An Open and Regulated Swedish Cryptocurrency Tax Regime: Overview and Outlook

TechFlow Selected TechFlow Selected

An Open and Regulated Swedish Cryptocurrency Tax Regime: Overview and Outlook

This article will analyze Sweden's cryptocurrency monetary policy from three aspects—summary and outlook—and provide an outlook on its future development trends.

By TaxDAO

1. Introduction

The Kingdom of Sweden (Swedish: Konungariket Sverige), commonly known as Sweden (Sverige), is a Nordic country located on the Scandinavian Peninsula and one of the largest economies in Northern Europe. In 2023, its GDP reached $593.12 billion, with a per capita GDP of $56,291, reflecting a high standard of living and strong economic potential. Despite recent challenges such as high taxation and substantial government deficits, Sweden continues to maintain a robust social welfare system that provides comprehensive cradle-to-grave support for its citizens. Additionally, Sweden offers a highly favorable environment for entrepreneurship. The government’s emphasis on education and technological innovation has driven significant research advancements and the rapid growth of "unicorn" companies. Cryptocurrencies have also flourished in Sweden due to relatively lenient regulations, leading to increasing transaction volumes. Sweden's cryptocurrency tax policies not only influence the stability and development of its domestic financial markets but are also of great significance to international investors and businesses. This article analyzes Sweden's cryptocurrency tax policy from three perspectives: the country's basic tax system, its cryptocurrency-specific tax regime, and a summary and outlook on crypto asset taxation in Sweden, while offering insights into future trends.

2. Overview of Sweden's Basic Tax System

2.1 Swedish Tax Framework

Sweden operates a dual-level taxation system comprising central and local authorities. The tax administration consists of the Swedish Tax Agency (Skatteverket) and regional tax offices. Skatteverket is responsible for issuing tax regulations, providing administrative interpretations, offering tax guidance, and overseeing regional tax policy implementation. Regional tax offices handle the actual collection of both national and local taxes. Among the 10 regional tax agencies under Skatteverket, Stockholm, Malmö, and Gothenburg have dedicated large enterprise tax management units. All levels of tax authorities independently enforce tax laws and are accountable directly to the law; neither the government nor parliament may interfere in their operations. All tax legislation is enacted by the Riksdag (Swedish Parliament), which includes a specialized Tax Committee responsible for tax-related matters. Sweden’s tax system centers around income tax, with value-added tax (VAT, known locally as MOMS) serving as another major revenue source. Key taxes include individual income tax, corporate income tax, VAT, excise duties, social security contributions, property and land taxes, and inheritance and gift taxes.

2.2 Income Tax

Swedish income tax is divided into corporate income tax and personal income tax.

The taxpayer for Swedish corporate income tax is the resident company, subject to a flat rate of 21.4%. In Sweden, companies are classified as either resident or non-resident entities. The determination of residency follows the place-of-incorporation principle—i.e., whether the company is registered with any level of government within Sweden. Under this criterion, any entity incorporated under Swedish law qualifies as a resident company regardless of where its headquarters, management, or control center is located, and irrespective of whether its investors are Swedish or foreign nationals. Even unregistered companies may be considered tax residents if their effective management is based in Sweden or if they are otherwise deemed taxable in Sweden due to residence, management location, or similar grounds—especially for purposes of tax treaties. In regions receiving special governmental support, up to 10% of social security contributions paid by employers can be added back as an additional deduction against corporate income tax. Furthermore, companies may annually set aside a “tax distribution reserve” amounting to no more than 25% of pre-tax profits. This reserve can be used to offset losses in future years and is not taxed when created. However, if unused after six years, it must be included in taxable income and taxed accordingly.

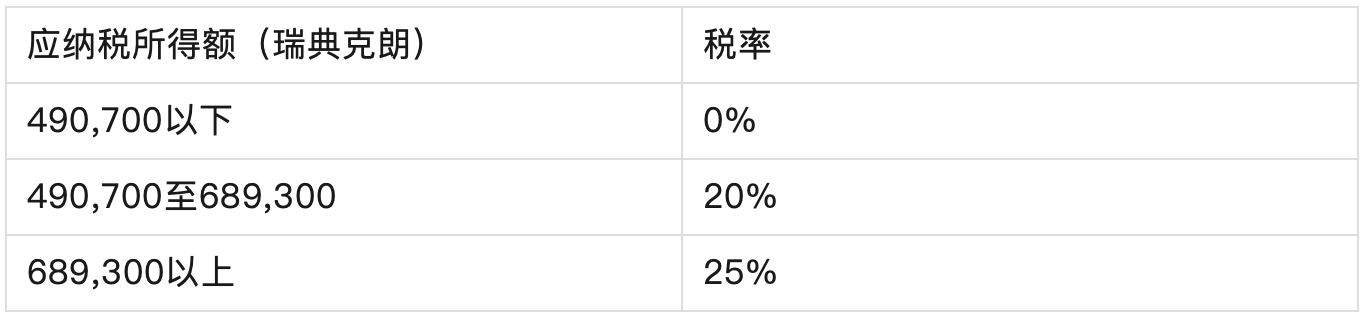

For personal income tax, taxpayers are categorized as residents or non-residents. Resident individuals—those who have a home or habitually reside in Sweden—are taxed on their worldwide income. Taxable income falls into three categories: employment income, business income, and investment income. Non-residents—individuals without a home or habitual residence in Sweden—are taxed only on income sourced within Sweden. For employment and business income, taxpayers may deduct personal allowances before calculating municipal and national income taxes. If a taxpayer receives income related to the previous two or next two tax years (including the current year)—specifically employment income or certain types of business income—and that income exceeds SEK 50,000, cross-period income adjustment rules apply. The progressive tax rates are detailed in the table below:

Investment income refers to gains realized from the disposal of assets minus acquisition costs. This is referred to as capital gains tax, and calculation methods vary depending on how the gain is realized. Except in cases of gifts or death, sales, exchanges, and transfers of assets are generally taxed as investment income. Investment income is taxed at a flat rate of 30%, and local governments do not levy additional taxes on such income.

2.3 Value-Added Tax (VAT)

Sweden’s value-added tax is known as MOMS. The tax liability applies to any entity or individual conducting economic activities in Sweden. This definition excludes individuals employed under employment contracts or other legal arrangements. Legal entities registered for VAT purposes are also considered liable when purchasing specific services from outside Sweden. Economic activity includes production, trading, or service provision, including mining, agriculture, and similar professions. Since January 1, 2017, small enterprises whose annual turnover does not exceed SEK 30,000 in the current and prior two fiscal years are exempt from VAT registration, though they may voluntarily choose to register. Broadly accessible non-profit organizations and registered religious communities are treated as non-taxable entities and thus exempt from VAT. This provision also applies to partnerships and trading companies. VAT-taxable activities include: (1) all supplies of goods and services not explicitly exempted by Swedish law; and (2) imports and intra-EU acquisitions. Sweden’s standard VAT rate is 25%, aligned with EU VAT Directive requirements. Reduced rates apply to certain goods and services: 12% (e.g., restaurants and catering services, food, artists selling their own works, imported artworks, collectibles, and antiques), and 6% (e.g., books, newspapers, magazines, passenger transport, circus, cinema, or theater admission fees, zoo entry fees).

3. Sweden's Cryptocurrency Tax Regime

In Sweden, investors can directly purchase Bitcoin and other cryptocurrencies through platforms such as Safello, btcx, and Trijo, or via online banks like Avanza and Nordnet. Goobit, the company behind btcx, serves approximately 200,000 Swedish customers. For emerging technology sectors like cryptocurrency, Sweden’s tax framework demonstrates advanced thinking and a welcoming approach, offering a transparent and predictable tax environment that supports long-term business growth, protects commercial reputations, and builds investor trust.

The Swedish Tax Agency (Skatteverket), as the primary authority for national taxation, is responsible not only for tax collection and administration but also for enforcing tax laws to protect society from tax abuse. In the field of cryptocurrency, Skatteverket has clearly defined its position: income derived from cryptocurrencies is classified as capital gains—a subset of income tax—subject to a 30% tax rate. This clear guidance provides both crypto businesses and individual investors with a straightforward path to compliance. For example, when a Swedish resident sells cryptocurrency holdings at a profit, that gain is taxed as capital income, whether the sale occurs on an exchange, the coins were obtained through mining, or payments were received in crypto for goods or services. All such income must be meticulously recorded in the annual tax return. Taxpayers are required to report detailed transaction information, including dates of purchase and sale, realized profits or losses, and conversions into Swedish krona (SEK) based on exchange rates on the transaction dates.

To ensure accurate tax reporting, taxpayers must closely monitor exchange rate fluctuations, as even small transactions can result in significant tax implications due to volatility. Moreover, if a taxpayer incurs losses from cryptocurrency trading, these losses can be used to offset other capital gains, thereby reducing the overall taxable base. However, this process is subject to specific rules and limitations, and taxpayers are advised to consult professional tax advisors to ensure full compliance.

In exceptional cases, income generated from cryptocurrency mining, staking, or participation in decentralized finance (DeFi) activities may be classified as business income and taxed according to the individual’s total income and applicable progressive rates. While most cryptocurrency transactions are taxable, certain specific activities may qualify for tax exemptions or exclusions under particular conditions.

In recent years, Skatteverket has enhanced tax standards through close cooperation with EU tax authorities and international organizations, ensuring fairness and transparency in tax policy. As an OECD member, Sweden actively adheres to OECD tax principles and has introduced new measures in cryptocurrency taxation, such as adopting the Crypto-Asset Reporting Framework (CARF), which mandates automatic reporting of tax-relevant data by crypto firms and facilitates international data sharing. In 2022, the European Commission proposed amendments to the DAC directive aligned with CARF objectives, establishing new rules for all crypto-asset service providers within the EU, consistent with MiCA regulations and anti-money laundering directives, enhancing capabilities to detect tax evasion and fraud. Additionally, in April this year, Skatteverket investigated 21 cryptocurrency mining companies and found that 18 had provided misleading information to evade taxes, resulting in demands for over SEK 990 million in unpaid taxes—demonstrating Sweden’s strict enforcement of cryptocurrency tax regulations.

4. Summary and Outlook on Sweden's Cryptocurrency Asset Taxation

At the forefront of global financial innovation, Sweden is actively shaping a market environment for cryptocurrencies that is both open and well-regulated, and is expected to further strengthen oversight in this area. Sweden is likely to deepen collaboration with other EU countries and international organizations, improving global compliance in cryptocurrency taxation through information sharing and best practice exchange. In the future, the Swedish government may explore innovative incentives—for instance, offering tax reductions to businesses that proactively report cryptocurrency transactions, or providing financial subsidies to companies investing in cryptocurrency-related research and development—to promote tax compliance while advancing the development and application of crypto technologies. Sweden might consider offering tax credits to enterprises adopting blockchain technology to enhance transparency and efficiency, or provide R&D grants to startups developing secure cryptocurrency storage solutions. Such policies would help cultivate a business environment conducive to innovation while ensuring tax regulations are respected and effectively enforced.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News