Understanding EigenLayer: What Are LST, LRT, and Restaking?

TechFlow Selected TechFlow Selected

Understanding EigenLayer: What Are LST, LRT, and Restaking?

To determine whether restaking is a panacea or a poison, one must fully understand it in order to reach an objective conclusion.

Authors: Baiding & Jomosis, Geek web3

Editor: Faust

Introduction: Restaking and Layer2 are two pivotal narratives within the Ethereum ecosystem in this cycle. Both aim to address existing issues with Ethereum, but their approaches differ in key aspects. Compared to technically complex mechanisms like ZK or fraud proofs, restaking primarily empowers downstream projects economically. While it may appear as simply incentivizing users to stake assets for rewards, its underlying mechanics are far more sophisticated.

In essence, restaking is a double-edged sword—empowering the Ethereum ecosystem while simultaneously introducing significant risks. Opinions on restaking remain divided: some view it as an innovation bringing liquidity and vitality to Ethereum, while others see it as overly profit-driven and accelerating the collapse of the crypto market.

Undoubtedly, determining whether restaking is a panacea or a poison requires understanding what it does, why it exists, and how it operates—only then can we form an objective and clear evaluation, which is also crucial for assessing the value of its associated tokens.

When discussing restaking, Eigenlayer is an unavoidable case study. Understanding Eigenlayer’s function equates to understanding restaking itself. This article uses Eigenlayer as an example to clearly explain its business logic and technical implementation, analyzing the technological and economic impacts of restaking on the Ethereum ecosystem and Web3 as a whole.

Understanding Restaking and Related Terms

As widely known, restaking refers to "re-staking," originating from the Ethereum ecosystem and gaining popularity after Ethereum's transition to Proof-of-Stake (PoS) in 2022. But what exactly is "re-staking"? To properly contextualize restaking, let us first review three foundational concepts: PoS, LSD, and Restaking.

1. POS (Proof of Stake)

Proof of Stake, or "staking-based consensus," is a mechanism that probabilistically allocates block validation rights based on the amount of staked assets. Unlike Proof of Work (PoW), which distributes validation rights according to computational power, POS is generally considered less decentralized and less aligned with permissionless ideals than PoW.

On September 15, 2022, the Paris upgrade activated, marking Ethereum’s official shift from PoW to PoS through the merge of the mainnet and beacon chain. The Shanghai upgrade in April 2023 enabled PoS validators to withdraw their staked assets, signaling the maturity of the staking model.

2. LSD (Liquid Staking Derivatives Protocol)

It's well-known that Ethereum’s PoS staking yields attractive returns, yet retail investors often struggle to access these benefits. Aside from hardware requirements, two main barriers exist:

First, validator deposits must be in multiples of 32 ETH—a threshold beyond most individual investors' reach.

Second, prior to the Shanghai upgrade in April 2023, staked ETH could not be withdrawn, resulting in poor capital efficiency.

To address these issues, Lido emerged. It introduced pooled staking—essentially “group staking with shared profits.” Users deposit ETH into Lido, which aggregates these funds to operate Ethereum validators, solving the accessibility issue for small investors.

Moreover, users receive stETH tokens at a 1:1 ratio when depositing ETH into Lido. These stETH tokens are redeemable for ETH at any time and can serve as ETH equivalents in major DeFi platforms such as Uniswap and Compound, enabling participation in various financial activities. This resolves the low capital utilization problem inherent in traditional PoS staking.

Since PoS involves locking highly liquid assets for mining rewards, products like Lido are referred to as "Liquid Staking Derivatives" (LSD). As mentioned above, stETH is a Liquid Staking Token (LST).

Notably, ETH staked in PoS protocols represents real, native assets—actual value—while derivative tokens like stETH are synthetically created. In effect, stETH leverages ETH’s value to effectively duplicate purchasing power—one asset becomes two—which mirrors the concept of "financial leverage" in economics. Leverage isn't inherently good or bad; its impact depends on the economic context and cycle. Crucially, LSD introduces the first layer of leverage to the ETH ecosystem.

3. Restaking (Re-staking / Re-delegation)

As the name suggests, restaking involves using LST tokens as collateral to participate in additional PoS networks or blockchains, earning extra yield while enhancing the security of those networks.

After staking LST assets, users receive a 1:1 receipt token for circulation, known as a Liquid Restaking Token (LRT). For instance, staking stETH yields rstETH, which can also be used across DeFi and other on-chain applications.

In other words, the synthetic LST tokens (like stETH) generated by LSD are themselves re-staked, creating another layer of synthetic assets—LRTs—thus adding a second layer of leverage to the ETH ecosystem.

Now, a natural question arises: higher leverage increases systemic instability. While the first layer (LSD) solves real problems—retail access to staking and improved capital efficiency—what justifies this second layer? Why re-stake already synthetic tokens?

This requires examining both technical and economic dimensions. The following sections will briefly outline Eigenlayer’s architecture, analyze the economic implications of restaking, and provide a holistic assessment.

(At this point, several acronyms have been introduced, among which LSD, LST, and LRT are core concepts frequently referenced later. Let’s reinforce them: ETH staked natively in Ethereum PoS is the base asset; stETH, pegged to staked ETH, is an LST; rstETH, obtained by restaking stETH on a restaking platform, is an LRT.)

Eigenlayer’s Product Functionality

We must first clarify the core problem Eigenlayer aims to solve: providing Ethereum-grade economic security to platforms whose underlying security relies on PoS.

Ethereum boasts high security due to its massive staked asset base. However, off-chain services—such as Rollup sequencers or verification layers—are not directly secured by Ethereum.

To achieve sufficient security, such services would need to build their own AVS (Actively Validated Services)—middleware providing data or validation services to end-user applications like DeFi, gaming, or wallets. Examples include oracles offering price feeds and Data Availability Layers ensuring consistent state updates.

However, building new AVS is extremely difficult because:

1. High setup costs and long development timelines.

2. New AVS typically use project-native tokens for staking, which lack the robust consensus of ETH.

3. Participating in AVS staking forces validators to forgo stable returns from Ethereum staking, incurring opportunity cost.

4. Security levels of new AVS are far below Ethereum’s, making economic attacks cheaper.

A solution would be a platform allowing startups to rent Ethereum’s economic security directly—this is precisely what Eigenlayer offers.

Eigenlayer’s whitepaper, titled “The Restaking Collective,” highlights two key features: “Pooled Security” and “Free Market.”

Beyond native ETH staking, Eigenlayer aggregates staking receipts into a shared security pool. It attracts users seeking additional yield to re-stake their assets and then rents out this economic security to PoS-based projects—this is “Pooled Security.”

Unlike traditional DeFi systems with volatile and unpredictable APYs, Eigenlayer codifies reward and penalty rules via smart contracts, allowing stakers to freely choose participation terms. Earning rewards becomes a transparent market transaction rather than a gamble—this embodies the “free market” principle.

In this model, projects rent Ethereum-level security without building AVS from scratch, while stakers earn predictable yields. Thus, Eigenlayer enhances ecosystem security while delivering user incentives.

Eigenlayer’s security delivery process involves three roles:

-

Security providers — Stakers. They stake capital to supply security.

-

Security intermediaries — Operators. They manage stakers’ funds and execute tasks for AVS.

-

Security consumers — AVS (e.g., oracle middleware).

(Image source: Twitter @punk2898)

An analogy compares Eigenlayer to bike-sharing: Eigenlayer acts as the bike-sharing company managing assets (bikes = LSD), while users (riders = AVS) rent these assets to perform services, just as AVS rent LSD/LRT assets to gain validation and security.

In bike-sharing, deposits and penalties prevent misuse. Similarly, Eigenlayer uses staking and slashing mechanisms to deter malicious behavior by Operators.

EigenLayer Interaction Flow from a Smart Contract Perspective

Eigenlayer’s security model rests on two pillars: staking and slashing. Staking provides baseline security; slashing raises the cost of misbehavior.

The staking interaction flow is illustrated below.

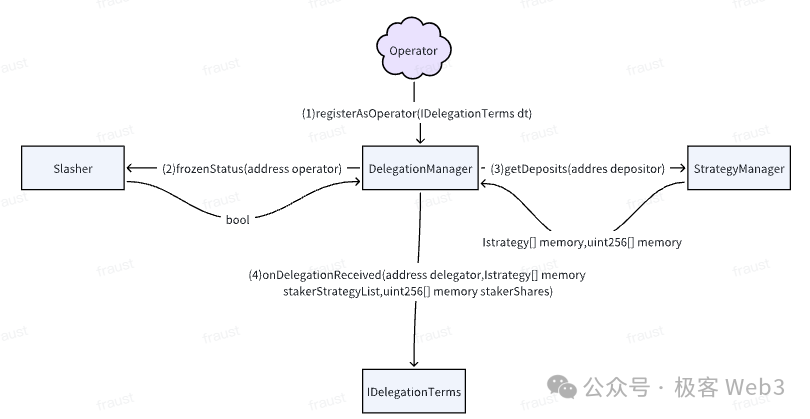

Within Eigenlayer, the primary contract interacting with stakers is the TokenPool contract. Stakers can perform two operations:

Stake — Deposit assets into the TokenPool contract and designate a specific Operator to manage them.

Redeem — Withdraw assets from the TokenPool.

Withdrawing funds involves three steps:

1) The staker submits a withdrawal request to a queue by calling the queueWithdrawal method.

2) The Strategy Manager checks whether the designated Operator is frozen.

3) If the Operator is not frozen (explained further below), the staker can initiate the complete withdrawal process.

Importantly, EigenLayer grants stakers full flexibility—they can either withdraw funds or convert them into new staking shares.

Stakers are categorized as regular stakers or Operators based on whether they personally run node infrastructure for AVS. Regular stakers supply PoS capital to AVS networks, while Operators manage pooled assets and participate in AVS operations to ensure network security—similar to Lido’s model.

Stakers and AVS are naturally disconnected parties—stakers often lack trust in or knowledge of AVS projects and cannot operate nodes directly, while AVS teams struggle to reach individual stakers. Operators bridge this gap.

On one hand, Operators manage stakers’ funds, benefiting from stakers’ trust—similar to trusting Lido or Binance. On the other, they operate nodes for AVS; if they act maliciously, they face slashing penalties, making dishonesty unprofitable. Thus, Operators act as trusted intermediaries between stakers and AVS.

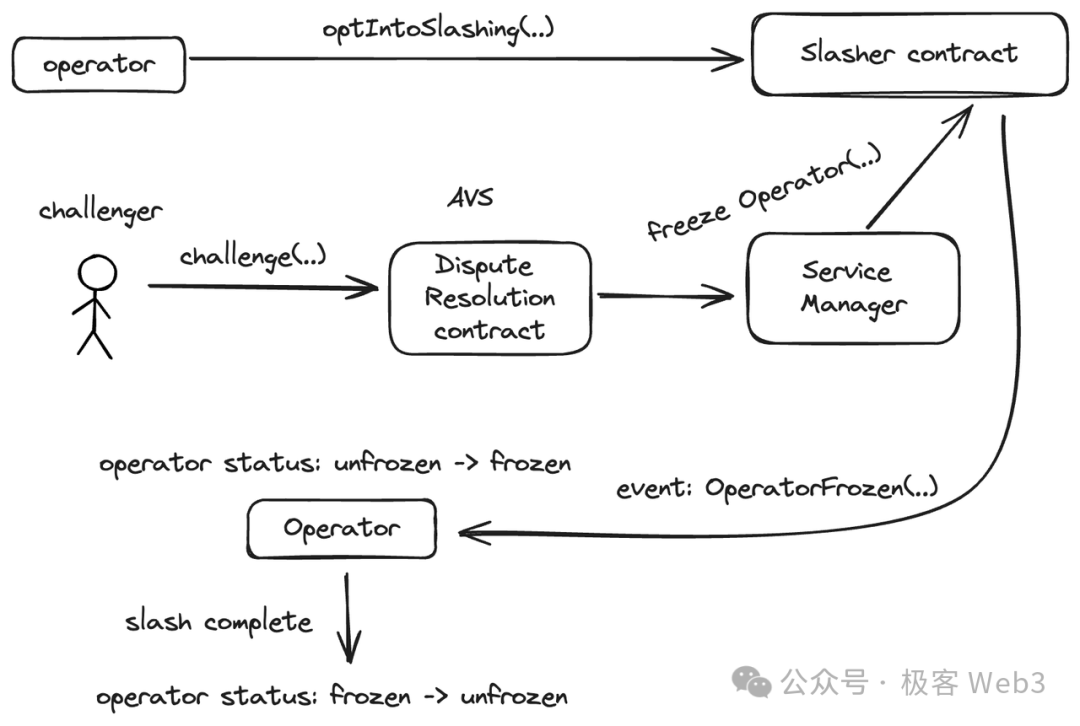

For an Operator to join Eigenlayer, they must first call the optIntoSlashing function in the Slasher contract, authorizing it to enforce penalties.

Next, the Operator registers via the Registry contract, which invokes functions in the Service Manager to record registration details and relay information back to the Slasher contract. Only after this process is the Operator fully registered.

Now consider the slashing mechanism. Among Restakers, Operators, and AVS, only Operators are direct targets of slashing. As noted, Operators must register with the Slasher contract to enable enforcement.

Besides Operators, several other actors are involved in slashing:

1. AVS: When engaging Operators, AVS defines slashing conditions and standards. Two critical contracts are involved: dispute resolution contract and Slasher contract.

The dispute resolution contract handles challenges; the Slasher contract freezes the Operator and executes slashing after the challenge window ends.

2. Challenger: Any participant on Eigenlayer can become a challenger. If they detect an Operator violating slashing conditions, they initiate a process similar to Optimistic Rollup fraud proofs.

3. Staker: Slashing an Operator also impacts corresponding stakers financially.

The slashing execution flow is as follows:

1) A challenger calls the challenge function in the AVS-specific Dispute Resolution contract.

2) If the challenge succeeds, the DisputeResolution contract calls ServiceManager’s freezeOperator function, triggering an OperatorFrozen event in the Slasher contract, changing the Operator’s status from unfrozen to frozen, initiating the slashing process. If the challenge fails, the challenger faces penalties to deter frivolous disputes.

3) After slashing concludes, the Operator’s status resets to unfrozen and resumes operation.

During slashing, the Operator remains in a frozen, inactive state. During this period, the Operator cannot manage staked funds, and stakers assigned to them cannot withdraw. Like a defendant awaiting trial, they are suspended until cleared. Only once unfrozen can normal interactions resume.

All Eigenlayer contracts follow this freezing principle. When stakers delegate funds to an Operator, the system checks the Operator’s status via isFrozen(); withdrawal requests also check this status. This ensures robust protection of AVS security and staker interests.

Finally, AVS do not obtain Ethereum security unconditionally. Although launching on Eigenlayer is easier than building AVS independently, attracting Operators and stakers still requires competitive APY offerings.

Economic Impact of Restaking on the Crypto Market

Restaking is undoubtedly one of the hottest narratives in the Ethereum ecosystem today. Given Ethereum’s dominant role in Web3 and the massive TVL accumulated by restaking projects, its influence on the crypto market is profound and likely to persist throughout this cycle. We can examine this from micro and macro perspectives.

Micro Impact

It's important to recognize that restaking brings both benefits and risks to different participants in the Ethereum ecosystem. The benefits include:

(1) Restaking strengthens the foundational security of downstream projects in the Ethereum ecosystem, benefiting their long-term development;

(2) Restaking unlocks liquidity for ETH and LST, improving capital efficiency and boosting ecosystem activity;

(3) High yields from restaking encourage more ETH and LST staking, reducing circulating supply and positively impacting token prices;

(4) Attractive yields draw more capital into the Ethereum ecosystem.

At the same time, restaking introduces significant risks:

(1) In restaking, a single IOU (instrument of obligation) may be pledged across multiple projects. Without proper coordination, this can over-amplify the perceived value of the IOU, leading to credit risk. For example, if multiple projects simultaneously demand redemption of the same IOU, it cannot satisfy all claims. A failure in one project could trigger cascading failures across others.

(2) A large portion of LST liquidity is locked. If LST prices are more volatile than ETH and users cannot exit quickly, they may suffer losses. Additionally, AVS security depends on TVL—high LST volatility threatens AVS stability.

(3) Restaking funds are ultimately held in smart contracts, often in vast amounts. This concentration creates a single point of failure—if exploited, the losses could be catastrophic.

Microeconomic risks can be mitigated through parameter adjustments and rule modifications, though detailed mitigation strategies are beyond the scope of this article.

Macro Impact

Crucially, restaking is fundamentally a form of multi-layered leverage. Since crypto markets are highly cyclical, understanding restaking’s macro impact requires analyzing the relationship between leverage and market cycles. Restaking adds two layers of leverage to ETH’s economy, as previously explained:

First layer: LSD doubles the effective value of staked ETH and its derivatives.

Second layer: Restaking doesn’t only involve ETH—it includes LSTs and LP tokens, which are synthetic instruments, not real ETH. Therefore, LRTs generated by restaking are assets built on top of leverage—constituting a second layer.

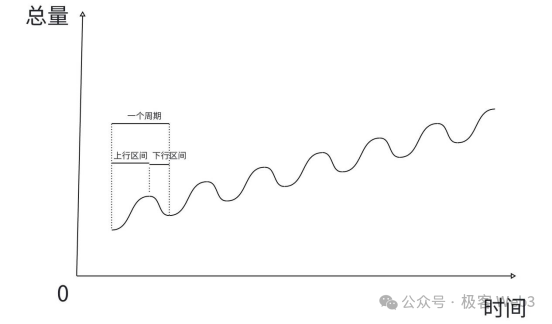

So, is leverage beneficial or harmful to an economic system? Conclusion: leverage must be evaluated within the context of cycles. During bull markets, leverage accelerates growth; during bear markets, it accelerates collapse.

Economic development follows cycles—rising periods inevitably lead to downturns, and vice versa. Over time, total economic output grows in a spiral pattern, with each cycle bottoming higher than the last. Currently, the crypto market follows a clear four-year Bitcoin halving cycle: the first 2–3 years post-halving typically see bull markets, followed by bearish phases.

However, while Bitcoin halvings correlate with market cycles, they aren’t the root cause. The true driver is the buildup and collapse of leverage. Halvings merely catalyze capital inflows and leverage formation.

How does leverage drive market cycles? If everyone knows leverage eventually collapses, why adopt it during upswings? The answer lies in universal economic principles. Just as in traditional economies, leverage is inevitable—and necessary.

During expansions, rapid productivity leads to surplus goods. To circulate these goods, sufficient money supply is needed. While money can be printed, unchecked issuance causes hyperinflation. Yet insufficient supply stifles demand and slows growth. So what’s the solution?

If money can’t be infinitely expanded, capital efficiency must increase. Leverage achieves this by amplifying the utility of each unit of capital. Example: $1M buys a house, $100k a car. With 60% loan-to-value mortgage, you can borrow $600k against your house. Without leverage, $1M buys one house or ten cars. With leverage, you can buy one house and six cars—effectively spending $1M as $1.6M.

Without leverage, limited money supply suppresses consumption, demand stagnates, profits shrink, and innovation slows. With leverage, spending and growth surge. Is this a bubble? Yes—but during bull runs, abundant external capital enters, preventing immediate collapse—much like long positions in futures during a bull market rarely get liquidated.

But during downturns? Capital absorbed by leverage eventually dries up. Asset values fall—your $1M house may drop below $1M, triggering margin calls. Across the system, widespread liquidations abruptly shrink available capital, causing rapid contraction. Compare spot trading (value drops) vs. leveraged positions (complete wipeout). Hence, in bear markets, leverage ensures faster, deeper collapses.

Macroscopically, leverage is inevitable—even if destined to burst. It is neither purely good nor bad—it depends on the phase of the cycle. Regarding restaking’s macro impact: leverage within ETH’s ecosystem plays a crucial role in amplifying market cycles. Its emergence is inevitable. Each cycle sees leverage manifest differently—DeFi Summer was fueled by LP token yield farming, driving the 2021 bull run. Today, restaking may be the catalyst. Though mechanisms differ, the economic essence is identical: leveraging incoming capital to meet liquidity demands.

Based on the above analysis, this multi-layered leverage via restaking may accelerate the current bull market’s ascent and extend its peak, while also intensifying the subsequent bear market’s decline, triggering broader cascading effects with greater overall impact.

Conclusion

Restaking is a secondary derivative of PoS. Technically, Eigenlayer leverages restaked value to secure AVS, using staking and slashing mechanisms to enforce accountability—"borrow responsibly, repay reliably." The withdrawal waiting period allows thorough operator behavior verification and prevents sudden mass withdrawals that could destabilize the system.

From a market perspective, impacts should be analyzed micro- and macro-economically: Microscopically, restaking enhances liquidity and yields for the Ethereum ecosystem but introduces manageable risks through parameter tuning. Macroeconomically, restaking represents multi-layered leverage, intensifying the cyclical dynamics of the crypto economy—amplifying both booms and busts. It likely contributes significantly to the eventual bursting of this cycle’s leverage and the transition into a bear market. This macroeconomic effect aligns with fundamental economic laws—it cannot be prevented, only anticipated and navigated.

We must clearly understand restaking’s broad implications—leveraging its benefits during upswings while preparing psychologically and strategically for leverage unwind and market downturns during contractions.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News