An analysis of the impact of Hong Kong's spot crypto ETFs from supply and demand perspectives

TechFlow Selected TechFlow Selected

An analysis of the impact of Hong Kong's spot crypto ETFs from supply and demand perspectives

But in the medium to long term, the in-kind creation and redemption mechanism of Hong Kong's crypto ETFs provides a pathway for crypto assets to be converted into traditional financial assets.

Author: Tom Analysis, Resident Researcher at SoSoValue

The Hong Kong Securities and Futures Commission (SFC) has officially released the approved list of spot virtual asset ETFs, including Bitcoin and Ethereum spot ETFs from China Asset Management (Hong Kong), Harvest Fund International, and Bosera International. These six spot ETF products opened for subscription from April 25 to 26 and were listed on the Hong Kong Stock Exchange (HKEX) on April 30.

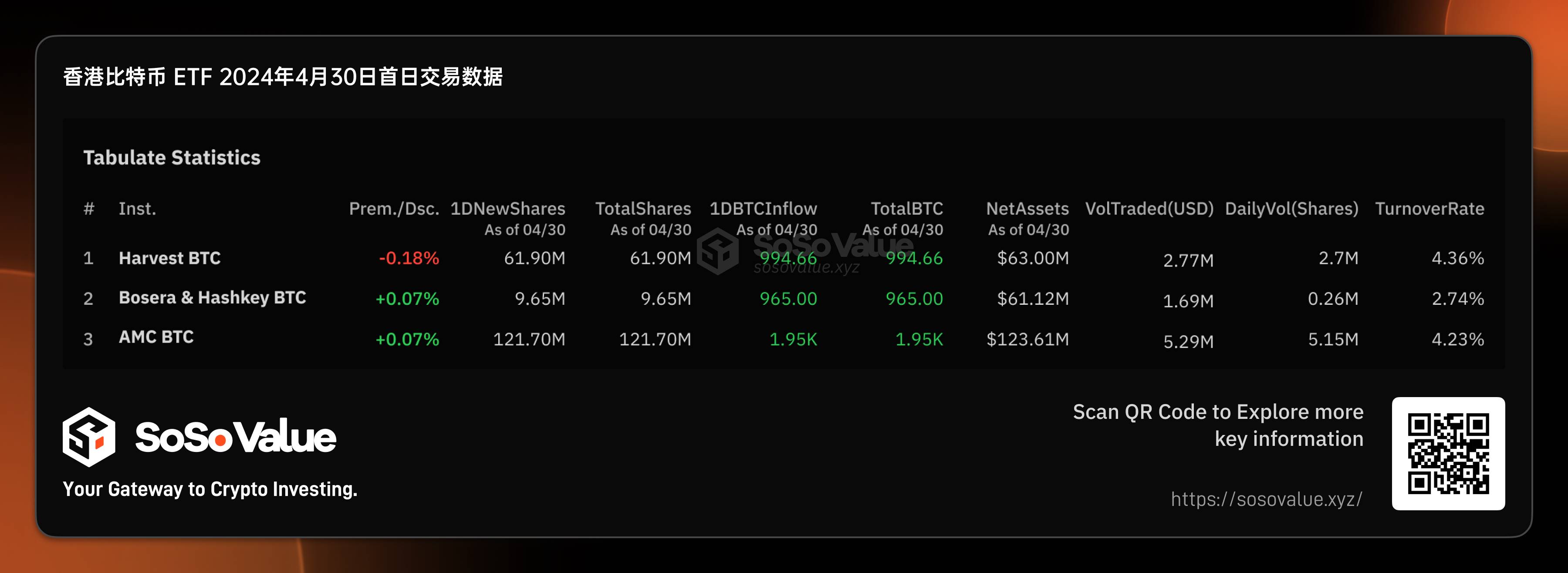

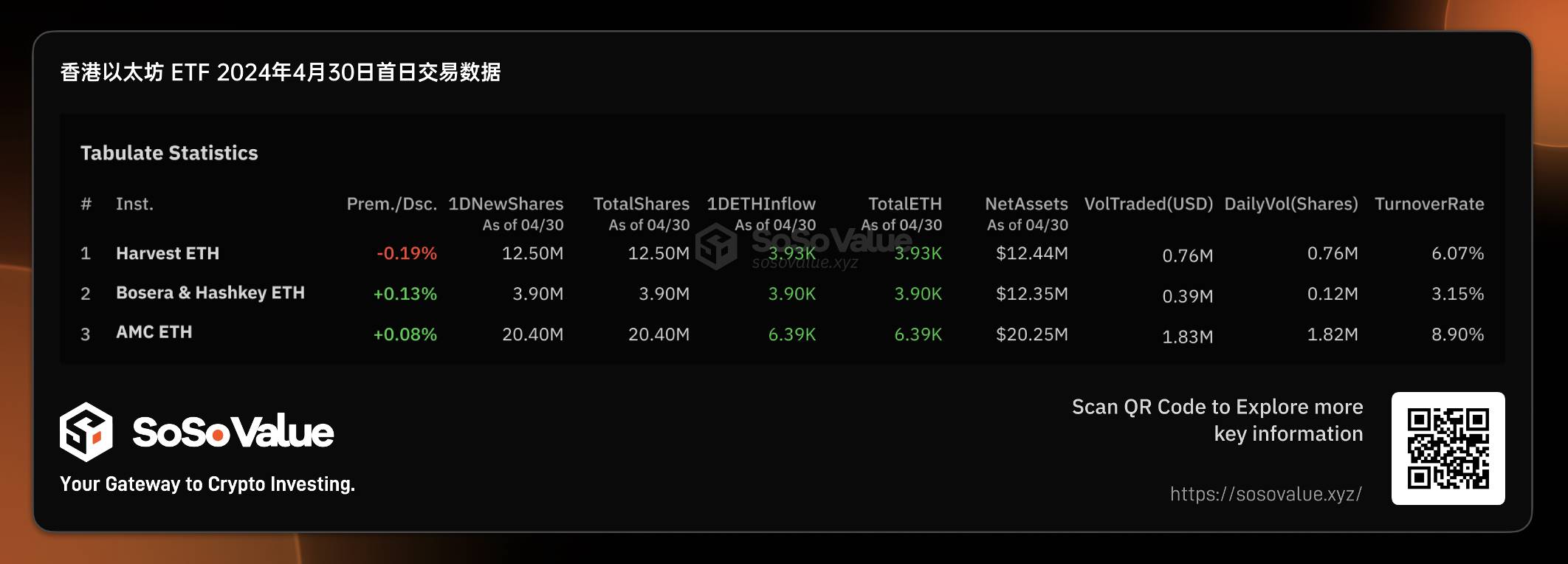

Through initial subscriptions, these six Hong Kong spot ETFs achieved strong starting scales. According to SoSo Value data, the net asset value (NAV) of the three Bitcoin ETFs totaled $248 million, while the three Ethereum ETFs reached $45 million, amounting to nearly $300 million in total—surpassing the first-day combined NAV of $130 million for U.S. spot Bitcoin ETFs (excluding Grayscale’s GBTC, which transitioned from a trust to an ETF).

However, in terms of first-day trading volume, Hong Kong's crypto ETFs significantly lagged behind their U.S. counterparts. Data from SoSo Value shows that the six Hong Kong crypto ETFs recorded only $12.7 million in trading volume on their debut day (April 30), far below the $4.66 billion traded by U.S. ETFs on their first listing day.

We observe a significant mismatch between initial规模 and first-day trading volume for Hong Kong crypto ETFs. How large can these Hong Kong spot ETFs ultimately grow? What impact will they have on the broader crypto market, and how should investors position themselves accordingly? The editor analyzes these questions through the lens of supply and demand dynamics in Hong Kong’s ETF market.

Figure 1: Overview of Hong Kong Spot Crypto ETF Data (Source: SoSo Value)

Demand Side: Exclusion of Mainland Chinese RMB Investors Limits Incremental Capital, Leading to Lower Trading Volumes

Eligibility for investing in these Hong Kong crypto ETFs remains strictly limited—Mainland Chinese investors are currently barred from participation. For example, Futu Securities requires account holders to be non-Mainland and non-U.S. residents to trade these products. The anticipated flow of Mainland capital via southbound Stock Connect channels is not permitted and is unlikely to be enabled in the near or medium term.

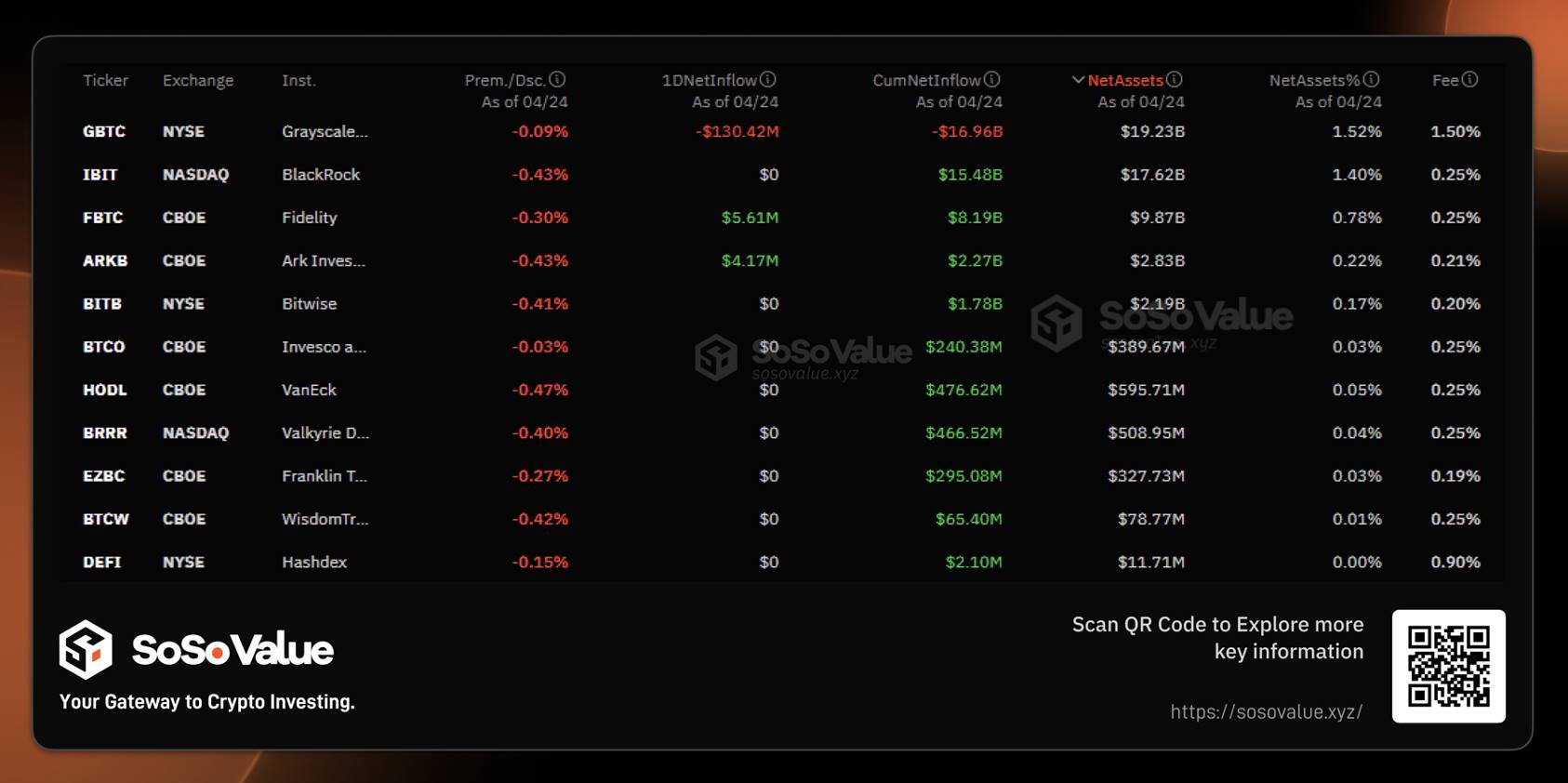

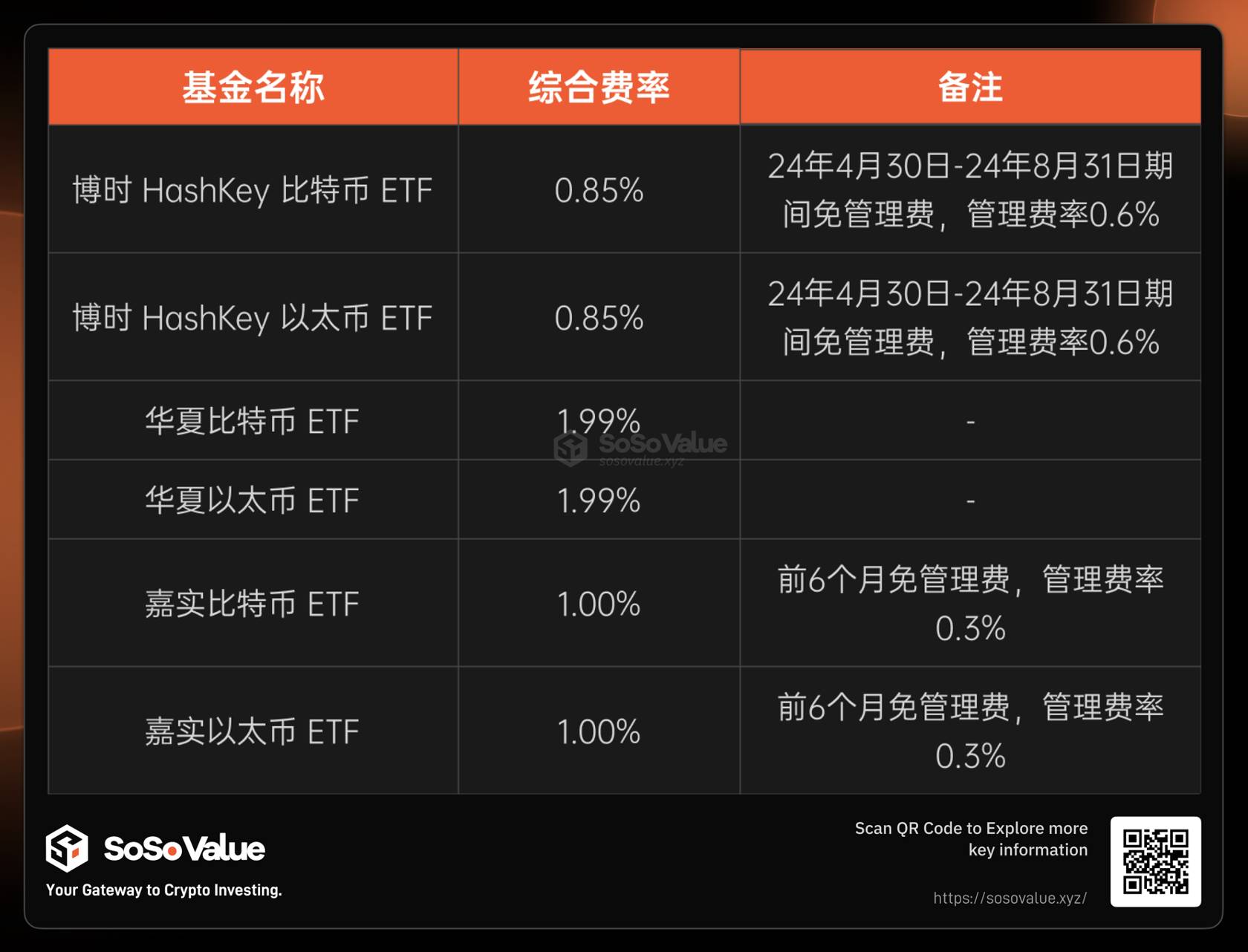

In terms of fees, Hong Kong crypto ETFs hold no competitive advantage over U.S. equivalents, reducing their appeal to institutional investors seeking long-term exposure. According to SoSo Value, among the 11 U.S. spot Bitcoin ETFs, major players like IBIT and CBOE charge management fees around 0.25%, excluding Grayscale and Hashdex. In contrast, Hong Kong's three Bitcoin ETFs carry higher all-in fees: China Asset Management at 1.99%, Harvest Fund at 1.00%, and Bosera—the lowest—at 0.85%. Even with temporary fee waivers, they remain less cost-efficient. This fee gap makes U.S. Bitcoin ETFs more attractive for institutions aiming to minimize holding costs.

Looking ahead, demand may come primarily from two sources: 1) Hong Kong retail investors. Local retail participants with Hong Kong IDs face lower barriers to entry. Unlike U.S. spot Bitcoin ETFs, which require Professional Investor (PI) status—requiring proof of an investment portfolio worth HK$8 million or total assets of HK$40 million—these Hong Kong ETFs allow direct access to retail investors. Additionally, trading hours align better with Asian time zones, representing a meaningful incremental advantage. 2) Traditional investors interested in Ethereum. As the world’s first spot Ethereum ETF, this product offers a regulated pathway for investors who face practical difficulties holding ETH directly but remain bullish on its long-term prospects, potentially driving new inflows into Ethereum ETFs.

Figure 2: Management Fees of U.S. Spot Bitcoin ETFs (Source: SoSo Value)

Figure 3: Fee Structure of Hong Kong Spot Crypto ETFs (Source: Compiled by SoSo Value)

Supply Side: In-Kind Creation/Redemption Mechanism Increases ETF Share Supply and Boosts Initial Scale

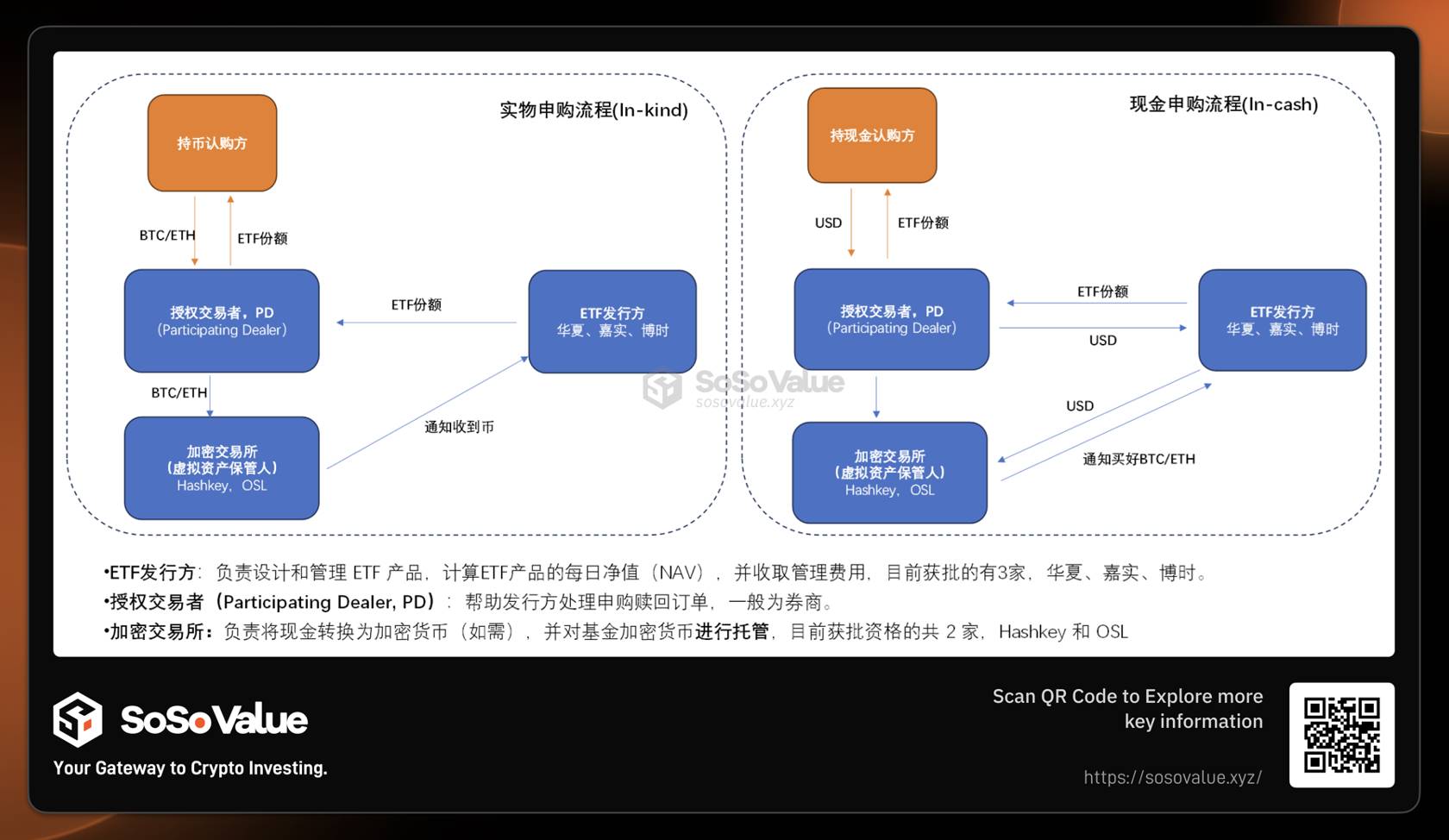

The key difference between Hong Kong and U.S. spot crypto ETFs: Beyond cash-based creation/redemption (in-cash), Hong Kong ETFs additionally support in-kind creation/redemption using actual cryptocurrencies (Bitcoin or Ethereum). This directly expands the pool of potential suppliers at the ETF share level.

In-kind creation/redemption allows investors to exchange physical crypto assets for ETF shares when subscribing (creating new units), or redeem ETF shares for underlying crypto during redemption. Specifically, investors deliver BTC or ETH to obtain ETF shares upon subscription, and return ETF shares to receive crypto upon redemption.

As shown in Figure 4 comparing Hong Kong crypto ETF subscription methods, in-kind creation differs from cash creation in two critical ways:

1) Coin holders can directly participate: Large holders such as miners can easily convert their holdings into ETF shares. These ETF shares can then either be held long-term, redeemed for cash, or directly sold on the HKEX, offering high flexibility.

2) From a market perspective, in-kind creation does not bring new capital into the crypto ecosystem—it merely shifts crypto assets between accounts. Cash creation, however, generates real on-chain buying pressure.

Therefore, Hong Kong crypto ETF subscribers include both traditional cash buyers and existing coin holders. While exact breakdowns of in-kind vs. cash creations are not yet disclosed, OSL’s public communications suggest in-kind creations may have accounted for over 50% of initial subscriptions. This explains why Hong Kong crypto ETFs achieved nearly $300 million in initial规模—where in-kind creation played a crucial role. However, these same ETF shares could later become secondary market sell-side pressure.

Figure 4: Comparison of In-Kind vs. Cash Subscription Processes for Hong Kong Spot Crypto ETFs

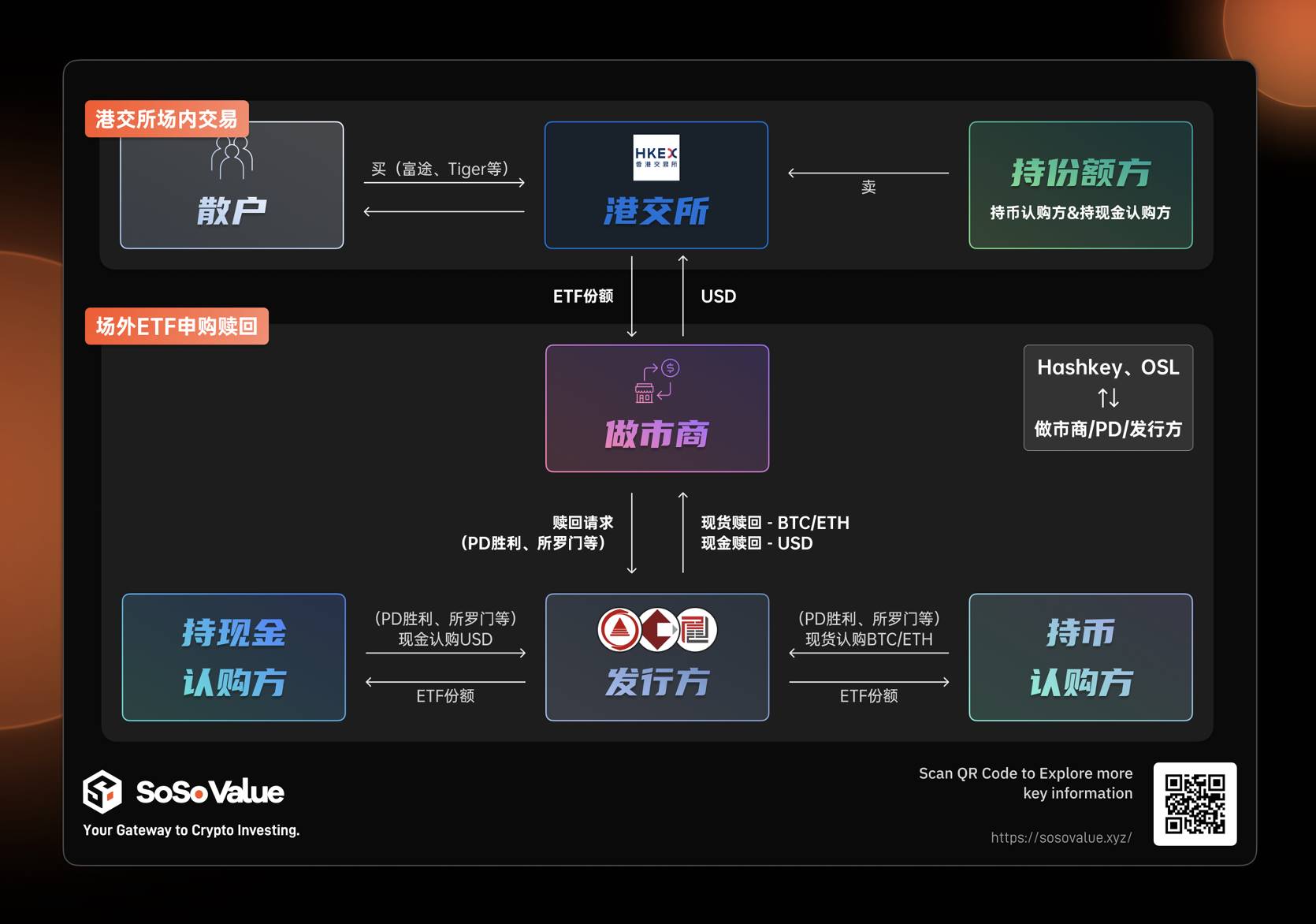

Integrated Supply-Demand View: Monitor Premium/Discount Rates to Identify Investment Opportunities

Unlike U.S. spot Bitcoin ETFs, where we can track daily net fund flows (Total Net Inflow) to gauge fresh capital entering the crypto market, Hong Kong ETFs present a more complex picture due to mixed in-kind and cash creation mechanisms. With fund managers not disclosing granular data on creation types, the premium/discount rate in the public market (HKEX trading) emerges as a more reliable indicator.

Premiums and discounts on the HKEX reflect the real-time balance of supply and demand. A discount indicates stronger selling pressure and oversupply. Market makers may buy discounted ETF shares on-exchange and redeem them off-exchange for underlying crypto, profiting from arbitrage. This leads to ETF shrinkage, net outflows, and negative implications for the broader crypto market. Simplified: ETF discount → stronger sell-side → potential redemptions → bearish for crypto. Conversely, a premium suggests stronger buying interest → potential creations → bullish signal.

According to SoSo Value, as of April 30 closing, only Harvest’s Bitcoin ETF (3439.HK) and Ethereum ETF (3179.HK) showed slight discounts (-0.18% and -0.19%, respectively); all others traded at premiums, with intraday highs reaching +0.33%. This indicates relatively restrained selling and solid initial buying momentum. Considering possible market maker influence on day one, this premium/discount trend warrants ongoing monitoring. Sustained positive premiums could attract further subscriptions—especially from coin holders—and push total ETF规模 beyond the projected $500 million. Conversely, persistent discounts may trigger arbitrage-driven redemptions, forcing issuers to sell underlying crypto and exert downward pressure on prices.

Figure 5: Supply-Demand Impact Mechanism of Hong Kong Spot Crypto ETFs (Source: Compiled by SoSo Value)

Hong Kong Crypto ETFs Offer Another Key Benefit: A New Pathway Converting Crypto Assets into Tradable Financial Instruments

While the immediate market impact of Hong Kong’s spot crypto ETFs may be smaller than that of U.S. equivalents, their in-kind creation mechanism creates a vital bridge converting crypto assets into tradable financial instruments within traditional finance. By using in-kind creation, investors can transform BTC or ETH into ETF shares. Since these shares carry fair market valuations and liquidity recognized by traditional markets, holding crypto asset ETFs can serve as verifiable financial assets, enabling leveraged strategies such as margin lending and structured product construction. This deepens integration between crypto and traditional finance, allowing crypto value to be more fully realized and monetized.

From a broader, long-term perspective, Hong Kong’s approval of Bitcoin and Ethereum spot ETFs marks a pivotal development for the global crypto market. This policy will have lasting implications across Chinese-speaking financial regions and represents a significant step toward the wider legitimization of cryptocurrencies within the global financial system.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News