Understanding the Design Principles and Future Development of EigenLayer at Launch

TechFlow Selected TechFlow Selected

Understanding the Design Principles and Future Development of EigenLayer at Launch

With the full operation of its mainnet launch, it will be necessary to closely monitor whether EigenLayer will bring to Ethereum the new DeFi Summer that some have been anticipating.

Author: DeSpread Research

1. Introduction

Since the second half of 2023, the long-anticipated approval of spot Bitcoin ETFs has become a reality, leading to a surge in institutional capital inflows. As a result, Bitcoin's price has returned to four-year highs for the first time since November 2021. During this period, trading volumes on centralized exchanges such as Binance and Upbit have exceeded $1 trillion, while the adoption of CEX mobile applications has increased, indicating greater retail investor participation.

Additionally, there has been an increase in users withdrawing assets from CEXs to participate in activities such as earning interest on digital assets in decentralized finance (DeFi) or receiving airdrops. This trend has led to the total value locked (TVL) in the DeFi sector doubling compared to the second half of last year.

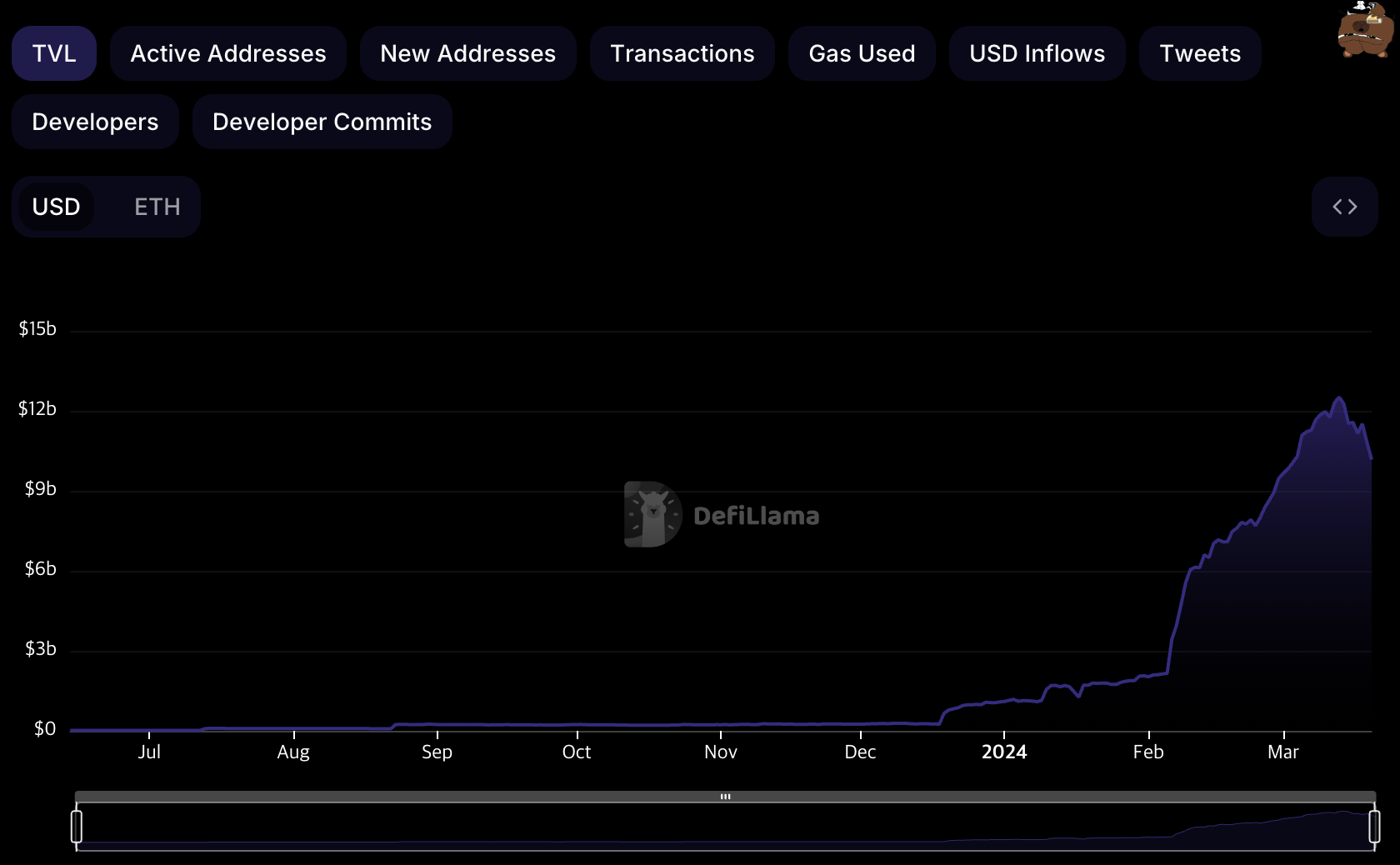

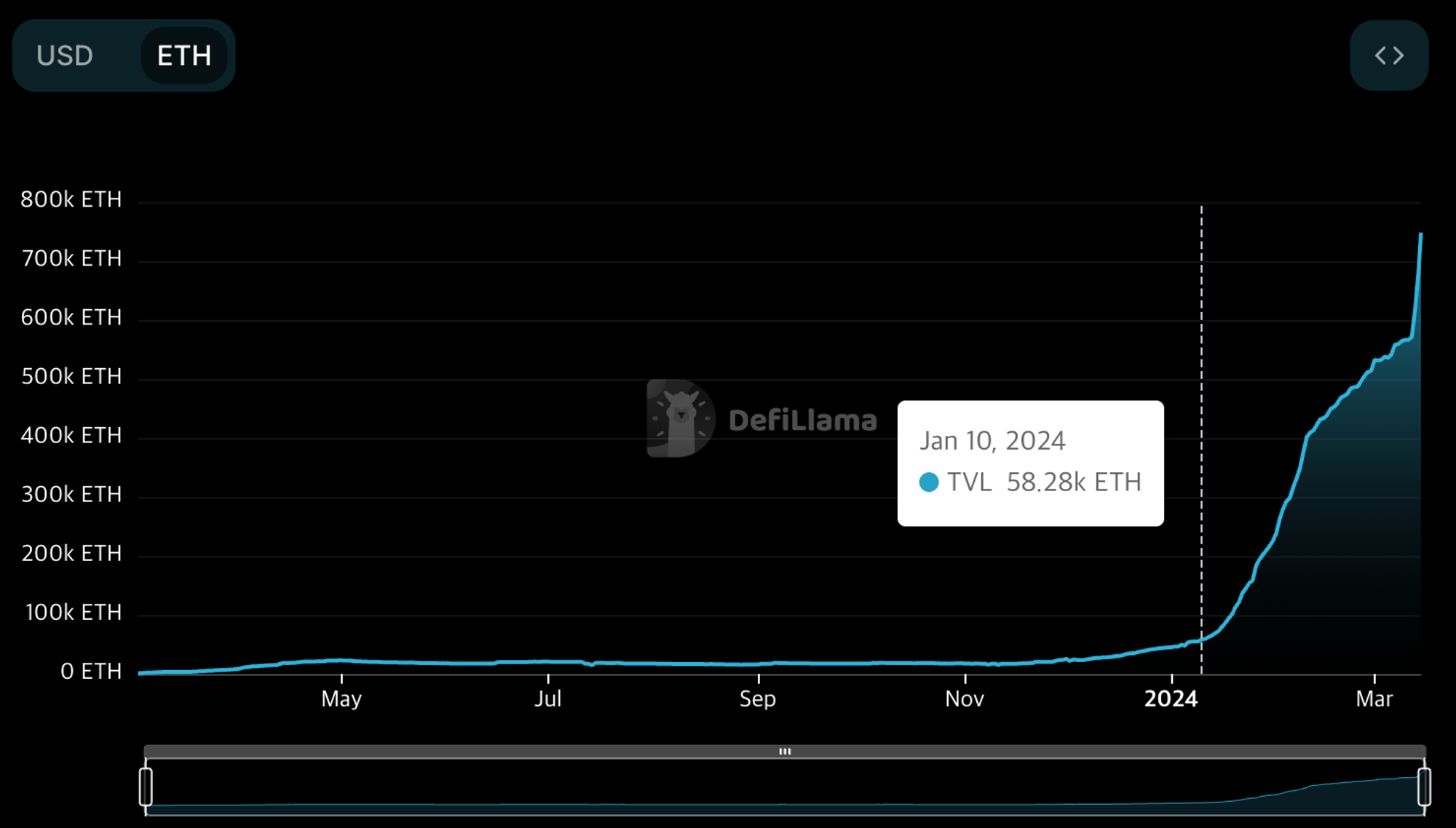

Amid these developments, EigenLayer—a protocol built on the Ethereum network—has seen its TVL grow approximately tenfold from early 2024 to now, rapidly rising to rank third among DeFi protocols by total TVL. This significant growth in TVL has had a profound impact on the overall rise in DeFi TVL.

EigenLayer TVL Trend (Source: Defi Llama)

EigenLayer introduces a restaking mechanism that leverages ETH staked for Ethereum network validation to share security with other protocols while offering additional yield incentives to participants. Thanks to its proposal aimed at maximizing capital efficiency and security within the Ethereum ecosystem, EigenLayer has attracted about $160 million in investment from crypto VCs including a16z.

Moreover, by effectively utilizing various points systems—which have become central to airdrop strategies—it has heightened investor expectations. Through derivative protocols that maximize these points systems, EigenLayer’s TVL has shown a consistent upward trajectory since the beginning of the year.

This article will cover the broader aspects of EigenLayer, focusing particularly on the synergies created between EigenLayer and its derivative protocols.

2. What is EigenLayer?

After Ethereum transitioned from a Proof-of-Work (PoW) consensus mechanism to Proof-of-Stake (PoS), approximately 980,000 Ethereum validator nodes began participating in network validation on the Beacon Chain, each staking 32 ETH. In PoS, the value staked directly correlates with network security, meaning around 31 million ETH are securing the reliability of the Ethereum network. Ethereum's decentralized applications (DApps) can deploy smart contracts on the Ethereum network, thereby inheriting its trust and security.

However, protocols known as Actively Validated Services (AVS), such as bridges, sequencers, and oracles, face significant challenges when relying solely on Ethereum's native capabilities. These AVSs often act as intermediaries between chains or require faster synchronization times than Ethereum can provide. Therefore, they must establish their own trust networks in a decentralized manner, which necessitates developing their own consensus mechanisms.

AVSs aiming to build their own trust networks using a PoS structure similar to Ethereum encounter several issues during network launch:

-

Lack of ways to promote the project and attract stakers

-

Stakers typically need to purchase the AVS network’s native token, which are often volatile and hard to obtain, reducing accessibility compared to ETH

-

AVSs must offer higher annual percentage yields (APY) than ETH to attract stakers, who otherwise would forego alternative asset management opportunities, thus bearing higher capital costs

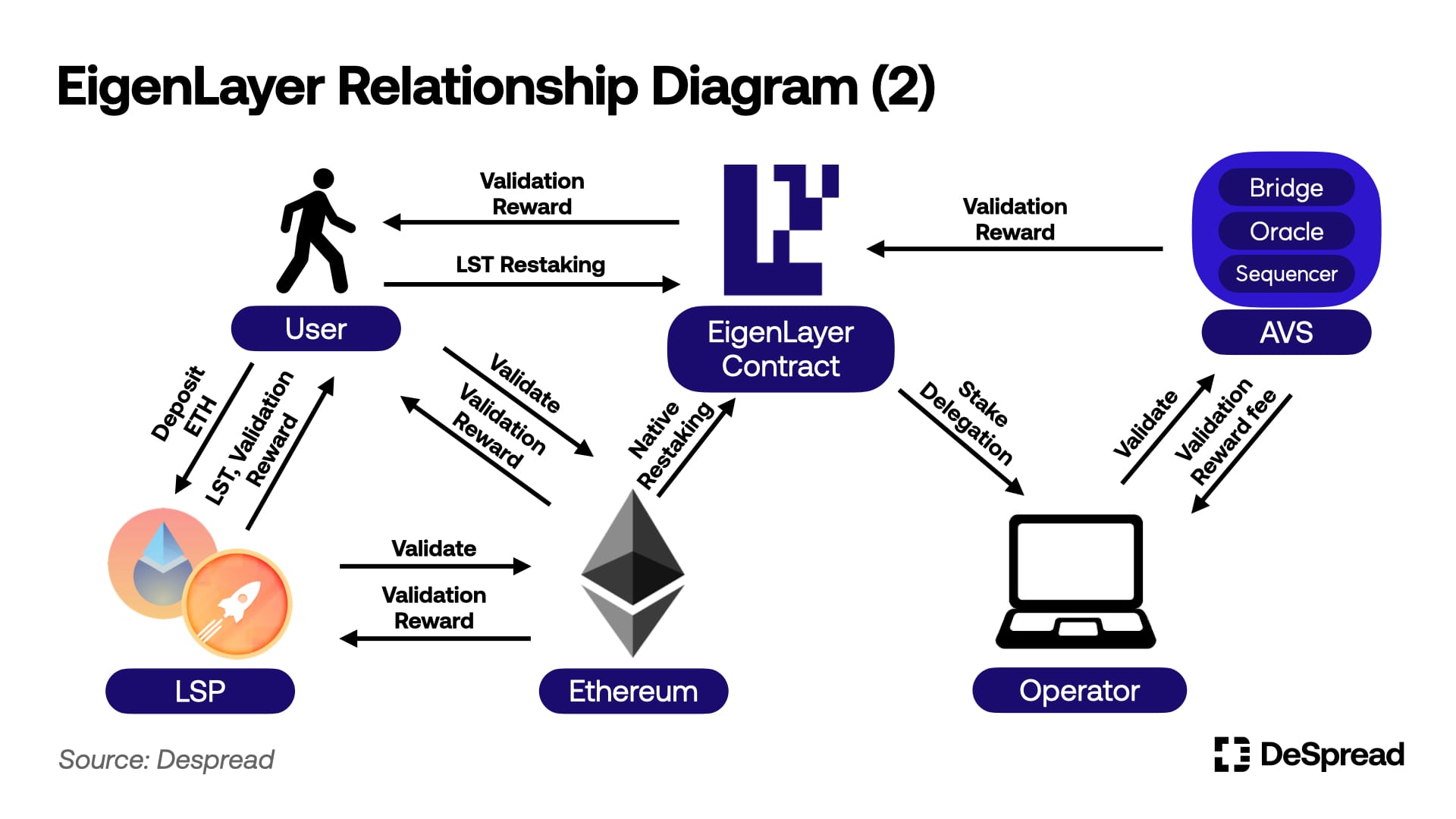

EigenLayer addresses these issues through a feature called restaking, which allows ETH staked on the Ethereum Beacon Chain to be reused for participating in AVS validation. Restaking enables restakers to earn additional validation rewards by engaging in AVS network validation without needing to buy other network tokens—using either ETH or LSTs. For AVSs, EigenLayer aims to provide an environment where they can promote their projects and build trust networks based on liquidity recruited via restakers through EigenLayer.

2.1. Leveraging Ethereum Security via Restaking

Currently, validators on the Ethereum network may lose up to 16 ETH out of their 32 ETH stake if they engage in actions harmful to network security. If their staked ETH falls below 16 ETH, they lose their validator status. This implies that if a method exists to use staked liquidity as collateral, it could be possible to leverage up to 16 ETH elsewhere, provided the remaining balance stays above 16 ETH, allowing continued participation in Ethereum validation.

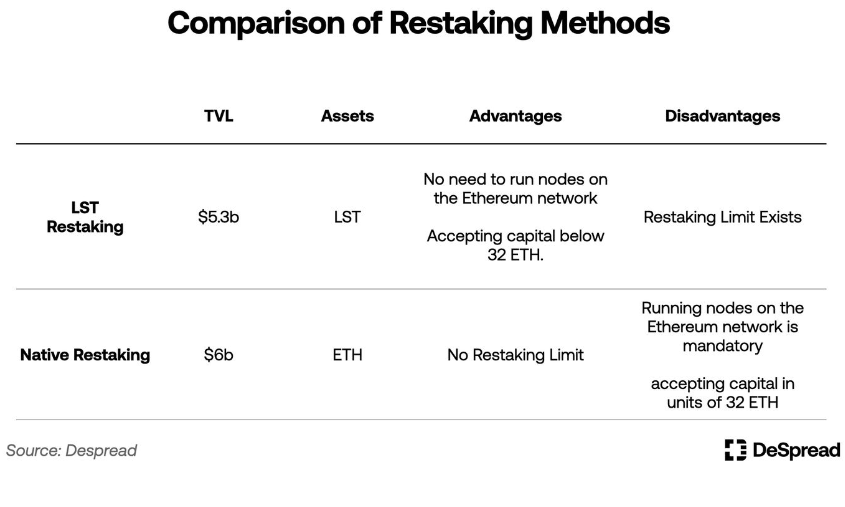

Restaking in EigenLayer refers to using the idle portion of a validator’s staked ETH as collateral by exposing it to slashing conditions of AVSs that use PoS consensus algorithms, thereby providing security through validation. Currently, EigenLayer supports two restaking methods: LST (Liquid Staking Token) restaking and native restaking.

Native vs. Liquid Restaking (Source: EigenLayer)

LST Restaking: Although referred to as liquid restaking in EigenLayer, this article uses "LST restaking" to reduce confusion with subsequent concepts.

2.1.1. LST Restaking

LSTs (Liquid Staking Tokens) are deposit certificates issued by LSPs (Liquid Staking Providers), linking ETH depositors with entities operating Ethereum nodes on their behalf. LSPs solve certain limitations of staking on the Ethereum network, such as:

-

Allowing users with less than 32 ETH to participate in Ethereum network validation and receive staking rewards.

-

Allowing LSTs to generate additional income in DeFi protocols or be sold on markets without waiting for unstaking periods, effectively providing unstaking-like benefits.

A prominent LSP, Lido Finance, currently holds about 10 million ETH in deposits. Many DeFi protocols have started adopting stETH—the LST issued by Lido Finance—as an asset usable within their platforms, making it infrastructure within the Ethereum ecosystem.

EigenLayer offers a restaking function involving depositing LSTs—Ethereum deposit certificates—into EigenLayer smart contracts and participating in AVS validation while being exposed to AVS network slashing rules. This method is known as LST restaking.

Following its mainnet launch in June 2023, EigenLayer began supporting restaking of stETH, rETH, and cbETH, and now supports a total of 12 types of LST restaking.

The EigenLayer development team has worked to ensure decentralization and neutrality of the protocol by imposing limits on each LST type. These measures include accepting LST restaking deposits only during specific periods or limiting any single LST’s access to incentives and governance rights within EigenLayer to a maximum of 33%. To date, EigenLayer has increased its LST restaking caps five times, and no further plans to raise deposit limits have been announced as of writing.

2.1.2. Native Restaking

While LST restaking involves using LSTs as collateral for AVS validation, native restaking is a more direct approach where Ethereum PoS node validators connect their staked ETH directly to EigenLayer.

Ethereum node validators can participate in AVS validation by using their staked ETH as collateral. They do so by setting the withdrawal address for their staked ETH to their own wallet address instead of the contract address (called EigenPod) created through EigenLayer.

In other words, Ethereum network validators give up the right to directly receive their deposited ETH and instead participate in native restaking to join AVS validation. This exposes their staked assets not only to Ethereum’s slashing rules but also to those of AVSs, though they may earn additional rewards.

Executing native restaking requires staking 32 ETH and directly managing an Ethereum node, presenting a higher barrier to entry compared to LST restaking. However, it is not subject to the restrictions imposed on LST restaking.

2.2. Operators

After restaking in EigenLayer, restakers have two options: either run AVS validation nodes directly or delegate their restaked share to operators. Operators represent restakers in AVS validation and earn additional validation rewards.

Operators grant slashing rights over the stakes they hold or are delegated, install software required for AVS validation, and then participate in the validation process. In return, they can charge fees set by themselves from restakers.

However, the process of sharing security with AVSs is currently running only on testnets. As such, there are currently no active operators or AVSs in EigenLayer, and restakers do not receive any additional validation rewards. Recently, EigenLayer mentioned entering the final preparation phase for launching its first AVS, EigenDA, on mainnet and activating AVS validation in Stage 2.

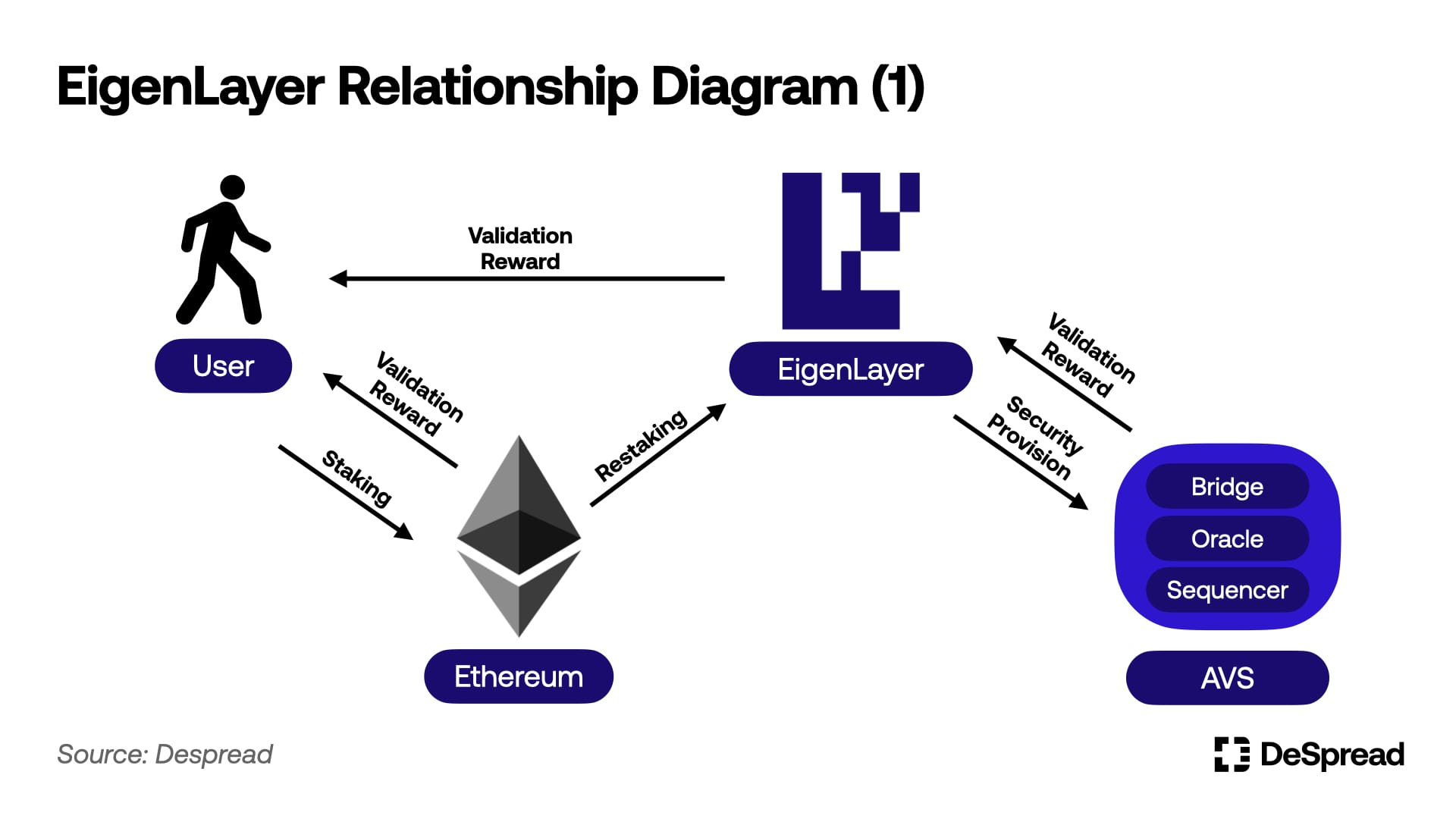

To summarize, the relationship map of EigenLayer looks like this:

2.3. EigenLayer Points

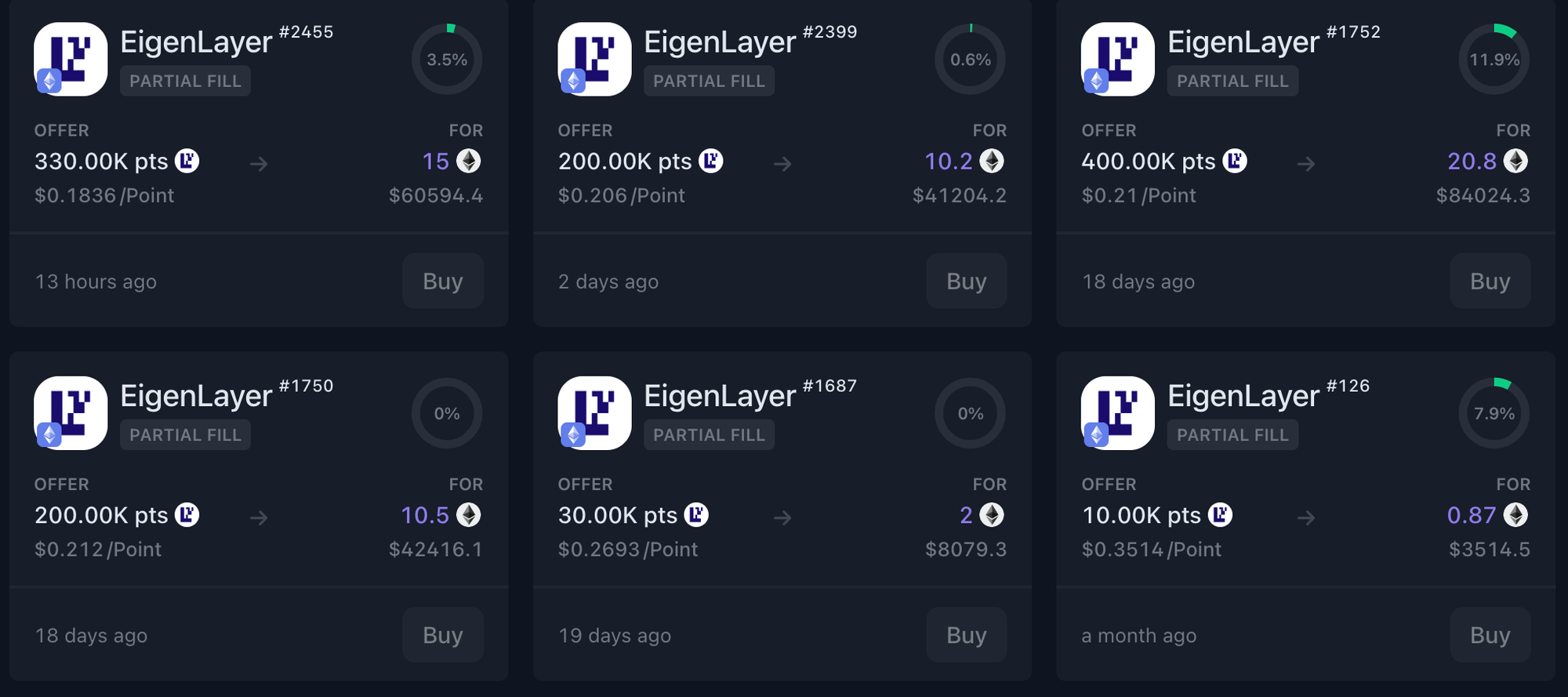

EigenLayer awards one EigenLayer point per hour for every ETH deposited by a restaker, measuring contribution. Although the team has not yet specified the use of these points or disclosed details about launching an EigenLayer token, many users are restaking in anticipation of a future token airdrop based on accumulated points.

As of writing, approximately 2.6 billion EigenLayer points have been distributed to all restakers, and on over-the-counter marketplaces, each EigenLayer point trades at $0.18.

This allows the market to estimate the expected value of an EigenLayer token airdrop at around $440 million—compared to Celestia’s airdrop value of $120 million on launch day—indicating substantial market anticipation and interest.

EigenLayer Points Status (Source: Whales Market)

However, users restaking purely for airdrop points face several inconveniences:

-

LST restaking has caps, preventing users from freely depositing desired amounts.

-

Native restaking requires 32 ETH in capital and involves directly running an Ethereum node.

-

Restaking locks liquidity in EigenLayer, forcing users to forgo other income-generating opportunities.

-

Unstaking from EigenLayer to retrieve bonded liquidity requires a 7-day withdrawal period.

To mitigate these drawbacks and make restaking more efficient, LRP (Liquid Restaking Protocols) have emerged. Using LRPs for accumulating EigenLayer points has become a more attractive investment option for users.

3. LRP (Liquid Restaking Protocol)

LRPs accept user deposits of ETH or LSTs and perform restaking on EigenLayer on their behalf. Additionally, LRPs issue LRTs (Liquid Restaking Tokens) as proof of deposited assets, allowing users to generate additional income by deploying these LRTs in DeFi protocols or selling them on markets—bypassing the waiting period for unstaking from EigenLayer. Structurally, LRPs resemble LSPs beyond just depositing assets into EigenLayer.

LSP (Liquid Staking Protocol): A protocol serving as an alternative to direct Ethereum network validation

LST (Liquid Staking Token): A token issued by an LSP to depositors as proof of principal amount

LRP (Liquid Restaking Protocol): A protocol serving as an alternative to direct restaking on EigenLayer

LRT (Liquid Restaking Token): A token issued by an LRP to depositors as proof of principal amount

Moreover, most LRPs, in addition to issuing EigenLayer points, also distribute their own protocol points to depositors. Thus, using an LRP provides several advantages over direct restaking via EigenLayer, such as:

-

Creating added value through the use of LRTs

-

Closing restaking positions by selling LRTs

-

Earning additional airdrops through protocol points

However, EigenLayer points generated through LRPs are attributed not to the depositor’s wallet address but to the ownership address of the LRP. Therefore, LRPs commit to distributing any received EigenLayer token airdrops to their depositors and provide dashboards for users to check their accumulated EigenLayer points via the LRP.

In the following sections, we will classify LRPs based on two criteria and continue with detailed explanations.

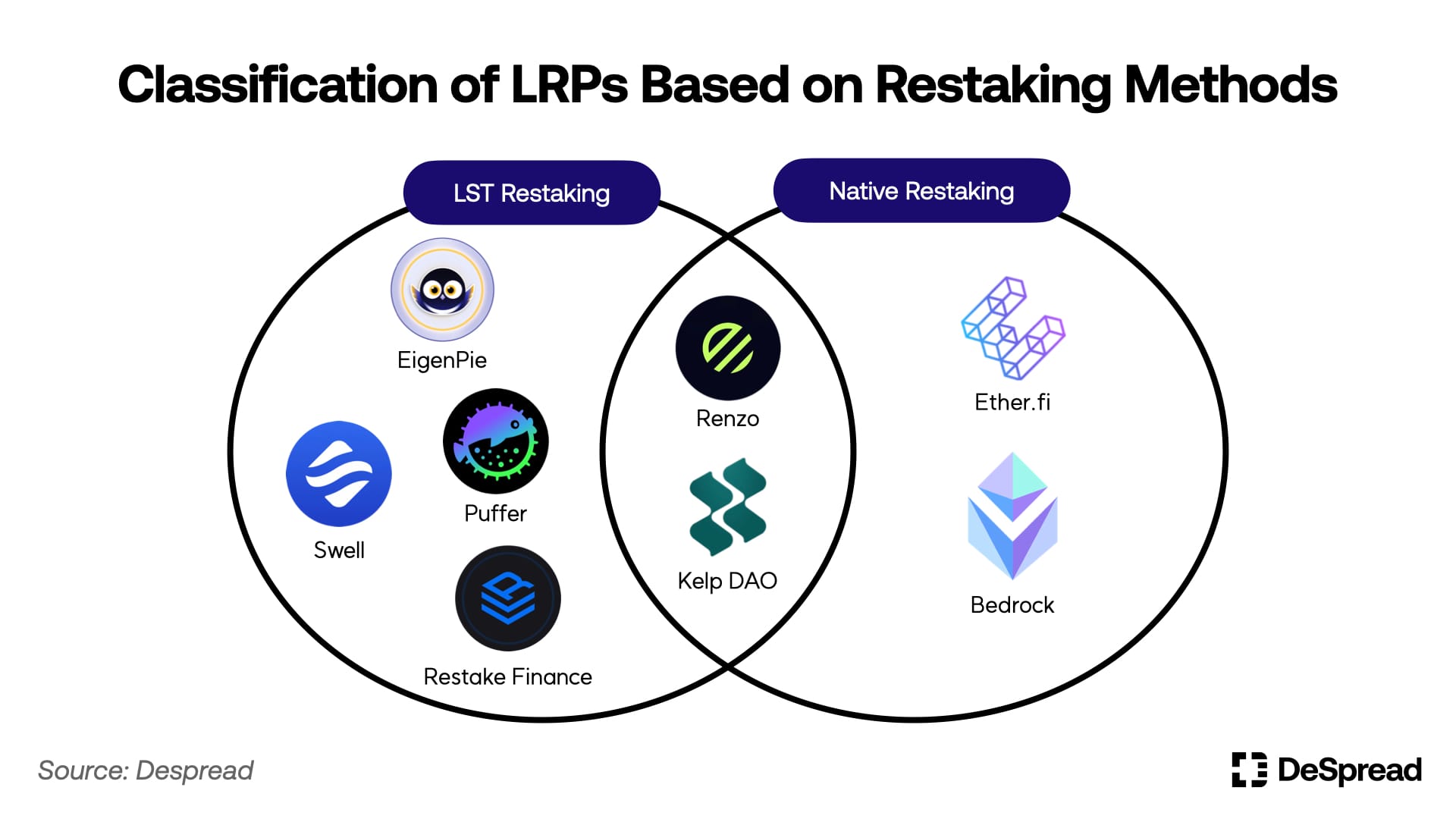

3.1. Classifying LRPs by Restaking Method

As previously discussed, EigenLayer offers two restaking methods: LST restaking and native restaking. These differ in terms of accepted deposit asset types and whether they involve operating Ethereum network nodes.

LRPs using the LST restaking method can build their protocols through a relatively simple mechanism. They accept users’ LSTs, deposit them into EigenLayer contracts, and issue equivalent-value LRTs to depositors. However, they are directly affected by LST restaking caps. Unless EigenLayer reopens LST restaking, LSTs deposited during capped periods remain within the LRP protocol, and depositors will not accumulate EigenLayer points until their assets are restaked.

On the other hand, LRPs using the native restaking method must directly manage and operate Ethereum network nodes, as they accept ETH from users. This requires significantly more work to build, operate, and maintain compared to LST-based LRPs. However, unlike the capped nature of LST restaking, native restaking has no such limits, allowing depositors to start earning EigenLayer points immediately after depositing funds.

Based on these characteristics, LRPs adopt restaking methods aligned with their protocol concepts and are not necessarily restricted to one method. For example, Kelp DAO initially supported LST restaking to quickly accumulate TVL post-EigenLayer launch and later adopted a strategy incorporating native restaking functionality.

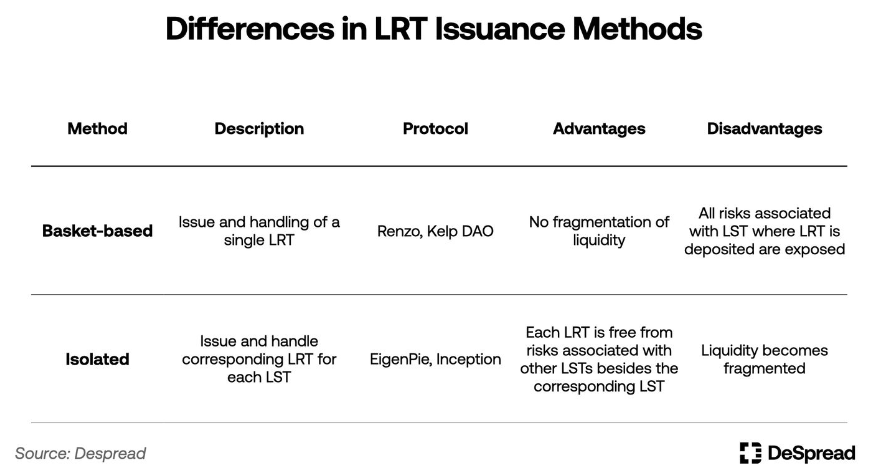

3.2. Classifying LRPs by LRT Issuance Method

Among LRPs that accept multiple LST types or use ETH as a single underlying asset and perform restaking, the method of issuing LRTs can be categorized as either basket-style or standalone-style.

The basket-style approach issues and pays out a single type of LRT regardless of the type of LST deposited into the LRP. Since it handles only one LRT, it is intuitive for users and avoids fragmenting LRT liquidity. However, a drawback is that the entire LRP is exposed to individual risks of the deposited LSTs, requiring adjustments to the LST deposit ratios within the LRP to mitigate these risks.

Conversely, the standalone-style approach issues and pays out different LRTs corresponding to each LST handled by the LRP. While this leads to fragmented LRT liquidity, the risks associated with each LST are isolated, eliminating the need to adjust deposit ratios.

Although the standalone approach carries fewer risks and is relatively easier to set up and operate, most LRPs adopt the basket-style method. This approach is simpler for users and facilitates collaboration with DeFi protocols.

Beyond these basic features, LRPs differentiate themselves through unique functionalities and market-entry strategies to attract users. Let us examine some examples in detail.

3.3. Exploring Notable LRPs

3.3.1. Ether.fi

Ether.fi originally started as an LSP with the concept of allowing stakers full control over their deposited ETH and was the first LRP to support native restaking after EigenLayer’s launch. This enabled Ether.fi to offer EigenLayer points farming to its depositors via native restaking, allowing it to continuously grow its TVL even during periods when restaking was capped.

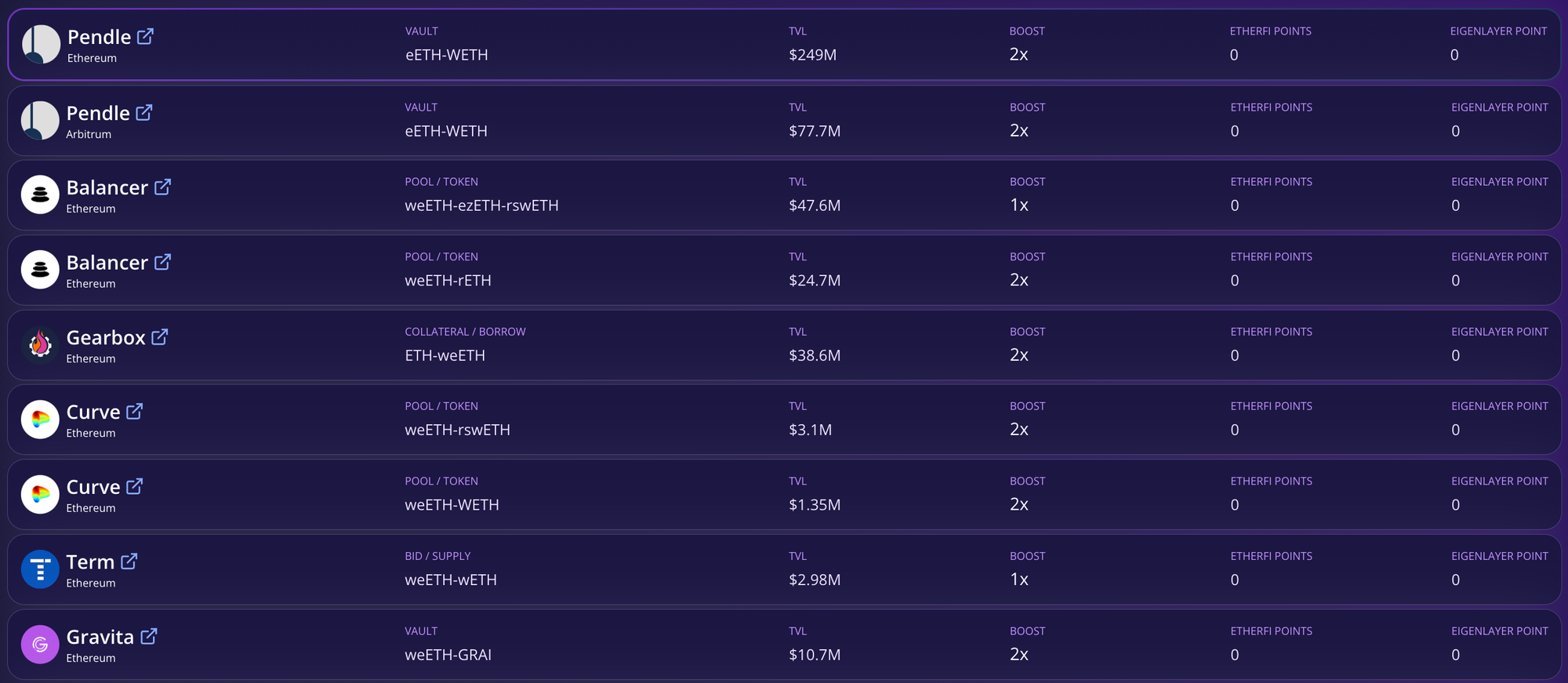

Ether.fi issues two types of LRTs: eETH and weETH. eETH is the base LRT received upon depositing ETH into Ether.fi and employs a rebasing mechanism where yield accrues directly into the token balance. Rebasing tokens adjust holders’ wallet balances upon yield distribution, maintaining a 1:1 value ratio with the underlying asset. However, some DeFi protocols do not support this token mechanism. To enhance compatibility between LRTs and DeFi protocols, Ether.fi offers a wrapping function converting eETH into weETH, a reward-bearing token reflecting accrued yield.

Ether.fi rewards LRT holders with both EigenLayer points and its proprietary protocol points, Ether.fi Loyalty Points. To reduce downward pressure on LRT prices and expand utility, Ether.fi partners with various DeFi protocols, enabling users to deposit LRTs into DeFi platforms while continuing to accumulate EigenLayer points. Ether.fi also runs campaigns to boost Ether.fi Loyalty Points for users actively using their LRTs in DeFi activities.

Ether.fi’s DeFi Dashboard (Source: Ether.fi)

Users can use eETH or weETH in various DeFi activities, such as:

-

Providing liquidity to weETH/WETH pools on decentralized exchanges like Curve and Balancer.

-

Using weETH as collateral in lending protocols like Morpho Blue and Silo.

-

Issuing overcollateralized stablecoins using weETH as collateral in protocols like Gravita.

-

Using weETH in derivatives protocols like Pendle and Gearbox.

Through these activities, users can simultaneously earn interest from DeFi protocols or utilize tokens obtained by using LRTs as collateral, while also accumulating EigenLayer and Ether.fi Loyalty Points. Recently, Ether.fi enabled bridging of LRTs to Ethereum L2s Arbitrum and Mode Network, offering users lower gas fees when using LRTs in DeFi.

On March 18, Ether.fi announced the TGE of its governance token $ETHFI and conducted an airdrop of 6% of the total supply based on Ether.fi Loyalty Points. A second airdrop is scheduled for June 30, allocating 5% of the total ETHFI supply.

Currently, Ether.fi holds the highest TVL among LRPs, at approximately $3 billion, accounting for about a quarter of EigenLayer’s total restaked liquidity.

3.3.2. Kelp DAO

Kelp DAO initially launched as a basket-style LRP offering LST restaking for two assets—Lido Finance’s stETH and Stader Labs’ ETHx—and issuing a single LRT, rsETH.

Initially, as EigenLayer raised its LST restaking cap, many users quickly filled the limit but faced inconvenience due to high gas fees and timezone differences. In response, Kelp DAO introduced a solution: users could deposit their LSTs into the protocol, and once the cap was reached, Kelp DAO would handle the restaking. Depositors would receive Kelp DAO’s proprietary points, Kelp Miles, attracting a large user base. Like other LRPs, it designed its system to boost Kelp Miles when users engaged their LRTs in specific DeFi protocols, encouraging both restaking and LRT usage.

Kelp DAO has now added native restaking to its offerings, providing depositors with unlimited EigenLayer points earning opportunities. Similar to Ether.fi, it focuses on enhancing user convenience by supporting restaking on the Arbitrum network, making it easier for users to hold and use their LRTs in DeFi.

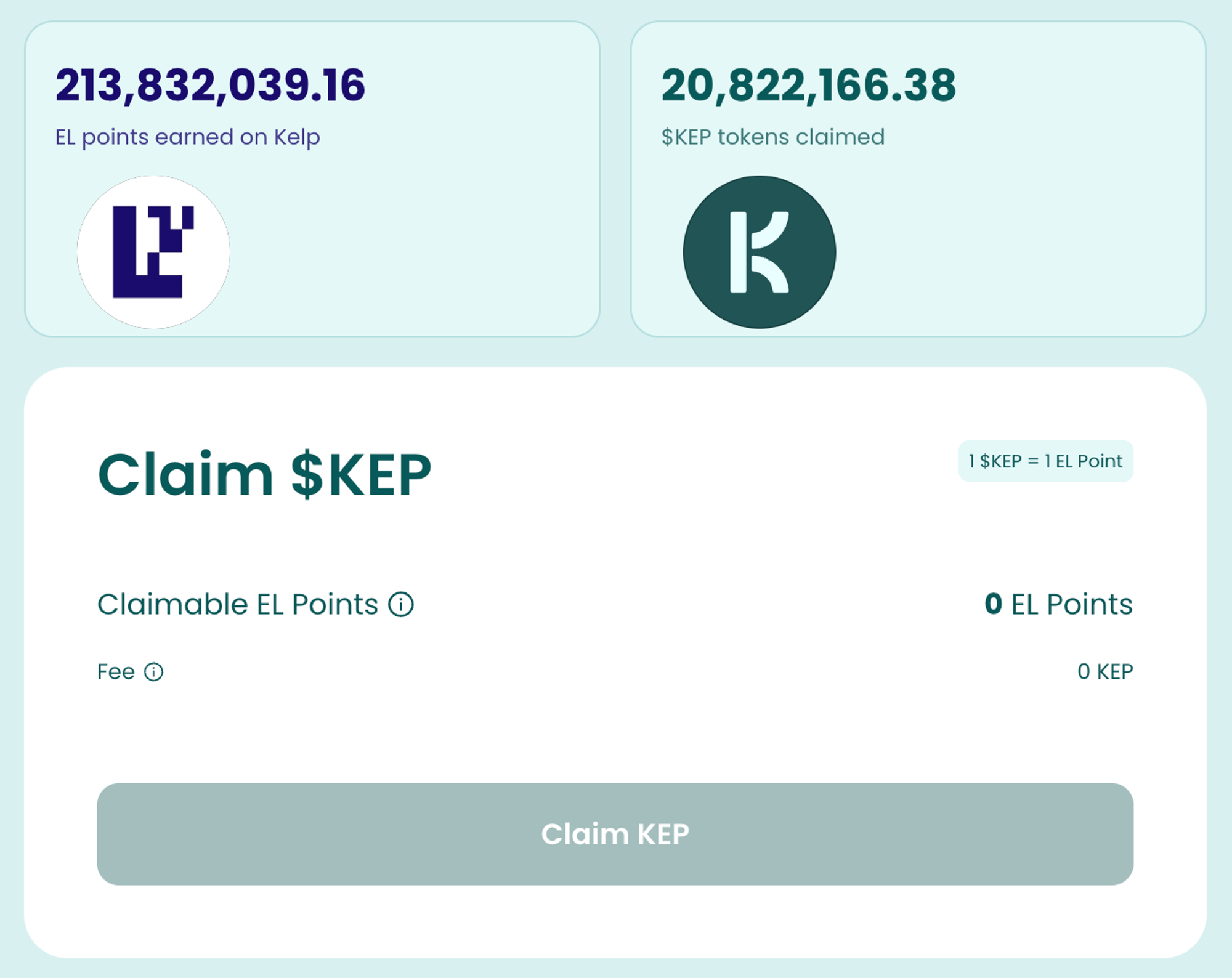

Additionally, Kelp DAO distinguishes itself by allowing users to convert their farm-earned EigenLayer points into a token called $KEP.

Kelp DAO’s $KEP Claim Page (Source: Kelp DAO)

Users can convert their accumulated EigenLayer points into $KEP tokens by paying a 0.5% fee. They can then sell these tokens on markets to monetize their EigenLayer points or provide liquidity on decentralized exchanges like Balancer, generating additional income and earning Kelp Miles. Moreover, users who haven’t deposited assets into Kelp DAO can still buy $KEP on the market, effectively gaining the same benefits as those who accumulated EigenLayer points through Kelp DAO.

3.3.3. EigenPie

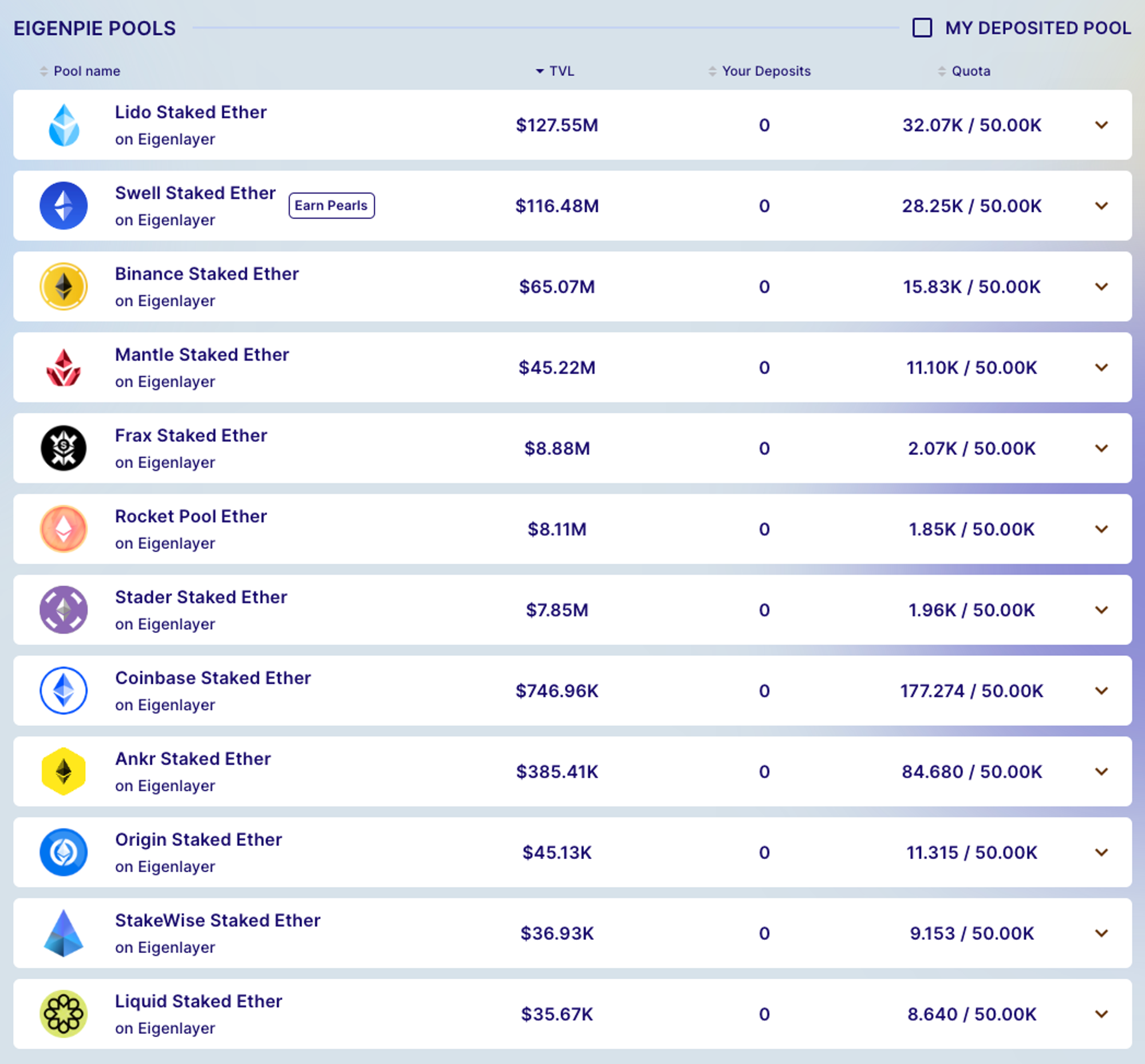

EigenPie is a sub-DAO launched under the MagPie ecosystem, aiming to aggregate governance tokens to exert significant influence over decisions in DeFi protocols, especially targeting EigenLayer. It supports restaking of all LSTs supported by EigenLayer and adopts a standalone approach, issuing and distributing distinct LRTs for each deposited LST.

List of LSTs Supported by EigenPie (Source: EigenPie)

Isolating pools for each LST shields EigenPie from risks associated with concentration in a particular LST and makes it easier to form partnerships and run campaigns with specific LST protocols. For instance, LSP Swell Network partnered with EigenPie to run a campaign rewarding users who deposited its native LST, swETH, into EigenPie with Swell Network’s proprietary points—prior to launching its own native restaking feature.

Depositors in EigenPie can accumulate both EigenLayer points and EigenPie points. The official team has announced that users holding these points will have the opportunity to participate in the upcoming airdrop and IDO of its governance token $EGP via this program.

However, EigenPie does not support native restaking, leaving it constrained by EigenLayer’s LST restaking caps. Furthermore, due to issuing twelve types of LRTs, its liquidity is more fragmented compared to other LRPs, resulting in relatively fewer integrations with DeFi protocols.

4. Leveraged Points Farming

LRPs serve as intermediaries for restaking and provide LRTs, offering users convenient access to EigenLayer points. Additionally, by introducing their own proprietary points systems and partnering with DeFi protocols to run engagement campaigns, they have attracted a large number of airdrop farmers to the EigenLayer ecosystem.

However, in the early days of LRPs, there were few lending protocols willing to accept LRTs as collateral. As a result, users participating in points-boosting campaigns could only honestly farm EigenLayer points proportional to the amount of LRT they held.

Gravita, an overcollateralized stablecoin issuance protocol, allows users to use Ether.fi’s weETH as collateral to mint stablecoins. Users can then leverage their position through a process called looping—using stablecoins backed by LRTs to buy and deposit more LRTs, thereby earning more EigenLayer points. However, high gas fees on the Ethereum network and Gravita’s minimum usage requirement (at least 2,000 stablecoins issued) posed significant entry barriers for many attempting to loop.

This changed on January 10, 2024, when Pendle Finance began supporting Ether.fi’s eETH, enabling users to conduct leveraged points farming with minimal capital. This development sparked considerable interest among airdrop farmers using Pendle Finance for EigenLayer points farming, leading to significant growth in the TVL of both EigenLayer and LRPs.

Ether.fi TVL (Source: Defi Llama)

4.1. Pendle Finance

Pendle Finance is a DeFi protocol that enables trading of yield-bearing tokens such as LSTs and LRTs by assigning a fixed maturity date and splitting them into a Principal Token (PT) and a Yield Token (YT).

The combined value of YT and PT always equals the value of the underlying asset. YT holders are entitled to claim the accumulated yield from the time of purchase until maturity. As the maturity date approaches, the value of YT tends toward zero, while the market price of PT discounts proportionally based on demand for the YT token.

Pendle Finance Operating Mechanism (Source: Pendle Learn)

For more information on Pendle Finance, please refer to “Pendle Finance – Discovering an Untapped Trading Market”.

Pendle Finance collaborated with Ether.fi to launch eETH as the first LRT available on its platform. Ether.fi designed a system to distribute both EigenLayer points and Ether.fi Loyalty Points to holders of the YT-eETH token. This allows users to purchase near-expiry YT-eETH (which becomes cheaper over time) and accumulate yield and points until maturity.

Here is an example:

Pendle Finance eETH Dashboard (Source: Pendle Finance)

The above image reflects the state of Pendle Finance’s eETH product as of writing, with the following details:

-

Product matures on June 27, 2024, about 103 days from the writing date.

-

eETH’s 7-day average APY is 3.13%, with a current price of $3,872.

-

YT-eETH is priced at $196; purchasing at this value results in a -99.8% annual yield on interest.

-

PT-eETH is priced at $3,676; purchasing at this value results in a 20.02% annual yield on interest.

As of the writing date, the exchange rate between eETH and YT-eETH is approximately 1:20. Ether.fi is currently running a campaign offering double Ether.fi Loyalty Points to YT-eETH holders. Therefore, a user exchanging one eETH for YT-eETH and holding until maturity would receive:

-

Interest equivalent to holding 20 eETH

-

EigenLayer points equivalent to holding 20 eETH

-

Ether.fi Loyalty Points equivalent to holding 40 eETH

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News