SEC Drops Case, CZ Granted Pardon, Sun Yuchen Reaches Settlement: Trump’s Crypto Business Is Going Stronger Than Ever

TechFlow Selected TechFlow Selected

SEC Drops Case, CZ Granted Pardon, Sun Yuchen Reaches Settlement: Trump’s Crypto Business Is Going Stronger Than Ever

Trump’s crypto project benefits from regulatory tailwinds.

Author: CryptoSlate

Translated by TechFlow

TechFlow Intro: This article does not merely report on Justin Sun’s $10 million settlement with the SEC. Instead, it situates that settlement within a broader policy landscape—namely, the systemic retreat of SEC enforcement pressure against major crypto players since Donald Trump assumed office. And the biggest beneficiary of this regulatory ebb is none other than Trump’s own token and stablecoin initiatives. Using quantifiable metrics ($802 million in revenue; $4.4 billion USD1 circulating supply), the article maps the transmission mechanism linking regulatory shifts to private gain—a must-read for anyone tracking the trajectory of U.S. crypto regulation.

Full Text Below:

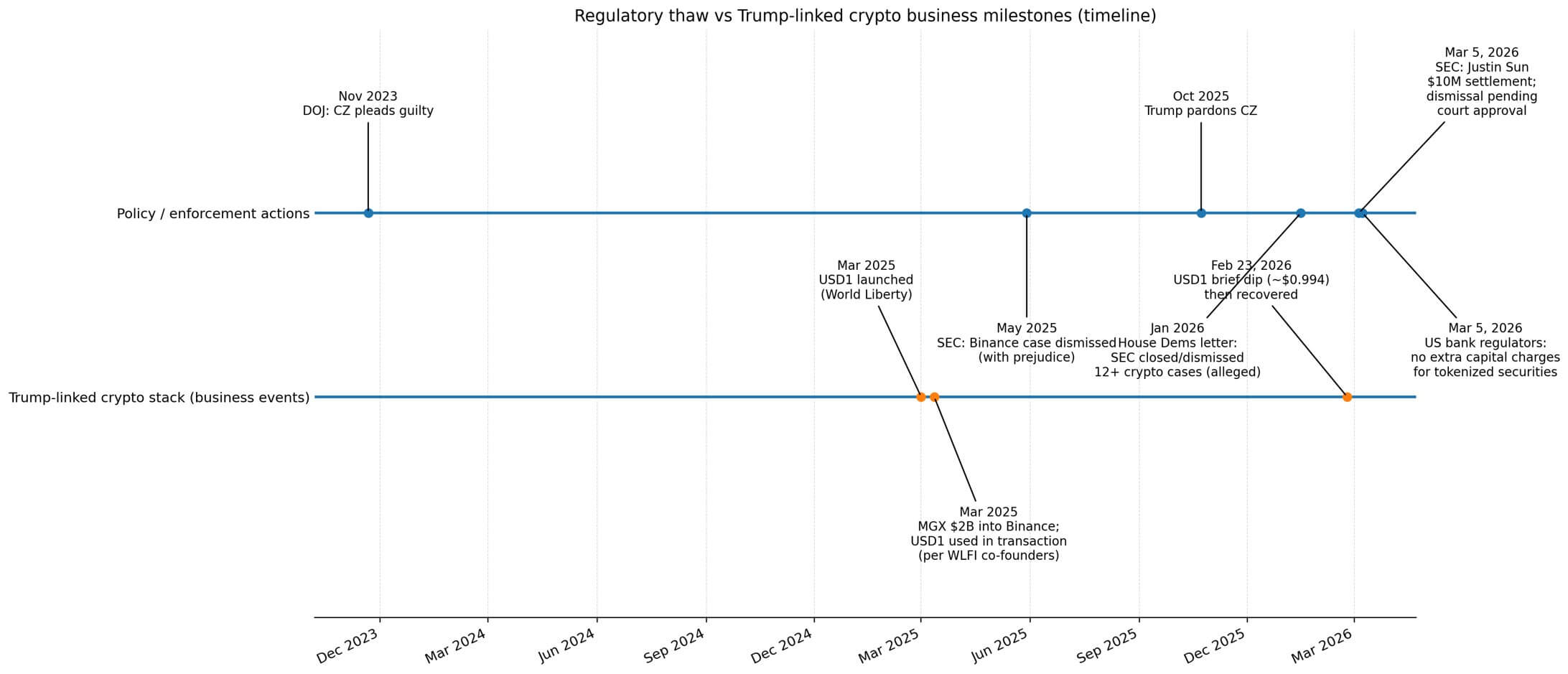

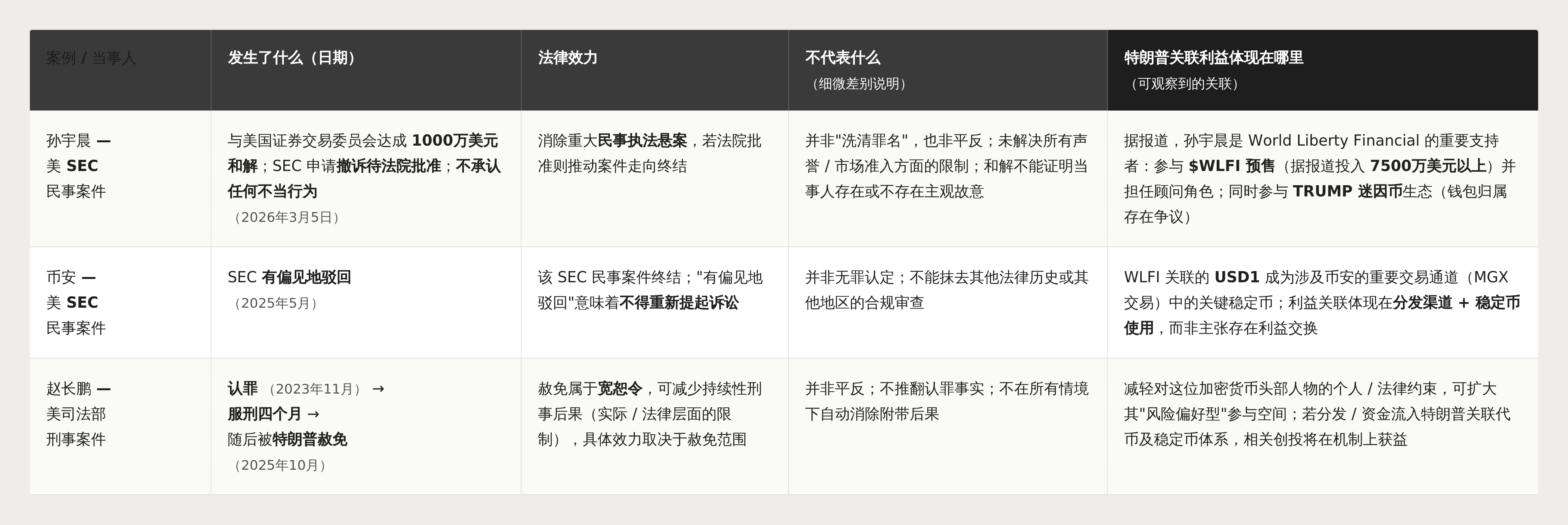

On March 5, Justin Sun settled a civil fraud lawsuit with the SEC for $10 million, resolving allegations that he earned $31 million through artificial trading volume and undisclosed celebrity promotions.

The settlement requires court approval and includes no admission of wrongdoing; the case will accordingly be dismissed.

On the same day, U.S. banking regulators announced that banks holding tokenized securities face no additional capital requirements beyond those applicable to traditional securities. This technology-neutral classification removes another brick from the wall of crypto regulation.

Sun’s settlement coincides precisely with the one-year anniversary of regulatory retrenchment under the Trump administration.

In May 2025, the SEC’s civil suit against Binance was dismissed with prejudice—meaning it cannot be refiled. In October 2025, Trump pardoned Binance founder Changpeng Zhao (“CZ”), who had pleaded guilty in November 2023 to anti-money laundering and unlicensed money transmission charges, paid billions in fines, and served four months in prison.

In January 2026, a bipartisan letter signed by Democratic members of the House Financial Services Committee noted that the SEC has withdrawn or terminated at least twelve crypto-related cases since January 2025.

The beneficiaries extend beyond the U.S. crypto market as a whole. Trump’s own crypto ecosystem has quietly taken position—and stands ready to capture outsized private gains from the distribution channels and commercial relationships controlled by these entrepreneurs.

The Token Economics of Proximity to the Presidency

In less than a year, two globally prominent crypto entrepreneurs have each escaped major U.S. legal constraints.

Sun’s settlement ends the civil fraud case—but is not an acquittal. Binance’s SEC civil suit was dismissed with prejudice. CZ’s pardon constitutes judicial clemency—not a reversal of his guilty plea.

Meanwhile, crypto projects linked to the Trump family have become direct beneficiaries of the crypto market’s renewed vitality.

Reuters estimates that the Trump Organization generated $802 million from crypto-related activities in the first half of 2025 alone—outpacing all other business lines—with World Liberty Financial’s token economics accounting for the largest share.

World Liberty’s white paper stipulates that, after deducting operating expenses, 75% of token sale proceeds flow to Trump-family entities. Its stablecoin component, USD1—launched in March 2025—adds another revenue stream via yield generated from reserve collateral. Reuters estimates that, at scale, USD1 could generate tens of millions of dollars annually.

Sun emerged as one of World Liberty’s most visible token buyers, investing at least $75 million into WLFI’s token presale and joining as an advisor.

He has also participated in the TRUMP Memecoin ecosystem. Reports link an “SUN” wallet and HTX-related activity to large holdings—though ultimate ownership remains contested.

Binance’s intersection with the Trump crypto ecosystem occurs via another channel: MGX—a firm backed by Abu Dhabi—invested $2 billion in Binance in March 2025, marking the largest institutional transaction in crypto history.

A co-founder of World Liberty confirmed that USD1 was used in that MGX–Binance transaction.

Reports found that when USD1’s total circulating supply stood at roughly $2.1 billion, a single wallet held approximately $2 billion worth of USD1—highlighting how a single pipeline dominated early supply.

By February 2026, per Artemis data, USD1 had grown into the sixth-largest stablecoin, with a circulating supply of ~$4.4 billion.

On February 23, USD1 briefly dipped to ~$0.994. World Liberty attributed the move to a “coordinated attack” on its X account—but the peg quickly recovered.

USD1’s early supply was highly concentrated within the MGX–Binance channel; subsequent growth created a distribution advantage that directly monetizes World Liberty’s revenue structure.

The Feedback Loop from Policy to Profit

This commercial architecture means: enforcement retreat and increasingly permissive regulatory guidance jointly reduce friction.

Reduced friction drives increased activity—and increased activity enables monetization of Trump-linked tokens and stablecoins.

Trump need not personally engineer regulatory outcomes to become their largest private beneficiary. The overlap is mechanical: when participants controlling distribution channels—such as Binance’s listing capacity or Sun’s investment power—see legal pressure lifted, projects capturing newly active participants benefit. And World Liberty’s token and stablecoin structure sits precisely atop those critical nodes.

Stablecoins have evolved from niche crypto infrastructure into macro-level collateral. A February 2026 working paper from the Bank for International Settlements (BIS) finds that a two-standard-deviation net inflow of dollar-pegged stablecoins lowers three-month Treasury yields by roughly 2.5–3.5 basis points—and up to 5–8 basis points during periods of Treasury scarcity.

Stablecoin growth now generates measurable demand for safe assets, embedding these instruments directly into interest-rate and Treasury-market plumbing.

A European Central Bank (ECB) working paper documents a “deposit-substitution mechanism”: stablecoin adoption reduces retail deposits, constraining bank intermediation activity.

Eurozone evidence provides a rigorous analytical framework for U.S. banks’ opposition to stablecoin interest-bearing functionality—a stance that directly mirrors the current legislative impasse. The Clarity Act remains stalled, primarily due to bank resistance to interest-bearing stablecoins (fearing accelerated deposit outflows) and unresolved controversy over ethics and anti-money laundering provisions tied to Trump-linked projects.

Per DeFiLlama data, stablecoins’ total market cap stands at ~$313 billion, up 3.7% over the past 30 days. Even absent new legislation, the U.S. is functionally lowering operational costs for crypto businesses—and Trump’s crypto ecosystem has positioned itself as the “toll booth” for distributing that growth.

Second-Order Beneficiaries and Structural Constraints

The first-order private beneficiaries are Trump’s crypto network. The second-order public beneficiaries are the U.S. crypto market writ large—lower enforcement risk premiums, accelerated product launches, and more U.S.-focused projects going live.

This distinction matters because it separates correlation from causation—without ignoring the observable direction of benefits. Settlements are not acquittals; dismissals with prejudice are not reversals of fact; pardons are acts of clemency—not factual repudiations of guilt.

Even without proving a direct causal link between enforcement outcomes and private commercial ties, distribution and revenue outcomes remain visible and quantifiable.

SEC Chair Paul Atkins stated in February 2026 that, following prior White House–directed staff reductions, the agency is now rehiring—and responded to accusations that the SEC’s crypto case withdrawals were politically motivated by noting that many decisions predated his tenure.

This thaw extends beyond individuals. U.S. regulators now tend to grant “exemptive relief” for tokenized securities experiments, whereas the UK favors sandbox mechanisms—a divergence creating cross-border friction even amid overall U.S. regulatory openness.

The next constraint may not be legal—but legislative and political.

Banks view stablecoins as threats to deposits. Ethics clauses in proposed legislation could structurally limit the scale of Trump-linked projects—even as markets expand—or prove toothless, enabling faster expansion.

Entrepreneurs who have already achieved civil exoneration or criminal pardons still face reputational and market-access constraints should future enforcement agencies adopt harder stances.

Regulatory pressure can reemerge—not as pure legal risk, but as policy risk.

Why This Matters

The concentration of benefits accruing to Trump’s crypto projects raises conflict-of-interest concerns—no proof of quid pro quo required.

Revenue-sharing arrangements, stablecoin reserve yields, and distribution touchpoints all appear in public filings and reporting. Policy shifts—reduced enforcement intensity, progressive guidance, civil dismissals, and pardons—have reduced friction.

The private capture of that friction reduction is most evident where token economics and stablecoin growth translate directly into presidential-linked income.

Trump need not be the *largest* beneficiary of regulatory retreat. His status as a beneficiary is empirically observable.

As Trump-era regulators lift legal pressure on top crypto figures, the clearest private upside accrues to Trump’s own token and stablecoin infrastructure—while the broader U.S. market serves as the second-order beneficiary. This pattern holds regardless of intent—and the numbers make it unmistakably clear.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News