The Underrated Hong Kong Crypto ETFs: Surface Appearances and Undercurrents Behind the Data

TechFlow Selected TechFlow Selected

The Underrated Hong Kong Crypto ETFs: Surface Appearances and Undercurrents Behind the Data

Trading volume and scale show an inverted trend, with stakeholders refining processes and clearing bottlenecks. The key inflection point for growth may come in two months.

Author: Jupiter Zheng, Partner at HashKey Capital's Secondary Fund

On May 24, the U.S. Securities and Exchange Commission (SEC) officially approved 19b-4 filings for eight spot Ethereum ETFs, signaling a shift in regulatory stance from rigid to more accommodating. The launch of spot Ethereum ETFs in the United States now appears imminent, igniting market sentiment and fueling an already heated secondary market.

In stark contrast, Hong Kong’s six crypto asset ETFs—covering both Bitcoin and Ethereum—which launched on April 30 as the first of their kind, have appeared relatively lackluster over the past month, even drawing criticism due to what some perceive as underwhelming market performance.

Markets often overestimate the short-term impact of new innovations while underestimating their long-term significance. This article aims to clarify how Hong Kong's crypto ETFs have truly performed over the past month, identify underlying factors, uncover overlooked variables, and explore potential future trajectories.

The "Lull" in Data and Key Variables

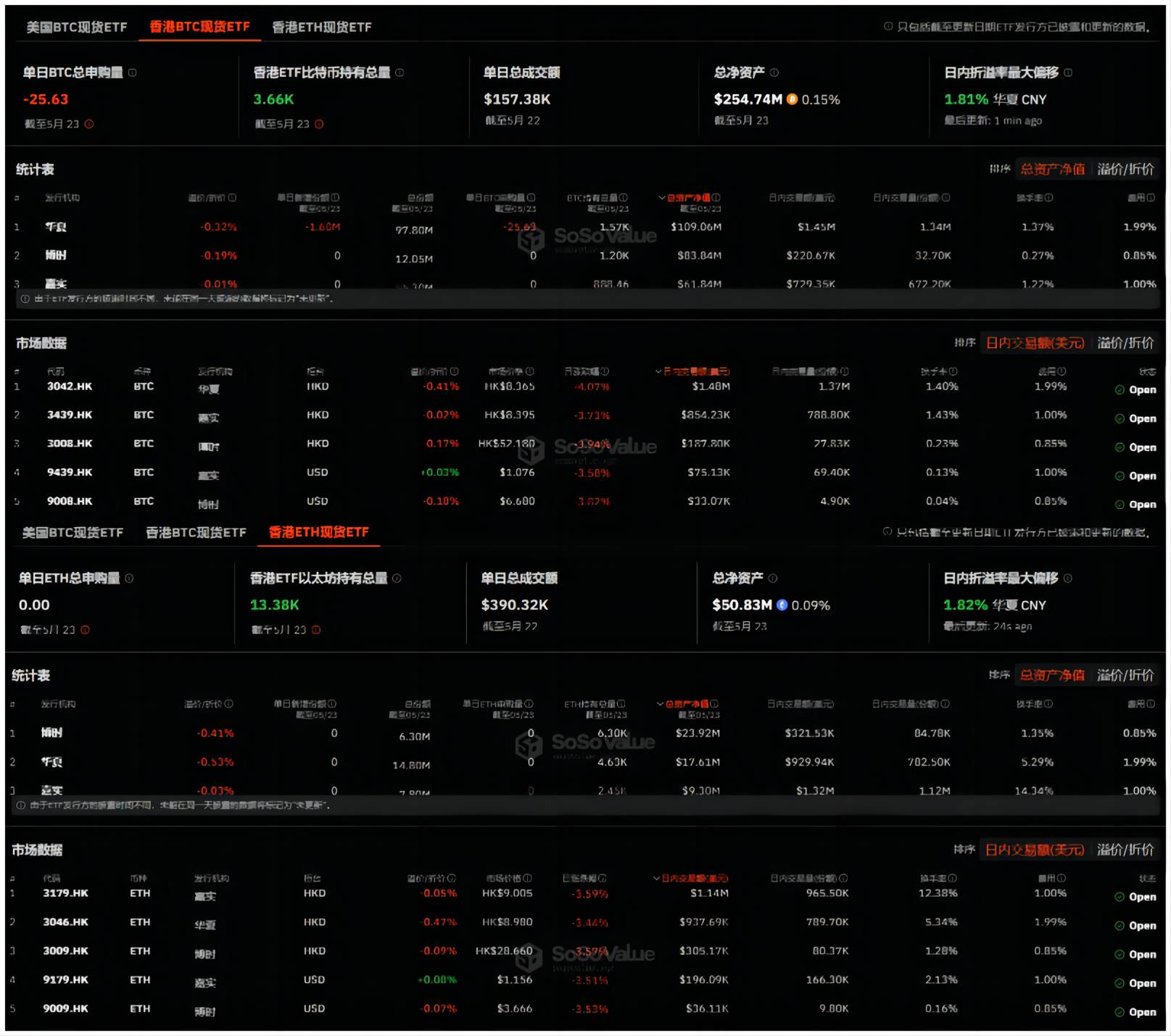

On April 30, six virtual asset spot ETFs officially debuted on the Hong Kong Stock Exchange (HKEX): Bosera HashKey Bitcoin ETF (3008.HK), Bosera HashKey Ether ETF (3009.HK), CSOP Bitcoin ETF (3042.HK), CSOP Ether ETF (3046.HK), Harvest Bitcoin Spot ETF (3439.HK), and Harvest Ether Spot ETF (3179.HK).

Judged by initial figures, the debut issuance size of the three Bitcoin spot ETFs reached $248 million on April 30 (with Ethereum spot ETFs raising $45 million), significantly surpassing the ~$125 million initial size of U.S. spot Bitcoin ETFs on January 10 (excluding Grayscale). This indicates strong market expectations for Hong Kong's crypto ETFs.

Criticism toward these six Hong Kong crypto ETFs has largely centered on their comparatively "weak" trading volumes relative to their U.S. counterparts: On their first trading day, total volume across all six Hong Kong crypto ETFs amounted to HK$875.8 million (~$112 million), with the three Bitcoin ETFs contributing HK$675 million—less than 1% of the U.S. spot Bitcoin ETFs’ first-day volume of $4.6 billion.

Trading volumes subsequently declined further, dropping below $1 million on May 23.

However, it is important to note that Hong Kong crypto ETF trading volumes have shown a clear inverse relationship with assets under management (AUM): As of May 23, 2024, the total AUM of the six Hong Kong virtual asset spot ETFs exceeded $300 million. Specifically, Bitcoin spot ETFs held 3,660 BTC with a net asset value of $254 million, while Ether spot ETFs held 13,380 ETH valued at $50.83 million—both showing slight increases since launch.

While $250 million pales in comparison to the ~$57.3 billion AUM of U.S. spot Bitcoin ETFs, this overlooks a critical structural difference—the sheer size disparity between the Hong Kong and U.S. ETF markets. The total size of Hong Kong’s ETF market is approximately $50 billion, whereas the U.S. ETF market stands at around $8.5 trillion—about 170 times larger.

Therefore, in relative terms, $250 million represents 0.5% of Hong Kong’s ETF market, compared to 0.67% for U.S. Bitcoin ETFs within the much larger American market. These proportions are not vastly different, especially considering the Hong Kong products have been live for less than a month—highlighting their significant impact on the local financial ecosystem.

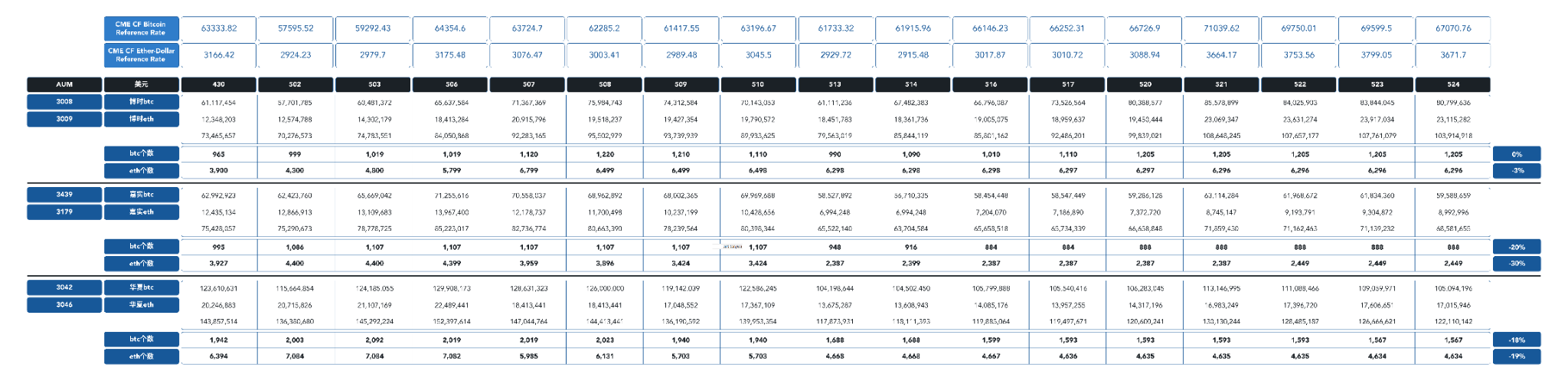

Looking deeper into internal data changes over the past month, a shifting dynamic among CSOP, Harvest, and Bosera HashKey has emerged:

CSOP and Harvest have seen noticeable declines in BTC and ETH holdings, while Bosera HashKey has gained momentum, achieving over $100 million in AUM—more than one-third of the total—and growing by $30 million since launch. Bosera HashKey now leads in ETH holdings and ranks second in BTC, narrowing the gap with CSOP from over a thousand BTC initially to fewer than 500 BTC.

The "Sweet Dilemma" Behind the Unexpected Approval

Data doesn't lie. The divergence between trading volume and AUM growth reflects an underlying structural trend—key stakeholders are actively refining processes and resolving bottlenecks.

Reflecting on the pace at which Hong Kong regulators approved and launched six crypto ETFs simultaneously, the prevailing market reaction was “expected, yet surprising”:

-

Expected because, since Hong Kong’s government began embracing virtual assets and Web3 in 2022, supportive policies and regulatory frameworks have steadily advanced—including the long-awaited crypto asset ETFs. Stakeholders had already begun intensive preparations;

-

Surprising because most expected approvals in Q3 or later, allowing gradual refinement of operational workflows and technical integrations. Instead, the government accelerated the process in April, far exceeding market expectations. As a result, institutions prioritized filing submissions, leaving original deployment plans misaligned.

In short, key players front-loaded application efforts, but left unresolved critical aspects such as operations, distribution channels, and product design—now requiring post-launch “catch-up.” This has led to several visible “sweet dilemmas.”

One must also acknowledge Hong Kong’s pioneering in-kind subscription/redemption model for crypto ETFs (i.e., coin-based subscriptions), allowing investors to directly use Bitcoin and Ethereum to subscribe to ETF shares. Investors can use BTC/ETH to purchase ETF units and redeem them in cash; conversely, cash subscriptions allow redemptions in BTC/ETH. For example, each share of Bosera HashKey’s 3008.HK represents 1/10,000 of a BTC, and each share of 3009.HK represents 1/1,000 of an ETH.

-

Participating Dealers (PDs): CMBI Securities, Mirae Asset Securities, Victory Securities, and eSecurities

-

Market Makers: Eclipse Options (HK) Limited, Jane Street Asia Trading Limited, Optiver Trading Hong Kong Limited, Vivienne Court Trading Pty. Ltd.

This innovative mechanism enables bidirectional flow between digital and traditional assets, but involves coordination among multiple stakeholders:

-

Participating Dealers (PDs), selected by ETF issuers (Bosera HashKey, CSOP, Harvest), responsible for creating new ETF units in the primary market. Current PDs include Victory Securities, CMBI, and eSecurities;

-

Brokers, through which retail investors trade ETF shares on the secondary market like stocks;

-

Custodians, responsible for securely holding the underlying crypto assets;

-

Market makers, providing liquidity by continuously quoting buy/sell prices in the secondary market.

Thus, seamless integration among PDs, brokers, custodians/exchanges, and market makers is essential to unblock the entire transaction pipeline.

For instance, using Bosera HashKey’s coin-based subscription process illustrated above:

-

Investors must first open an account with a PD;

-

Submit an ETF share creation instruction within a specified timeframe;

-

Transfer coins to the PD, which are then held in custody by HashKey Custody;

-

Hong Kong Securities Clearing Company (HKSCC) creates ETF shares and delivers them to the PD, who forwards them to brokers;

-

Retail investors can then trade these shares via their brokerage accounts.

This process involves numerous integration points: KYC information exchange between PDs and brokers, primary market subscription execution, coordination between PDs and custodians, and connectivity between PDs and brokers. These remain current pain points, causing many investors—especially institutional ones—to remain cautious. This creates a negative feedback loop: low trading volume → slow arbitrage activity → persistently low volume.

Nevertheless, improvements are underway. The steady growth in AUM over the past month serves as clear evidence.

Crypto ETFs May Need Another Two Months to Gain Momentum

From this perspective, Hong Kong’s crypto ETFs still require time to mature. Based on current developments, it may take another 1–2 months to fully optimize operational workflows, distribution channels, and technical integrations.

So, what positive changes might we expect in the Hong Kong crypto ETF landscape two months from now?

First, as operational and technical processes improve, more PDs and brokers will join the ecosystem, bringing with them large client bases that can serve as seeds for user growth—dramatically expanding reach and accessible capital pools, thereby enhancing the long-term potential of Hong Kong’s crypto ETFs.

Second, traditional financial institutions that are currently观望 (on hold), needing more time to evaluate, could begin launching leveraged products, lending services, asset management offerings, and other derivatives based on ETFs—enabling financial innovation previously impossible with direct BTC holdings, and meeting diverse investor demands for crypto exposure.

These developments can reinforce each other, forming a virtuous cycle: broader participation from PDs and brokers drives greater financial innovation around ETFs, while new structured products and derivatives based on spot ETFs unlock fresh opportunities in Hong Kong’s market.

Additionally, another major variable deserves attention: For institutional investors, Hong Kong’s spot Ether ETFs now offer a strategic window to “front-run” U.S. ETF launches.

Although the SEC has approved 19b-4 filings for eight spot Ethereum ETFs, the final green light remains pending. Market consensus suggests formal launches are still 1–2 months away.

During this interim period, institutions interested in spot Ether ETFs—particularly those aiming to position ahead of anticipated inflows and a potential surge in ETH prices—can leverage Hong Kong’s secure and compliant channel to gain early exposure, securing a first-mover advantage on a near-certain alpha opportunity.

Conclusion

In Samuel Beckett’s *Waiting for Godot*, Godot symbolizes hope and a better future. For today’s Hong Kong crypto ETFs, the awaited “Godot” is the full optimization and alignment among all parties involved in the trading infrastructure.

Behind the inverted trend of volume and AUM, stakeholders are actively streamlining processes and removing friction. Two months from now may mark the true inflection point when Hong Kong ETFs finally gain traction and enter their real opening phase.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News