Plain-language explanation of asset allocation: How to stay invincible in the market?

TechFlow Selected TechFlow Selected

Plain-language explanation of asset allocation: How to stay invincible in the market?

"In the world of investing and trading, as long as you're alive, you have a chance"—this is one of the rare sentences that can be considered 100% correct.

Author: JZ

Today’s topic—“Asset Allocation”—is about staying alive in any market condition so you can wait for the next opportunity. This ability is especially crucial in crypto, where opportunities abound, but if you get wiped out during a bear market, you’ll miss future chances to strike it rich. Since asset allocation is a broad and deep subject, this article aims to quickly and clearly explain two key things:

-

What is asset allocation?

-

How do you actually do asset allocation?

We’ll wrap up with real-world examples to make sure you fully grasp asset allocation. The goal is to ensure your investing and trading are built on a stable foundation—so you can steadily gain experience and improve, rather than just shooting in the dark and relying on luck. Let’s get started!

Basic Concepts of Asset Allocation

Asset Allocation Is Standard Practice for Institutional Investors

One major difference between retail and institutional investors is whether they use asset allocation—the core idea being risk management. Understanding proper asset allocation (also known as portfolio management) means you’ve grasped the fundamentals of risk control.

What most people call “trading” is actually just one part of asset allocation. Yet many focus only on reading charts and predicting price movements, imagining they can dominate the market—only to end up wiped out by its harsh realities.

Asset Allocation Keeps You Alive!

As the saying goes: if you’re not dead, you still have a chance. And asset allocation helps ensure you stay in the game, waiting for the right opportunities.

Next, we’ll cover how to implement asset allocation, but first let’s review the relationship between risk and expected return: “The higher the expected return, the higher the risk—but the reverse isn’t always true.”

In short, asset allocation involves combining strategies with different expected returns, balancing them within a certain range so that overall risk stays within what you can tolerate.

That’s the essence of asset allocation. Now, let’s dive into how to actually do it.

How to Do Asset Allocation?

Next, I’ll walk you through the steps of asset allocation, guide you step-by-step through the process, and then show some practical examples.

Steps of Asset Allocation

Here’s a simple, distilled version of the asset allocation process in four main steps:

-

Assess the current state of financial markets and the economy, and consider possible (especially worst-case) future scenarios.

-

Identify all your current assets and divide them into emergency reserves and low-, medium-, and high-risk investment buckets.

-

Based on your personal financial situation and investment experience, decide the allocation percentages for each bucket.

-

Determine the specific investment or trading strategies for each bucket.

From my observation, most crypto investors only do a small part of step 4 and treat it as “investing.” They might get lucky with a big win from a single trade, but without proper asset allocation or risk control, they eventually lose it all back to the market due to “bad luck.”

This is why many feel intense pressure from investing and trading—so much that it affects their daily lives. Emotions then lead to poor decisions, creating a vicious cycle that ultimately results in being eliminated from the market.

Remember: if you believe “investing should improve your quality of life,” then practice proper asset allocation. Don’t treat the market like a casino.

Next, I’ll go into detail on steps 2, 3, and 4. Step 1 requires long-term skill development—follow JZ Invest if you’d like to build market intuition over time. First, let’s define what we mean by emergency reserve, low-, medium-, and high-risk buckets.

Defining Risk Levels of Investment Buckets

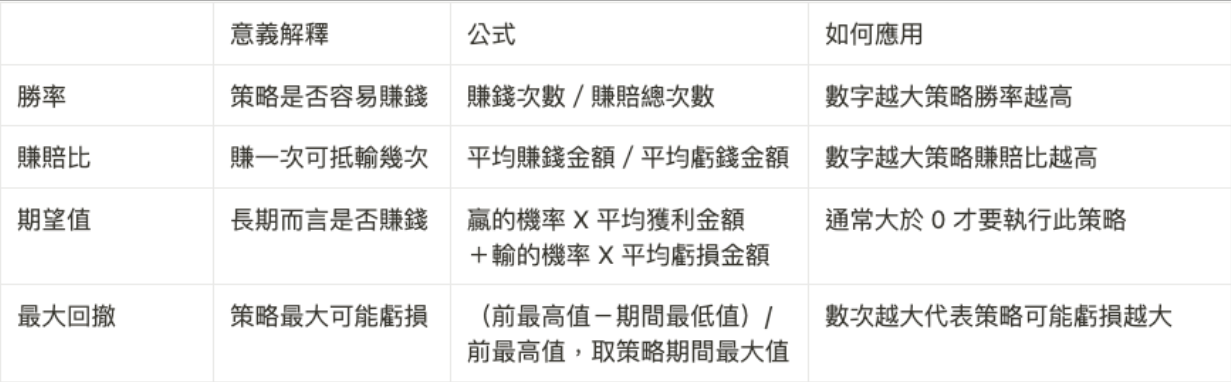

Everyone has a different risk tolerance, so definitions of low, medium, and high risk will vary from person to person.

However, you can assess risk using win rate, risk-reward ratio, expected value, and maximum drawdown (MDD). The table below explains how to interpret these four metrics in plain terms.

Once you understand these four criteria, you can apply them to classify low-, medium-, and high-risk strategies, as shown in the table below.

-

Low-risk strategies: Focus on consistent profitability. Win rate should ideally exceed 95%, with relatively modest returns but very limited downside. Maximum drawdown should be kept under 5%, and liquidity should be high for easy access to funds.

-

Medium-risk strategies: These span a broader range of metrics. Any strategy that isn’t clearly low- or high-risk typically falls here.

-

High-risk strategies: Offer potentially very high returns, but also come with significant downside risk compared to low- and medium-risk strategies. Win rates are often below 20%, with reward-to-risk ratios above 5. Maximum drawdown could reach 100%. Position sizing and risk controls must be handled carefully. These are often long-term positions with poor liquidity.

What about the emergency reserve bucket?

I haven’t mentioned it yet because it’s straightforward: just remember the two key principles—“safety” and “liquidity.”

One special consideration: unlike many other countries, Taiwan faces potential geopolitical risks, including war. Therefore, individuals holding more than 10 million TWD in cash might consider converting part of it into foreign currency and storing it in overseas banks.

Now that we’ve defined each type of strategy, let’s discuss how to determine appropriate allocation ratios.

Building a Personalized Asset Allocation Strategy Based on Your Circumstances

First, there’s no one-size-fits-all allocation ratio. You can assess your own risk tolerance based on the following five factors. If your risk tolerance is low, allocate more to low-risk buckets—and vice versa.

-

Cash flow: How high and stable is your income (e.g., salary or other cash inflows)?

-

Funding needs: Do you have short-term financial obligations—due to age, health, family needs, or other expenses?

-

Expertise: Do you have financial or investment knowledge? How much time can you dedicate to research each day?

-

Opportunity cost: Could the time spent investing generate more stable and higher returns if used elsewhere?

-

Personality: Are you risk-seeking or risk-averse?

Thinking through these five points will help you objectively and subjectively evaluate your risk tolerance. If you’re still unsure how to begin, refer to the example I’m about to share.

Real-World Asset Allocation Example

Let’s walk through a simplified example based on a friend of mine (a native Taiwanese) to illustrate the asset allocation process.

1. Assess Current Financial and Economic Conditions

He’s pessimistic about global economic growth in 2023, but from a capital markets perspective, he believes the downside is limited. So while his overall outlook is bearish, he’s actively looking for opportunities to buy (go long) certain assets.

2. Identify All Current Assets

His total asset value isn’t disclosed, but the amount is large enough to warrant international diversification—making asset allocation essential. He sets aside approximately 3–5% of his total funds as an emergency reserve.

He plans to open a bank account abroad. Currently, he uses a U.S. brokerage account, transferring TWD via wire transfer. This allows him to diversify into USD, invest in U.S. stocks, and reduce exposure to Taiwan’s geopolitical risks.

3. Determine Investment Allocation Ratios

Below are his financial and investment characteristics:

-

Income isn’t as stable as a salaried job, but he has consistent investment-generated cash flow

-

Good health and no family financial responsibilities

-

Eight years of investing/trading experience; trades full-time

-

Strong financial expertise; opportunity cost of focusing on investing is low

-

Risk profile is neutral-to-conservative, but willing to take calculated risks

Based on these factors, he’s a relatively high-risk-tolerant investor. After setting aside his emergency fund, he can allocate most of his capital to medium- and high-risk strategies.

Considering current and future market conditions, he decides on a 30% low-risk, 50% medium-risk, and 20% high-risk allocation. He’ll adjust these ratios based on market developments and forward-looking expectations, aiming to keep liquidity flexible across all buckets, with each containing some cash component.

4. Determine Investment and Trading Strategies for Each Bucket

Since my friend is familiar with crypto and sees more opportunities there—and understands its high-risk nature—he allocates most of his capital to the blockchain sector. That said, he also holds some positions in Taiwan and U.S. equities. Below, we’ll focus on his blockchain-specific strategy allocations.

-

Low-risk: Lending on Bitfinex, arbitrage opportunities (exchange and on-chain), exchange yield products, and “freebie” farming

-

Medium-risk: Event-driven trading, trend-following (right-side) trading, delta-neutral long-short strategies

-

High-risk: Options strategies to capture market crashes, long-term DCA investing (left-side trading)

As for the details of these strategies, he’ll be sharing them later on the JZ Invest Facebook and Telegram channels—feel free to follow along.

If you have any questions about the content above, please join the JZ Invest Telegram group, where I’ll be answering questions and learning together with you!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News