Memory chip stocks retreat over 20% from their highs—where is the real danger signal hiding?

TechFlow Selected TechFlow Selected

Memory chip stocks retreat over 20% from their highs—where is the real danger signal hiding?

The real sell signal isn’t a Google paper—it’s the buyer’s first “no.”

Author: Dan Nystedt

Compiled by TechFlow

TechFlow Intro: Micron has fallen over 24% from its recent peak; SanDisk is down nearly 21%. The market has blamed Google’s latest research paper—but the real reason runs deeper.

According to the author’s firsthand source: smartphone memory chip buyers have simply stopped accepting higher prices. That “no” is the first sell signal seasoned memory-cycle investors wait for.

This article analyzes the current position within the industry cycle—and examines whether the AI “super-cycle” narrative still holds.

Full Text Below:

Bullish investors in memory chip stocks blame Google’s recent research paper for the recent downturn—but that’s not why prices are falling.

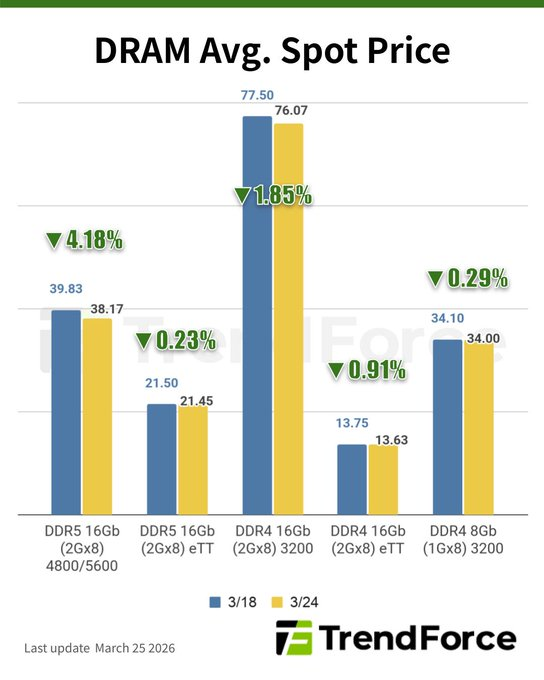

The real cause is far simpler: pricing for certain smartphone memory chips has plateaued. Buyers have finally said “no”—the very first sell signal experienced memory-cycle investors look for before exiting.

Some smartphone manufacturers now plan to reduce (or even eliminate entirely) production of mid- and low-end models in 2026. Soaring DRAM and NAND prices have made these devices too expensive.

I heard this news through a friend.

I was furious.

“My contact called me two weeks ago saying some buyers recently refused to accept higher DDR4 quotes,” he said.

Me: “Two weeks ago?!”

“Well, that’s why I asked you for coffee.”

Me: “I asked you!”

Since then, memory chip stocks have pulled back. Micron has dropped over 24% from its recent high of $471.34. SanDisk has fallen nearly 21% from $777.60.

Investors who follow the memory-cycle playbook exited swiftly. This industry—DRAM and NAND—is famously cyclical.

Over the past 50 years, memory chips have undergone roughly a dozen major boom-and-bust cycles; at least three have occurred since 2010:

- 2012–2015: Smartphones (3G/4G transition + social media explosion). Cloud/data centers provided support. Smartphones surpassed PCs as the largest memory consumers.

- 2016–2019: Cloud/scale-out data center expansion + smartphones (storage upgrades, 5G rollout approaching).

- 2020–2023: COVID-driven surge in remote-work PC/server demand. Cloud providers became the largest memory buyers.

- 2024–202?: AI-driven upcycle—focused on training (HBM) and inference (SRAM) server memory.

These cycles are so common they’re nicknamed the “hog cycle,” borrowed from livestock farming.

High pork prices incentivize farmers to raise more hogs—but breeding takes time. So new pork hits the market en masse about a year later—causing prices to crash.

In the DRAM/NAND world, the “breeding time” is the long lead time required to build new wafer fabs.

When prices soar, companies rush to expand capacity—but when everyone ramps up output simultaneously, the flood of new supply once again crushes prices.

As prices rebound, the cycle repeats. Memory chips behave just like hogs.

Memory-cycle investors follow their playbook religiously. No matter how many people write “this time is different”—that phrase itself is a classic sign that bullish sentiment has gone unchecked.

“The market is never wrong—opinions often are.” — Jesse Livermore, Reminiscences of a Stock Operator, 1923

Is This the Top?

In the long term, there’s good reason to believe this memory chip cycle will last longer than previous ones. Surging AI demand is real—even amid Wall Street skepticism, infrastructure buildout continues.

All cycles begin with soaring chip prices driving stock rallies. Chip buyers appear to have finally halted panic buying.

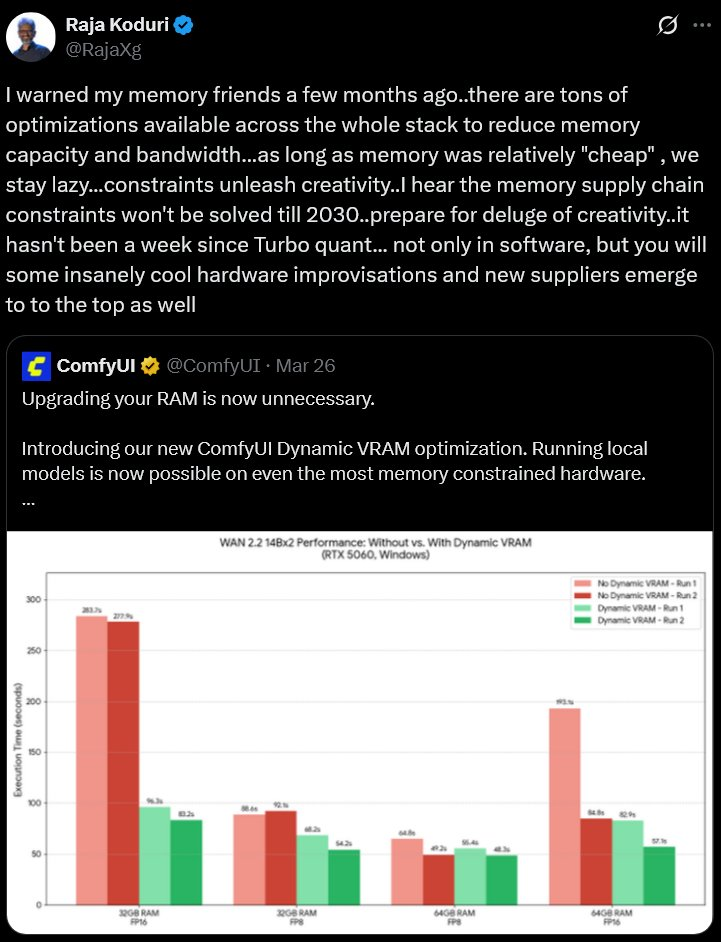

The minor selloff triggered by Google’s TurboQuant paper had less to do with its technical findings—and more to do with what it symbolizes: everyone is searching for solutions to high memory chip prices.

He’s right. High DRAM and NAND prices make novel ideas worth pursuing.

Memory investors may find the next big idea among R&D-focused companies. On-chip memory, for instance, is hot right now.

NVIDIA acquired Groq’s inference technology and core team for $2 billion. The resulting NVIDIA Groq 3 LPU chip—built on Samsung’s 4nm process—packs ~500MB of on-chip SRAM into a standard-sized die—one of the highest densities available—with bandwidth up to 150 TB/s for faster inference (e.g., quicker responses from Grok, Gemini, or ChatGPT).

Research is also underway to integrate more on-chip SRAM in next-generation products using wafer stacking and other methods.

That’s not all.

New memory technologies like ReRAM or MRAM could one day help by offering greater on-chip storage capacity while maintaining SRAM-like speeds. Because they retain data after power loss and operate more efficiently, they can deliver extra fast memory without consuming as much precious silicon area—or power—as pure SRAM does today.

These are just a few examples of memory types likely to thrive in the AI era. AI companies are willing to pay premium prices for performance and energy efficiency.

The wide moat DRAM and NAND have long enjoyed—their lowest cost per bit—has diminished somewhat in importance amid sharp price hikes and looming shortages.

So Has the Memory Boom Ended?

Unlikely.

The memory chip boom still appears early—and may run longer than a typical cycle. The label “super-cycle” fits, given the massive scale of AI data center construction.

Memory stocks could well experience a second leg up.

But seasoned “hog-cycle” investors will always follow their playbook.

Memory stocks must prove themselves. Watch how they perform. If rebounds meet persistent selling pressure, wait—and let them reestablish momentum.

What do you think: Are we still early—or is caution warranted?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News