Oil Price Surpasses $100—Who Is Reaping This “War Dividend”?

TechFlow Selected TechFlow Selected

Oil Price Surpasses $100—Who Is Reaping This “War Dividend”?

Every major wealth transfer begins with a sharp surge in oil prices.

Author: David, TechFlow

Today, Brent crude oil surged past USD 110 per barrel, while WTI crude broke above USD 100.

You should know that the last time oil prices crossed USD 100 was in March 2022—during the Russia-Ukraine war.

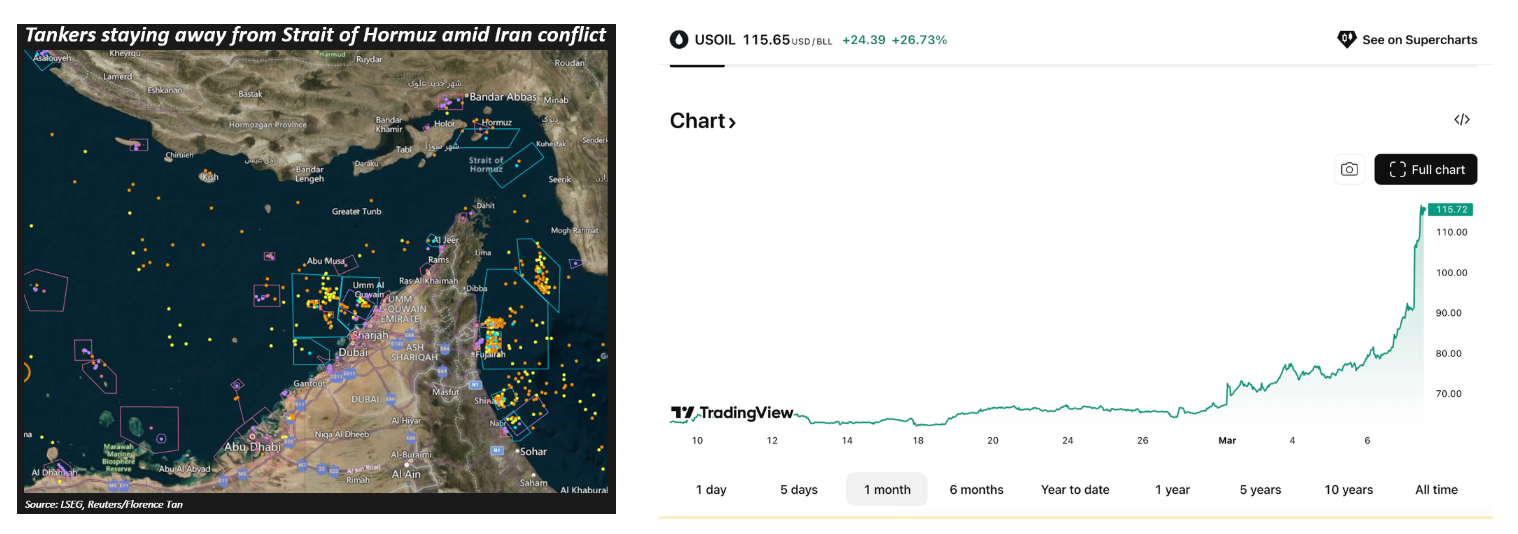

This time, it’s Iran. U.S.-Israeli airstrikes, the killing of Ayatollah Khamenei, and the de facto closure of the Strait of Hormuz. One-fifth of the world’s seaborne oil passes through this waterway—its daily transit volume has plummeted from over 100 vessels to just a handful.

Source: TradingView

With oil unable to be shipped out, storage tanks are filling up—and Iraq, Kuwait, and the UAE have all begun shutting wells and cutting output. Qatar’s global-largest LNG export facility has halted operations.

U.S. crude oil prices rose 35% in one week—the largest single-week gain since futures trading began in 1983. Qatar’s Energy Minister warned that if the situation persists, oil prices could reach USD 150.

For ordinary people, these figures may still feel remote. But tonight at 24:00 (midnight), China’s retail fuel price adjustment window opens. The price of 92-octane gasoline will rise by CNY 0.39 per liter—filling a standard 50-liter tank will cost an extra CNY 20. This marks the fourth consecutive increase this year.

Yet gas stations are merely the first link in the chain you’ll personally feel.

When Middle Eastern Straits Get Blocked, Dongguan’s Zhangmutou Gets Clogged

Three hundred oil tankers are backed up in the Strait of Hormuz—8,000 kilometers away, trucks are jammed bumper-to-bumper in Zhangmutou, Dongguan.

Petroleum isn’t just gasoline. It’s the lifeblood of the entire industrial system—plastics, synthetic fibers, rubber, fertilizers: all are downstream products of oil.

Once the strait is blocked and oil prices surge, the ripple effect from the Middle East to South China takes only days.

According to Southern Finance, over the past week, a buying frenzy erupted at Zhangmutou—the largest plastic raw materials distribution hub in South China. Online, images titled “Massive traffic jams at Zhangmutou Plastic Trading Market” went viral.

This market, with nearly CNY 100 billion in annual transaction volume, saw buyers rush in en masse amid fears of further price hikes. Large trucks queued up to haul raw materials, clogging roads around the market. The largest plastic e-commerce platform crashed temporarily; its 90,000-square-meter public warehouse neared full capacity; workers labored overtime for several days to clear space.

Source: Southern Finance Network

Meanwhile, on-site trading rules shifted: quotes are valid only for the day; payment must be received before shipment; verbal pre-orders are no longer accepted. Prices change hourly.

How steep is the surge?

Polycarbonate (PC)—used in smartphone cases and car headlights—has jumped from a low of CNY 10,000 per ton last year to CNY 14,000 per ton—a 40% weekly gain. BASF, one of the world’s largest chemical companies, announced price hikes for plastic additives of up to 20%.

Upstream petrochemical firms have suspended sales and imposed strict quotas. Downstream factories hesitate to accept current prices—but fear tomorrow’s will be even higher.

The logic is straightforward:

Rising oil prices push up chemical feedstock costs, which drive up plastic pellet prices, ultimately raising the cost of the smartphone case in your hand, the running shoes on your feet, or the PET water bottle on your desk. From oil well to retail shelf, this chain is far shorter than most realize. Gas stations are simply the first link you feel—not the last.

The last time we saw such rapid price surges was during the 2022 Russia-Ukraine war.

That year, oil prices also breached USD 100, sparking a full-year inflationary spiral and sending global stock markets tumbling from January to December. Many still recall 92-octane gasoline hitting CNY 9 per liter.

Some Fill Up Their Tanks—Others Fill Up Their Portfolios

At 24:00 tonight, China’s retail fuel price adjustment window opens. 92-octane gasoline is expected to rise by CNY 0.39 per liter; 95-octane by CNY 0.41 per liter. Filling a 50-liter tank of 92-octane will cost an extra CNY 20—the fourth consecutive hike this year.

Tomorrow morning, you’ll pay more at the pump. But today, as markets opened, others were already counting their gains.

On March 2nd and 3rd, PetroChina, Sinopec, and CNOOC achieved back-to-back涨停 (limit-up) sessions—the first time in history all three “major oil companies” did so simultaneously. Of the 48 oil-and-gas stocks, 28 hit daily limits; the entire sector turned red.

PetroChina’s market cap surpassed CNY 2.4 trillion, reclaiming the top spot among A-share listings.

In fact, the “Big Three” have been rising quietly for three years. PetroChina is up 210% since early 2023; CNOOC, 232%.

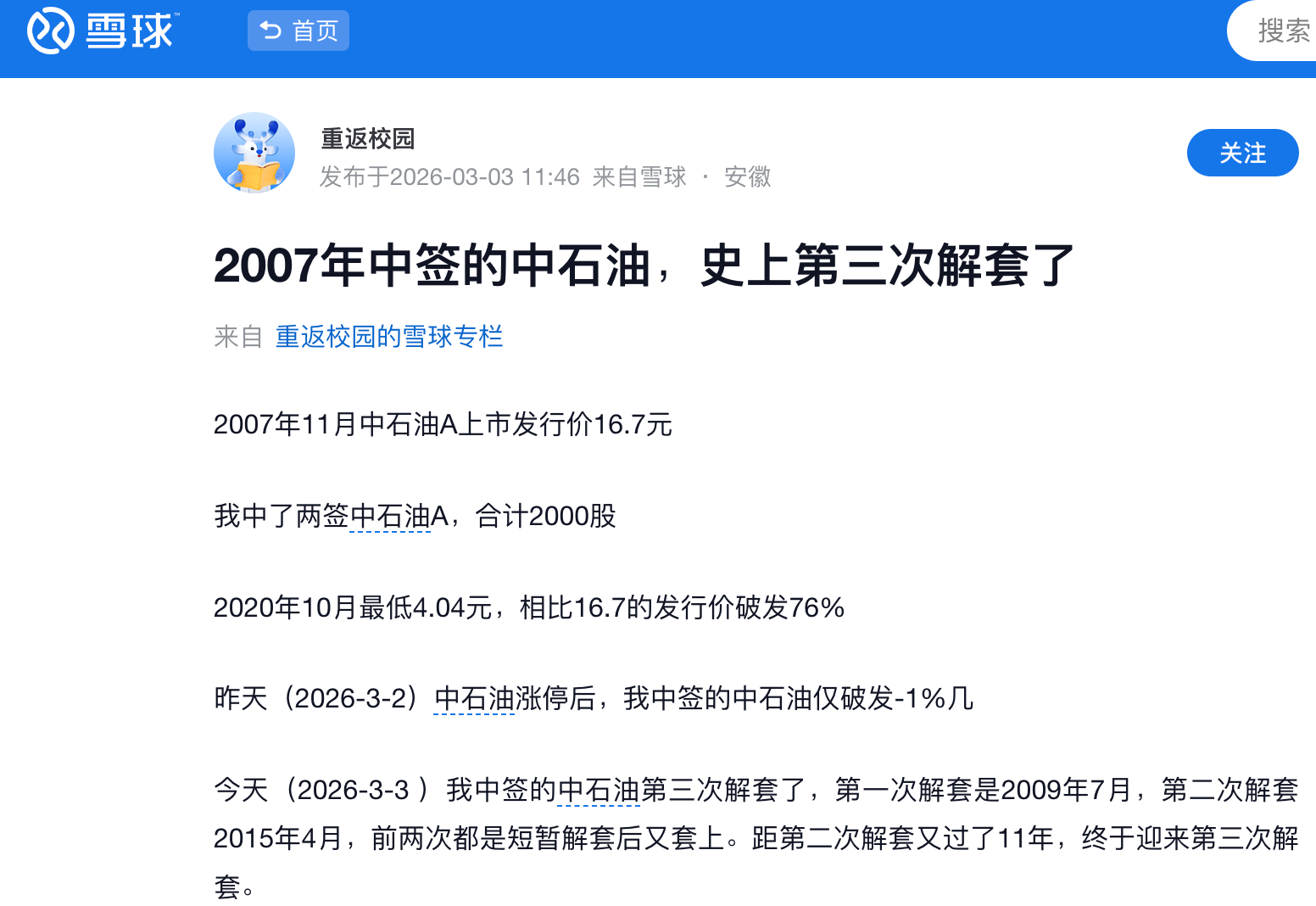

But this three-year rally has been slow and steady—so quiet that most investors didn’t notice. Retail investors who bought PetroChina at its IPO price of CNY 48 in 2007—trapped for nearly two decades—have gradually recouped losses during this prolonged, muted uptrend.

War acts like kicking a slow-burning fuse straight into a powder keg.

The chemical sector follows the same script.

Funds began flowing in last year: assets under management (AUM) in chemical-themed ETFs ballooned from CNY 2.5 billion to CNY 25.7 billion—tenfold growth in one year. Once hostilities erupted, momentum accelerated sharply: main funds poured CNY 31.3 billion into chemicals over five trading days; chemical ETFs saw single-day net subscriptions exceeding 300 million shares.

On the oil-and-gas ETF front, over CNY 8 billion has flowed in this year alone, prompting multiple fund managers to file applications for new oil-and-gas thematic products.

A slow burn for a year—then war triggers a sprint.

Move one step further downstream, and financial markets are asking the same questions as Zhangmutou’s plastic traders. On March 3rd, the front-month plastic futures contract surged 6%; polypropylene (PP) futures hit the daily limit intraday.

Futures are rising—and so are spot prices. Traders are hoarding inventory, and some investors are quietly positioning themselves in plastic-related equities.

Thus, some hoard plastic raw materials to capture arbitrage spreads; others trade plastic futures to profit from volatility; still others buy chemical-sector ETFs… Every node along the chain hosts active bets.

Those who held the “Big Three” for three years likely bet on long-term structural shifts in China’s energy mix—seeking steady, certain returns. Those rushing in post-war are betting on something entirely different: that the conflict won’t end soon, and oil prices still have room to climb.

Panic and speculation often manifest as the same action. The same barrel of oil represents a cost to you—and a profit to someone else. The difference lies solely in where you stand along the chain.

Those filling up their tanks hope it ends quickly. Those adding positions hope it drags on.

New Opportunities Lie Beyond the Old Strait

Historically, every oil-price crisis reshapes value distribution across the supply chain.

2022 offers a textbook case. When oil prices breached USD 100, upstream oil producers reaped immediate gains—a pattern repeating today. Yet the true structural winners emerged in a sector few paid attention to then:

New-energy vehicles (NEVs).

When 92-octane gasoline hit CNY 9 per liter, the operating cost of fuel-powered vehicles spiked—prompting mass consumer recalculations of total ownership costs between ICE and electric vehicles.

NEV penetration was already trending upward, propelled by policy subsidies, technological progress, and expanding charging infrastructure. But the 2022 oil shock acted as a direct catalyst—pushing hesitant observers to become actual buyers.

Today’s situation bears striking parallels.

Oil prices breaking USD 100 again triggers the most instinctive response: capital flooding into oil and chemical sectors. Yet zooming out to a two- to three-year horizon, what truly matters may not be who profits from this round—but rather, which substitution-driven demand will accelerate.

Over the past three decades, the operation of global manufacturing and trade systems rested on several implicit assumptions: abundant energy supply, secure shipping lanes, highly globalized supply chains…

The Strait of Hormuz disruption may stem from war—but the underlying geographic vulnerability remains unchanged. Every energy-linked participant is now forced to reassess its risk exposure.

Every newly recalculated cost equation spawns a new business opportunity: alternative energy, alternative materials, alternative shipping routes, localized supply chains… The very idea of “oil independence” is rapidly evolving into a massive industry.

Will oil prices fall back? I believe they likely will—Iran itself ships 90% of its oil exports through the Strait; prolonged closure would starve its own economy.

Yet every spike leaves behind durable changes. Recalculated equations won’t be forgotten; rebuilt supply chains won’t be dismantled.

An oil price above USD 100 doesn’t just raise your fuel bill—it reshapes how everyone calculates costs.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News