Is RWA the next step for Bitcoin ETFs, or just a modified version of stablecoins?

TechFlow Selected TechFlow Selected

Is RWA the next step for Bitcoin ETFs, or just a modified version of stablecoins?

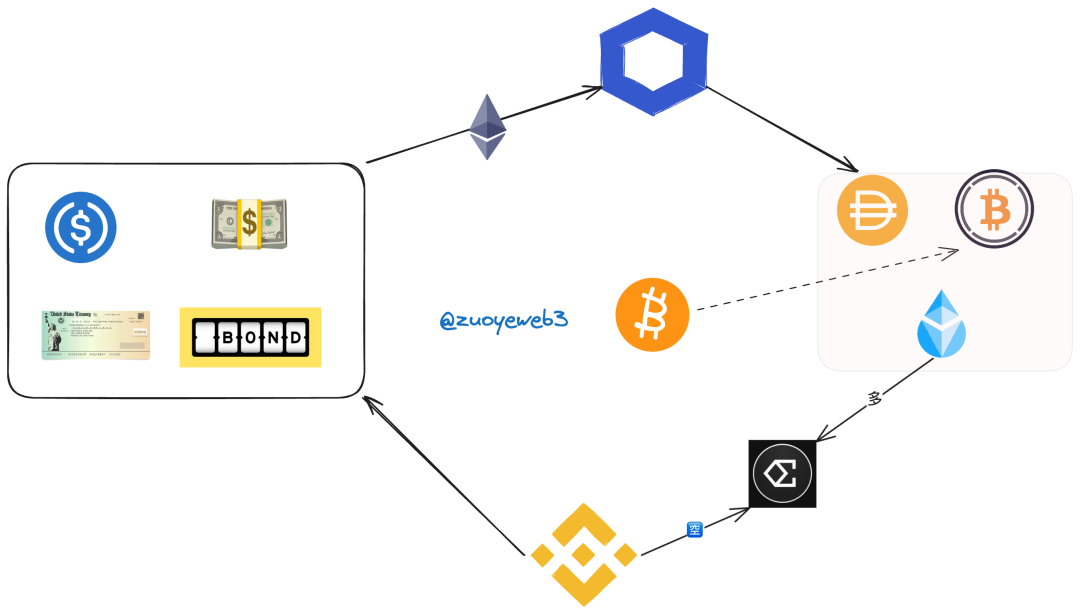

This round of RWA is limited to onboarding dollar-related assets, bridging BTC/ETH off-chain, with stablecoins as the primary issuance method and lending as a supplementary development path.

Author: Zuo Ye

Is RWA the Next Step for Bitcoin ETFs, or Just a Modified Version of Stablecoins?

The only lesson retail investors have learned from market cycles is that they never learn from history.

Faced with Ethena’s high yields, the painful memory of Luna-UST quickly fades into the past, returning everyone to a game of who can exit fastest.

Even MakerDAO's DAI couldn't resist temptation, abandoning its traditionally low-risk USDC-backed structure and actively embracing the high returns offered by USDe.

Although Ondo’s USDY has been live for less than three weeks, its TVL surged from $100 million to $200 million. By partnering with BlackRock’s BUIDL fund, it shares risk and jointly expands the RWA ecosystem.

As we can see, all three above examples are stablecoins—and represent the latest developments in RWA: real-world assets going on-chain, native on-chain arbitrage, and ultimately feeding value back into real-world assets—forming three interconnected yet independently operating microcosms.

New Forms of RWA

Specifically, current RWA developments extend beyond just stablecoins, reflecting several emerging trends:

-

Dollar-denominated real world: Real-world assets now focus on U.S. Treasuries, dollars, bonds, and compliant stablecoins. Rather than "real-world assets going on-chain," it's more accurate to say dollar-related assets are being tokenized.

-

Dual-currency standard in crypto: Bitcoin and Ethereum are widely recognized within the crypto world. Ethereum not only serves as an issuance chain but ETH itself functions as reserve collateral equivalent to Bitcoin.

-

Integration over disruption: Traditional finance (TradFi) institutions and exchanges have become infrastructure for crypto operations. RWAs originate from them, flow back to them, and their existence is no longer questioned—reality’s gravity has ultimately bowed the head of idealism.

From Dollar Tides to ETH “Deflation–Recirculation” Standard

Each bull-bear cycle typically starts with Bitcoin, followed by capital concentration into major platforms such as exchanges, DeFi protocols, or stablecoins, eventually collapsing due to a liquidity crisis in one project.

This cycle differs significantly. On one hand, off-chain inflows brought approximately $60 billion via ETFs, alleviating the global "tide-like" dollar shortages historically caused by U.S. interest rate cuts followed by hikes. Bitcoin acts as a reservoir, mitigating this impact—with potential for over tenfold expansion.

Key takeaway 1: Bitcoin exhibits dual nature—both a real-world asset and a crypto asset.

This reservoir model has two development paths: increasing Bitcoin’s capacity or expanding into additional ETF products, such as Ethereum.

On the other hand, Ethereum’s staking system creates an internal “deflation–recirculation” mechanism. Using ETH as the base asset, even if LSDfi (liquid staking derivatives finance) or LRTfi (re-staked token finance) projects collapse, ETH’s staking yield remains intact. During bull markets, increased usage drives deflationary appreciation.

In short, going long on ETH increases USD-denominated returns; going short doesn’t reduce ETH-denominated gains—as long as ETH maintains its phoenix-like resilience akin to Bitcoin through market cycles.

Key takeaway 2: Profiting in both directions becomes possible if you survive market cycles—losses in bear markets can be recovered in bull runs.

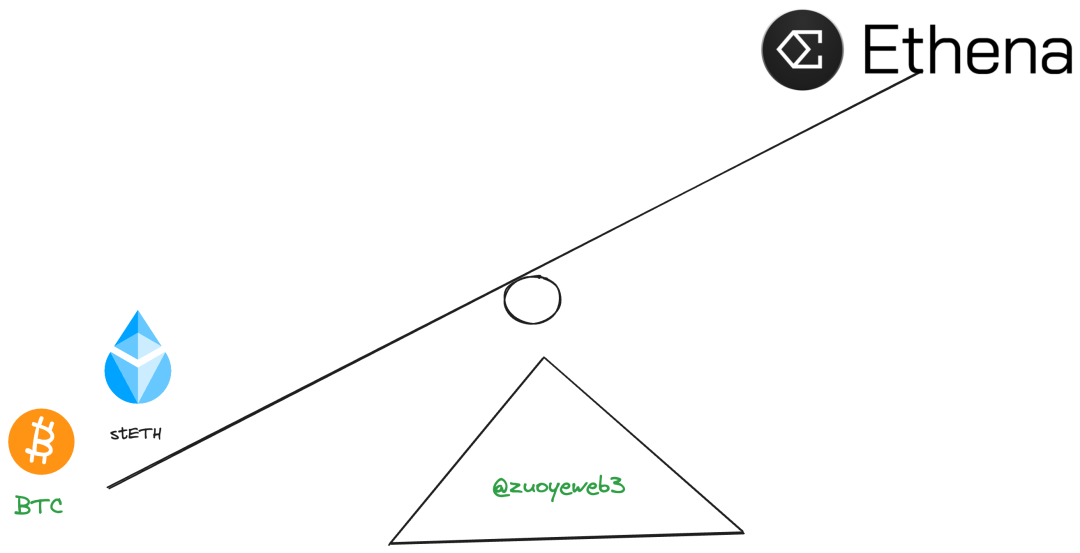

Now consider this: What if a new asset were pegged 1:1 to the dollar, used a gold-silver bimetallic standard (BTC+ETH) as reserves, and seamlessly integrated with centralized exchanges? Could such a USDe under this RWA model survive market cycles?

Key takeaway 3: Don’t resist centralized exchanges—treat them as a source of profit.

We cannot predict the future, only hypothesize based on past patterns. USDe will likely collapse eventually, but if the bull market lasts long enough, it may decline gradually and fade into obscurity. However, if ETH’s price crashes sharply, USDe would collapse rapidly.

Based on these three key points, let’s clarify why this conclusion applies to USDe.

How USDe Works

USDe issuance is linked to ETH long/short positions. According to AC’s theory, spot trading is essentially a perpetual contract with zero or 1x leverage—buying equals going long, selling equals going short.

USDe’s delta neutrality works similarly: collateral consists of stETH and BTC (equivalent to long positions), while simultaneously taking offsetting short positions on exchanges. This balance achieves risk hedging through opposing exposures.

There are two sources of yield here: stETH provides ~4% annual return, and shorts earn funding fees paid by longs. Combined, during bull markets when ETH prices rise continuously, USDe’s USD-denominated yield becomes extremely high.

However, risks follow closely. If ETH’s price falls, USD-denominated returns vanish—and worse, shorts must pay funding fees to longs, potentially leading to insolvency and sudden collapse.

Yet there remains hope: even if ETH’s dollar value drops, stETH still generates yield in ETH terms. As long as the protocol survives until the next bull market, selling ETH can still generate profits—provided users maintain confidence and don’t withdraw funds prematurely.

During bull markets, everything works smoothly. Exchanges need shorts to maintain liquidity for BTC/ETH pairs, and technical manipulations like disconnections or wick spikes are now routine and tolerated.

But as we’ve seen, rather than relying solely on ETH derivatives pricing, USDe fundamentally depends on exchange cooperation. Exchanges themselves are black boxes—an issue oracles cannot resolve. Moreover, it remains unclear how exchanges will react to USDe communities profiting from funding fee farming.

USDe is undeniably innovative, prompting me to discuss it mid-article. Next, I’ll speculate on Ondo’s new business model and where MakerDAO’s DAI might be headed.

Ondo essentially tokenizes assets like U.S. Treasuries, representing a broader trend in RWA: full dollarization and “virtualization” of underlying assets. Physical assets like real estate or non-dollar currencies are no longer the primary focus.

From physical to virtual, ascending to bliss

MakerDAO, meanwhile, represents the struggle of on-chain protocols. Its recent proposal to directly purchase U.S. Treasuries is still fresh in memory—yet the path forward for RWA remains uncertain. Should assets go on-chain, should native crypto assets move off-chain, or should both approaches be combined? Perhaps time is needed to validate these ideas.

Divergence and Coexistence: Navigating Relations with the Barbarians

After discussing the BTC/ETH dual-standard system, it's important to note that massive off-chain capital inflows aren't universally beneficial. Asset management giants like BlackRock and Franklin Templeton manage assets over ten times larger than Bitcoin’s market cap. Yet partnering with them offers regulatory resilience against the SEC and a continuous supply of resources. A tripartite equilibrium has emerged:

-

Traditional financial giants: Opening new fronts beyond futures and spot ETFs, aiming to enter on-chain markets and experiment with innovative financial combinations;

-

RWA projects: Approaching from a crypto-native perspective, seeking collaboration with TradFi to achieve regulatory compliance and become mainstream investment options—not fighting regulators, but seeking legitimization (“amnesty”);

-

Regulators: Attempting resistance initially, then shifting to control when overwhelmed—OFAC targeting Ethereum nodes, SEC defining what constitutes a “security,” Congress and the Federal Reserve focusing on stablecoins and exchanges, with anti-money laundering and illegal securities charges as common tools.

From the perspectives of Bitcoin and Ethereum, regulators have effectively given approval—ETH spot ETFs are merely a matter of time. But smaller projects lack the strength to resist regulation alone. Aligning with traditional financial giants and proactively implementing KYC/AML measures helps shed the image of financial disruptors and repositions them as innovators within the existing system.

Put simply, anything tied to real-world assets faces immense challenges—the gravity of reality is too heavy. Broadly speaking, the evolution of RWA can be divided into three stages:

-

Eastern “Chain Everything” Craze: The belief that everything can and should be put on-chain—emphasizing traceability and immutability, exemplified by projects like GXChain (Gongxinbao), which ultimately ended in failure;

-

Western “Tokenization”: Converting physical and digital assets into tokens on-chain—RealT’s real estate projects being the most iconic example, alongside lending platforms like Maple and Centrifuge;

-

Followed by today’s trend of U.S. financial assets going on-chain, along with the convergence and co-development of BTC/ETH native assets and the traditional financial system.

This is my personal view. While RWA.XYZ categorizes RWA into four types—lending, U.S. Treasuries, stablecoins, and real estate—I maintain that the current wave of RWA boils down to three core elements: tokenizing dollar-related assets, bringing BTC/ETH off-chain, primarily using stablecoins as issuance vehicles, with lending serving as a supplementary layer.

However, this ecosystem faces three major constraints: CeFi’s desire for control, CEXs’ incentives to act maliciously, and the heavy hand of regulation (SEC).

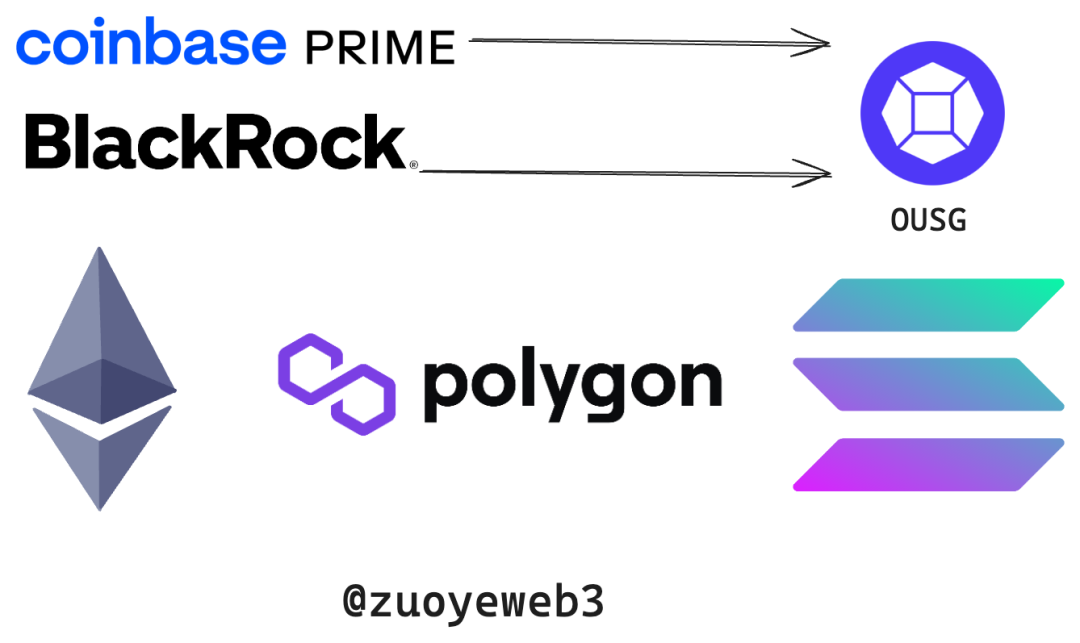

Take Ondo as an example: it has launched two main products—OUSG (backed by U.S. Treasuries) and USDY (a yield-bearing stablecoin). Future offerings will expand further. Their mechanisms are similar: relying on registered entities, Big Four audits, bank/institutional custody, and investments in dollar-denominated assets—a process too familiar to detail again.

OUSG Components

OUSG primarily holds BlackRock’s short-term Treasury ETF products. Ondo has deeply partnered with BlackRock and plans to further collaborate on BlackRock’s RWA product BUIDL—making it a prime example of bidirectional integration.

Taking it further, some are already managing wealth for the old money—for instance, Compound founder’s Superstate directly purchases U.S. Treasuries and tokenizes them. The process may seem dull, but it signifies a shift: the crypto world has spawned its own Old Money class. They’ve moved past the high-risk, high-reward “Age of Exploration” and now seek peaceful retirement ashore, enjoying their looted treasures.

Yet, fresh forces continue pushing forward. For example, MakerDAO’s DAI is preparing to embrace USDe’s high yields, initially allocating $600 million, with potential to scale up to $1 billion. Not only can DeFi stack layers, but stablecoins can now become building blocks for other stablecoins. Crucially, remember: USDe is not fundamentally a dollar-equivalent—it’s a proxy for ETH volatility.

Faced with vast real-world assets, the crypto world still appears somewhat immature. Compared to asset managers controlling trillions of dollars, hundreds of millions or even billions in TVL are negligible. More importantly, do we truly believe RWA will become a major asset class—on par with ETFs—or is it merely crypto’s unrequited love affair, leaving behind nothing but debris after the hype dies down?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News