Climbing Mount Taihang Amid Snow-Covered Peaks: Reviewing ETHENA's Gains and Losses, and the Future of the Algorithmic Stablecoin/Funding Rate Track

TechFlow Selected TechFlow Selected

Climbing Mount Taihang Amid Snow-Covered Peaks: Reviewing ETHENA's Gains and Losses, and the Future of the Algorithmic Stablecoin/Funding Rate Track

In the long bear market, there are still many trials ahead for ETHENA.

Author: Luke|DeFi

Before we dive into ETHENA, let’s rewind the timeline to May 2022.

At that time, UST's issuance volume hit a record high. Exchanges began progressively supporting trading pairs between UST and major cryptocurrencies like BTC/ETH/SOL. The Terra ecosystem appeared vibrant and thriving—its native token Luna reached an all-time high at the beginning of the year and remained resilient even during the bearish Q1 market. After several instances of depegging and re-pegging, the market seemed to believe—or Terra believed itself—that its algorithmic stablecoin model was indestructible.

Yet everything came crashing down with the death spiral. In the aftermath, the market was left in disarray—billions in bad debt from Genesis and 3AC, leading to the collapse of Celsius and BlockFi, and ultimately bankrupting hundreds of thousands of South Korean families.

In a way, Terra’s collapse marked or triggered the true beginning of the last bear market, peaking when 3AC was liquidated (does anyone remember ETH being in triple digits back in June 2022?), and finally concluding with the fall of FTX. What followed was the now-familiar rebound (though I wouldn’t call the market since late 2023 a bull run—more on that later).

Afterwards, the algorithmic stablecoin space fell silent for a long time—until early this year, when ETHENA emerged out of nowhere with its synthetic asset concept.

What is ETHENA? How does it work?

I’ll try to explain ETHENA’s mechanism in the simplest terms possible.

Imagine Xiao Ming owns 1 ETH and decides to deposit it into ETHENA.

At that moment, ETH is priced at $2,500 per unit. After depositing his ETH, Xiao Ming receives 2,500 USDe.

Xiao Ming can then stake his USDe to earn ETHENA’s high APY rewards.

Where do these rewards come from?

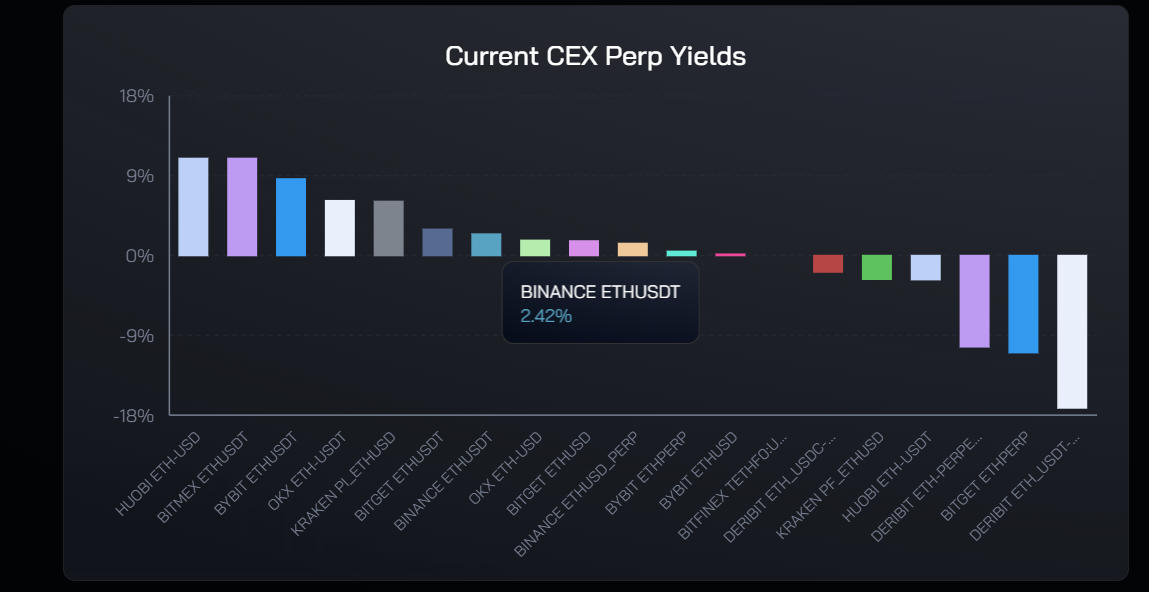

When ETHENA receives Xiao Ming’s staked ETH, it opens 1x leveraged short positions on ETH perpetual contracts denominated in crypto (coin-margined) across multiple centralized exchanges, with a perpetual liquidation price of zero.

The yield comes from the funding rate income generated by these coin-margined short positions.

ETHENA painted a beautiful picture for exchanges, VCs, and users alike—a synthetically created dollar backed entirely by on-chain assets, with no risk of liquidation, generating fee revenue for exchanges while offering users substantial annualized returns. It looked like a win-win game—no losers, at least not until April when ENA was listed.

Over a month before listing, ETHENA completed a funding round, raising $14 million at a $300 million valuation. In this three-way win among exchanges, VCs, and retail investors, VCs were the first to cash in big. Even at today’s price (August 9, 2024, ENA trading around $0.30), early VC investors are sitting on roughly a 15x return—let alone the peak prices seen in early April when new ATHs were constantly being set.

I don’t intend to join the chorus of FUD-spewing KOLs who attacked ENA right after launch with baseless conspiracy theories or comparisons to LUNA’s “death spiral.” At its core, ENA is a rare innovative product in DeFi this cycle. Compared to countless copycat ZK L2s, one dead GameFi project after another, cross-chain bridges packed with VC cronies, or yet another “girlfriend token” on Binance, ENA stands out as a genuinely novel product with real user demand. Too many people have wasted time reinventing the wheel. Despite its flaws, ENA remains a strong project built by a talented team driven by a solid idea—the good outweighs the bad.

ETHENA’s vision is grand—but reality seems unable to support such lofty ambitions.

According to the latest data from the ETHENA dashboard:

They’ve accumulated over $17 billion in positions across more than ten CEXs and DEXs.

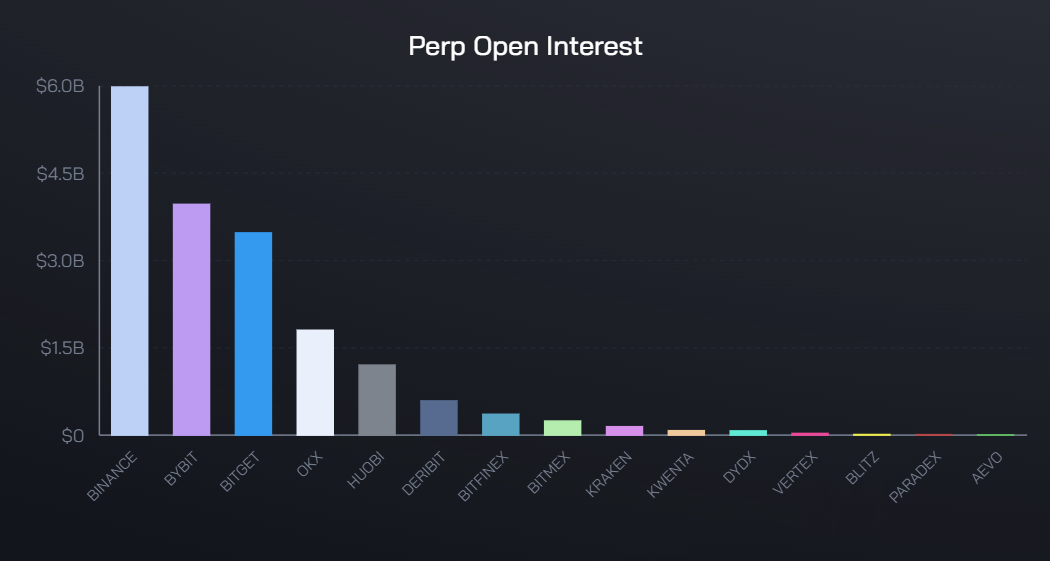

Take Binance as an example: To secure yields for ETH stakers and USDe holders, ETHENA claims to have opened $2.8 billion worth of contract positions on Binance.

Here, I’m unsure whether the error lies with ENA or Binance. A quick calculation shows Binance’s total open interest in ETH coin-margined and USD-margined contracts combined is about $4.1 billion.

If ETHENA truly holds $2.8 billion in contract positions as claimed, the displayed positive funding rate APY on their dashboard would be impossible.

When one counterparty controls more than half of the total open interest in the same direction, the funding rate must move against them. That is: if ETHENA really opened the amount of ETH short positions they claim (regardless of whether they’re coin-margined) at 1x leverage, their funding rate would definitely be negative.

Either Binance or ETHENA is lying.

Even allowing for the possibility that I miscalculated or missed some volume/open interest, ETHENA’s model of distributing funding rate income to users to sustain USDe’s value and encourage further minting is fundamentally unworkable.

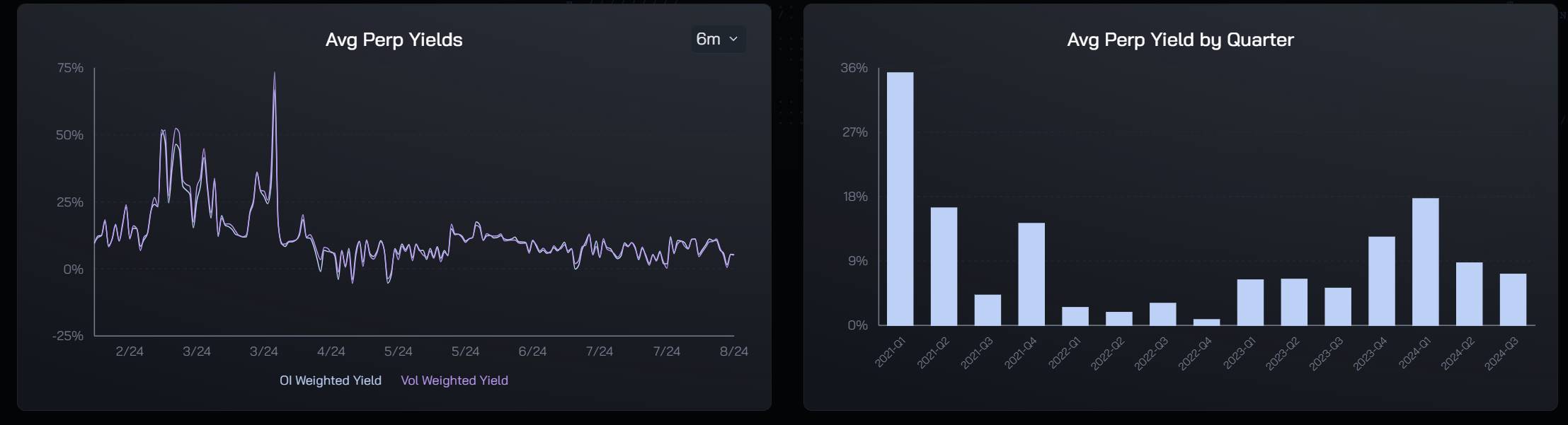

Most importantly: current trading volumes across exchanges are far too low to support ETHENA’s ambition of becoming a native synthetic asset. There’s a meme in Chinese internet culture: “the bigger xx, the smaller xx.” Here, I’d say: the more ETH ETHENA holds, the lower user yields will become.

CEX and DEX trading volumes have ceilings. As USDe issuance grows, so does the required size of 1x ETH short positions—eventually reaching a point where ETHENA disrupts market equilibrium, single-handedly dragging ETH’s funding rate into prolonged negative territory (where shorts pay longs).

Not to mention, during future bear markets—even without disrupting market balance—prolonged negative funding rates would cause the protocol’s income to fall short of payouts.

ETHENA’s foundational design—using perpetual contract funding rates as yield—is a double-edged sword. It enables stable returns under normal conditions (assuming no data manipulation and position sizes don’t skew the long/short ratio), but it also caps ETHENA’s ceiling: given finite market capacity, USDe cannot scale indefinitely without eroding user yields.

On another front, USDe’s use cases aren’t unfolding as smoothly as ETHENA hoped. To date, the largest investor and exchange, Binance, still doesn’t accept USDe as collateral. ETHENA’s envisioned dual flywheel—rising USDe demand boosting ETH price—is increasingly difficult to achieve in the current market.

Moreover, despite being a DeFi and on-chain project, ETHENA lacks transparency. Users have no API access to verify whether their funds are actually being hedged as promised. In a way, this contradicts the essence of blockchain: decentralization. Hedging inside exchange black boxes means any data shown to users could be fabricated or manipulated.

Finally, ETHENA’s choice to issue a stablecoin USDe to generate user yield is smart, but issuing a stablecoin inherently imposes a glass ceiling on the project. ENA can only extract funding rate yields from assets supported for USDe minting—and those assets are limited. Countless altcoin perpetual contracts’ funding rates remain untapped, mere scraps in retail traders’ battles. ETHENA can’t possibly support every crypto asset for USDe minting.

Ice blocks the Yellow River; snow blankets Mount Taihang. During this long bear market, ETHENA faces many trials ahead.

Oh, I almost forgot to mention the other asset ETHENA issued besides USDe—the so-called governance token ENA. At the end of June, ETHENA updated ENA’s tokenomics. But it’s still the same old wine in a new bottle. The persistent criticisms—lack of utility, minimal functionality—remain unaddressed.

I don’t understand why basic staking functionality wasn’t implemented until months after listing. And the APY offered to users is single-digit—lower than even staking ETH itself.

The team behaves like a貔貅 (a mythical creature that only takes in, never gives out)—hoarding massive token and fee revenues, giving nothing back to users, while extending unlock schedules.

Well, after all, ENA is your so-called “governance token.” Aside from suddenly changing users’ vested ENA from monthly to weekly unlocks and forcing 50% of holdings to be locked, how many actual governance proposals have even been passed?

To conclude, let me reiterate my view: ETHENA is an innovative and so far promising project, but the ENA token is a complete shitcoin.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News