Bitcoin spot ETF approval is not good news for stocks of crypto companies

TechFlow Selected TechFlow Selected

Bitcoin spot ETF approval is not good news for stocks of crypto companies

Investors have been treating these stocks as Bitcoin substitutes.

Author: Hal Press

Translation: TechFlow

With the approval of ETFs, speculation among cryptocurrency market participants has intensified, and stock investors are increasingly seeking exposure to cryptocurrencies—particularly Bitcoin. However, investing in Bitcoin remains challenging without spot ETFs, as most investors either dislike futures-based ETFs or are prohibited from directly holding crypto assets. This drives demand for proxy assets, leading to significant capital inflows and extreme re-rating of crypto-related equities. We believe that once spot ETFs become available for trading, these flows will experience a one-time reversal, as investors shift from these suboptimal instruments to the direct spot Bitcoin exposure they originally sought.

As a result, there are now multiple attractive hedging opportunities: using long exposure to spot BTC to hedge overvalued alternative crypto-equity positions. Our three preferred equity shorts against Bitcoin proxies are MicroStrategy (MSTR), Marathon Digital Holdings (MARA), and Coinbase (COIN). While each stock has its own nuances, they share one key characteristic—investors have treated them as substitutes for Bitcoin, and we expect their valuations to correct downward once genuine Bitcoin instruments become accessible.

Given strong market demand for leverage, there is an opportunity to earn an effective risk-free yield of 10–30% annually by going long Bitcoin and shorting futures contracts on CME (a classic basis trade). As noted above, due to the lack of direct access to Bitcoin, it's reasonable to assume that some traditional investors have used these proxy assets as a substitute for trading Bitcoin.

On December 28, these proxy assets began a sharp sell-off during the pricing window on CME’s roll date (note: roll date refers to the day when futures contracts transition from one delivery month to the next, requiring investors to roll their positions). This may already signal early signs of reversal. If so, this adds further downside pressure for two reasons. Not only do we expect the CME basis premium to permanently compress—now that ETF approvals provide investors with direct Bitcoin exposure—but this compression will necessitate unwinding existing trades. Such unwinds will involve buying back short futures and selling the crypto-linked equities used to express long exposure.

MicroStrategy (MSTR)

MicroStrategy is often viewed as a Bitcoin proxy, with most observers suggesting its shares trade at a reasonable 5–10% premium to the fundamental book value of the business (operating company + held Bitcoin). However, proper adjustment for share count reveals a much deeper discount—around 25%, recently peaking at 50–60%. These calculations assume a roughly 15x EBITDA multiple for its software business, which is generous given the business has seen no growth for years. Bulls cite two justifications for the sustained premium: leverage and absence of management fees. Neither holds up. With the conversion feature maturing in December 2025 being in-the-money, it should be treated as equity, meaning leverage accounts for less than 20% of enterprise value; even counting the conversion as debt, leverage rises only to 27%, and natural deleveraging occurs as BTC prices rise. In fact, given premiums on both the operating business and BTC holdings, there is negative leverage—each dollar of MSTR is worth less than a dollar of BTC. The management fee argument also lacks merit: MSTR issues approximately 150,000–200,000 shares annually in stock-based compensation (SBC), effectively charging shareholders about 130 basis points in fees—far exceeding the 0–25 bps charged by competing spot ETFs. Under these conditions, MSTR is extremely vulnerable. Considering SBC, uncertainty around BTC unlocks, and the emergence of more attractive spot ETF alternatives, we see no reason why MSTR shouldn’t trade at a discount to its BTC holdings.

Not to mention, investing in BTC via MSTR offers less governance rights compared to ETFs, and comes with higher costs of leverage due to elevated capital costs. Moreover, Saylor (CEO of MicroStrategy) has recently begun selling his own shares, adding further downward pressure. A similar situation occurred with GBTC, which traded at large premiums for years as a proxy ETF, but eventually reversed into discounts when better alternatives emerged and sentiment deteriorated. As shown in the chart below, GBTC’s decline began in late January 2021, when Grayscale halted issuance of new GBTC shares. Despite high premiums persisting, MSTR has not yet launched its latest ATM shelf offering, suggesting awareness of this issue.

Faced with these realities, the expansion of MSTR’s premium to net asset value is difficult to justify. While historical premiums ranged between 30–50%, a 5–10% discount may be more appropriate from a fundamentals standpoint. We estimate “par” at approximately 0.0094 MSTR/BTC, with potential for further downside.

It’s understandable that Saylor is reluctant to sell any BTC, but a scenario could arise where persistent discounting is perceived as damaging to the company. Although he controls the majority voting power, if the discount widens sufficiently, hostile investors may begin accumulating stakes and asserting fiduciary responsibilities. Saylor might personally buy discounted MSTR shares, but that could require liquidating his personal BTC holdings for funding. While unlikely, the possibility that MSTR may eventually be forced to sell part of its BTC holdings (totaling $8 billion) is not zero. In a worst-case scenario, if MSTR attempts to close the discount by selling BTC and repurchasing MSTR stock, this could have reflexive negative effects on the broader crypto market.

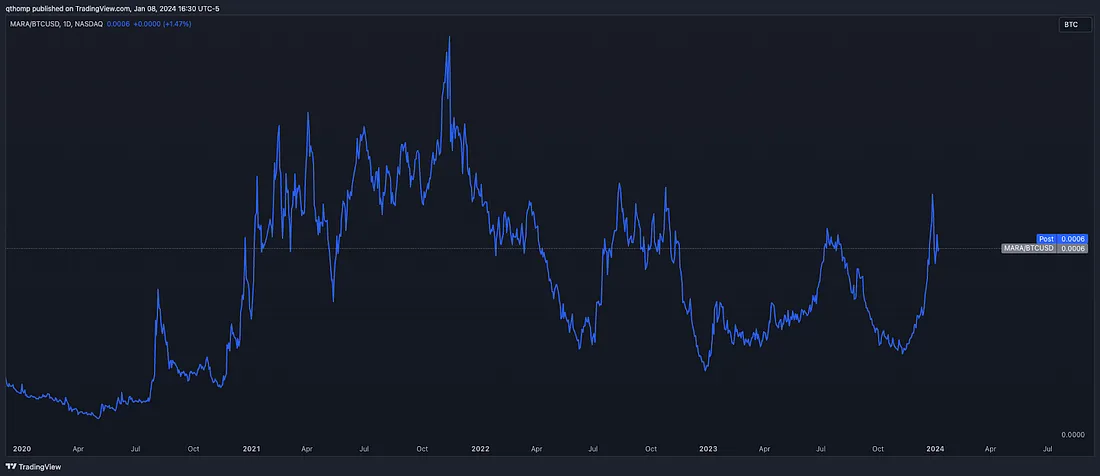

Marathon Digital Holdings (MARA)

The case against Marathon Digital Holdings is slightly more complex but equally bearish. MARA is a publicly traded Bitcoin mining company.

Publicly traded MARA has long been seen as a Bitcoin proxy, but once spot ETFs are available, this rationale disappears. Additionally, the halving is imminent, which will instantly cut revenue by 50%. This creates a powerful double whammy: ETFs benefit BTC while simultaneously harming miners.

The fundamental challenge facing MARA can be summarized as follows. Below is a chart of LTM hashprice—the expected revenue per unit of hashpower for miners. Broadly speaking, let’s assume most public miners need around 90+ PH/s hashprice to be considered a "good" business. The chart shows that even during recent surges in transaction activity, this threshold was never reached. All else equal, this figure will drop to record lows after the April halving, far below the levels seen at the end of 2022.

Two offsetting factors could mitigate this decline: falling hash rate due to unprofitable miners shutting down (short-term), and increased transaction activity (long-term). Historically, miner shutdowns reduce hash rate by about 20–30%, but recovery typically occurs within 1–3 months, suggesting such relief boosts profitability by only 25–40% temporarily. Given that this would occur from a new low base of 40–45 PH/s, short-term relief would bring hashprice only up to 50–60 PH/s—barely reaching pre-2022 lows. Conservatively assuming the duration of hash rate decline may last longer than before due to the magnitude of this halving seems fair, but this would trigger a race among miners to deploy new machines and increase efficiency. We don’t expect this, as all signs indicate these public companies will deliver and activate tens of thousands of new machines throughout the year.

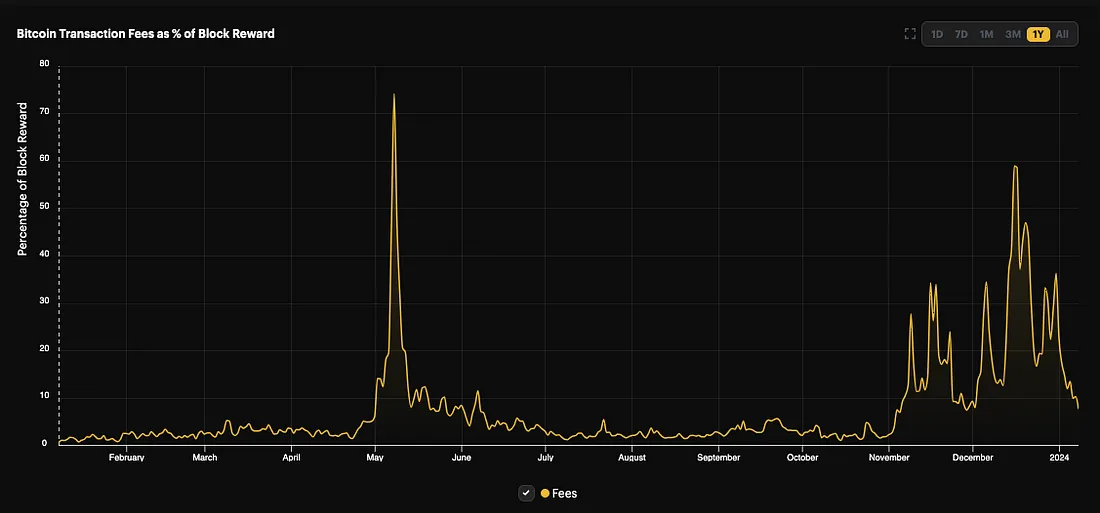

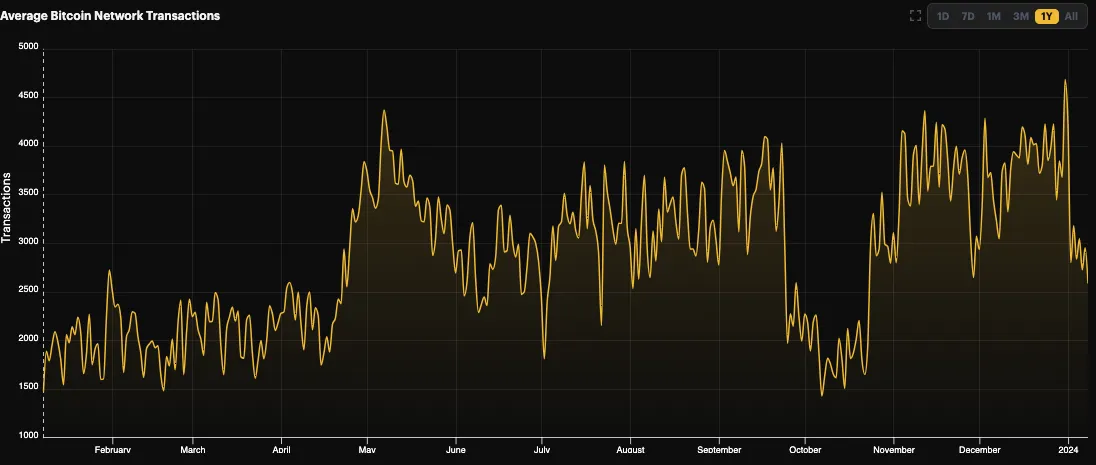

A second potential mitigant for MARA is rising fees and transaction volume driven by Ordinals, inscriptions, and NFTs built on the Bitcoin network. However, this activity is highly cyclical and often signals local peaks in sentiment, which we believe have already been reached mid-cycle. The charts below support this view, as both fee income and total network transactions have doubled.

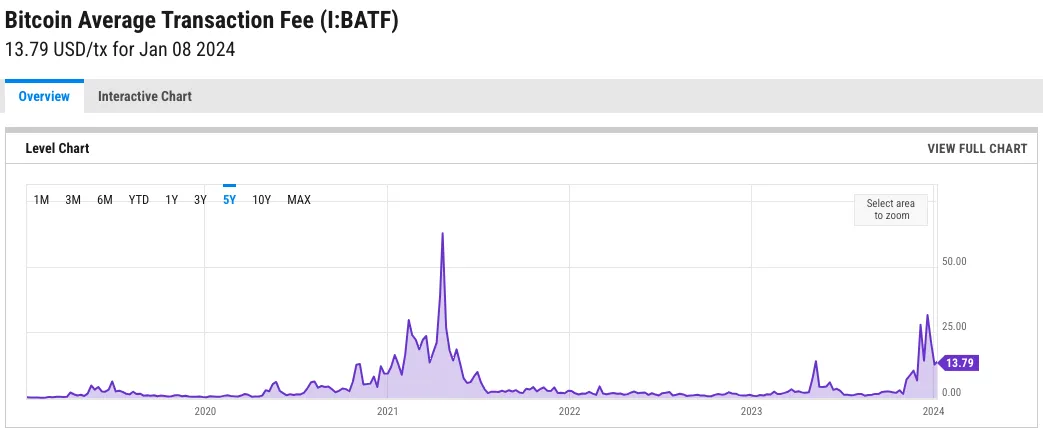

Average transaction fees on the BTC L1 network have ranged from $10 to $30 over recent months—comparable to 2021 highs—and are already becoming prohibitive, suggesting little room for sustained further increases.

For MARA, the third and final factor is a long-term structural issue, but still critical. Since miners cannot differentiate themselves in output or production (1 BTC = 1 BTC), the sole competitive advantage lies in cost structure. With global governments continuing loose monetary and fiscal policies, inflation remains sticky, and energy costs may have reached a local floor. While producers like RIOT and CIFR have contracted power agreements, most miners face price volatility risks—especially MARA, which already has the highest electricity costs in the industry.

This also affects broader interest rates and capital costs for these firms. Debt markets for these companies are effectively closed, and even where debt is available, most cannot afford the carrying costs. This leaves equity financing as the only means to extend runway, and they will inevitably be forced to pursue it. It’s important to remember that a miner’s worst action is shutting down machines due to lack of profitability—because then they have no business left, and most machines are worth pennies upon liquidation. Their second-worst action is issuing equity, which dilutes existing shareholders. This happens at every local top, and it has already begun—with Cleanspark’s recent offering as an example. Similar to the period from July to September 2023, we expect more such events ahead.

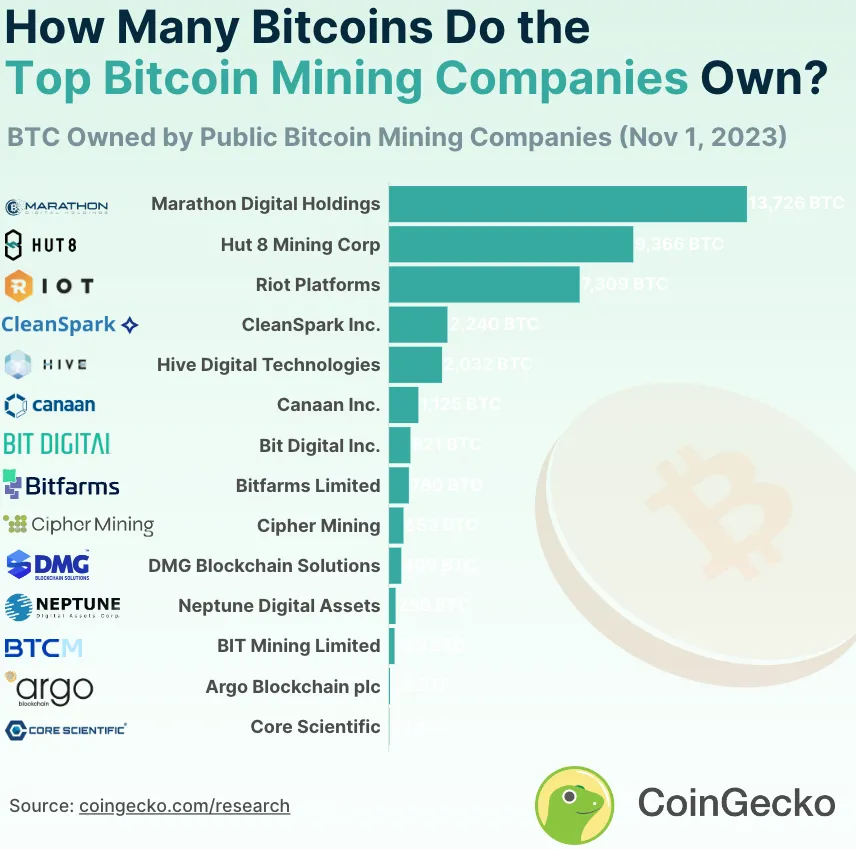

Bitcoin miners’ balance sheets may also impact the broader market. The largest listed miners collectively hold nearly $2 billion in BTC on their balance sheets. If operating conditions are expected to deteriorate significantly and public markets reassess the premium on these proxy assets, miners will face greater pressure to sell BTC to fund operations. Historically, during periods of tight profitability, miners almost always sell BTC on hand—first newly mined BTC, and only in desperation do they tap into held BTC. Such balance sheet sales could happen earlier this time, as post-halving threats to their businesses are more severe. After all, oil and gas producers don’t hold the commodities they produce to speculate on future price increases.

In the mining space, we view MARA as the best short candidate. It has the highest breakeven operating costs among peers and may lose out to competitors who can remain profitable with smaller BTC price appreciation. We believe MARA’s valuation of over $5 billion is excessive both relatively and absolutely.

Long-term, the MARA/BTC chart should follow hashprice, not Bitcoin price. Post-halving, we estimate miners will need BTC prices above $75,000 to restore current profitability levels. Given the magnitude of price increase required to restore margins, owning BTC directly is economically superior, and we expect the MARA/BTC ratio to return to or make new lows.

Coinbase (COIN)

The bear case for Coinbase is straightforward and aligns with the arguments made for the other two names regarding ETFs.

Additionally, some argue ETFs will benefit COIN as it may serve as a custodian. Further analysis reveals a more uncertain equation. While COIN may earn 5–15 bps in custody fees, it risks losing higher-margin retail trading volume, which will inevitably shift from Coinbase to ETFs. That retail business generates over 100 bps per trade. Thus, COIN would effectively replace high-margin, per-trade revenue with lower-margin custody fees.

Moreover, low-fee ETFs will put downward pressure on COIN’s overall fee structure. We’re already seeing early signs of this erosion as ETF issuers compete to lower fees. Most importantly, in our view, once spot BTC and ETH ETFs launch, retail users will have less incentive to open Coinbase accounts, potentially harming user growth trends. Finally, COIN currently trades at a rich valuation—around 35x 12-month EBITDA—which we believe may miss expectations and appears highly vulnerable to declining crypto sentiment.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News