens could both be viable strategies.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News