Has Ethereum gotten closer to or further away from surpassing Bitcoin as we leave 2023 behind?

TechFlow Selected TechFlow Selected

Has Ethereum gotten closer to or further away from surpassing Bitcoin as we leave 2023 behind?

From the beginning of the year to now, the amount of Ethereum has decreased from 120.5 million to the current 120.1 million, with a total of 340,000 ETH burned over the year, worth 750 million U.S. dollars.

Author: Day, Baicai Blockchain

With the new bull market placing Bitcoin narratives at center stage, Ethereum's ecosystem—which had been highly anticipated during the bear market—has gradually weakened. Coupled with Solana’s explosive rise, the crypto industry seems to have entered 2024 under the narrative of "the emergence of new public blockchains."

Although Ethereum’s price has doubled over the past year, it still faces widespread criticism, with many even spreading FUD about Vitalik’s leadership decisions, claiming major issues exist within the decision-making layer. This phenomenon stems primarily from excessively high expectations for ETH (at least outperforming Bitcoin), as well as Solana’s exceptionally strong performance. Today, let's review what new developments have occurred in Ethereum’s ecosystem over the past year. (FUD: Fear, Uncertainty, Doubt—a term referring to negative sentiment spread to trigger investor panic.)

01 Ethereum Enters Full Deflation

From the beginning of the year to now, the total supply of Ethereum has decreased from 120.5 million to 120.1 million, with a total of 340,000 ETH burned—worth $750 million. As the bull market progresses, burn volumes are expected to increase significantly.

Ethereum total supply changes, Source: ultrasound.money

02 Explosion of the LSD Sector

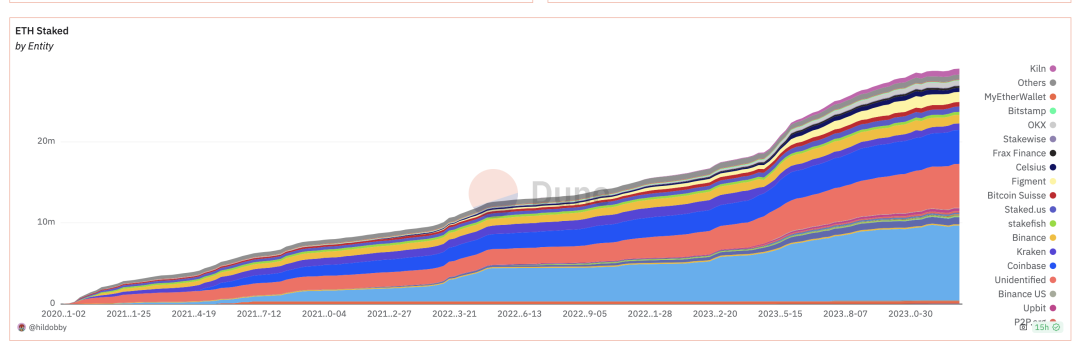

After Ethereum completed The Merge in September 2022, the Liquid Staking Derivatives (LSD) sector developed over several months and became a key trend in Q1 2023. During the tail end of the bear market, stable annualized yields of around 4% attracted significant capital inflows. LSD projects such as Lido, Rocket Pool (RPL), and SSV experienced explosive growth, pushing Ethereum’s staking ratio higher. By January 3, 2023, the total staked amount reached 28.8 million ETH.

Ethereum staking volume changes, Source: dune.com

As staked capital continued to grow and the Shanghai upgrade approached, a few early movers began targeting this locked capital by launching DeFi products that layered on top of each other to improve capital efficiency. After generating visible wealth effects, more institutions and capital poured into related sectors, giving rise to the LSDFi niche and gradually improving LSD-related infrastructure.

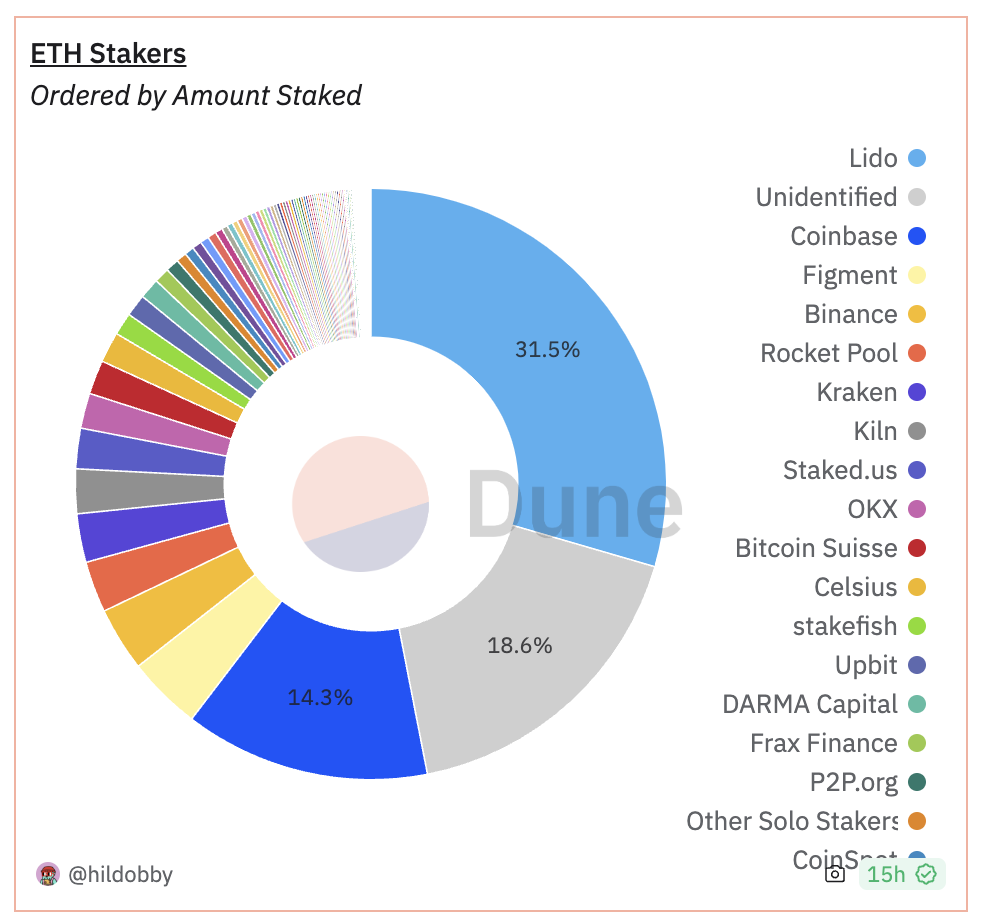

While there are positive aspects, dissatisfaction also emerged. As staking ratios increased, Lido came to control over one-third of Ethereum’s staking market share, raising concerns about excessive centralization in the staking space. Market participants began questioning whether Lido’s dominance could threaten Ethereum’s consensus security. Opinions remain divided on whether Lido’s centralization poses real risks.

On December 28, Vitalik introduced DVT (Distributed Validator Technology), which aims to address these concerns by decentralizing validator operations while maintaining centralized staking. In fact, as early as November 28, 2023, the Lido DAO had already begun adopting DVT technology provided by Obol Network and SSV Network.

Market share distribution among staking projects, Source: dune.com

With the arrival of the bull market and Ethereum’s price appreciation, the Ethereum staking sector becoming a multi-billion dollar market is almost certain. Additionally, as the industry matures, stable yield products will likely become essential for some users, making future innovation and development in this space worth watching.

03 Layer2 Proliferation

Layer2 solutions have become an integral part of Ethereum. Each Layer2 network has made unique progress, showcasing distinct characteristics. Let’s briefly review them.

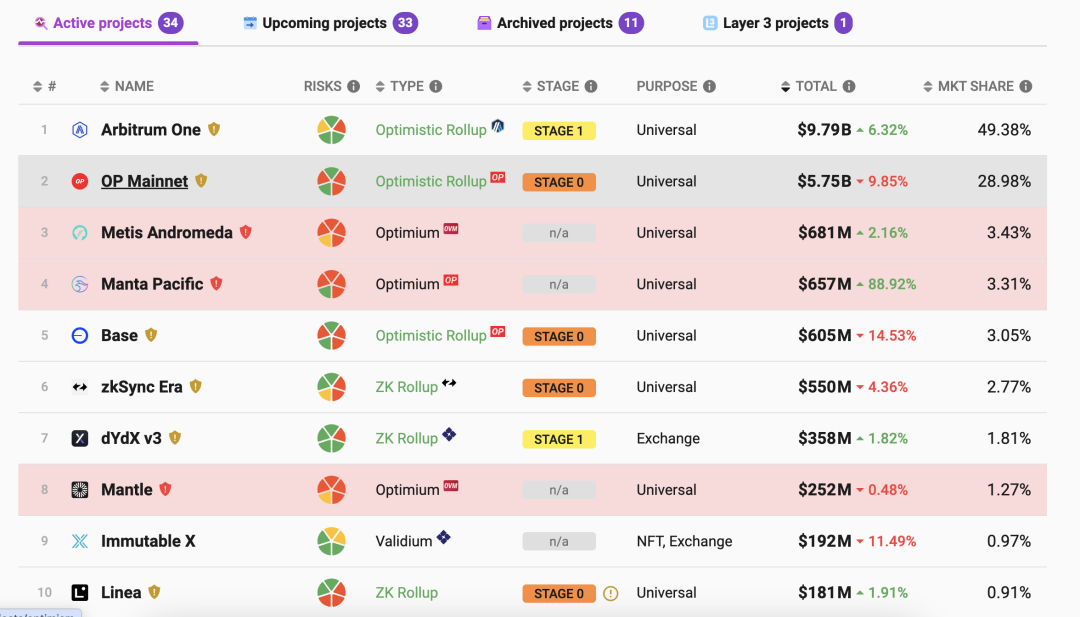

Top 10 Layer2 TVL rankings, Source: L2 Beat

-

Optimism

Following the establishment of the bear market bottom in 2022, Optimism’s token saw a surge in early 2023. Although its ecosystem is clearly weaker than Arbitrum’s, the project carved out a different path—leveraging modular design and OP Stack’s one-click chain deployment technology to partner with multiple projects, including Base, opBNB, Manta Network, and DeBank, all choosing to build using OP Stack. Recently, confirmation of the timing for the Cancun upgrade has brought renewed attention to Optimism and other Layer2s.

-

Arbitrum

In Q1 last year, following the launch of Arbitrum’s token, its ecosystem exploded—so much so that it was dubbed “Arbitrum Summer.” Notable projects included GMX, MAGIC, RDNT, GNS, and AIDOGE, most of which have since been listed on Binance.

However, both Optimism and Arbitrum suffer from the same issue common to “institutional tokens”—high market cap but low circulating supply. Over the past year, despite rapid increases in their circulating market caps, token prices have remained stagnant, effectively turning them into “ATMs” for institutions, offering only scraps to retail investors—even when the underlying projects perform well.

-

zkSync & StarkNet

zkSync and StarkNet are often seen as the twin masters of community manipulation in the industry. They’ve profited handsomely from transaction fees while alienating yield farmers—especially StarkNet, whose controversial moves have turned the community against the team. zkSync continues its long-running marketing campaign, with rumors suggesting a token launch in 2025. However, ZK progress has generally been slow, and neither project achieved anything notable in 2023.

-

Base

Base attracted significant capital in a short time due to short-term wealth effects, rising quickly with waves of traffic—though most of its ecosystem projects proved short-lived. In early August, just before Base’s mainnet launch, a meme token called Bald surged 1,000x, reaching a $100 million market cap in two days. The massive FOMO effect drew in users, though the project ultimately rug-pulled. Still, much of the capital remained on-chain.

Shortly afterward, Friend Tech—a social protocol leveraging a Ponzi-like model combined with Paradigm’s institutional backing and anticipated airdrops—became one of the few breakout products in the bear market, bringing hundreds of thousands of users to Base and solidifying its position among Layer2s. However, Friend Tech has since cooled down significantly.

-

Blast

Launched on November 21, Blast leveraged Blur’s existing user base and an airdrop-driven Ponzi model. Despite controversy over centralized wallet management, it achieved over $1 billion in TVL within about two months and has become another destination for large-scale stable-yield strategies.

-

Manta Pacific

In less than three weeks, Manta Pacific’s TVL surged from $30 million to $650 million. Similar to Blast, it runs a yield program through its New Paradigm campaign, attracting deposits for airdrop eligibility. Its selling point? Shorter lock-up periods and higher capital efficiency compared to Blast.

-

Metis

With the upcoming Cancun upgrade, Metis has recently surged, delivering strong short-term performance and rising into the top three by TVL. Most Layer2s face issues with overly centralized sequencers, and Metis specifically focuses on decentralized sequencer solutions. Whether this rise is driven by genuine technical merit or capital influence remains open to interpretation.

-

ZKFair

By distributing 100% of its tokens via gas fee airdrops to all community users, ZKFair rapidly attracted participation. Within a week of launching its gas airdrop campaign, the chain consumed over 60 million USDC in gas fees, surpassed 200,000 active addresses, and achieved over $120 million in TVL—though activity declined after the event ended. With its emphasis on fair distribution, it stands out as refreshingly user-friendly for those tired of being teased by zkSync and StarkNet. Future developments warrant close observation.

Clearly, Layer2 development is now characterized by teams leveraging their respective strengths. As market conditions improve, growth is accelerating and becoming increasingly direct—many projects no longer require months or years of gradual buildup. Instead, they use aggressive incentives to explode onto the scene and capture market share. Whether they can sustain momentum remains to be seen.

04 Rise of Dex Bots

Before BRC20 inscriptions gained traction, over 90% of meme coin launches occurred on Ethereum, with dozens or even hundreds of new projects emerging daily. Some players constantly monitor on-chain activity hoping for outsized returns. As participant numbers grew, powerful tools became essential for investors—and Dex Bots emerged in this environment.

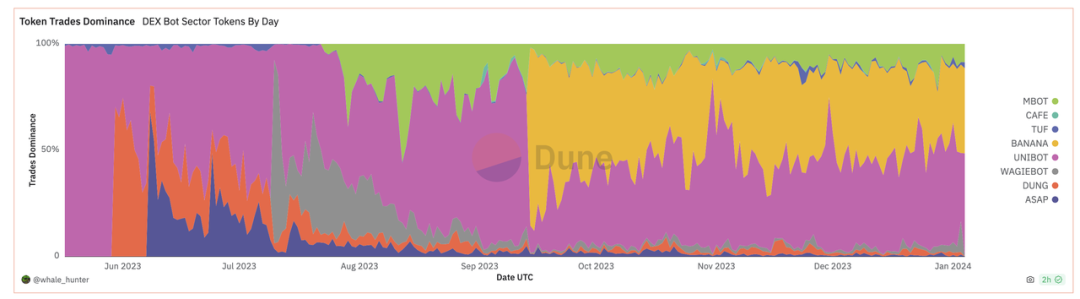

In mid-May, Unibot launched and became a breakout product within just over two months, earning millions in profit even during the bear market and triggering a frenzy around the entire Dex Bot concept. However, after Banana Gun launched in September with superior usability, Unibot lost significant market share. More recently, with attention shifting toward Bitcoin and Solana, Ethereum’s on-chain trading volume has plummeted, naturally reducing demand for Dex Bots. Still, as a newly emerged narrative in 2023, it deserves ongoing attention.

Dex Bot trading market share, Source: dune.com

05 Ethereum Inscriptions & Memes

The emergence of Ethscriptions—an Ethereum inscription protocol—is essentially a direct copy of Bitcoin’s Ordinals protocol. Since its inception, it has faced widespread rejection, with mainstream opinion viewing it as a step backward. Yet riding the wave of Bitcoin’s ecosystem boom and other factors, it too gained traction.

Currently, apart from ETHs, no other standout projects exist in the Ethereum inscription space. While there have been minor innovations and combinations of runes with NFTs, most are short-term speculative plays that result in chaos once the FOMO fades. Similarly, the inscription minting craze on new blockchains creates temporary excitement, stress-testing various chains’ performance—but ultimately results in short-lived booms. Anyone who buys in late ends up trapped, without exception. Whether this sector can develop new narratives or meaningful innovations going forward remains to be seen. (Note: FOMO – Fear Of Missing Out)

Meme coins, as one of the dominant narratives in the previous cycle, produced breakout projects like Doge and Shiba Inu. This cycle, PEPE reignited activity on Ethereum. In mid-2023, users began expressing FUD toward institutional tokens, believing new project launches existed solely to dump holdings, leaving retail investors holding the bag.

Meme coins directly addressed this pain point—offering relatively fair distribution, community-driven governance, zero barriers to entry, and open participation for anyone. The later explosion of BRC20 is closely related to this dynamic. While most meme projects are fleeting, achieving brief viral fame before fading away—with very few achieving lasting success—they remain one of the closest and most accessible sectors for retail investors.

06 Others

Beyond the above, other sectors performed modestly.

In DeFi, RWA initiatives led by Maker began expanding outward but received lukewarm responses. Legacy DeFi platforms like Uniswap focused on internal improvements—implementing minor technical upgrades and launching cross-chain expansion plans to capture greater market share.

In gaming, the sector is completely dormant. While some games launched on alternative chains and cross-chain gaming saw limited progress, no breakout hits emerged to ignite the market.

In NFTs, Yuga Labs made efforts in gaming but saw little impact. Their own NFT collections made minimal progress this year. Azuki raised 20,000 ETH in June but delivered a product that simply copied the “Red Beans,” draining liquidity from an already thin NFT market and causing the Red Bean series to sharply decline. Regarding NFT marketplaces, OpenSea’s valuation dropped from a peak of billions to just $140 million or less, with institutional investors losing over 90%. Blur continues to eat into OpenSea’s market share. On Ethereum, the space is now a fiercely competitive red ocean where standing out is extremely difficult. In contrast, Bitcoin presents a blank slate—entirely undeveloped and ripe for replication of Ethereum’s successes.

07 Summary

The above covers the key innovations I’ve observed in Ethereum’s ecosystem this year. Concepts like account abstraction and AI are under development but haven’t produced breakout applications yet, so they’re not included here.

On another note, due to Ethereum’s recent underperformance, many have started spreading FUD, blaming Vitalik’s strategic decisions—arguing that delegating tax authority could lead to Layer2 fragmentation and weaken Ethereum’s value capture. Opinions on this remain deeply divided.

Finally, two upcoming catalysts worth anticipating: the Cancun upgrade, which will benefit Layer2s; and the potential approval of an Ethereum ETF following the greenlighting of a Bitcoin ETF.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News