Japan's central bank hikes rates, U.S. economy heading into recession? What's the underlying logic behind Bitcoin's plunge?

TechFlow Selected TechFlow Selected

Japan's central bank hikes rates, U.S. economy heading into recession? What's the underlying logic behind Bitcoin's plunge?

Risks showed early warning signs, but the market chose to ignore them selectively.

Author: Babywhale, Techub News

August 5, 2024, is destined to go down in history. Following last weekend's U.S. July non-farm payroll data that fell far short of expectations and an unexpected surge in unemployment, markets began fearing an impending recession in the U.S. economy. After a brief period of calm over the weekend, Asian financial markets were hit hard when trading resumed on Monday. Stock markets in Japan and South Korea triggered circuit breakers one after another, while Bitcoin plummeted from nearly $60,000 in the early hours of the morning to $49,000.

Asset prices typically rise slowly, step by step, but often just one or two days of decline can erase months or even years of gains. Will this brief market selloff reverse rapidly like it did at the beginning of 2020, or will the downward trend continue?

Bitcoin Falls Below $50,000; Japanese and Korean Markets Trigger Circuit Breakers

Let’s first review what happened on this “Black Monday” morning.

At around 9 a.m. today, Bitcoin plunged from $56,000 to approximately $52,000. After a brief consolidation, it continued falling and dropped as low as $49,000 after 2 p.m.

According to Coinglass data, as of writing, over $1.1 billion in liquidations have occurred across the cryptocurrency market in the past 24 hours—$382 million in Bitcoin and $356 million in Ethereum. Nearly 290,000 positions were wiped out mercilessly by the market, including a single largest liquidation on Huobi involving a $27 million Bitcoin-denominated futures position.

Traditional financial markets fared no better. Today, Asian, European, and Australian equities were all battered (data below sourced from Jinshi Data):

-

South Korea’s KOSPI index closed down 8.78%, with intraday losses briefly widening to 10%, marking its largest single-day drop since October 2008 and triggering the circuit breaker mechanism.

-

Japan’s Nikkei 225 index closed down 12%, having plunged as much as 15% intraday; the Topix index fell 13%. Both indices triggered secondary trading halts. The Nikkei 225 Volatility Index surged 132%, setting a new record for single-day gain.

-

India’s NIFTY and SENSEX indices both dropped 3%. India’s stock volatility index rose 52%, the largest increase since August 2015.

-

Taiwan Weighted Index closed down 8.35%, recording its worst single-day performance ever. Australia’s stock market plunged 3.6% at close, its worst result since 2020.

-

Turkey’s stock market triggered a full-market circuit breaker shortly after opening, followed by a second halt.

-

European markets opened sharply lower: Germany’s DAX index and Euro Stoxx 50 both fell 3%, while Italy’s FTSE MIB dropped 4%.

Risks Were Forewarned, But Markets Chose to Ignore Them

The Federal Reserve’s July meeting kept interest rates unchanged, but Fed Chair Jerome Powell almost explicitly signaled during the subsequent press conference that a rate cut in September is all but certain—provided August data doesn’t bring major surprises. The market widely priced this anticipated cut as a "preventive measure": although inflation hasn’t yet returned to target levels, it shows a clear downward trend, and with unemployment starting to fall, a rate cut could help stabilize employment. Even if inflation rebounds slightly, it would still be within manageable bounds.

Just as markets were basking in the belief that the U.S. economy remains strong and that this rate cut would further unleash liquidity, reality struck hard. On Friday evening Beijing time (Friday morning U.S. time), the U.S. released July seasonally adjusted non-farm payroll data showing only 114,000 jobs added—far below the expected 175,000. Additionally, the unemployment rate unexpectedly rose to 4.3%, officially triggering the "Sahm Rule" (when the three-month moving average of the U.S. unemployment rate exceeds its lowest point over the past 12 months by 0.5 percentage points or more, it signals the early stage of a recession).

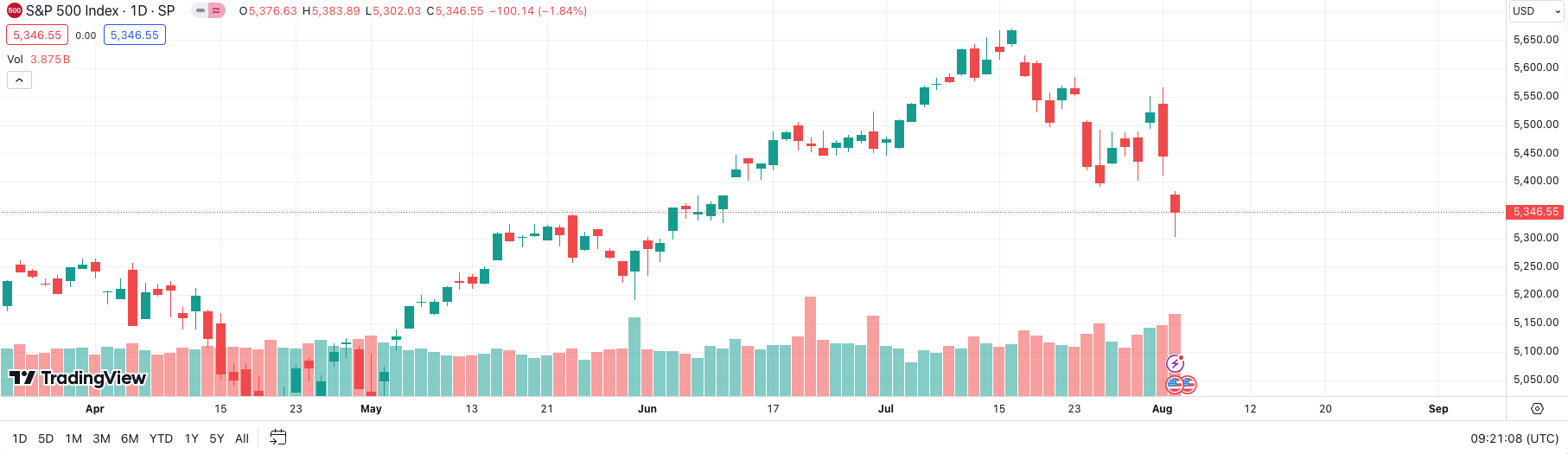

Although some Fed officials later commented that “the non-farm data, while disappointing, remains within a reasonable range,” and that “triggering the Sahm Rule does not necessarily mean a recession has begun,” the market voted with its feet. The S&P 500 dropped nearly 2% in a single day, the Nasdaq fell over 2%, and Bitcoin briefly dipped to around $61,000.

S&P 500 index declined for two consecutive days last Thursday and Friday

Looking back over recent months, despite solid performances by global equity markets including U.S. stocks, there were numerous warning signs that may have been selectively ignored due to excessive market optimism.

First, Berkshire Hathaway’s consistent move since the start of the year to sell stocks and increase cash reserves suggests that perhaps the world’s most astute investor had already begun de-risking. At the Q1 shareholder meeting, Buffett stated that unless they see opportunities with minimal risk and high returns, they wouldn’t deploy their cash—then nearing $200 billion. Then, on Saturday Beijing time, Berkshire Hathaway’s quarterly report revealed it sold nearly half of its Apple shares in Q2, bringing its cash reserves to a record $277 billion.

When the U.S. June unemployment rate was reported at 4.1% in July, warning voices emerged because it was perilously close to triggering the Sahm Rule. Some analysts argued that, given data lags, the Fed should have started cutting rates in July to prevent an oncoming recession. Unfortunately, these warnings were drowned out by stronger-than-expected GDP and other data that followed.

Now rewind to March 19 this year: after its monetary policy meeting, the Bank of Japan decided to raise its benchmark interest rate from -0.1% to 0%-0.1%, marking Japan’s first rate hike since 2007 and signaling an end to decades of ultra-loose policy aimed at stimulating the economy. Yet following the hike, USD/JPY suddenly spiked, even briefly breaking above 160—perhaps one reason why the market didn’t pay much attention to this highly symbolic move.

On July 31, contrary to widespread expectations that Japan would maintain its prior rate, the Bank of Japan surprised markets by hiking rates by 15 basis points to 0.15%-0.25%. This move clearly intensified market fears. Peter Berezin, Chief Global Strategist and Research Director at BCA Research and former Goldman Sachs and IMF economist, had said as early as March—when Japan first hiked—that “in modern financial history, no single indicator better predicts the onset of the next global recession than the moment the Bank of Japan begins raising rates.”

If you believe such macro-level information may not fully dictate Bitcoin’s price movements, consider this highly significant risk signal visible solely from Bitcoin’s behavior: this year, Bitcoin has failed six consecutive times to break and hold above $70,000. If you’re ignoring such a clear signal, then frankly, you might be overly bullish.

Returning to Bitcoin: although every crash has its scapegoat, Bitcoin was already exhibiting a clear downtrend before today’s plunge. So the real question now is whether there exists a logical framework to determine Bitcoin’s overarching trend—one capable of explaining its movements in recent years. Here’s a perspective worth considering.

“A Pure Risk Asset Without Fundamentals”

Before elaborating on this potential logic governing Bitcoin, I must share a few candid thoughts.

First, I urge everyone—if you haven’t already—to mute all so-called “institutional views.” Most publicly stated institutional opinions are driven by self-interest. You’ve likely seen numerous institutions aggressively bullish on Bitcoin in recent months amid its rally. If even I—a non-professional investor—could identify the many risks outlined earlier, these institutions should be even more alert.

Why choose to ignore these risks and blindly promote bullish sentiment? We don’t know—perhaps for attention, to stimulate retail trading, or to attract investors to paid products. But the core truth remains: “All gifts of fate come with a hidden price tag.” You may use others’ views as reference, but don’t let them lead you by the nose.

Second, readers should distinguish between “investment” and “trading.” Many of you claim to be investing, but in reality, you’re trading. In my view, investment means identifying macro trends and selecting assets accordingly, exiting only when the underlying thesis breaks down. For example, when the U.S. launched unlimited QE in 2020 and global inflation surged, investors should have favored risk assets. Similarly, amid rising geopolitical tensions, gold should have been bought as a hedge—as savvy investors did when the Russia-Ukraine war erupted two years ago.

What is trading? In my opinion, most activity in the crypto space can only be classified as trading, because projects lack fundamentals—no transparency into fund operations, rampant unregulated insider information, and virtually no foundation for genuine investment. So-called research often merely analyzes market sentiment and ultimately serves trading purposes.

Back to the main argument: the analytical framework I propose rests on a basic assumption—that global financial markets currently treat Bitcoin as a pure inflation-hedging risk asset with no need to assess fundamentals. Think of it as the opposite of gold. Gold is a pure safe-haven asset unaffected by corporate revenues, profits, or industry prospects; Bitcoin, conversely, is a pure risk asset free from such fundamental influences.

When did this definition emerge? I believe the clearest evidence dates back to March 12, 2020—the so-called “Black Thursday.” Let’s retrace the market’s trajectory from that day using this logic.

From March 12, 2020, to April 14, 2021, the Fed slashed rates and launched unlimited QE, flooding markets with liquidity. Equities soared, and some capital spilled into crypto. Fueled by the DeFi phenomenon, Bitcoin surged from around $3,800 to nearly $65,000. As a pure risk asset, the outcome—rising prices amid dollar printing—was predictable.

From April 14, 2021, to May 19, 2021, Bitcoin dropped from nearly $65,000 to a low of $30,000. This correction stemmed from profit-taking, panic triggered by China’s mining ban announcement on May 19, and excessively high leverage across the market.

But I’d highlight one overlooked point: although many weren’t focused on macro then, ahead of the April 2021 FOMC meeting, markets had begun pricing in potential rate hikes as early as May—or even April—due to surging U.S. home prices and growing equity bubbles. Although the Fed remained dovish in April, markets already sensed looming inflation. Bitcoin traders started worrying about sudden rate hikes. The failure to break $60,000 in the days leading up to May 19 sent a clear signal of market divergence. The May 13 dip confirmed that risk-off sentiment had overtaken blind buying—what followed needs no explanation.

How do we explain the subsequent rally to a new high of $69,000, followed by a plunge to around $15,000?

Everyone knows the Fed began hiking rates in March 2022, but Powell had spent months preparing the market—the hikes were anticipated, and markets reacted early. This is likely why Bitcoin, after surpassing $65,000, stalled at $69,000 instead of soaring. Once the Fed made clear its commitment to fighting inflation, Bitcoin began a steady decline. In 2022, inflation persisted for a time, but markets expected aggressive hikes would quickly curb it—removing any upward catalyst for Bitcoin. Of course, extreme events like Terra’s collapse and FTX’s bankruptcy amplified the downturn. Without them, Bitcoin might not have fallen to $15,000—but the bearish trend was inevitable.

Bear markets are easy to explain, but the hardest part is explaining Bitcoin’s rise from $30,000 in late 2021 and the bull run from late last year until recently. While earlier phases relied heavily on “expectations,” these two rallies required combining expectations with “facts.”

The late-2021 rally occurred as markets realized Powell wasn’t planning rate cuts and inflation continued to build—so “no near-term cuts” plus “persistent inflation” drove Bitcoin to new highs.

As for the recent bull run, many attribute it to rate-cut expectations and optimism about future liquidity. I’ve repeatedly stated in public forums that once rate cuts are confirmed, Bitcoin will likely fall—because whether inflation has truly cooled or the economy is faltering, the very factor Bitcoin hedges against—“inflation”—is no longer present.

Thus, the primary drivers behind this Bitcoin-specific bull market were: persistent inflation, no clear Fed rate-cut plan, and the approval of Bitcoin spot ETFs—which provided institutions and funds unable to directly buy Bitcoin with a tool to invest in a “pure inflation-hedging asset.” So I’ll boldly say: even without spot ETFs, Bitcoin would have risen. But whether it would have reached $70,000? That’s uncertain.

Zooming in: after Trump was shot, Bitcoin surged. Many argue this reflected increased odds of a Trump victory and his pro-crypto stance, fueling market optimism. That’s half right—Trump’s rising chances are accurate, but the deeper reason lies in his anti-globalization policies, which markets anticipate could boost U.S. inflation. In essence, the market was trading that expectation.

And the subsequent drop? Likewise, because even if Trump wins, he won’t take office until next year—while current inflation is indeed cooling. That’s the reality.

I won’t claim this analysis is flawless, but since this logic consistently explains directional moves (with exact magnitudes influenced by events and sentiment), I believe it holds meaningful value.

Looking ahead, under this logic, as long as rate cuts continue, Bitcoin is likely to remain in a downtrend. When this decline ends and a new uptrend begins will depend on whether a future economic crisis forces the Fed to restart large-scale quantitative easing—reigniting inflation—or whether this selloff proves merely a panic-driven episode, with the Fed’s rate cuts unfolding without triggering a global recession, instead fostering gradual or even accelerated economic recovery. These factors will critically shape Bitcoin’s future trajectory.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News