Crypto Market Guide for July: Macroeconomic Analysis and Upcoming Key Market Events

TechFlow Selected TechFlow Selected

Crypto Market Guide for July: Macroeconomic Analysis and Upcoming Key Market Events

In such an environment, is now the best time to buy the dip?

In the first half of 2024, the cryptocurrency market experienced numerous major events. For instance, the approval of Bitcoin spot ETFs, the imminent greenlighting of Ethereum ETFs, and now growing expectations for a Solana ETF. At the same time, the global economy is entering a rate-cutting cycle. Although the exact timing of U.S. rate cuts remains uncertain, inflation has been effectively contained—undoubtedly positive news for the crypto market. Regulatory shifts continue to be a key factor influencing the market, with governments around the world holding differing stances on cryptocurrencies, making regulatory developments a crucial variable in shaping market trends. In the recently concluded quarter, BTC dropped by 16%, with sustained outflows of institutional capital and a lack of breakthrough technological innovation placing the entire cryptocurrency market in a challenging situation. Currently, BTC continues to fluctuate within a range of $56,000 to $70,000, and investors remain largely观望 (on the sidelines). Under such macro conditions, is this the best time to buy the dip? Will the cryptocurrency market enter a new bull run in the second half of the year? These questions warrant deeper exploration.

1. Key Cryptocurrency Events Timeline This Month

As we enter July, beyond the above-mentioned project milestones, the crypto market must also closely monitor:

-

The impact of Mt. Gox’s June Bitcoin repayment plan, which triggered a market downturn—this remains a critical dynamic to watch in July;

-

Close attention to the approval process for Ethereum spot ETFs, including the remaining S-1 filings;

-

Large token unlocks for WLD, SOL, ALT, XAI, ARB, and others;

-

FTX creditors will vote on whether to receive compensation in cash or cryptocurrency;

-

On the public chain front, Cardano will undergo the Chang mainnet hard fork; HNT will have a new subnetwork proposal; Arbitrum’s ARB will launch staking functionality;

-

Finally, Jupiter’s JUP will reduce total supply by 30%; Gala Games’ G token will undergo a 1:60 remint; Orion’s ORN will roll out its Lumia brand upgrade.

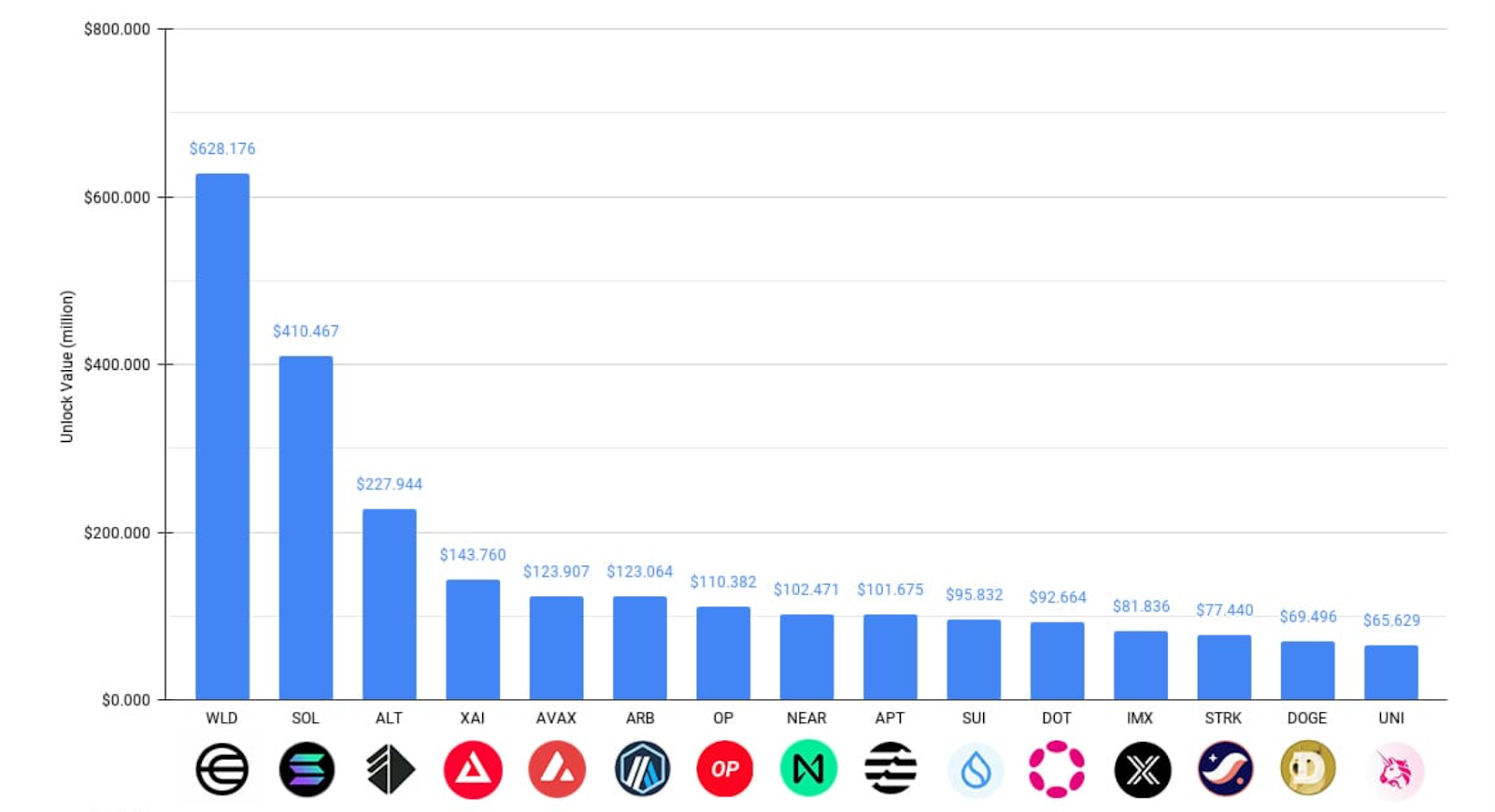

With many tokens facing large-scale unlocks, the chart below shows the top 15 projects by unlock volume in July, as tracked by @Token_Unlocks:

-

$WLD has the highest unlock value this month, exceeding $600 million, accounting for 53.36% of current circulating supply.

-

$SOL ranks second with over $400 million unlocked. While this amount seems significant, due to $SOL’s high market cap, the unlock represents only 0.5% of current circulating supply.

-

$ALT sees a notable unlock this month, with nearly 45% of its current circulating supply being released.

-

$XAI also faces a high unlock volume this month, representing 71.59% of its current circulating supply.

-

Layer-2 Ethereum tokens $ARB, $OP, and $STRK will see unlocks of $120 million, $110 million, and $70 million respectively in July.

2. Macro Data Analysis

After entering July, the focus of macroeconomics remains centered on when interest rates will be cut. Federal Reserve Chair Jerome Powell has long stated that the timing of rate cuts will depend on two key indicators: inflation and unemployment (the “4+2” metrics). Against the backdrop of sweeping global changes and industrial restructuring between China and the U.S. having profound impacts on the world economy, these transformations are not ones whose results will manifest quickly.

Last Friday, the U.S. core PCE annual rate for May fell to 2.6%, the lowest level in three years, providing confidence for a September rate cut. However, how economic data for July and August will perform remains a focal point for markets. The decline in core PCE was primarily driven by falling prices in housing, automobiles, and crude oil. Yet in July, prices across these three categories have rebounded, and expectations for June’s core PCE data are not optimistic. As a result, smart money in the market has not yet positioned early.

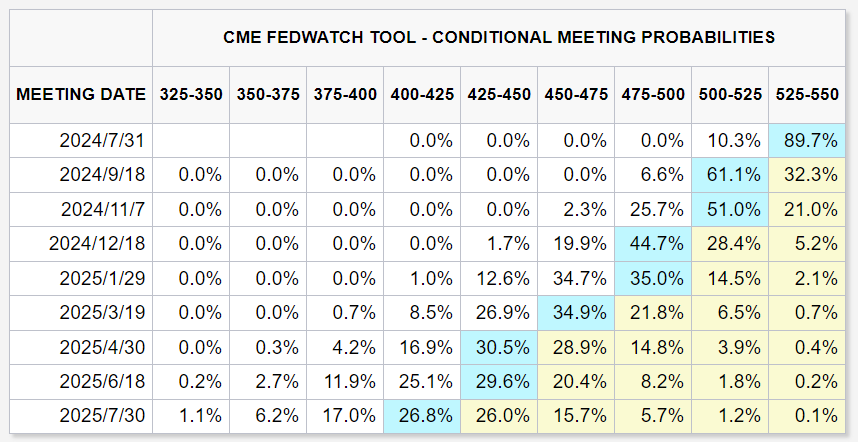

Notably, following the release of May’s core PCE data, the CME FedWatch tool showed that market expectations for a 25-basis-point rate cut in September rose to 61%, with a 44.7% chance of another cut in December. While rate cut expectations have increased, the market remains cautious—especially ahead of June’s data release. Market sentiment toward risk assets like Bitcoin reflects this caution. Although Bitcoin faces downside risks, its room for further decline appears limited in the absence of major negative catalysts.

Moreover, changes in the international economic environment cannot be overlooked. Industrial realignment between China and the U.S. is having far-reaching effects on the global economic landscape—a process that may take considerable time before its full impact becomes evident. This adjustment affects global supply chains, trade relations, and investment flows, all of which require ongoing market attention.

Economic data over the coming months will play a pivotal role in shaping market expectations and guiding Fed policy decisions. Investors need to closely track upcoming data releases while considering shifts in the global economic environment and market sentiment to make more informed investment decisions.

Since March, altcoins have undergone over three months of consolidation, and Bitcoin has formed a clear M-top pattern. We had previously hoped that key events—the June 27 presidential debate, June 28 PCE data release, and July 2 potential launch of an Ethereum spot ETF—would provide bullish momentum. While the PCE figures were favorable for equities and risk markets, market interpretation of the data has become more hesitant due to the influence of the U.S. election. Short-term volatility highlights the market's divergence and uncertainty about future direction.

3. Key Factors in the Macro Market

The cryptocurrency market continues to face multiple influential factors. The correlation between U.S. equities and crypto assets over past cycles is undeniable. As the global economy enters a rate-cutting cycle, the overall performance of risk assets will be critical. At the same time, the strength of the U.S. dollar—hovering near its highest levels in 30 years—exerts downward pressure on crypto markets. A strong dollar makes dollar-denominated cryptocurrencies relatively more expensive and can dampen investor risk appetite. With high interest rates, investors may prefer parking funds in banks to earn yield, thereby affecting market liquidity.

Additionally, the anticipated approval and listing of Ethereum spot ETFs could inject fresh momentum into Ethereum and the broader crypto ecosystem. The upcoming U.S. election in the second half of the year will also significantly influence market sentiment. These intertwined factors will collectively determine the trajectory of the crypto market in H2 2024.

On Tuesday morning Eastern Time, Federal Reserve Chair Jerome Powell spoke at the ECB’s Central Banking Forum, stating that the Fed has made substantial progress in controlling inflation but wants to see further evidence before beginning rate cuts. The forum also included European Central Bank President Christine Lagarde and Brazil’s central bank governor.

Powell expressed satisfaction with inflation control over the past year: “We’ve made considerable progress in bringing inflation back toward our target. Recent data suggests we’re back on track toward disinflation.” However, he emphasized that adjusting policy too quickly could undermine gains, while moving too slowly might hinder economic recovery. Powell noted the Fed must strike a delicate balance between taming inflation and avoiding labor market deterioration.

Regarding the labor market, Powell said the U.S. unemployment rate remains low at 4%, though the job market is gradually cooling. He expects inflation over the next year to settle in the lower-middle part of the 2%-3% range but expressed concern about persistently high services inflation, particularly wage-related components.

Despite rising market expectations for a September rate cut, Powell refused to specify a date. When asked if a September cut was possible, he replied: “I won’t commit to any specific date right now.” This signals the Fed remains cautious, with future policy firmly data-dependent.

Powell also remarked that fiscal policy lies in the hands of politicians, and debt sustainability should be a future priority. His comments boosted markets—Nasdaq turned positive, S&P 500 erased early losses, Treasury yields declined further, and the dollar index dipped to session lows. Swap traders continue to price in nearly two rate cuts by year-end.

Potential Impact of the U.S. Election on Markets

The primary source of potential political and economic volatility in the U.S. going forward remains the presidential election. As voter expectations shift between Trump and Biden, markets are already pricing in the different implications of each candidate’s victory. If a “Trump rally” takes hold—driven by expectations of large-scale loose policies and massive injections into the stock market—capital could flow early into risk markets, triggering sharp rallies.

Market participants are concerned about election-related uncertainty not only because of stark policy differences between candidates, but also due to their divergent economic impacts. Trump’s platform favors large fiscal stimulus and tax cuts, which markets may view as equity-positive. In contrast, Biden emphasizes infrastructure spending and social welfare, which could support growth but raises concerns over potential tax increases.

If Trump’s odds of winning rise, markets may front-run this outcome, rapidly channeling funds into equities and other risk assets, pushing prices higher. However, this scenario carries inherent risks, including uncertainty around policy implementation and long-term economic consequences. Markets will continue monitoring campaign developments and assessing each candidate’s likelihood of victory and their respective economic implications.

Overall, the U.S. election is not just a political contest—it is a globally significant event. Investors must stay vigilant and adapt strategies promptly to navigate potential market turbulence.

4. Sectors to Watch

Ethereum Ecosystem

Key Focus: ETH, ENS, LDO, SSV, ETHFI

The ETF Store predicts Ethereum spot ETFs could launch during the week of July 15. Once approved and listed by the SEC, an Ethereum spot ETF would significantly improve market sentiment. Similar to Bitcoin ETFs, Ethereum ETF approval would allow easier access for institutional investors, potentially driving up prices. The entire Ethereum ecosystem would likely follow suit. Pay close attention to native Ethereum projects like ENS, leading staking protocol LDO, and restaking leader ETHFI. In the second half of the year, anticipate innovation from parallel EVMs—keep an eye on Fuel, Monad, Berachain, and Sei’s applications in gaming chains.

Solana Ecosystem

Key Focus: SOL, JUP, HNT

On June 28, asset manager VanEck filed an application with the SEC for a Solana ETF (VanEck SolanaTrust). Subsequently, 21Shares submitted an S-1 filing for a Solana ETF, capturing significant market attention. Solana recently launched powerful Blinks, transforming on-chain interactions like Mint and Swap into Twitter buttons. By linking social media accounts, users can one-click copy-trade trending assets, opening up diverse application scenarios. High-speed information demands from early meme tokens may be fulfilled via Blinks, further expanding the meme market. Phantom and Backpack wallets, DEX Jupiter, NFT marketplace Tensor, and other protocols already support Blinks.

This month, Helium will also announce a new subnetwork proposal—watch HNT’s price action. Additionally, Sanctum, Solana’s liquid staking token (LST) aggregation protocol offering restaking, is即将 (soon) to airdrop. It has published tokenomics for $CLOUD, with 10% allocated to airdrops. With TVL exceeding $800 million, it ranks fifth in Solana’s ecosystem by TVL—an important project to monitor.

AI Sector

Key Focus: RNDR, AKT

Continued large-scale capital inflows are fueling AI technology development and driving interest in AI-related crypto projects. Ongoing market preference for AI is expected to benefit decentralized GPU platforms like Render and Akash. In July, watch for updates on the merger of three tokens: AGIX, FET, and OCEAN.

Meme Sector

Key Focus: PEPE, BONK, WIF, TRUMP

Pump.fun, the meme coin factory, has surpassed Ethereum in daily revenue. Amid broad market declines and altcoin crashes, investors are turning to memes for solace. Consider investing in well-established projects with strong community consensus like PEPE to avoid rapid drawdowns. Memes are emotion-driven; any exciting news can act as a catalyst. A large, active, and engaged community remains the backbone of any successful meme—WIF and BONK excel here. For Solana-based meme investments, WIF and BONK are likely top choices. With the U.S. election still ongoing in the second half of the year, TRUMP offers numerous cyclical opportunities. Overall, meme projects carry high risk and randomness—invest with caution.

GameFi and SocialFi

Key Focus: TON, RON

TON demonstrated strong resilience during this correction, maintaining positive monthly returns—an impressive performance. In July, Telegram mini-program games Hamster and Catizen are set to launch tokens—closely monitor their price action. Meanwhile, gaming chain Ronin will undergo its Goda upgrade this month. After the hard fork, validators will earn daily rewards for block production, and smart contract upgradability will be introduced. Proposal REP-0014 implements Ethereum’s EIP-1559, directing gas fees to the Ronin treasury—future use of these funds, such as RON buybacks, warrants attention.

5. Conclusion

BTC has once again fallen below $58,000, creating widespread pessimism. Currently, BTC hash rate has dropped to its lowest level since December 2022. Multiple indicators—including miner reserves, exchange reserves, and the Miner Position Index (MPI)—suggest the market may have bottomed. Miners are showing stronger holding intent and reduced selling behavior, lowering the likelihood of further BTC dumps. These signs collectively indicate improving market sentiment and expectations. Bitcoin is searching for new upward momentum to lay the foundation for a rebound—this catalyst could come from an official U.S. rate cut, the emergence of breakthrough technology, or the resolution of the election with pro-crypto advocate Trump introducing market-friendly policies. At that point, long-time观望 (sidelined) investors may re-enter, reigniting capital inflows.

Overall, the cryptocurrency market retains strong rebound potential in the second half of 2024. We should continuously monitor changes in policy, fundamentals, innovation, and market sentiment. This article does not constitute investment advice. Risk management remains the most important—and oft-repeated—priority: “If a losing position is causing you emotional distress, the solution is simple: exit immediately, because you’ll always have another opportunity to re-enter (Paul Tudor Jones).” When market conditions are unfavorable, it’s best not to linger. Step back, observe, and patiently wait for the next opportunity—avoid overtrading driven by emotions.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News