Unpacking MakerDAO RWA: Exploring DeFi's Governance System and Transaction Architecture for Capturing Off-Chain Assets

TechFlow Selected TechFlow Selected

Unpacking MakerDAO RWA: Exploring DeFi's Governance System and Transaction Architecture for Capturing Off-Chain Assets

This article will cover relatively mature RWA projects within MakerDAO.

Author: Will Wang

Real-world assets (RWA) exist off-chain, from which asset owners can derive expected returns. Ownership rights and associated benefits are governed by legal systems rooted in our social contracts. For on-chain DeFi built upon the principle of "Code is Law," adapting to off-chain governance structures and legal frameworks—so as to enable crypto capital to securely and compliantly capture real-world assets—is a critical challenge that must be explored and resolved.

Following our previous analysis of RWA tokenization pathways via Centrifuge, this article examines how decentralized on-chain protocols like MakerDAO govern, structure legally, and practically engage with real-world assets. We hope this provides valuable insights for teams building RWA projects, and welcome further discussion and collaboration.

This article covers several mature RWA initiatives within MakerDAO, including New Silver Restructuring, BlockTower Credit, BlockTower Andremeda, Monetalis Clydesdale, and Centrifuge’s transaction architecture supporting Aave.

1. Why Should DeFi Capture Off-Chain Real-World Assets?

The narrative around RWA is essentially also the narrative around MakerDAO’s vision for DeFi. It is therefore crucial to understand the significance of RWA in the broader DeFi ecosystem through MakerDAO's lens.

MakerDAO is a decentralized autonomous organization (DAO) responsible for managing the Maker Protocol, which operates on Ethereum. The protocol introduced DAI—the first decentralized stablecoin (essentially an Ethereum-native dollar)—and a suite of derivative financial instruments. Since its launch in 2017, DAI has consistently maintained its peg to the US dollar.

During the 2021 DeFi Summer, numerous unsustainable yield-generating products emerged, ultimately triggering a market crash and widespread credit defaults across the ecosystem. While native crypto assets remain central to DeFi’s long-term value proposition, current demand cannot always align with sustainable development goals.

Due to the high volatility of cryptocurrency markets, reliance on a single collateral type may lead to massive liquidations. For large lending protocols like MakerDAO, a key consideration is the stability of collateral value. Previously, MakerDAO accepted volatile cryptocurrencies as collateral, introducing significant risk into borrowing activities and severely limiting its scalability.

Thus, MakerDAO—and DeFi more broadly—urgently needs a more stable foundational layer of collateral (a Baselayer Level of Collateral) to support widespread adoption of the DAI stablecoin and establish a sustainable, scalable pathway.

(Centrifuge & Maker: A Partner's View of Real-World Assets)

RWA has become one of MakerDAO’s most important topics, continuously debated and validated by the community as a vital solution. In its Endgame Plan released in May 2022, MakerDAO emphasized that incorporating RWAs as collateral is a key component of building a decentralized stablecoin.

Benefits of RWA include:

(1) Increased transparency in market risks and asset usage;

(2) Enhanced composability within DeFi;

(3) Improved accessibility for underbanked and underserved populations;

(4) Value capture from larger, more stable traditional financial markets.

For MakerDAO, RWA offers two crucial characteristics: stability and scalability. More specifically, DAI can expand its utility by being backed by non-volatile, yield-generating, and scalable real-world assets—especially relevant in today’s environment where crypto yields are low while U.S. Treasury yields remain high. By capturing value from RWAs, MakerDAO can continue growing even during bear markets and prepare thoroughly for the next bull cycle.

Most importantly, RWA enables MakerDAO to realize its grand vision: providing a credit-neutral, decentralized channel that enhances utility for everyday life and business financing needs. Through open, on-chain, community-driven, programmable, and decentralized protocols, it aims to create a new open DeFi financial market.

However, bringing real-world assets on-chain is not easy. It presents challenges in product architecture design, financial and legal compliance, technical risks, and unknown unknowns.

2. How Can DeFi Capture Off-Chain Real-World Assets?

After establishing the need for DeFi to capture real-world assets, we must now build governance systems and legal architectures suitable for on-chain protocols or DAOs. Some might argue this isn't necessary—why not simply purchase third-party tokenized U.S. Treasuries? It would save time and effort.

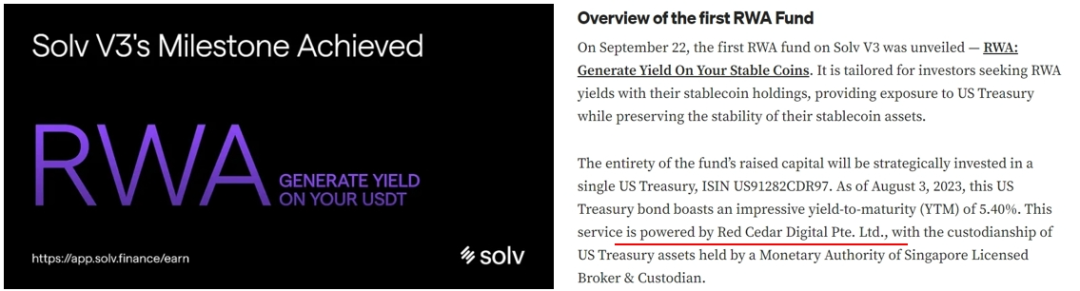

For example, consider Solv Protocol, a successful on-chain fund project. With its V3 release, it launched two RWA funds managed by Solv RWA, currently overseeing $2 million in total value locked (TVL). KYC/AML-compliant users can deposit stablecoins to earn U.S. Treasury yields. According to their press release, these RWA funds are backed by tokenized U.S. Treasuries provided by Red Cedar Digital Ltd.

(Solv V3's Milestone Achieved: The First Ever RWA Fund Launch)

For smaller-scale projects operating under manageable risk conditions, directly purchasing third-party tokenized U.S. Treasuries may suffice. However, several questions still arise:

(1) How can we ensure the counterparty providing the underlying assets (e.g., Red Cedar Digital Ltd.) won’t go bankrupt or abscond? Recall the once-dominant FTX;

(2) Furthermore, if the counterparty does go bankrupt, how can a chain-based protocol without legal personhood participate in court-supervised asset liquidation or restructuring?

While building internal governance and legal frameworks may incur high costs for DeFi projects, they serve as essential hedges against risk. Regardless, studying successful RWA cases helps inform strategic decisions tailored to specific needs.

2.1 The Necessity of Legal Wrappers for DeFi

MakerDAO, managing billions of dollars in RWA exposure, considers identifiable risks from both fund security and legal entity perspectives. These include:

Counterparty risk: Consider scenarios where counterparties go bankrupt or disappear. MakerDAO must ensure no third party—including fund managers or investment advisors—can directly control, manage, or transfer its substantial funds.

Entity qualification: On-chain protocols or DAOs cannot complete customer identification requirements (KYC/AML) needed to legally own off-chain assets, thus preventing lawful purchase or ownership.

Similarly, they cannot hold intellectual property (IP) assets.

Bankruptcy claim eligibility: If off-chain assets default, face bankruptcy, or require liquidation, the on-chain protocol or DAO—lacking legal status—cannot interact directly with courts or insolvency administrators. Therefore, MakerDAO must have mechanisms to exercise rights over off-chain assets promptly through proper governance and legal structures.

Hence, it becomes imperative to use legal wrappers to construct governance and legal frameworks for on-chain protocols or DAOs. By bridging DAO governance with corporate legal governance, DeFi can achieve effective control over real-world assets.

(The DAO Legal Wrappers and Why You Need Them)

2.2 How DeFi Implements Legal Wrapping

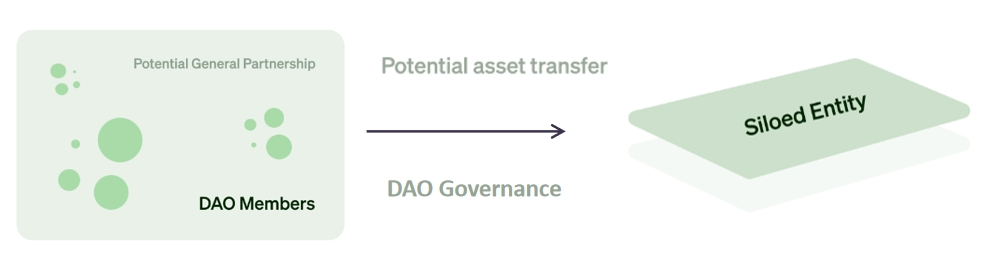

A legal wrapper is a collection of legal frameworks or legal entities specifically designed for on-chain protocols or DAOs, granting them recognized legal standing within certain jurisdictions. Its essence lies in “wrapping” the on-chain protocol or DAO within a legal framework—or establishing a subordinate legal structure—thereby enabling interaction with the real world and connecting with traditional legal systems.

Legal wrapping does not absorb or replace the DAO; the on-chain protocol continues operating as before. Only certain functions and responsibilities are delegated to the legal entity, allowing the DAO to gain legal protection, manage tax and regulatory obligations, sign contracts, own assets, make legal payments, and conduct real-world operations. The DAO and multisig wallets retain direct control over smart contracts, treasuries, and all on-chain assets, funding the legal entity only when necessary.

Therefore, from an RWA perspective, we can establish dedicated legal entities beneath on-chain protocols or DAOs for specific purposes, enabling efficient capture of off-chain asset value.

2.3 How DeFi Governs Off-Chain Legal Entities

Let us further illustrate using MakerDAO, currently the largest player in RWA implementation.

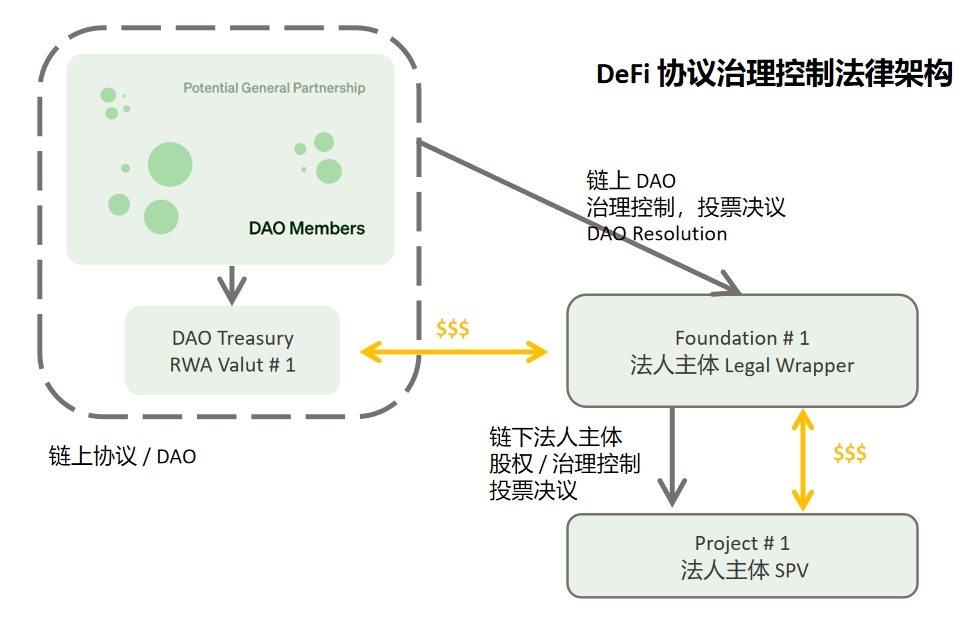

The diagram above shows the Foundation + SPV structure proposed under MakerDAO MIP58, specifically established for RWA projects. This setup allows value capture from underlying RWA through governance control over the foundation legal entity.

First, MakerDAO established RWA Foundation #1 under Cayman Islands law (the Foundation Company Law of the Cayman Islands 2017), creating a flexible governance framework for on-chain protocols or DAOs.

Internally, the foundation—as a legal entity—requires no minimum capital, shareholders, or members, making it a single-purpose, independent orphan entity. Like a trust, it can designate MakerDAO or its members as beneficiaries. It also ensures bankruptcy remoteness: even if MakerDAO or the foundation ceases operations (“goes dark”), neither affects the other.

Externally, the foundation enables:

(1) Interaction with off-chain entities (e.g., signing agreements, delivering services);

(2) Legally holding off-chain assets/IP after completing KYC/AML;

(3) Protecting DAO members with limited liability;

(4) Representing the DAO in executing off-chain actions based on DAO resolutions.

Second, the foundation’s organizational documents—such as Articles of Association and Memorandum of Association—can be customized for MakerDAO’s governance. For instance, the charter can stipulate that the foundation executes only MakerDAO resolutions and makes no independent decisions. Supervisors and Directors appointed by MakerDAO assume fiduciary duties and act according to granted powers (e.g., Power of Attorney), ensuring full governance control by MakerDAO at the legal entity level.

Finally, based on MakerDAO resolutions, Foundation #1 acts as an independent orphan holding company owning equity interests in SPV #1. SPV #1 is incorporated locally according to the jurisdiction of the underlying asset and acquires off-chain assets funded by Foundation #1. For example, if the asset is located in the U.S., a Delaware LLC can serve as the SPV, financed via a loan agreement between Foundation #1 and MakerDAO.

Although some other projects adopt SPV + Trust structures, the general principles remain:

(1) Ensuring governance control by the on-chain protocol or DAO;

(2) Making the DAO or tokenholders the beneficiaries;

(3) Enabling the wrapped legal entity to legally, effectively, and promptly dispose of assets.

3. MakerDAO’s RWA Case Studies

Since participating in the Solar X energy project financing, MakerDAO has gradually developed a viable RWA pathway for DeFi—using legal wrappers (Foundation + SPV or Trust)—to capture value from off-chain assets. Despite variations, the core transaction structure remains consistent.

Below are several notable RWA projects by MakerDAO, including New Silver Restructuring, BlockTower Credit, BlockTower Andremeda, Monetalis Clydesdale, and Centrifuge’s transaction model for Aave.

3.1 MakerDAO – New Silver Restructuring (Credit Asset RWA)

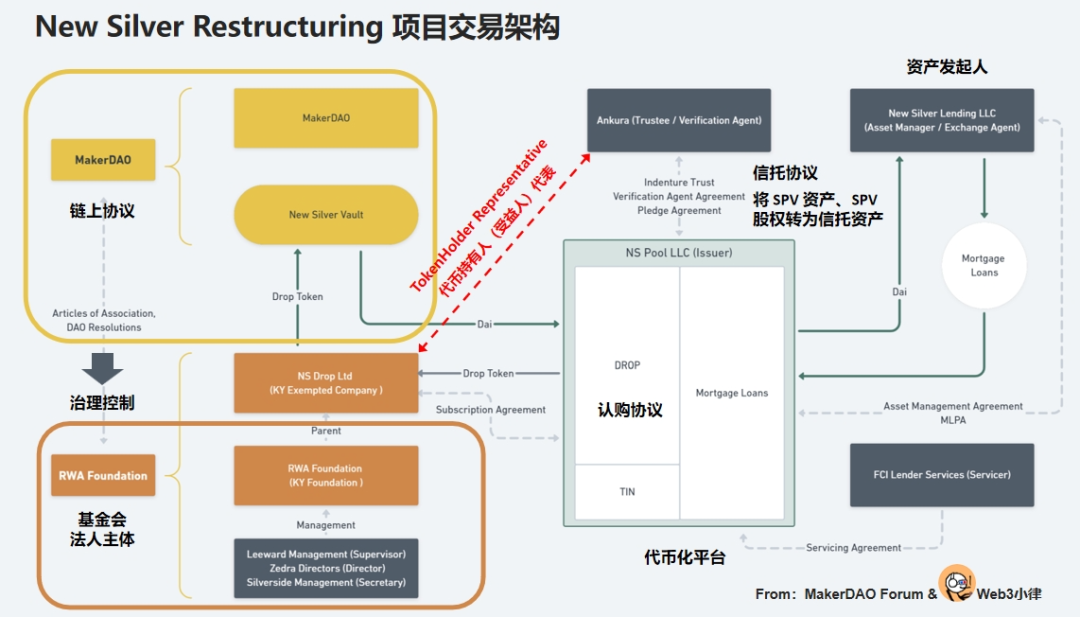

New Silver was MakerDAO’s first official RWA project, launched in 2021 with a debt ceiling of $20 million. The underlying asset consists of mortgage loans originated by New Silver, tokenized via an issuer SPV on Centrifuge’s platform.

In November 2022, the community proposed an upgrade and restructuring of the 2021 New Silver project. This restructured version fully adopted the Foundation + SPV model—an exemplary case study.

Key participants in the New Silver Restructuring transaction architecture include:

RWA Foundation: Established in 2021 and previously operated the Huntingdon Valley Bank (HVB) project, this foundation is under MakerDAO’s governance. Governance documents specify that foundation directors must act solely based on MakerDAO Resolutions, ensuring complete control at the legal entity level through combined on-chain DAO governance and off-chain foundation governance.

NS DROP Ltd: A wholly-owned subsidiary of the RWA Foundation, serving as the execution entity. It subscribes to DROP tokens issued by the borrower on Centrifuge, represents MakerDAO as token holder (DROP/TIN), exercises delegated rights per MakerDAO Resolutions, and instructs trustee Ankura Trust on various asset operations.

Ankura Trust: Ensures independence of the issuer SPV’s assets and safeguards MakerDAO’s funds. Under the trust agreement between the SPV and Ankura Trust, the SPV’s loan assets are pledged along with its equity, protecting MakerDAO’s asset integrity and enabling timely, adequate remedies in case of default—ensuring fund safety.

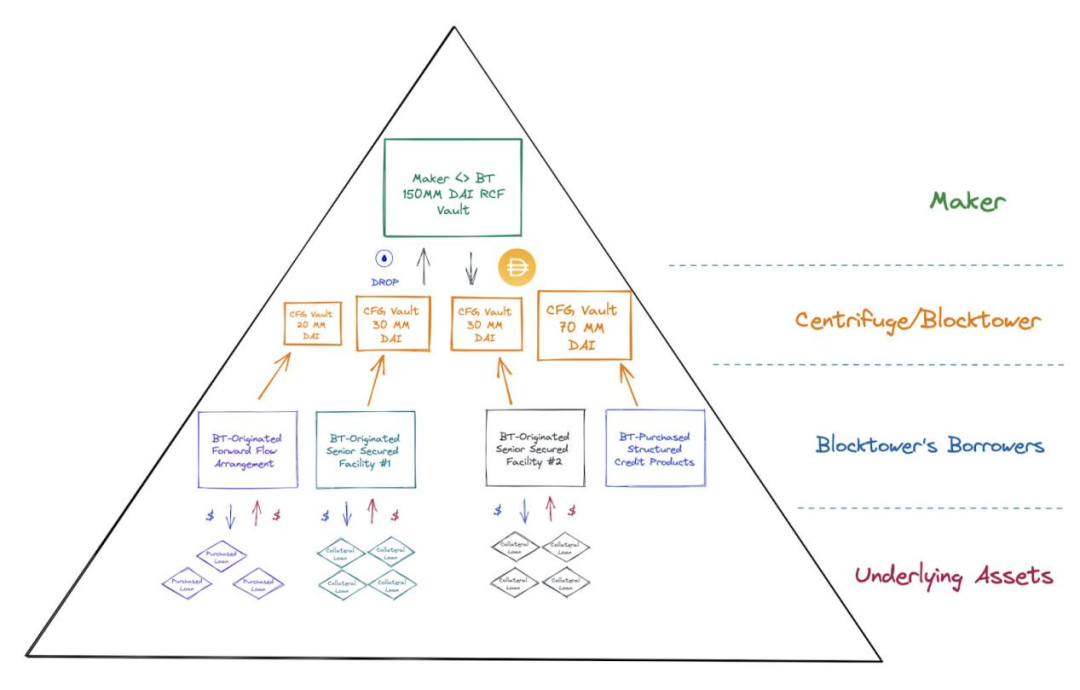

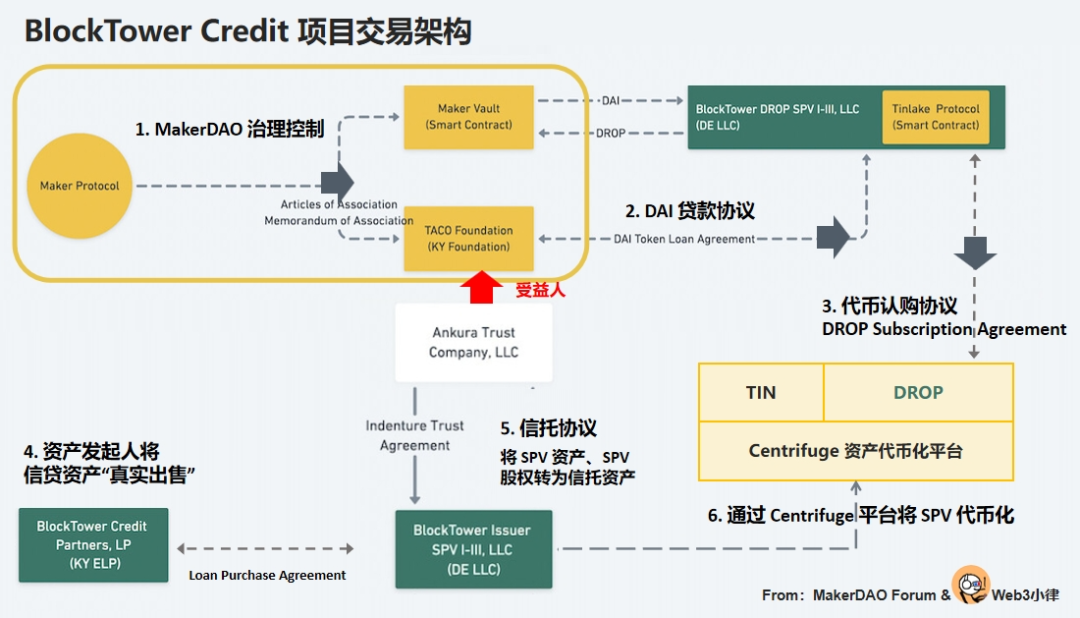

3.2 MakerDAO – BlockTower Credit (Credit Asset RWA)

BlockTower Credit is a credit asset tokenization initiative launched by BlockTower Capital in November 2022, with a total debt limit of $150 million split across four asset pools. As originator, BlockTower Credit raises funds via an issuer SPV on Centrifuge’s tokenization platform.

(BlockTower Credit - Commercial and Legal Risk Assessment - Part I)

BlockTower Credit’s transaction structure closely mirrors New Silver Restructuring. We break it down into two parts:

On the funding side: securely and compliantly moving on-chain assets off-chain while retaining control within MakerDAO;

On the asset side: tokenizing off-chain assets and securing funding from MakerDAO.

From MakerDAO’s DeFi perspective:

1. MakerDAO first achieves governance control over the TACO Foundation (similar to the RWA Foundation, both governed by MakerDAO);

2. The TACO Foundation provides DAI funds to Blocktower DROP SPV under a loan agreement, secured by DROP tokens;

3. These funds are used to subscribe to DROP tokens on Centrifuge, issued by an SPV holding BlockTower’s underlying assets.

From the asset financing perspective:

4. BlockTower Credit Partners, as originator, transfers credit assets into the issuer SPV via “true sale”;

5. To safeguard asset independence and fund security, the issuer SPV enters a trust agreement with Ankura Trust, pledging both the loan assets and SPV equity, with DROP/TIN token holders (i.e., TACO Foundation) as beneficiaries—ensuring asset integrity and prompt enforcement upon default;

6. The issuer SPV issues two token types—DROP (senior tranches, subscribed by TACO) and TIN (junior tranches, subscribed by BlockTower Credit Partners)—via Centrifuge’s asset tokenization platform.

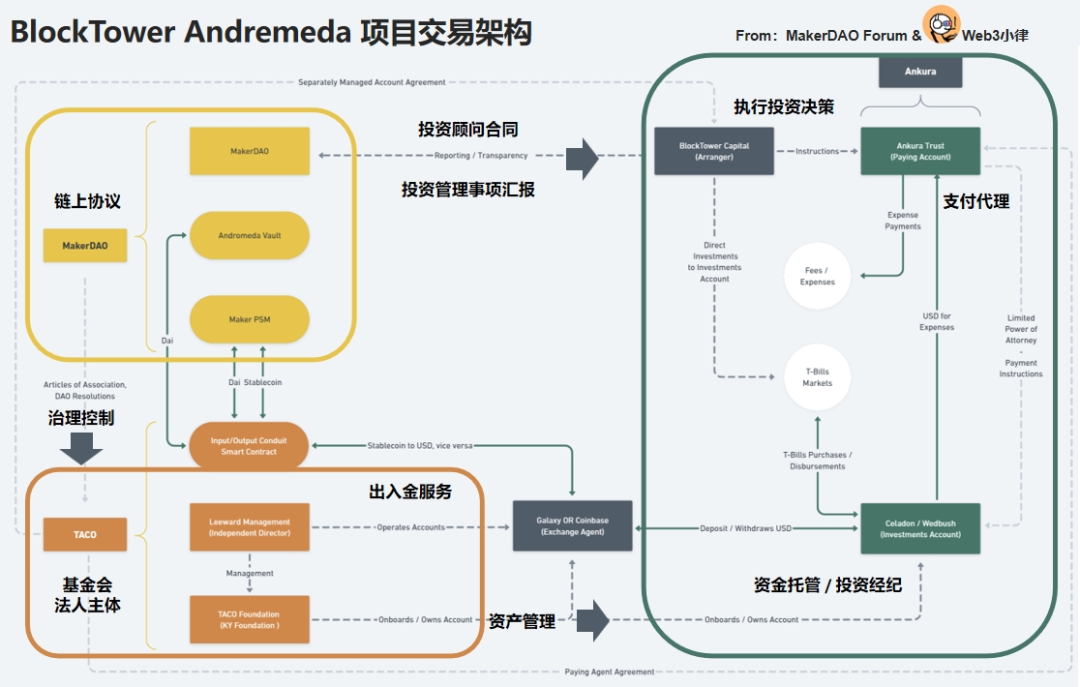

3.3 MakerDAO – BlockTower Andremeda (U.S. Treasury RWA)

BlockTower Andremeda is one of MakerDAO’s largest RWA projects, with a debt ceiling of $1.28 billion and current assets exceeding $1 billion. Initiated by BlockTower Capital and executed via the TACO Foundation, this U.S. Treasury RWA project aims to diversify treasury holdings by investing in off-chain U.S. Treasuries.

Key participants in the BlockTower Andremeda structure include:

TACO Cayman Foundation: Established in 2022, previously managed the $150 million BlockTower S3/S4 credit asset RWA projects. Like the RWA Foundation, it is governed by MakerDAO. Per Article 4.16 of its Articles of Association, foundation directors must act exclusively based on MakerDAO Resolutions.

BlockTower Capital serves as investment advisor, managing accounts and making investment decisions under contract with TACO Foundation. Coinbase and Galaxy Digital act as on/off-ramp providers; Celadon Financial Group as broker executing trades; Wedbush Securities Inc. as custodian; and Ankura Trust as paying agent.

In this structure, MakerDAO primarily uses the TACO Foundation as a legal signatory to fulfill off-chain investment obligations, adopting the traditional finance practice of separating investment decision-making from custody for risk-compliant operations.

Compared to BlockTower Credit, the similarity lies in governance: both rely on the combination of MakerDAO’s on-chain governance and foundation-level off-chain governance to ensure full control.

The difference lies in value capture: Andremeda directly invests funds—via on/off ramps, investment advisors, brokers, custodians, and paying agents—into U.S. Treasuries through the TACO Foundation. In contrast, the BlockTower S3/S4 projects, due to different underlying assets, incorporate an additional SPV layer to capture assets tokenized via Centrifuge.

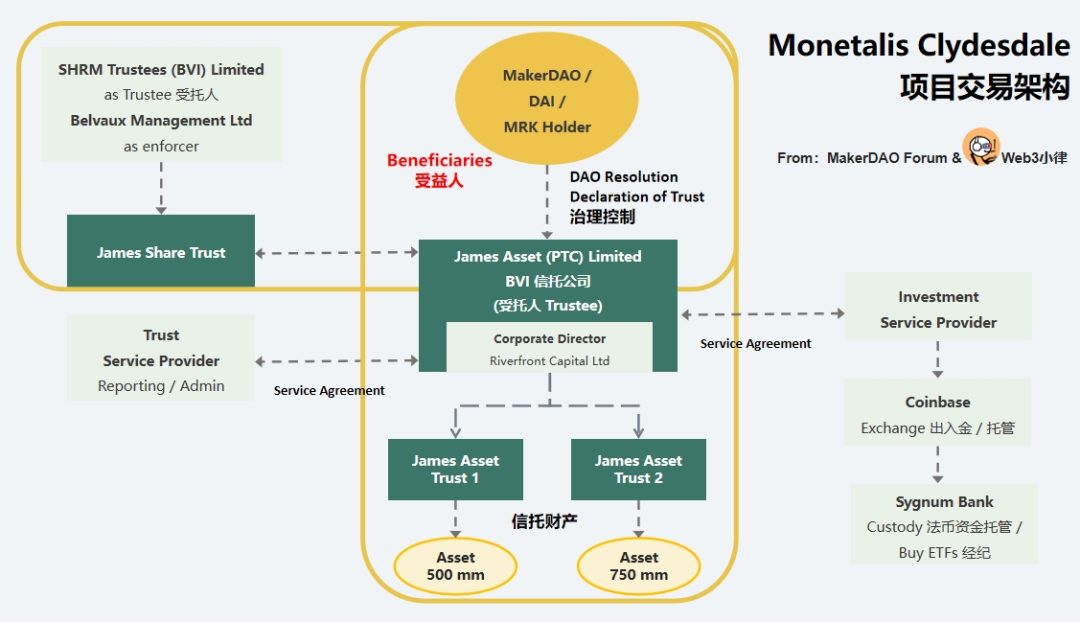

3.4 MakerDAO – Monetalis Clydesdale (U.S. Treasury RWA)

Despite BlockTower’s success within MakerDAO, concerns remain about excessive counterparty concentration—for example, BlockTower playing multiple roles such as investment advisor and originator.

To address this, Monetalis Clydesdale, initiated by Monetalis founder Allan Pedersen, explores a safer RWA path. Proposed in January 2022 and approved/executed in October 2022, the project started with a $500 million debt ceiling, raised to $1.25 billion in May 2023, investing in U.S. Treasury ETFs.

In Monetalis Clydesdale’s transaction architecture, the funding side is critical: how to convert on-chain assets securely and compliantly off-chain while keeping control within MakerDAO.

Establishment of a Property Trust: First, JAL—a BVI trust company—is formed. It establishes the James Asset Trust via a Declaration of Trust. JAL, as trustee, holds DAI/ETF trust assets provided by MakerDAO, with MakerDAO MKR tokenholders as beneficiaries. Governance documents allow MakerDAO to control the trustee’s actions regarding asset purchases and dispositions.

MakerDAO’s Governance Control:

Per the Declaration of Trust, the trustee JAL must act only upon MakerDAO Resolutions;

All actions require approval and confirmation by a transaction manager verifying the MakerDAO Resolution; JAL cannot take any action outside of MakerDAO Resolutions.

Establishment of an Equity Trust:

Once governance over JAL’s trust property is secured, JAL’s equity itself becomes trust property forming the James Asset Share Trust. SHRM Trustees (BVI) Limited acts as trustee, Belvaux Management Ltd as enforcer, and MakerDAO MKR holders as beneficiaries.

This dual-trust structure enables MakerDAO to control both JAL’s trust assets (representing DAI) and JAL’s equity (representing the trustee itself). All operations require verification of MakerDAO Resolutions, and fund flows bypass third-party control (MakerDAO Vault → JAL Trust Account → Sygnum Bank Custody Account).

With this architecture, MakerDAO achieves:

(1) Minimal or zero counterparty risk—third parties or managers cannot alter legal terms or access funds;

(2) Seamless on-chain/off-chain governance integration;

(3) Trust mechanisms enabling MKR holders to promptly respond to default and liquidation risks;

(4) Clearly defined fund usage with no misappropriation risk.

Subsequent asset investments by trustee JAL are relatively straightforward: converting DAI to USD via Coinbase, then using Sygnum Bank for custody and ETF trading.

3.5 Centrifuge – RWA Roadmap (U.S. Treasury RWA)

Centrifuge participated early in several MakerDAO credit asset RWA projects, such as New Silver Restructuring and BlockTower Credit. Specific processes are not detailed here; readers interested can refer to our prior article: *Decentralized Asset Financing Protocol Centrifuge Through the Lens of RWA Essence*.

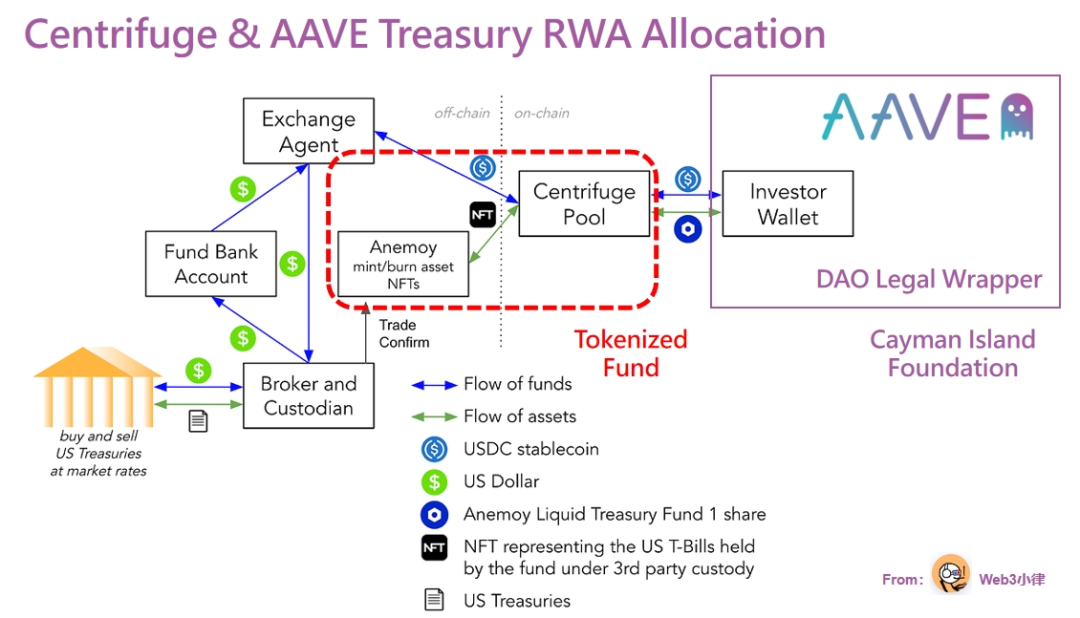

Here, we focus on Centrifuge Prime, a service helping crypto capital, DeFi protocols, and DAO treasuries capture yield from real-world assets like risk-free U.S. Treasury returns. On August 8, 2023, the Aave community proposed partnering with Centrifuge to invest Aave’s stablecoin reserves in RWA assets, targeting a 5% risk-free yield from U.S. Treasury-backed RWAs.

(POP: Anemoy Liquid Treasury Fund 1)

The Centrifuge Prime service consists of two steps:

Step 1: Legal wrapping for on-chain DeFi protocols—e.g., establishing a dedicated legal entity (a Cayman Foundation) for Aave. This entity replaces unlimited liability for DAO members and acts as an independent vehicle for RWA value capture, governed and controlled by the Aave community—bridging DeFi and TradFi.

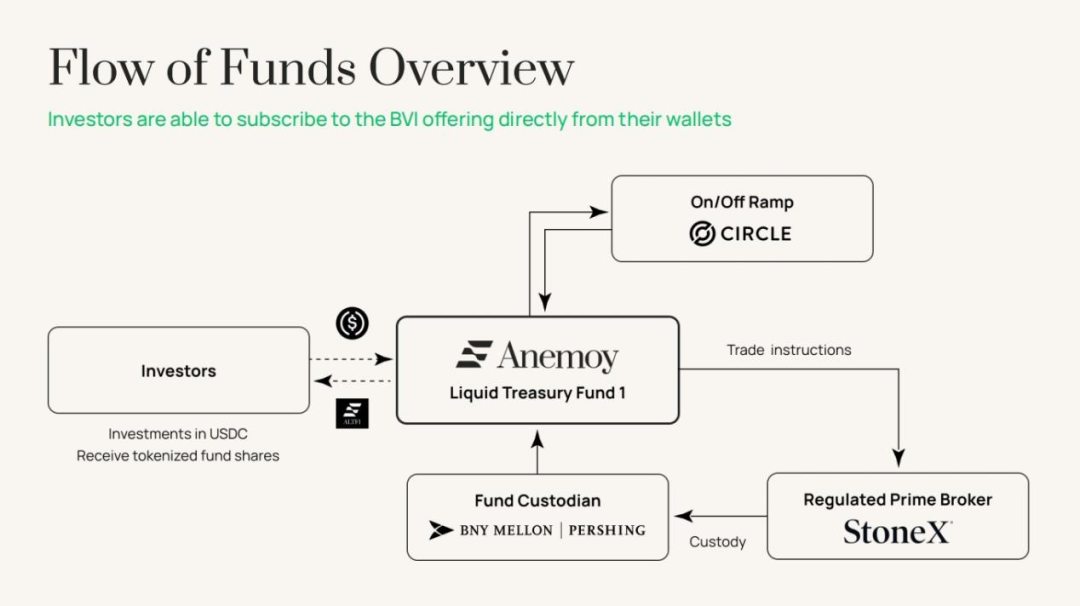

Step 2: Centrifuge establishes a dedicated asset pool—Anemoy Liquid Treasury Fund 1. Unlike previous pools backed by credit assets (where assets are placed into SPVs and minted as NFTs into Centrifuge pools), this pool’s underlying asset is U.S. Treasuries—requiring direct tokenization of the Anemoy LTF fund holding those Treasuries.

(Anemoy Liquid Treasury Fund 1)

Anemoy LTF is a BVI-registered fund. First, it is tokenized via the Centrifuge protocol. Then, Aave allocates treasury funds into the corresponding Centrifuge pool, receiving fund tokens. The Centrifuge pool routes Aave’s capital to the Anemoy LTF fund, which uses on/off ramps, custodians, and brokers to purchase U.S. Treasuries—bringing Treasury yields on-chain.

Using the same method, Centrifuge helped stablecoin project Frax Finance capture off-chain asset yields with $20 million.

4. Permissionless Integration of RWA and DeFi

We observe that most RWA projects—including those covered here—are accessible only to select or qualified investors, excluding retail participants. Due to regulatory compliance and local securities laws, opening access to retail would entail IPO-level issuance costs. Thus, not every RWA platform can freely open to all users post-tokenization.

As discussed in our earlier report *RWA Deep Dive: Dissecting Current Implementation Paths and Exploring Future RWA-Fi Logic*, some projects successfully integrate with DeFi to offer permissionless access for retail participation.

Examples include Ondo Finance & Flux Finance, Matrixdock & T Protocol’s DeFi lending path: qualified investor-restricted tokens serve as collateral to create DeFi lending pools where retail users deposit stablecoins to earn interest. Additionally, models like Ondo & USDY, MatrixDock & USDV issue yield-bearing stablecoins backed by restricted tokens, allowing retail users to swap stablecoins for interest-earning versions.

DeFi’s composable nature is evident—Pendle already integrates RWA assets for yield swapping. We are actively exploring RWA-DeFi integration and currently building a U.S. Treasury RWA platform to unlock infinite possibilities.

5. Final Thoughts

Current market offerings represent RWA 1.0—primarily addressing off-chain asset-side financing needs (whether through Security Token Offerings or collateralized lending) and on-chain capital-side investment demands (how to capture low-risk, stable-yield, scalable, crypto-market-independent real-world assets).

Soon, RWA will evolve toward deeper integration with the real world—entering versions 2.0, 3.0, and beyond. Until then, preparation is key.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News