Bitget UEX Daily Report | U.S.-Iran Talks Reach Impasse; Trump Says Ceasefire Between Lebanon and Israel to Be Extended; Intel’s Earnings Exceed Expectations

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | U.S.-Iran Talks Reach Impasse; Trump Says Ceasefire Between Lebanon and Israel to Be Extended; Intel’s Earnings Exceed Expectations

Overall, the peak of geopolitical uncertainty may have passed, but energy price volatility will continue to affect corporate earnings and the inflation trajectory. Investors are advised to seek structural opportunities aligned with the long-term trends in AI and semiconductors.

Author: Bitget

I. Key News Highlights

Federal Reserve Updates

Fed Pressures Wall Street to Support New Capital Rules

- Federal Reserve Vice Chair for Supervision Michael Barr met with CEOs of major banks—including JPMorgan Chase and Goldman Sachs—in early April, explicitly urging the industry to assess the proposed new capital rules from a holistic perspective rather than continuing to seek additional exemptions.

- The proposal overall lowers capital requirements for banks; the feedback period, expected to conclude in mid-June, is likely to focus on constructive input, with major revisions deemed unlikely.

- Market Impact: This move may ease tensions between regulators and banks, providing short-term confidence support to the financial sector. However, if final capital requirements remain binding, long-term profitability for large banks will still face pressure.

International Commodities

Escalating U.S.-Iran Tensions Push Oil Prices Higher; Gold Retreats Under Pressure

- Trump claimed he had “fully closed” the Strait of Hormuz until Iran reaches an agreement and ordered the sinking of any mine-laying vessels; Iran activated its Tehran air defense system to intercept “hostile targets,” causing negotiations to stall.

- Crude oil surged over 5% intraday and closed up more than 3%; Brent crude hit its highest level in over two weeks. Gold fell over 1%, hitting a fresh daily low.

- Market Impact: Geopolitical risk provides short-term support to energy prices, but prolonged deadlock could further amplify inflationary pressures and dampen global growth expectations.

Macroeconomic Policy

U.S. April Manufacturing PMI Hits Nearly Four-Year High; Resurgent Inflation Deepens Fed’s Dilemma

- Initial jobless claims for the week ending April 18 stood at 214,000, slightly above the forecast of 210,000; the prior week’s figure was revised upward from 207,000 to 208,000.

- Manufacturing PMI rose to 54; Composite PMI climbed to 52; Services PMI stood at 51.3—indicating modest overall economic expansion.

- Growth was primarily driven by tariff-related precautionary inventory buildup—not genuine demand—and price increases for both goods and services reached their highest since July 2022.

- Market Impact: The coexistence of weak demand and rising inflation significantly raises the bar for Fed rate cuts; markets must continue monitoring upcoming data to validate economic resilience.

II. Market Recap

Commodities & FX Performance

- Spot Gold: Up 0.27%, trading near $4,700;

- Spot Silver: Up 0.14%, trading near $75;

- WTI Crude: Up 0.98%, at $96.75;

- Brent Crude: Up 1.09%, at $106.22;

- U.S. Dollar Index: Accelerated upward to 98.81, reaching a two-week high.

Cryptocurrency Performance

- BTC: Down 0.04%, trading near $78,378;

- ETH: Down 1.67%, trading near $2,333;

- Total Cryptocurrency Market Cap: Slightly declined 0.2% to $2.7 trillion;

- Liquidations: Total 24-hour liquidations amounted to ~$204 million, with long positions accounting for $126 million;

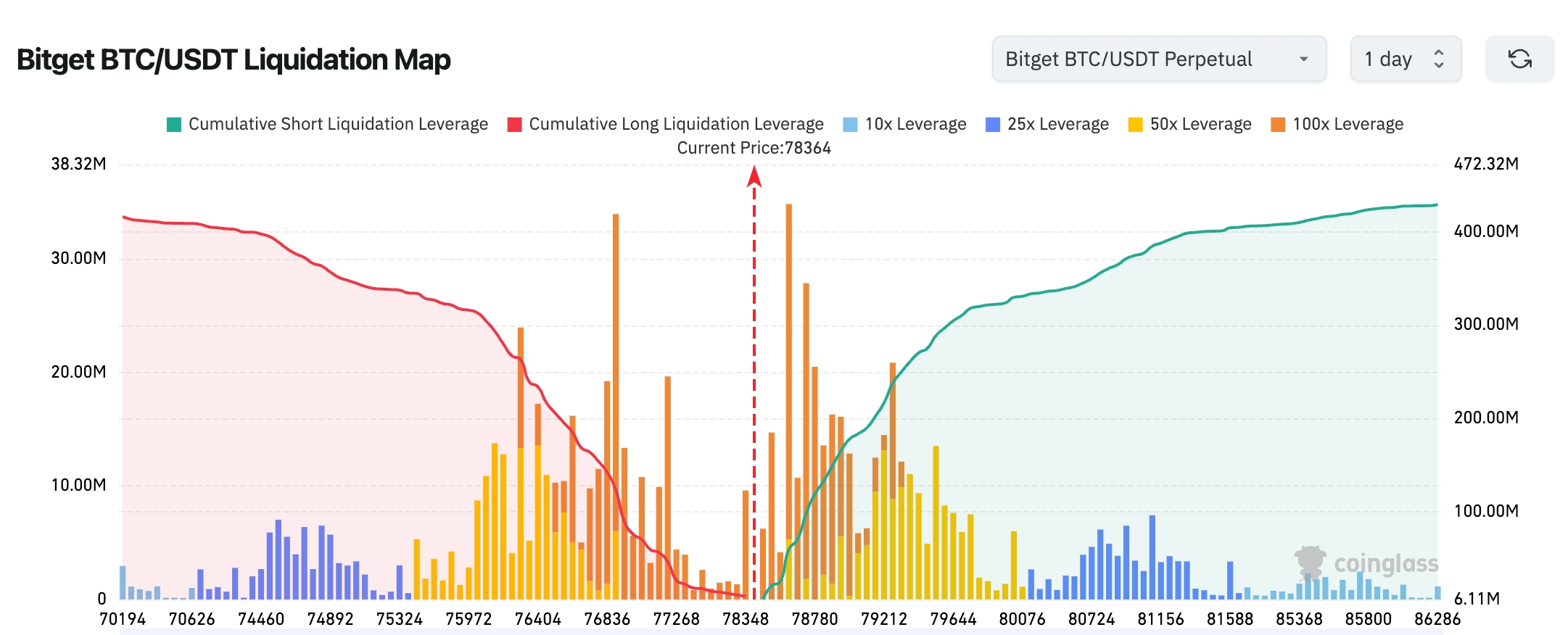

- Bitget BTC/USDT Liquidation Map: Current price sits around $78,364. A large volume of long liquidations (red) below $77,000 has already been absorbed, while dense short liquidations are stacked in the $78,500–$80,000 zone—providing short-term upward “short-squeeze” potential. Additionally, high-leverage positions (50x/100x) are heavily concentrated near $78,000–$79,000, indicating exceptionally high volatility risk in this range. A breakout could amplify momentum, but reversals may trigger rapid liquidations.

- Spot ETF Net Flows: BTC spot ETFs recorded a modest net inflow of $55.8 million yesterday; ETH spot ETFs saw a net outflow of $54.9 million;

- BTC Spot Flows: $2.355 billion inflow vs. $2.395 billion outflow yesterday, resulting in a net outflow of $40 million.

U.S. Equity Index Performance

- Dow Jones Industrial Average: Down 0.36%, closing at 49,310.32, weighed down by software stocks;

- S&P 500: Down 0.41%, closing at 7,108.40, well off recent record highs;

- Nasdaq Composite: Down 0.89%, closing at 24,438.50, with tech stocks diverging amid geopolitical tensions.

Tech Giants’ Updates

- Intel (INTC): +2.31% ($66.78), surged nearly 20% after hours following Q1 revenue and guidance that vastly exceeded expectations;

- Tesla (TSLA): -3.56% ($373.72), pulled back as investors took profits following raised full-year capital expenditure guidance;

- Microsoft (MSFT): -3.97% ($415.75), dragged down by broader weakness across the software sector;

- Apple (AAPL): +0.30% ($273.99), largely insulated from geopolitical risks;

- Amazon (AMZN): -0.11% ($255.08), adjusted in line with broader market trends;

- NVIDIA (NVDA): -1.41% ($199.64), while the chip sector remained broadly strong;

- Alphabet (GOOGL): +0.37% ($340.59); intensified AI competition remains a key driver—semiconductor stocks extended gains led by strong earnings from Intel and Texas Instruments, whereas software stocks faced collective pressure due to concerns over AI-driven business model transformation.

Sector Movement Observations

Software Sector Led Declines

- Key Stocks: ServiceNow down nearly 18%; Salesforce down nearly 9%

- Drivers: Large contracts impacted by Middle East conflict, compounded by AI’s disruption of traditional software models—investors express concern over long-term growth narratives

Semiconductor Sector Gained Nearly 2%

- Key Stocks: Texas Instruments up 19%; Intel surged over 20% after hours

- Drivers: Robust quarterly results and guidance, sustained strong demand from data centers extending the sector’s winning streak

III. In-Depth Stock Analysis

1. Salesforce (CRM) – Renewed Concerns Over AI Disruption to Software Business Models

Event Summary: Salesforce shares plunged nearly 9%. Although the company is poised to post one of its fastest revenue growth rates in years, investors worry that rapidly evolving AI tools will reshape traditional software sales—from “feature-based seat licenses” to “productivity-based units.” Goldman Sachs research indicates software firms are attempting to tap into larger labor budget allocations, yet short-term transition pains are evident. Market Interpretation: Institutions broadly view this shift as positive for long-term SaaS valuations, but current investor focus remains on near-term execution risks. Investment Insight: As AI reshapes the software landscape, companies with clear pathways to productivity-driven monetization are best positioned to lead the transition.

2. Intel (INTC) – Q1 Earnings and Guidance Both Beat Expectations

Event Summary: Intel surged nearly 20% after hours. Q1 revenue of $1.36 billion exceeded expectations, and strong Q2 guidance pointed to 22% growth in data center business. The semiconductor index has now posted its longest-ever 17-session winning streak. Market Interpretation: Institutions expect continued recovery in chip demand, with Intel’s strategic positioning in AI servers gradually bearing fruit. Investment Insight: Earnings season continues delivering highlights—the semiconductor sector’s fundamentals remain robust, offering compelling valuation-recovery opportunities.

3. Tesla (TSLA) – Raised Full-Year Capital Expenditure Guidance

Event Summary: Tesla fell over 3% after raising its 2026 capital expenditure outlook, signaling aggressive investment in future growth. Market Interpretation: Analysts view the increased spending as a near-term headwind but a long-term tailwind for autonomous driving and energy business expansion. Investment Insight: Elevated capex reflects management confidence; investors should closely monitor execution progress and tangible outcomes.

4. Texas Instruments (TXN) – Q1 Results Vastly Exceed Expectations

Event Summary: TXN reported Q1 revenue of $4.83 billion, up 19% YoY; EPS of $1.68, up 31% YoY—both substantially surpassing analyst estimates. Strong demand for analog chips and data center applications drove growth, pushing the stock up nearly 19% on the day. Market Interpretation: Institutions believe the semiconductor cycle’s recovery remains intact, with TXN’s entrenched leadership in industrial and analog chips allowing it to fully benefit. Investment Insight: Semiconductor demand recovery is unequivocal; companies with diversified application exposure possess resilient fundamentals.

IV. Cryptocurrency Project Updates

1. Ben Slavin, Global ETF Head of Asset Services at BNY Mellon, stated that Bitcoin ETF annual fund flows have turned positive. Twelve spot Bitcoin ETFs collectively recorded over $335 million in net inflows on a single day, over $2.1 billion monthly, and approximately $1.8 billion year-to-date and over the past three months.

2. Nikolaos Panigirtzoglou, analyst at JPMorgan, noted that persistent DeFi security vulnerabilities and sluggish growth continue to constrain institutional interest in the DeFi space. The Kelp DAO-related exploit caused roughly $20 billion in total value locked (TVL) to evaporate from DeFi within days; attackers minted $292 million in uncollateralized rsETH tokens and borrowed real ETH on Aave, resulting in approximately $230 million in bad debt.

3. 3F, a treasury protocol built on Morpho, announced completion of a $4 million funding round: a $750,000 pre-seed round launched in July 2025 and closed in November 2025, followed by a $3.3 million seed round launched in November 2025 and closed in March 2026. Maven 11 led the seed round.

4. Chun Wang, co-founder of F2Pool, tweeted that he received 83.7 million SPK rewards from Spark over the past year, which he exchanged via CoWSwap for 663 ETH and ~$1.4 million in cash—expressing regret over having sold all of it.

5. According to Iranian media outlet Fars News, reports claiming Iran intends to collect tolls for passage through the Strait of Hormuz in cryptocurrency are inaccurate.

V. Today’s Market Calendar

Data Release Schedule

Upcoming Key Events

- Event: U.S. University of Michigan Consumer Sentiment Index—Monitor inflation expectations and consumer resilience

Institutional Views:

Leading investment bank analysts generally agree that yesterday’s modest pullback in U.S. equities reflected stalled U.S.-Iran negotiations. Software sector corrections highlight growing pains in AI-driven business model transitions, while the semiconductor sector’s 17-session rally underscores fundamental resilience. Oil prices strengthened short-term due to geopolitical risk, while gold weakened; risk assets like Bitcoin moved in tandem with U.S. equities. Analysts note that April’s PMI data reveals inventory-driven growth masking underlying demand softness, and rebounding inflation has further delayed Fed rate cut expectations. Markets await next week’s consumer sentiment data to validate economic resilience. Overall, peak geopolitical uncertainty may have passed, yet energy price volatility will continue influencing corporate earnings and inflation trajectories. Investors are advised to seek structural opportunities aligned with long-term AI and semiconductor trends, while maintaining close watch on developments in the Middle East.

Disclaimer: The above content was compiled via AI search and verified manually before publication. It does not constitute any investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News