XMAQUINA: An On-Chain Marketplace for Pre-IPO Robot Equity

TechFlow Selected TechFlow Selected

XMAQUINA: An On-Chain Marketplace for Pre-IPO Robot Equity

XMAQUINA is a DAO-governed on-chain capital vehicle that already holds real equity stakes in seven privately held humanoid robotics companies and plans to tokenize these stakes via the RCM protocol to build a fee-compounding flywheel—but whether this vision materializes hinges on whether genuine trading volume emerges after RCM’s launch.

Key Takeaways

1. The humanoid robotics industry is entering its early commercialization phase. In 2025, funding in this sector reached nearly $14 billion, and the combined valuation of leading companies exceeded $8.5 billion. Goldman Sachs forecasts the market size to reach $38 billion by 2035; Morgan Stanley projects it will grow to $5 trillion by 2050. Currently, no investment vehicle exists that offers retail investors direct, tokenized, and governable exposure to pre-IPO humanoid robotics companies. Existing secondary-market platforms are accessible only to accredited investors and typically impose a 10%–30% liquidity discount and 3%–5% transaction fees.

2. XMAQUINA holds verified equity stakes in six humanoid robotics companies, with governance conducted entirely via on-chain proposals. Its stake in 1X has appreciated 119% above cost basis, while its preferred-share position in Apptronik has appreciated 103% above cost basis.

3. The DAO treasury currently holds $6.7 million in humanoid robotics equity assets and $3.3 million in cash. The headline figure of $28 million shown on the DAO Portal includes $18 million of the DAO’s own $DEUS tokens—untraded and held in treasury—valued at the Genesis Auction price (corresponding to a $60 million FDV). Whether this valuation represents a discount or premium relative to NAV depends on which treasury benchmark and token supply assumption the allocator adopts.

4. The Robotics Capital Markets (RCM) Protocol converts each verified equity asset into a subDAO token paired with $DEUS on decentralized exchanges (DEXs). Transaction fees flow back into the DAO treasury, and each new subDAO trading pair creates demand for $DEUS as the intermediary asset. Whether the protocol generates sustainable compounding effects—or maintains static treasury size—depends on whether trading volume can sustain growth.

Executive Summary

Robotics private equity has already created hundreds of billions of dollars in value—but access remains structurally constrained.

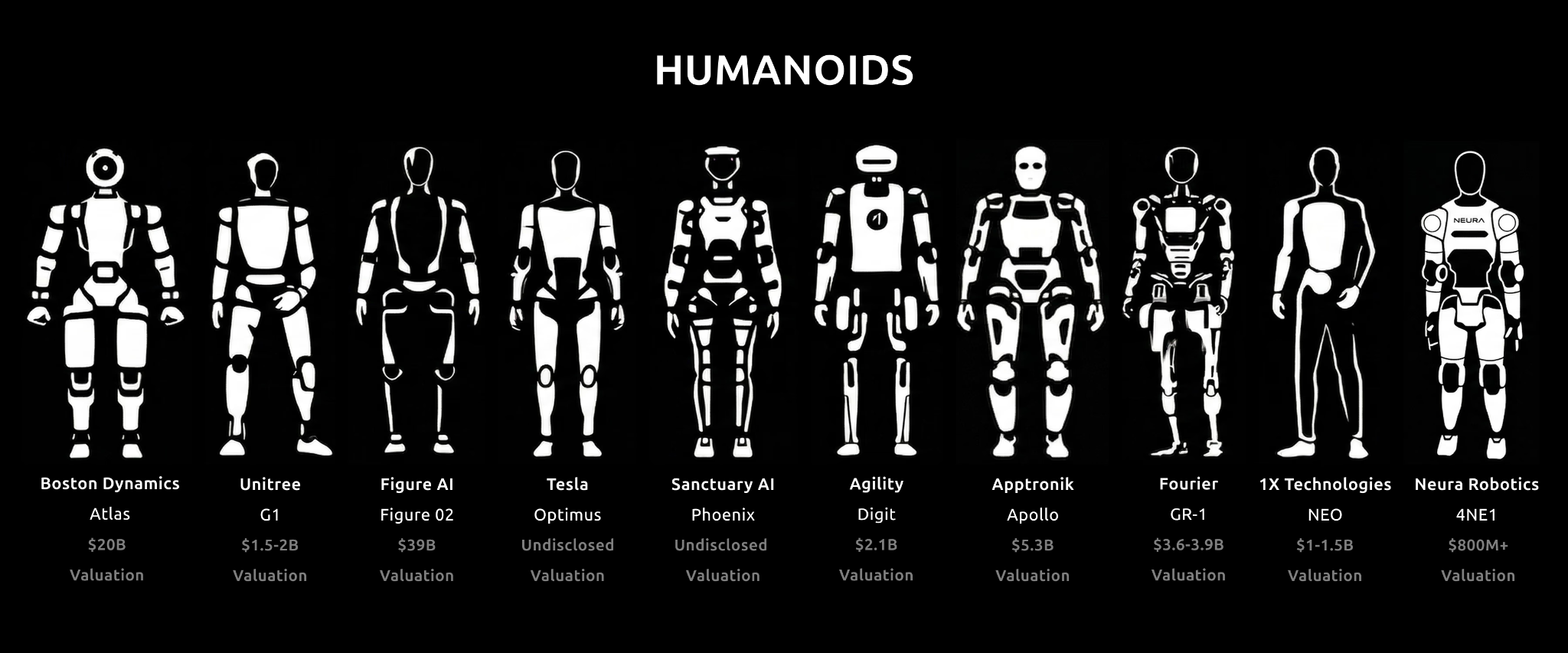

In 2025, robotics startups raised nearly $14 billion—up 71% from 2024. Today’s most advanced companies in the humanoid robotics space—including Figure AI, Apptronik, 1X Technologies, NEURA Robotics, and Agility Robotics—are still several years away from IPO.

Retail investors currently have only diluted, indirect exposure through public equities (e.g., Tesla, NVIDIA) or hybrid venture funds (e.g., ARK). No instrument yet exists offering governable, direct exposure to specific pre-IPO humanoid robotics companies.

XMAQUINA’s RCM Protocol is designed precisely to address this structural gap. Each equity asset is held via a dedicated SPV and converted into a subDAO token traded on DEXs against $DEUS. Fees generated by the protocol flow into the treasury to fund new asset allocations and drive further subDAO launches. Its compounding logic is: fee revenue grows the treasury, the larger treasury funds more equity allocations, and each new position spawns additional trading markets. The DAO’s currently deployable treasury stands at approximately $10 million; its full composition is detailed in Section 3.

This report covers the following: the current state of the humanoid robotics market; structural access barriers; XMAQUINA’s treasury and portfolio; the operational mechanics and competitive positioning of the RCM Protocol; the $DEUS tokenomics (including xDEUS staking); NAV premium analysis; and related risk factors, potential catalysts, and capital deployment framework.

All market cap, protocol metric, and token price data cited herein are as of May 2026 and will be updated dynamically as market conditions evolve.

1. Humanoid Robotics

Humanoid robotics is transitioning from a decade-long R&D cycle toward early commercialization—real-world deployments are increasingly replacing demo-only demonstrations. Yole Group estimates over 60 active humanoid robotics companies operate globally today, having collectively raised over $10 billion since 2017. Crunchbase data shows robotics startups raised nearly $14 billion in 2025—up from $8.2 billion in 2024—and even surpassing the previous peak of $13.1 billion in 2021.

Funding momentum continues into 2026: Skild AI closed a $1.4 billion round in January; Apptronik raised $520 million in February; EngineAI secured $200 million in April; and NEURA Robotics is reportedly finalizing a ~€1 billion (~$1.2 billion) round backed by Tether.

Why Now?

Adoption of humanoid robots is now visible in actual shipment volumes. Global production surged from ~2,000 units in 2024 to 16,000 units in 2025—with China accounting for over 80% of total deployments. Market forecasts project shipments exceeding 100,000 units by 2027.

Per-unit manufacturing costs continue to decline—down ~40% between 2022 and 2023—from $50,000–$250,000 to $30,000–$150,000. Unitree launched the consumer-facing humanoid robot R1 at $5,900 and later listed it on AliExpress, signaling early retail distribution infrastructure is forming. Kia announced plans to deploy Boston Dynamics’ Atlas robots in its manufacturing plants starting in 2029.

Commercial deployments by leading firms are beginning to replace pilot programs. BMW has deployed Figure AI robots for daily 10-hour shifts at its Spartanburg plant for over 11 months, accumulating over 1,250 hours of runtime across production of more than 30,000 vehicles. GXO Logistics deployed Agility Robotics’ Digit, becoming one of the first enterprises to use humanoid robots in commercial warehousing operations. Toyota Motor Manufacturing Canada signed a commercial agreement with Agility to deploy Digit in its production facilities. Apptronik is running pilots with Mercedes-Benz, GXO, and Jabil, and has an exclusive partnership with Google DeepMind on Gemini Robotics. 1X Technologies has opened consumer pre-orders for its NEO robot at $20,000, with a $499/month leasing option, targeting delivery in 2026.

Market Size Estimates

Analyst projections for the humanoid robotics market vary widely, reflecting differing assumptions and scope definitions.

Goldman Sachs forecasts the market to reach $38 billion by 2035—a roughly six-fold increase from its prior $6 billion estimate—implying ~1.4 million units deployed.

Morgan Stanley provides a broader estimate, incorporating supply chain, maintenance, and supporting infrastructure, projecting a total market size of $5 trillion by 2050. Between these two extremes, MarketsandMarkets, Barclays, and UBS forecast ranges between $15 billion and $200 billion, depending on coverage scope and time horizon.

Macroeconomic context reinforces this demand logic. Embodied AI is reshaping labor cost structures—much as software once transformed information cost structures. In the U.S., Deloitte and the Manufacturing Institute project 2.1 million unfilled manufacturing jobs by 2030, costing $1 trillion annually.

Access Barriers

The disclosed or target valuations of leading humanoid robotics companies total ~$8.5 billion across seven firms:

Figure AI ($3.9B), Skild AI ($1.4B), 1X Technologies (target $1B), Unitree (target $700M), Apptronik ($530M), Physical Intelligence ($560M), and NEURA Robotics (target >$400M).

When these companies eventually go public, their primary returns will likely have already been captured by institutional and accredited investors. No robotics-focused ETF currently covers these pre-IPO companies.

Anthropic’s pre-IPO implied valuation stood at ~$140 billion in May 2026—illustrating how substantial value accrues in the private stage before public listing. Figure AI issued cease-and-desist letters to brokers in 2025 to halt unauthorized secondary trading of its shares; Anthropic took similar action in May 2026. Meanwhile, Forge and Hiive—secondary-market platforms—remain accessible only to accredited investors and typically apply 10%–30% liquidity discounts, 3%–5% transaction fees, and multi-week settlement cycles.

2. Blockchain’s Role

Tokenizing private equity can improve access through fractional ownership, programmable compliance, and near-instant settlement efficiency. But not all tokenized equity is valid. The key distinction between legitimate tokenized equity exposure and empty promises lies in whether underlying assets are verified and associated rights legally enforceable.

A compliant SPV (Special Purpose Vehicle) holds shares directly on the target company’s cap table, and tokens represent fractional ownership of that SPV. Upon exit events, proceeds flow to token holders. Conversely, LP structures lacking asset backing may sell tokens without actually acquiring target equity—leaving holders with only promises and no recourse if the operator collapses.

For retail investors seeking entry into private robotics equity markets, this means a fundamental difference: do you hold verified, real equity—or a hollow claim that could vanish to zero overnight?

Cases like BlackRock’s BUIDL Fund, Securitize, and tZERO demonstrate how on-chain assets can be linked to audited, legally enforceable holdings with custodial proof. On March 17, 2026, the SEC and CFTC jointly issued an interpretive statement proposing a token classification framework and clarifying that most crypto assets are not inherently securities. For structures like RCM’s subDAO tokens, the Howey Test’s “investment contract” analysis remains the most relevant standard.

Blockchain infrastructure delivers three capabilities unavailable in traditional private secondary markets: programmable compliance, fractional ownership, and near-instant settlement. Programmable compliance enforces transfer restrictions directly at the smart-contract layer; fractional ownership allows splitting traditionally $500,000 SPV stakes into arbitrarily small investment thresholds; and near-instant settlement enables trades to complete in minutes—not weeks, as with Forge or Hiive. These attributes fundamentally restructure access layers for private-market assets.

XMAQUINA’s RCM model requires demonstrable proof that every SPV holds shares on the target company’s cap table—and that those share rights are legally enforceable.

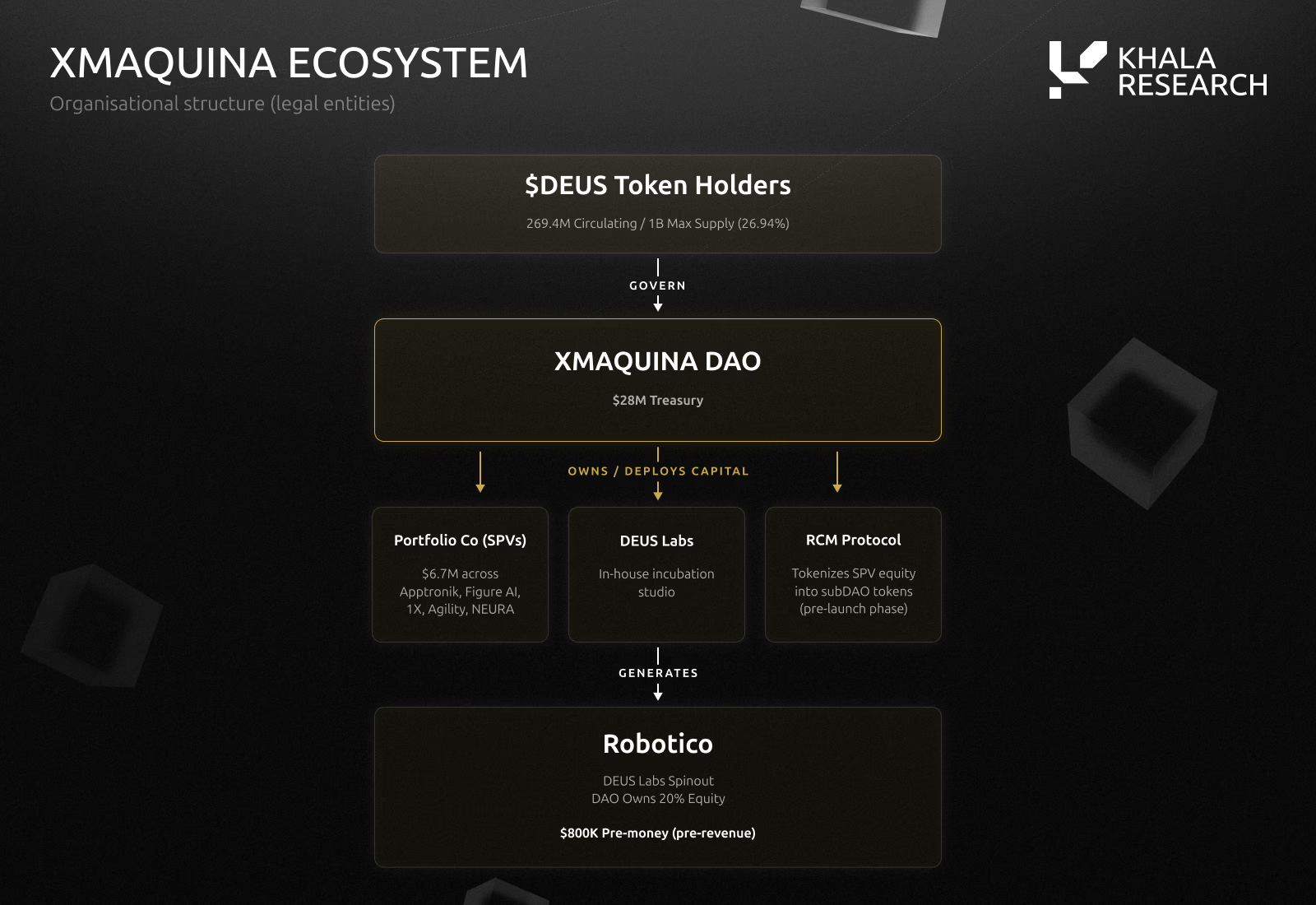

3. XMAQUINA

A DAO-governed capital vehicle focused on building an on-chain secondary market for private-market humanoid robotics equity.

Watch video: Mauricio, Co-Founder of XMAQUINA, discusses XMAQUINA on Supercycle Podcast

Overview

- Category: DAO-governed capital vehicle for humanoid robotics private equity

- Market Cap: $60 million FDV pre-TGE at Genesis price of $0.06 per $DEUS

- Treasury Size: ~$28 million (or ~$10 million excluding $DEUS)

- Equity Portfolio: $6.7 million across eight positions in seven entities

- Value Capture Mechanism: 5% of each subDAO token supply allocated to DAO at launch; 1% transaction fee; all subDAO trading pairs routed via $DEUS

- Risks: Pre-TGE token; unproven protocol revenue; 84% of portfolio concentrated in three revenue-negative companies

- Watchlist: $DEUS TGE; first RCM subDAO auction; monthly DEX trading volume of subDAOs; financing rounds or IPO filings of portfolio companies

XMAQUINA launched in early 2024 to acquire and hold private-market robotics assets via DAO-held treasury, with all capital allocations decided via on-chain governance. The DAO raised $10 million through five fully sold-out Genesis Auctions, attracting ~1,860 participants and support from Borderless Capital, Moonrock Capital, MH Ventures, Generative Ventures, Fundamental Labs, Waterdrip Capital, and strategic angel investors affiliated with Delphi Digital, Arkstream Capital, and KuCoin Ventures.

To date, 15 governance proposals have been submitted via Snapshot, with 14 passed—averaging ~6.7x quorum threshold. At the current Genesis Auction price of $0.06 per $DEUS, its FDV stands at ~$60 million.

XMAQUINA operates under a unified governance layer: MachineDAO LLC, registered in the Marshall Islands as a DAO LLC, is fully governed by on-chain $DEUS token voting. It serves as the ultimate beneficial owner and legal controller of all subsidiary entities, holding power to appoint and remove directors.

XMAQUINA Foundation Ltd., registered in the Cayman Islands, acts as the off-chain execution entity, holding legal title to equity on behalf of the DAO and executing investments solely upon governance approval.

RWA Robotics Ltd., registered in the British Virgin Islands (BVI), is a limited-purpose entity for $DEUS token issuance and SAFT execution.

Treasury Composition

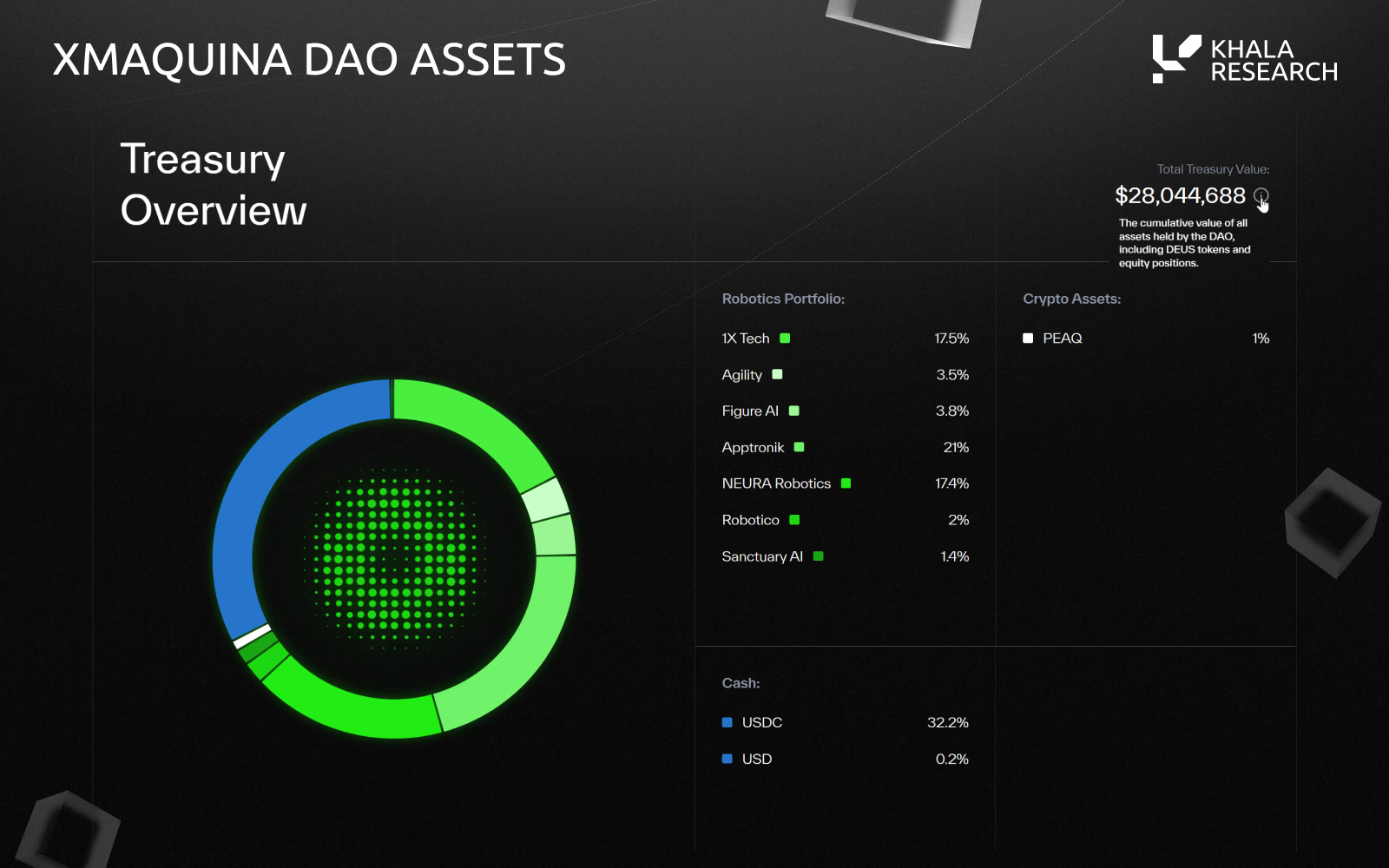

As of May 2026, the DAO Portal displays a total treasury value of $28 million.

Source: XMAQUINA DAO Portal, May 2026. This dashboard is live and values update dynamically.

The $18.1 million in crypto assets shown on the DAO Portal consists primarily of 300 million $DEUS and 3.7 million $PEAQ. $DEUS is valued at the Genesis Auction price of $0.06, corresponding to ~$18 million; $PEAQ is valued at ~$100,000—the payment asset received during Genesis Wave 1, which accepted PEAQ only.

This $DEUS belongs to the DAO treasury’s token allocation and is currently governance-locked—usable only via on-chain voting for liquidity provision, staking incentives, or sales to support operations and equity acquisitions. As $DEUS has not yet listed on public exchanges, its $0.06 valuation reflects auction pricing—not public-market clearing prices—a common practice for pre-TGE DAO treasuries.

Thus, in NAV analysis, the $28 million figure reflects the total treasury including token assets; if assessing only deployable capital—i.e., robotics equity and cash—the working treasury stands at ~$10 million. Both metrics are further illustrated in Section 3.2.

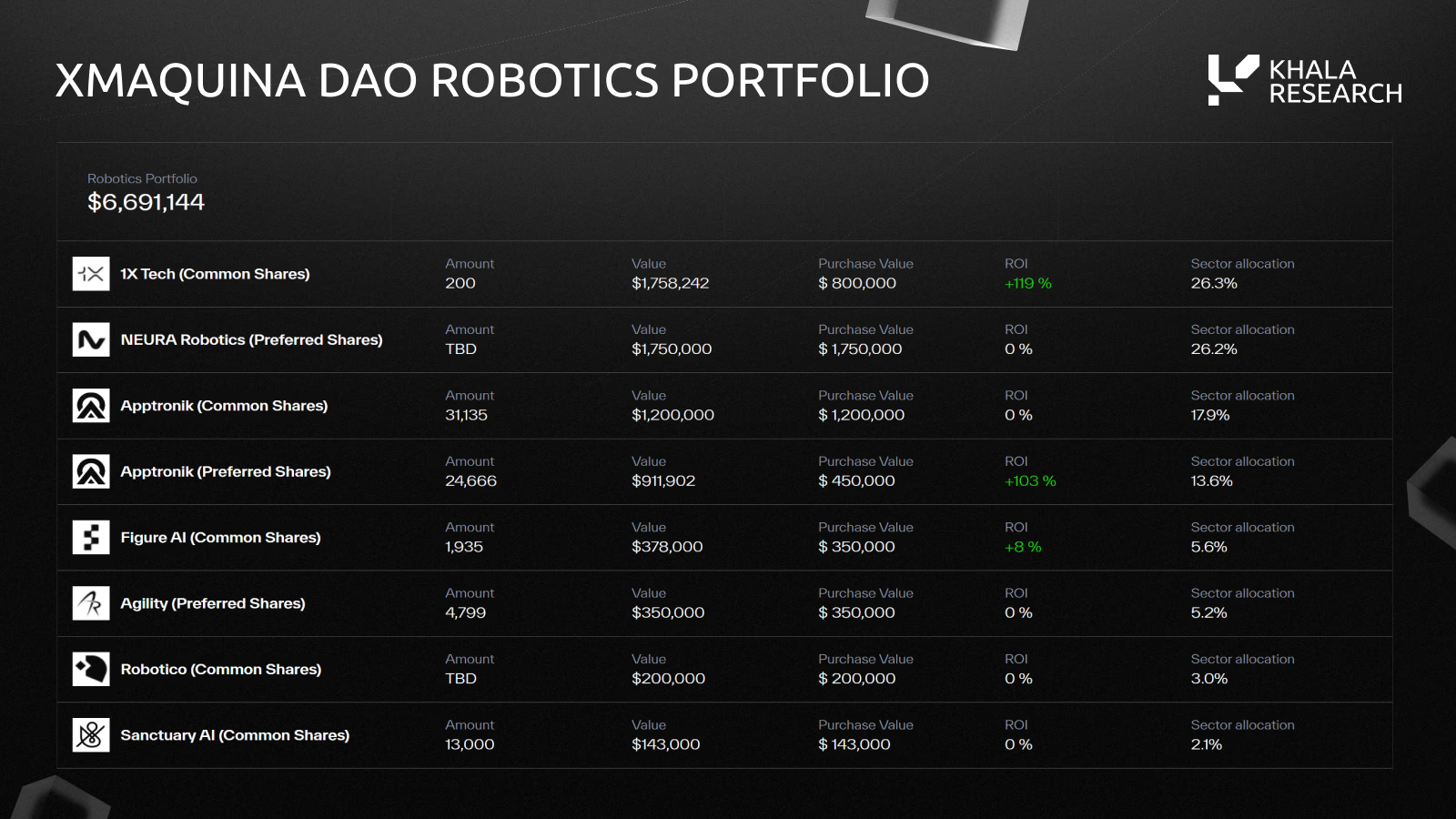

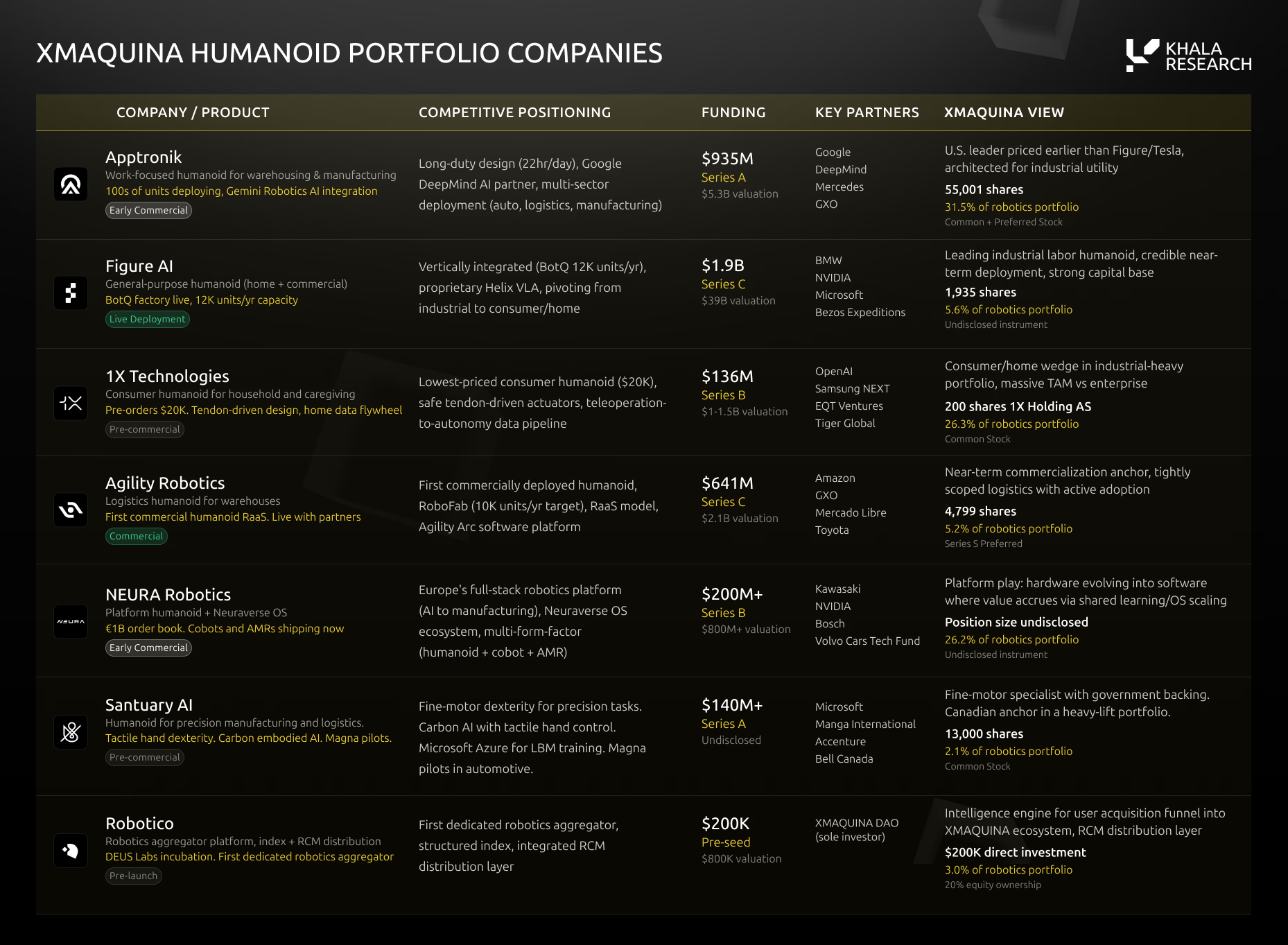

Robotics Portfolio

As of now, XMAQUINA’s robotics portfolio totals ~$6.7 million across eight positions in seven entities, with cumulative cost basis of ~$5.2 million.

Source: XMAQUINA DAO Portal, May 2026.

Attestation letters from Andersen LLP confirming holdings have been published on XMAQUINA’s documentation page. These currently cover six allocations: Apptronik (BOT-01), Figure AI (BOT-03), Agility Robotics (BOT-04), Apptronik follow-on (BOT-06), 1X Technologies (BOT-07), and NEURA Robotics (BOT-09). The two Apptronik positions reflect separate allocations approved by governance at different entry points.

Portfolio Company Profiles

Below is a company-by-company overview of XMAQUINA’s core holdings.

- Apptronik

Apptronik is developing Apollo, an AI-driven humanoid robot for manufacturing and logistics. In its Series A extension in February 2026, the company raised $935 million at a $5.5 billion valuation, with participation from Google, Mercedes-Benz, John Deere, and Qatar Investment Authority. It has an exclusive partnership with Google DeepMind on Gemini Robotics and runs pilots with Mercedes-Benz, GXO, and Jabil. Apollo is designed for 22-hour daily operation with hot-swappable batteries.

The DAO holds two independent Apptronik positions totaling 55,801 shares: 24,666 preferred shares purchased for $450,000 (current return +103%); and 31,135 common shares purchased for $1.2 million (currently flat).

Combined, the DAO’s total exposure to Apptronik is $1.65 million—31.5% of the portfolio—and represents its largest single allocation at the company level.

- 1X Technologies

1X Technologies is developing NEO, a consumer-facing humanoid robot priced at $20,000 with a $499/month leasing option. The Norwegian firm relocated to Palo Alto in 2025 and has tested NEO in hundreds of homes. In January 2025, 1X acquired Kind Humanoid, integrating the team developing the bipedal humanoid Mona. To date, the company has completed 10 funding rounds totaling $136.5 million.

The DAO’s stake was acquired at a company valuation of ~$4.55 billion. Crunchbase shows 1X closed a new Series B round on February 27, 2026—but lists only one investor and discloses no valuation. This appears to be a modest extension round rather than the rumored $10+ billion round. On secondary markets, Hiive shows 1X shares trading at ~$2,163/share as of May 2026.

The DAO holds 200 common shares purchased for $800,000 (current return +119%), representing 26.3% of the portfolio.

- Figure AI

Figure AI develops general-purpose humanoid robots for industrial and home applications. Its Figure 02 completed an 11-month deployment at BMW’s Spartanburg plant and was retired in late 2025. Figure 03, launched in October 2025, is the current production model for scaled manufacturing. Figure also operates BotQ, a vertically integrated manufacturing facility that has produced over 350 robots, with capacity scaling toward one unit per hour.

The company closed its Series C round in September 2025, raising over $1 billion at a $39 billion valuation, led by Parkway Venture Capital with participation from NVIDIA, Brookfield, and Intel Capital.

The DAO holds 1,935 common shares purchased for $350,000 (current return +8%), representing 5.6% of the portfolio.

- NEURA Robotics

NEURA Robotics, a German firm, focuses on cognitive humanoid robots and Neuraverse—an OS enabling skill-sharing across robot fleets. NEURA has partnered with Schaeffler, HD Hyundai, and GFT Technologies, and has disclosed €1 billion in orders. Amazon has also deployed NEURA’s cognitive robots in its fulfillment centers.

NEURA has raised €185 million across five rounds, with its most recent being a €120 million Series B in January 2025, led by Lingotto. Bloomberg reported in March 2026 that NEURA is raising ~$1.2 billion backed by Tether, implying a ~$4.3 billion (~€4 billion) valuation. In October 2025, the company acquired industrial automation firm EK Robotics, which employs ~300 people.

The DAO holds a $1.75 million position in NEURA, representing 26.2% of the portfolio.

- Agility Robotics

Agility Robotics develops Digit, a bipedal warehouse robot and the first humanoid robot certified for commercial workplace safety. Digit is deployed at GXO, Amazon, and Toyota facilities. The company also operates RoboFab—a 70,000-square-foot production facility targeting annual output of 10,000 units.

Agility has raised ~$680 million, with market reports estimating its valuation at ~$1.8 billion.

The DAO holds 4,799 preferred shares purchased for $350,000, representing 5.2% of the portfolio.

- Sanctuary AI

Sanctuary AI is developing Phoenix, a general-purpose humanoid robot for fine-motor tasks in manufacturing and logistics. The company focuses on Carbon—a system for embodied intelligence—integrated with tactile-feedback dexterous hands to enable high-precision manipulation. Phoenix has been tested in automotive factories with Magna International and has a strategic partnership with Microsoft.

To date, Sanctuary has raised over $140 million from investors including BDC Capital, Accenture, Magna, Verizon Ventures, and Workday Ventures, plus $30 million from Canada’s Strategic Innovation Fund.

The DAO holds 13,000 common shares purchased for $143,000, representing 2.1% of the portfolio.

- Robotico

Robotico—the first project incubated by DEUS Labs—is a market intelligence platform covering the embodied AI sector, tracking companies, robot products, and capital flows. It catalogs 95+ humanoid robot models and provides real-time stock trackers for robotics-related public companies, funding round tracking, valuation data, and weekly intelligence reports.

The DAO, as the sole pre-seed investor, acquired 20% equity at an $800,000 pre-money valuation for $200,000—representing 3.0% of the portfolio.

Portfolio Risk Observations

The portfolio exhibits high concentration.

The top three positions are:

- Apptronik: 31.5%

- 1X: 26.3%

- NEURA: 26.2%

Together, they account for 84.0% of the robotics portfolio—meaning overall performance hinges heavily on valuation and liquidity progress of just a few core companies.

Geographically, the portfolio is 100% allocated to Western companies (U.S., Norway, Germany), while over 80% of global humanoid robot deployments in 2025 occurred in China—indicating a geographic misalignment with real-world deployment patterns.

Technologically, all portfolio companies rely on NVIDIA’s tech stack for simulation and training. Two additionally depend on exclusive AI lab partnerships:

- Apptronik / Google DeepMind

- 1X / OpenAI

This introduces upstream model and platform dependency risk.

Exit decisions are made by xDEUS holders via on-chain proposals. Upon exit events, governance may vote to allocate up to 40% of realized gains to active xDEUS stakers (weighted by staking duration), with the remainder retained in treasury for new capital allocations. Settlement for RCM-linked SPV holdings occurs at the SPV level.

Deal Sourcing Channels

The DAO’s Northstar Council has identified a pipeline of potential targets, including:

- FieldAI (confirmed)

- Skild AI

- Physical Intelligence

- Clone Robotics

- RoboForce

- AgiBot

- Unitree

- Sunday Robotics

The roadmap aims to complete 10 capital allocations by Q3 2026. These investments align with expected growth: more investments mean more subDAO markets, more protocol fees, and a broader portfolio base.

3.1 ROBOTICS CAPITAL MARKETS (RCM)

An infrastructure bringing private robotics equity on-chain—creating 24/7, permissionless markets around verified holdings.

To move beyond treasury-only allocation, XMAQUINA is launching the RCM Protocol. Governance proposal XMQ-03 (RCM Protocol Development) passed with 152 votes and a 601% quorum threshold. The roadmap targets Q2 2026 for initial launch, with early governance proposals defining first asset allocations and launching the first RCM subDAO auctions on-chain—followed by full protocol rollout in Q3 2026. Expansion phases (perpetual contracts, prediction markets, new asset listings) are planned for Q4 2026.

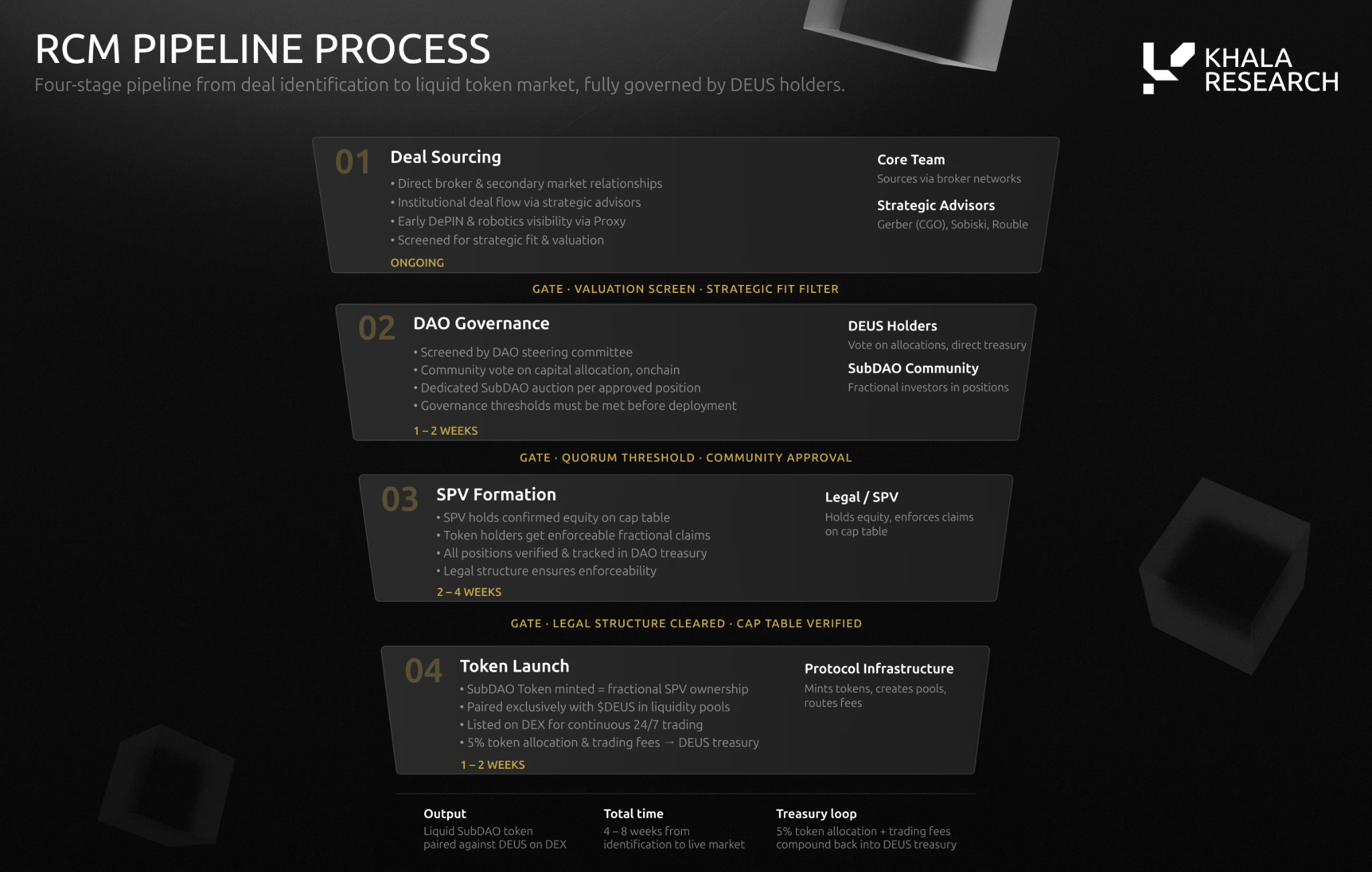

How RCM Works

The team sources deals through direct relationships with brokers, seed investors, and secondary-market platforms. Strategic advisors include Michael Ganser (former CEO, Cisco Germany), Lex Sokolin (Generative Ventures), Ruben Portela (Wise3 Ventures), Simon Dedic (CEO, Moonrock Capital), and Alvaro Gracia (General Partner, Borderless Capital). The DAO also integrates with peaq to enhance visibility into robotics and physical AI projects.

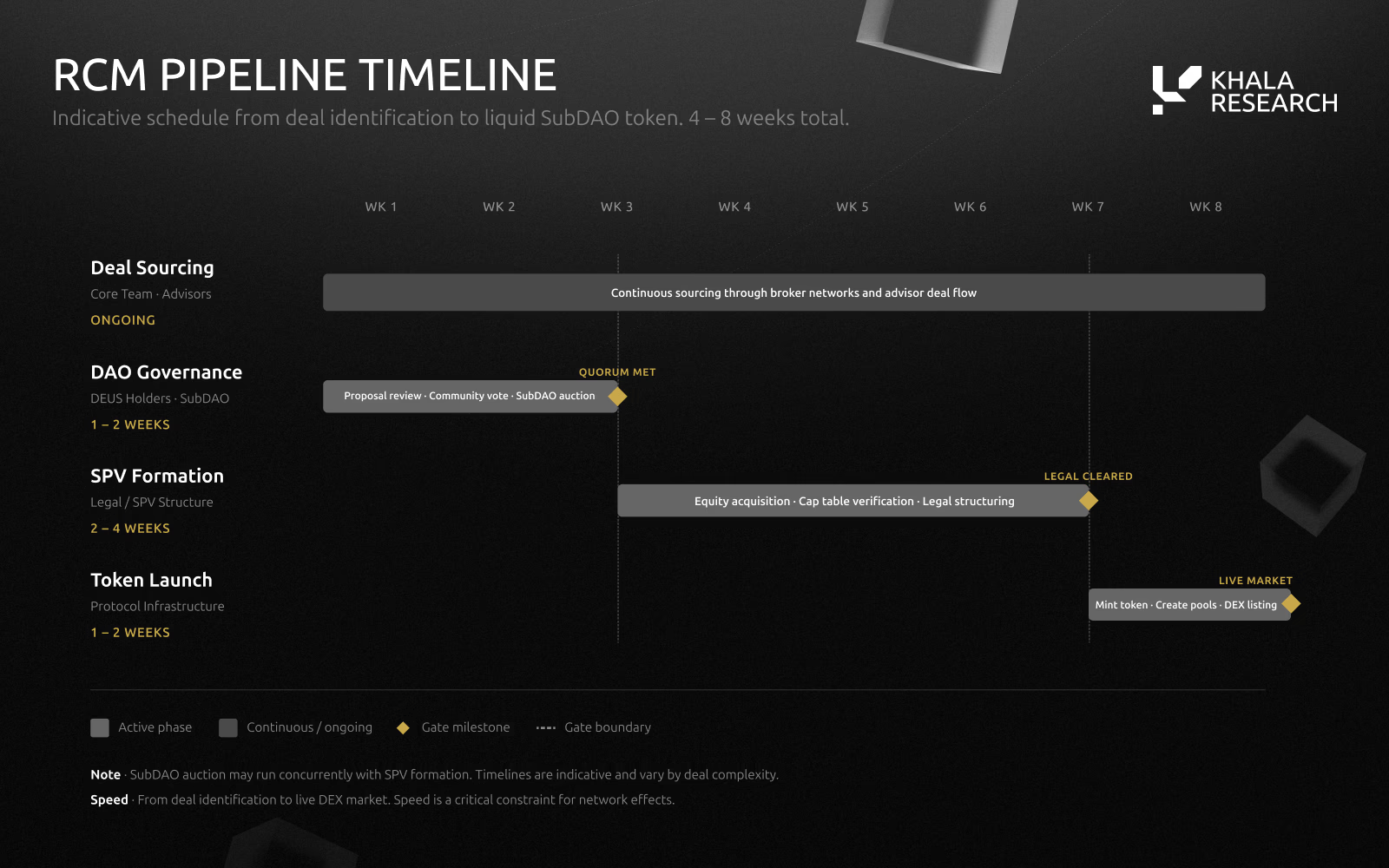

The process unfolds in four stages:

- XMAQUINA identifies an allocation opportunity;

- The community raises capital via subDAO auction;

- A dedicated SPV is formed to hold verified equity on the cap table;

- subDAO tokens are minted, paired with $DEUS, and listed on DEXs.

Total time from deal discovery to market launch is ~4–8 weeks.

subDAO tokens grant users 24/7 trading exposure to SPV-held positions—without requiring accredited investor status or broker intermediaries. For example, a $500,000 Figure AI position can be traded as a subDAO token (e.g., $dFIGURE) on DEXs, introducing price discovery to private equity. Under normal operation, such tokens trade freely against $DEUS on secondary markets, with pricing determined by market supply/demand, liquidity depth, and available information. Market prices may trade at premiums or discounts to the implied NAV of the underlying SPV position.

Token holders do not own equity in the underlying company, nor shares in the SPV, nor entitlement to dividends. Any value accrued by subDAO tokens is purely market-driven and may not reflect the SPV’s valuation. They serve as coordination and sentiment tools—not tokenized securities.

Upon liquidity events (e.g., IPO, acquisition, or other exits), the SPV realizes gains from underlying assets. The current framework assumes a Reg S structure, excluding U.S. persons from subDAO token issuance and redemption. Eligible non-U.S. holders may redeem or claim proceeds post-KYC/KYB, subject to applicable token terms.

XMAQUINA treasury does not absorb exit proceeds. Settlement occurs at the SPV level. The team has indicated that the full redemption and settlement framework will be documented and disclosed ahead of RCM Protocol launch.

Equity positions are executed via SPVs managed by Tier-1, regulated secondary-market operators—including Forge Global, Hiive, EquityZen, and Zanbato—all SEC-registered broker-dealers and FINRA/SIPC members. SIPC protection covers up to $500,000 per account against broker-dealer insolvency risk at the platform level.

Revenue Model

Per RCM blog posts, RCM generates revenue through two mechanisms:

- At launch, each subDAO allocates 5% of its total token supply to XMAQUINA DAO;

- Ongoing transaction fees from DEX trading activity flow into the treasury.

Governance proposal XMQ-03 also establishes a 1% protocol fee on subDAO trades. Governance decides how to allocate these revenues—for new humanoid robotics equity purchases, $DEUS buybacks, staking incentives, etc.

Competitive Positioning

RoboStrategy has proven this model’s viability in traditional finance (TradFi). Registered under the 1940 Investment Company Act as a closed-end fund, RoboStrategy listed on Nasdaq under ticker BOT in May 2026, with a portfolio spanning 12+ robotics and physical AI companies—including Figure AI, Apptronik, Dyna Robotics (co-led by CRV and First Round Capital in its $120M Series A), Standard Bots, and Dexmate—and publishes monthly NAV and quarterly SEC disclosures.

It offers institutional and retail investors exposure to private-stage robotics companies via a listed, regulated vehicle—at the cost of limited redemption windows, quarterly pricing updates, and active management by FP Strategies LLC. Most closed-end funds trade persistently at NAV discounts—but BOT is an exception.

The stock debuted on May 11, 2026, at the pre-listing private price of $10.00/share and has since traded between $19.20 and $59.00. Against its most recent disclosed NAV of ~$7.34/share (based on $146.2M net assets as of Feb 28, 2026, and 19.9M shares outstanding), this implies a premium range of ~160%–700%. Its May 15 close at $36.01 sits near the midpoint—implying ~390% premium.

Unlike BOT—a passive portfolio lacking compounding mechanics—RCM claims a distinct structure: 24/7 DEX trading, no minimum investment thresholds, governance-directed fee allocation, and a “fee-funded equity acquisition” revenue flywheel. Whether this structure sustains meaningful premiums depends on trading volume and execution capability.

XMAQUINA draws design inspiration from Pump.fun and Virtuals Protocol.

Pump.fun demonstrated automated liquidity and frictionless token creation—generating ~$1 billion in historical revenue across 18M+ tokens.

Virtuals Protocol evolved from a simple launchpad into a broader AI agent coordination layer. Its aGDP framework measures total economic activity generated by AI agents across the ecosystem, and the protocol is expanding into agentic commerce and robotics. With 18,000+ deployed agents, $13.8B cumulative DEX volume, and $70M cumulative revenue, Virtuals has built the most mature model for tokenized belief markets around specific projects.

RCM borrows from both models—but optimizes for a different goal: executable equity claims—not frictionless speculation. This introduces structural friction—4–8 weeks from deal identification to market launch versus Pump.fun’s 30 seconds—but that friction ensures positions backed by verifiable cap-table entries.

Partnership with Virtuals

XMAQUINA partnered with Virtuals Protocol in its final pre-TGE community sale—the first project launched via Virtuals Titan model. This auction sold out completely, raising $3.2 million ($3.046M USDC, $190,400 $VIRTUAL) and allocating 92M $DEUS.

The $VIRTUAL portion will fund the DEUS/VIRTUAL liquidity pool at TGE, targeting >$1M TVL. Separately, governance proposal XMQ-02 allocated 18M $DEUS and $150,000 USDC for liquidity support.

This partnership grants XMAQUINA access to Virtuals’ user base of >1M wallets and embeds the project within one of crypto’s most active on-chain ecosystems.

3.2 $DEUS

$DEUS is the core coordination and value-capture asset of the XMAQUINA ecosystem—serving critical functions in DAO treasury governance, capital allocation decisions, and protocol cash-flow distribution. Its maximum supply is fixed at 1 billion tokens, with no inflation mechanism; all tokens unlock over four years.

Governance follows a veToken model. Users stake $DEUS to mint xDEUS, gaining voting power. Voting weight increases with staking duration—from base multiplier to a maximum 12x after 12 consecutive months. To boost governance participation, a Governance Activation Program has been launched, allocating 1M $DEUS as staking rewards—linearly released over 90 days starting May 18, 2026. The entire governance system runs on Aragon OSx, supporting on-chain proposals, treasury management, and protocol parameter adjustments.

xDEUS holders decide on treasury deployment, exit timing, and fee allocation. Following liquidity events, governance may vote to distribute up to 40% of realized gains to active xDEUS holders (weighted by staking duration); if approved, remaining proceeds stay in treasury for future asset allocations.

Value Capture

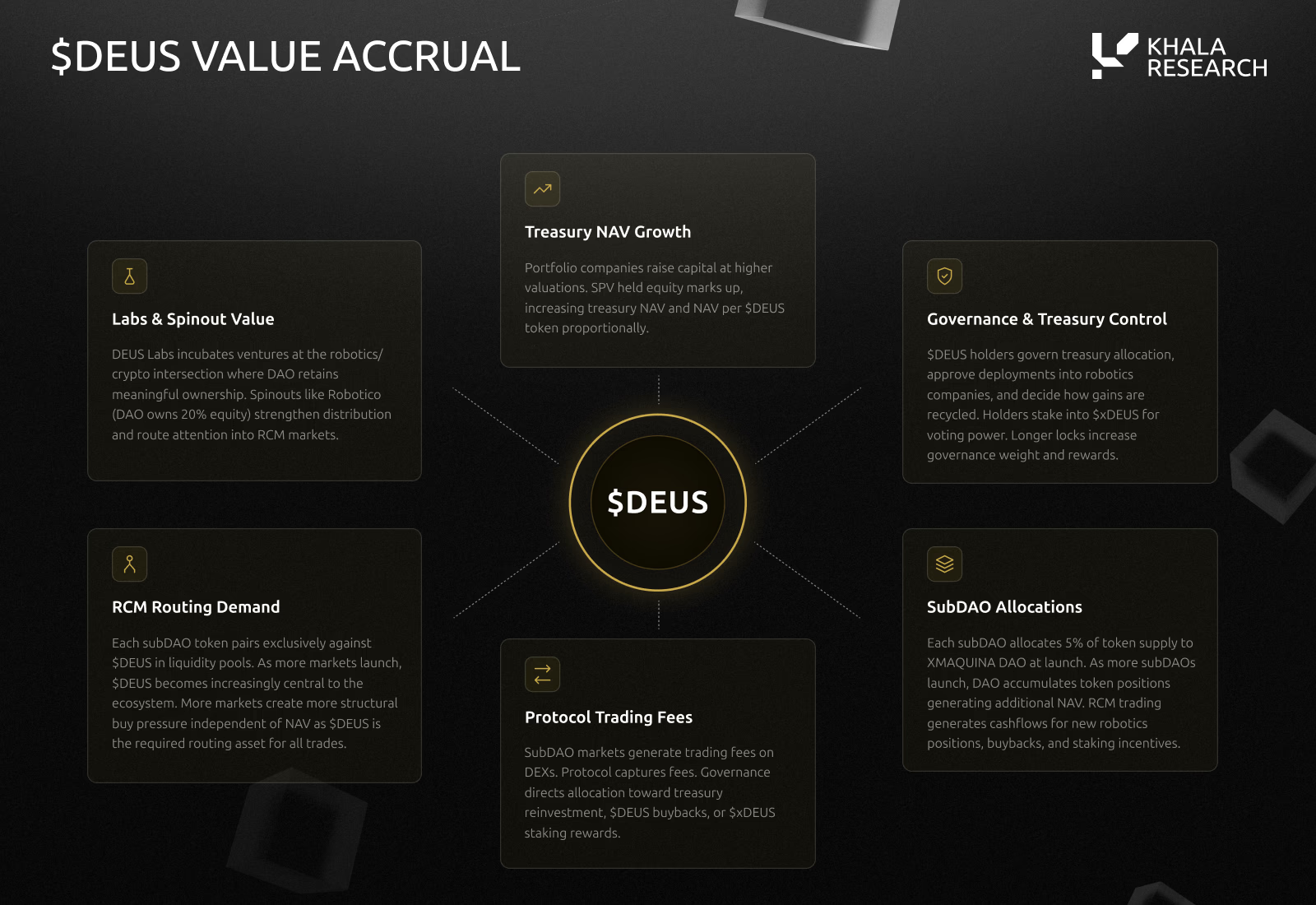

$DEUS captures value across six dimensions:

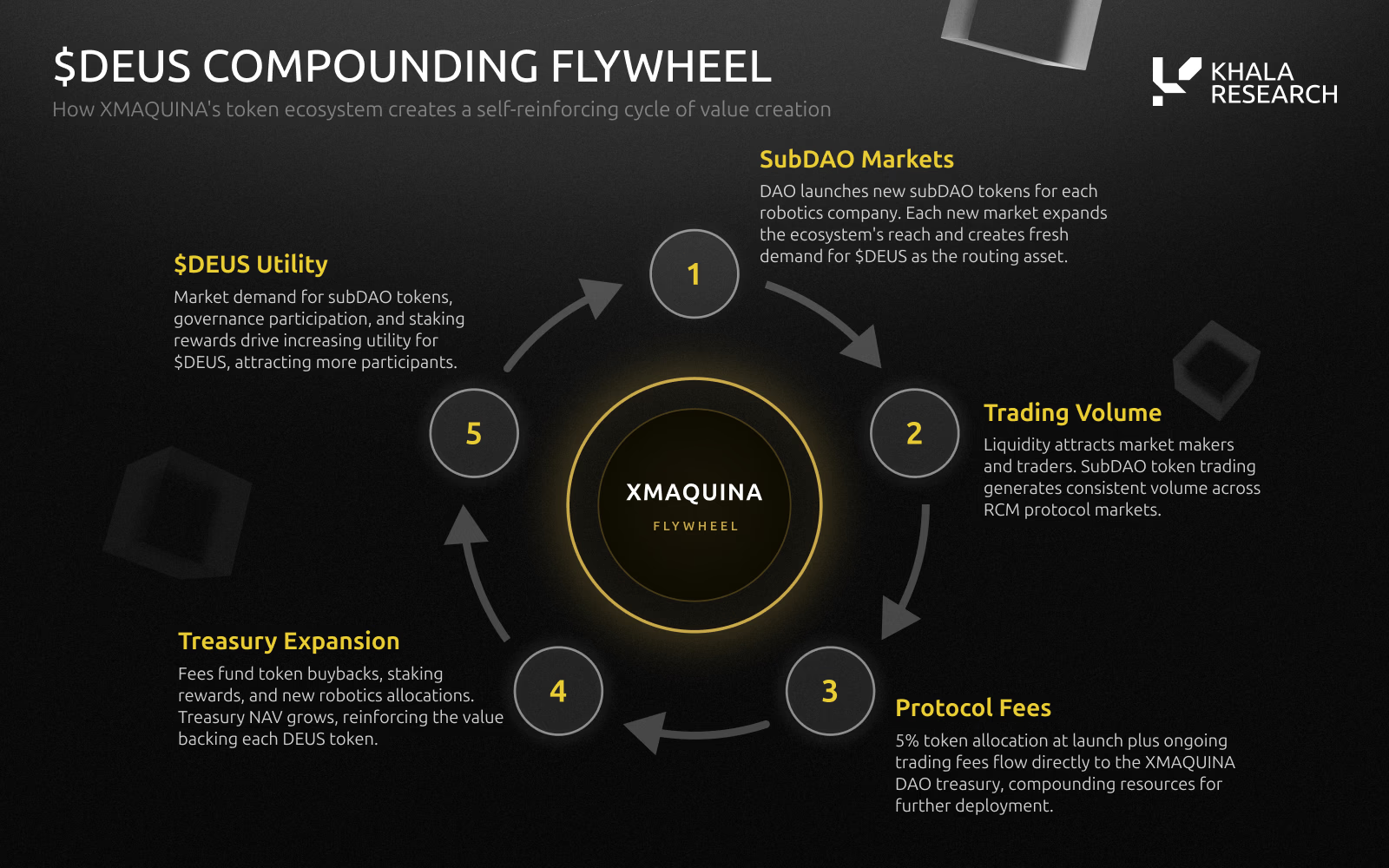

First is protocol carry. Every subDAO launched via RCM allocates 5% of its total token supply to the DAO at launch—granting the DAO native exposure in each market it creates without additional capital outlay. As active subDAO markets multiply, the DAO accumulates concurrent stakes across more markets—and shares in their trading activity.

Second is routing demand. All subDAO tokens trade exclusively against $DEUS on DEXs—making $DEUS the intermediary asset across the entire subDAO market system. Analogous to $TAO’s pairing with subnet tokens in Bittensor and $VIRTUAL’s role as foundational asset across all agent markets in Virtuals Protocol, $DEUS’s structural demand strengthens as active market count and trading volume grow.

Third is fee flow. Transaction fees generated by subDAO trading on DEXs flow into the DAO treasury, with governance deciding their use—new equity investments, $DEUS buybacks, or xDEUS staking incentives. As this mechanism is not hardcoded, value-capture pathways evolve dynamically with ecosystem maturity.

Fourth is treasury NAV growth. The underlying equity portfolio appreciates independently of token economics. When portfolio companies raise at higher valuations—or exit via IPO, M&A, etc.—the DAO gains either paper appreciation or realized gains, compounding alongside protocol-layer revenue.

Fifth is DEUS Labs incubation returns. The DAO currently holds 20% equity in Robotico and will retain similar stakes in future incubated projects. If these projects achieve product-market fit, their valuation growth may significantly exceed external investments—and further translate into new subDAO markets.

Sixth is governance rights themselves. $DEUS holders stake to obtain xDEUS and decide on investment targets, fee usage, exit timing, and reinvestment strategies. In essence, all ecosystem value capture is ultimately coordinated through this governance layer.

XMAQUINA emphasizes a core compounding logic: protocol fees expand the treasury; treasury expansion funds more equity allocations; more allocations spawn more subDAO markets; and more subDAO markets generate more protocol fees.

NAV Premium Analysis

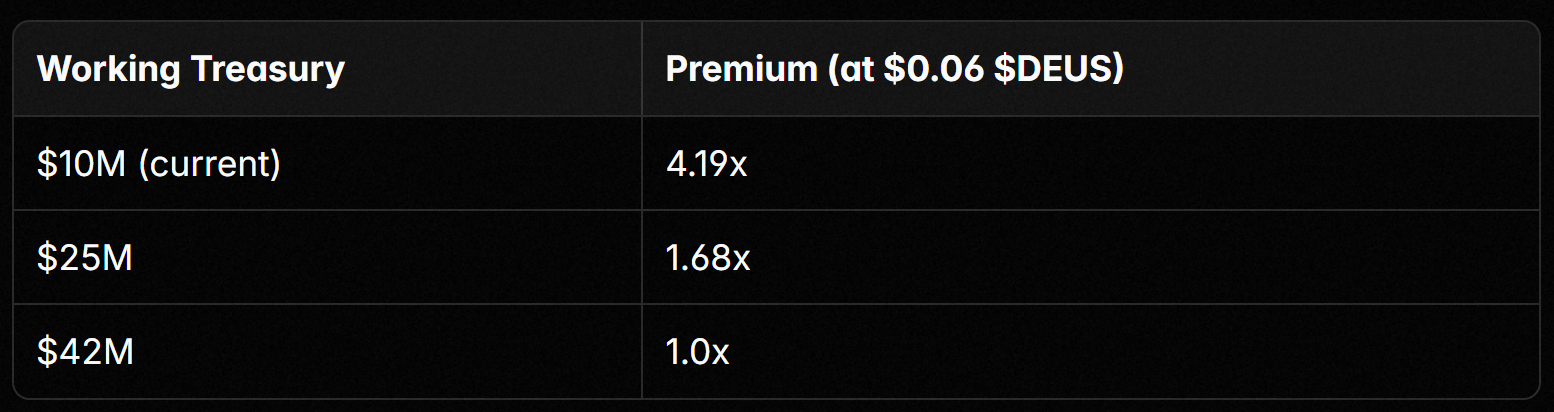

The DAO Portal displays a $28 million treasury—but as outlined in Section 3, $18 million stems from DAO-held $DEUS valued at the $0.06 Genesis price. Excluding this self-valued $DEUS, the operationally meaningful figure is ~$10 million—comprising robotics equity, cash, and other crypto assets. Two analytical frameworks apply—and in each, treatment of treasury-held $DEUS must remain symmetrical.

Method One: Include treasury-held $DEUS in both FDV and NAV

Under this method, nominal treasury size is $28 million, comprising:

- $6.7M robotics equity

- $3.3M cash & stablecoins

- 3.7M $PEAQ

- 300M $DEUS

Total token supply is 1B. With circulating supply at 314.7M tokens, NAV per token is ~$0.089. FDV at $0.06 is $60M. Thus:

FDV / NAV = $60M / $28M = 2.14x, i.e., a 114% premium.

This approach is internally consistent: the 300M $DEUS held in treasury count both as assets and remain included in total supply.

Method Two: Exclude treasury-held $DEUS from both FDV and NAV

If treasury-held $DEUS is treated as non-circulating—akin to corporate treasury stock—then both FDV and NAV must exclude these 300M tokens. Adjusted:

- Adjusted FDV = $42M (700M tokens × $0.06)

- Adjusted NAV = $10M (robotics equity, cash, and crypto assets)

Thus: Adjusted FDV / NAV = $42M / $10M = 4.19x, i.e., a 319% premium.

A third perspective is the ratio of floating market cap to NAV—distinct from fixed market cap/NAV (FDV/NAV).

$DEUS has a fixed max supply of 1B tokens, but its floating supply is smaller due to unlocks, treasury reserves, and xDEUS staking. In vote-escrow models, staked $DEUS is non-transferable.

Smaller floating supply amplifies premiums when demand exceeds immediately tradable supply. This ratio is dynamic: floating supply increases as tokens unlock. If the robotics portfolio appreciates and new treasury investments occur, NAV rises too.

Cross-checking against live markets: RoboStrategy (see Section 3.1) trades at ~2.6–8.0x its most recently disclosed NAV. XMAQUINA’s two methods yield multiples below this range (2.14x and 4.19x respectively).

But differences exist. BOT is a passive portfolio with no redemption mechanism or compounding revenue model.

XMAQUINA adds active governance, protocol revenue potential via RCM, and incubation returns via DEUS Labs. Yet it also introduces execution risk, pre-TGE pricing uncertainty, and untested protocols. Whether XMAQUINA sustains comparable premiums depends on actual RCM trading volume and market pricing of governance, ecosystem value, and underlying assets.

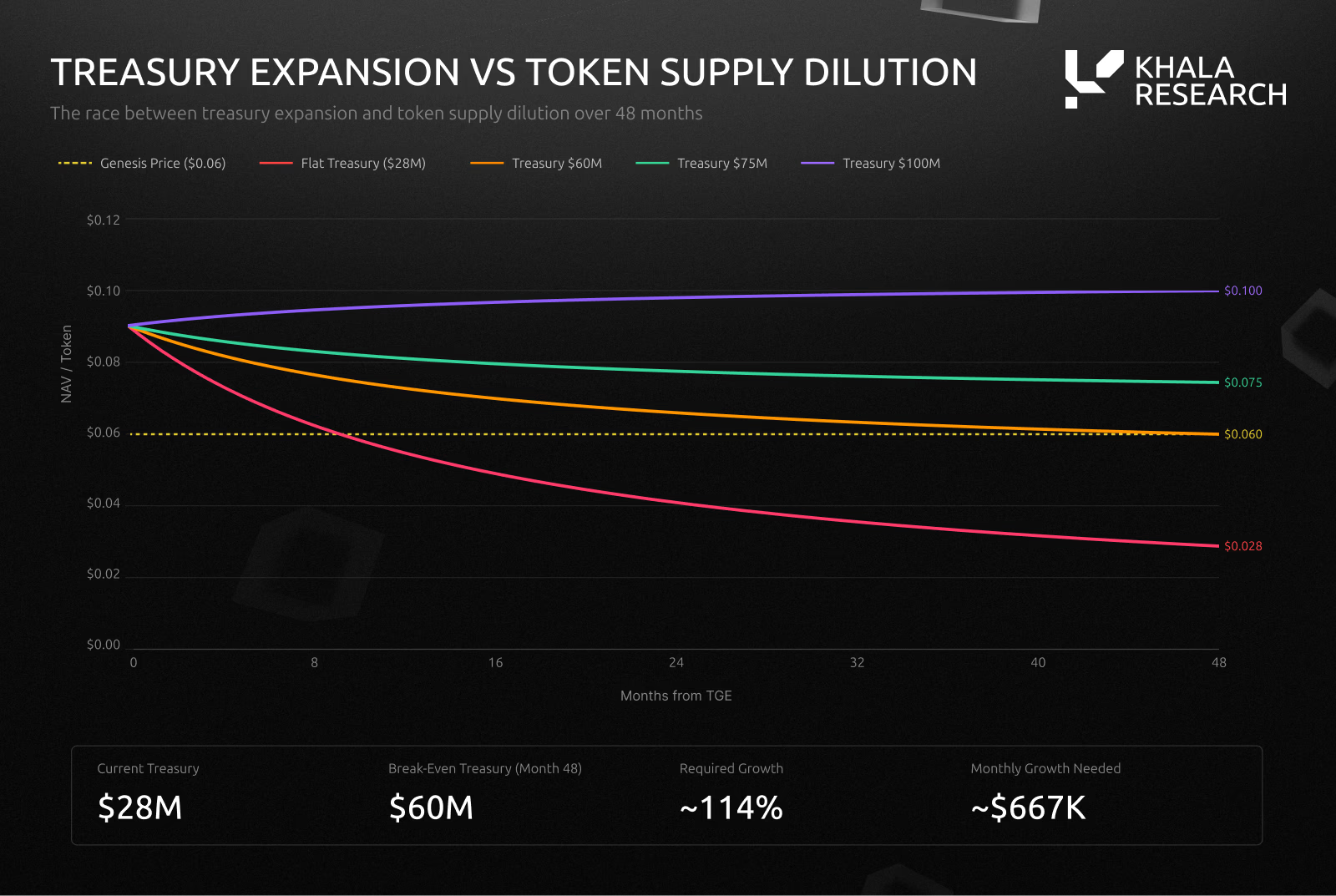

Over 48 months, the remaining 685.3M tokens will gradually unlock—bringing circulating supply to 1B. Per Method One, major allocations are distributed across 1B tokens. If treasury remains fixed at $28M, fully diluted NAV per token drops to $0.028. A $0.06 price requires treasury to reach $60M by month 48—i.e., ~$667K net monthly growth. RCM protocol fees, new equity allocations, portfolio appreciation, and eventual $DEUS market cap all contribute. If RCM generates sustained volume, the compounding effect is: fees grow treasury; larger treasury funds more equity; more equity spawns more subDAO markets; more markets generate more fees.

MicroStrategy Comparison and Limitations

XMAQUINA’s documentation compares itself to MicroStrategy (now Strategy Incorporated).

MicroStrategy’s Bitcoin premium fluctuated between -30% and +200%, peaking at 3.89x mNAV on November 20, 2024—before falling below 1x by end-2025 amid influx of alternative asset management tools. This comparison offers analytical value but exaggerates similarity.

MicroStrategy sustains its premium by issuing equity at a premium to buy more Bitcoin—and has issued $8.2B in convertible bonds across six issuances, with a weighted-average coupon rate of 0.42%.

Its capital structure also incurs rising costs: as of August 2025, annual dividend obligations on STRK, STRF, STRD, and STRC series preferred shares totaled ~$588M—and continue growing with new issuances.

$DEUS could replicate one mechanism: if markets price $DEUS at a premium, the treasury could deploy funds to buy more robotics positions—boosting NAV faster than dilution. But it cannot replicate Nasdaq’s liquidity (DEUS has not undergone TGE testing), real-time pricing (Bitcoin trades 24/7; private robotics equity uses quarterly pricing), or debt market access.

A structural advantage for XMAQUINA: its underlying robotics equity has clear exit paths (IPO, acquisition) generating discrete value realization events—unlike Bitcoin, which relies on continuous appreciation.

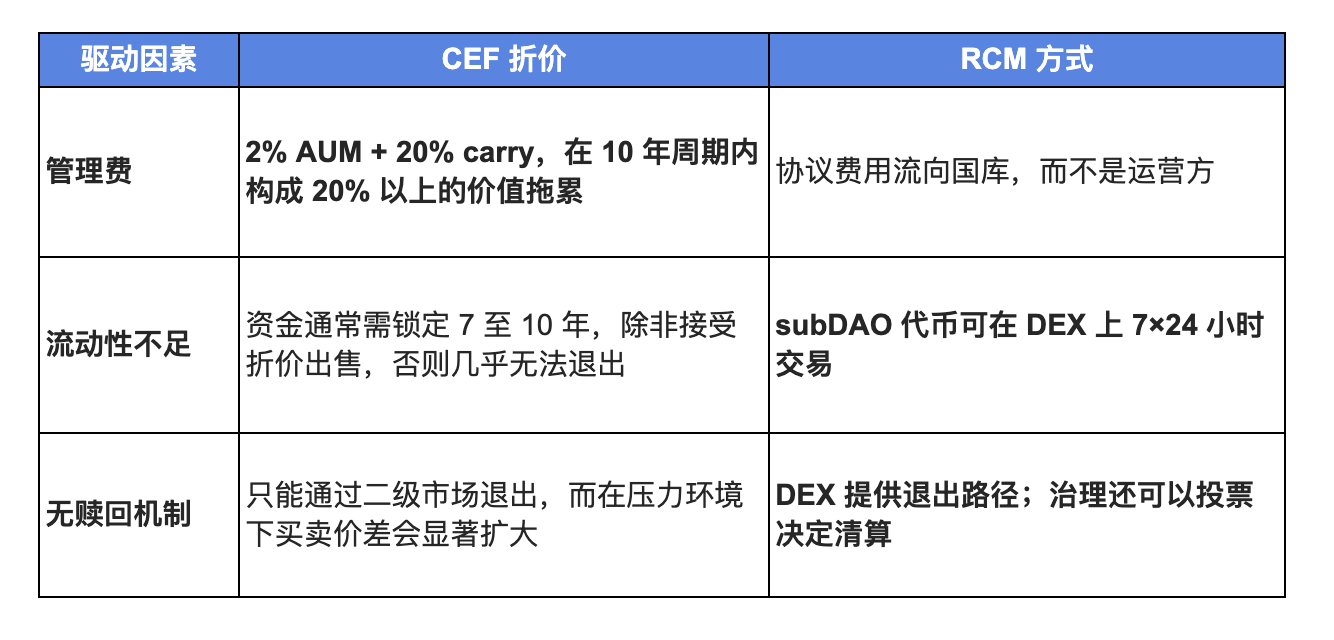

CEF Discount Drivers

Most closed-end funds trade persistently below NAV, with traditional funds exhibiting discounts of 9%–14%.

Scarcity-exposure funds often trade well above NAV—RoboStrategy exemplifies this. RCM addresses two of the three structural drivers:

Redemption mechanism is partial: DEX exits depend on counterparty liquidity in subDAO token pools. Depth will develop as trading volume grows.

Governance Value: Theoretical Framework

Note: This section estimates governance value using traditional fund economics—not actual cash flows paid or received by $DEUS holders. The DAO charges no management fee. No one pays 2/20. This is an analytical exercise—not a description of real cash flows.

$DEUS holders control treasury allocation, exit timing, and fee usage—governance rights possessing standalone economic value independent of underlying assets. Under traditional fund valuation logic, capital-allocation control typically commands a 2x–4x multiple on annual management fee.

Assuming a $28M nominal treasury and a 2% traditional fund fee, annual management fee income would be ~$560K; assuming a ~$10M working treasury (excluding $DEUS), annual fee would be ~$200K. Capitalized at 2x–4x, governance value is ~$400K–$800K—or $1.1M–$2.2M under nominal口径. Against current circulating supply, this translates to ~$0.0013–$0.007 per token.

Relative to the $0.06 Genesis price, governance value accounts for ~2%–12% of current token price. This serves better as a reference split between governance premium and asset backing—not as a real-world revenue stream.

This framework’s validity rests on several premises: governance must be actively exercised, treasury effectively managed, and RCM protocol fees meaningfully scaled. If RCM annual fees reach $1M–$2M, governance value’s contribution to current token price could rise to 7%–33% under this framework.

3.3 DEUS LABS

DEUS Labs is XMAQUINA’s internal development studio, operating as an independent sub-DAO.

Unlike the DAO treasury—which acquires minority stakes in later-stage external companies—DEUS Labs builds new companies from scratch, with the DAO holding >20% equity. Robotico is the first incubated project. Return profiles differ: external investments (e.g., Figure AI or Apptronik) capture established valuations; incubations offer pre-seed economics—with successful Series A rounds potentially delivering 10–50x returns.

Per the roadmap, the second incubated project (undisclosed) is slated for Q4 2026. If DEUS Labs incubates two or three viable companies within 24 months, DAO-held equity could become the highest-returning asset class in the treasury.

Robotico: An Intelligent Platform for the Humanoid Robot Economy

Robotico passed BOT-10 approval (83.9% support, 3.29M votes). As the sole pre-seed investor, the DAO acquired 20% equity at an $800K pre-money valuation for $200K (3.1% of robotics portfolio).

The platform aggregates and builds data for humanoid robotics companies—serving investors, researchers, and developers. Core features include: a global directory of 50+ humanoid robotics firms; AI-driven signal monitoring (PR, research, funding, patents); VC tracking; an editorial platform with CMS and newsletter; and a creator publishing program featuring monetizable expert profiles.

Founding team includes Ben Knaus (10+ years in Web3, AI, and data infrastructure; M&A deals exceeding $160M) and Favio Velarde (ex-Growth Lead at Sologenic, Coreum, SoloTex).

Robotico serves three functions in the XMAQUINA ecosystem: user acquisition (attracting robotics-interested users to the DAO); RCM distribution (linking company profiles to subDAO token markets); and equity appreciation (DAO holds 20% equity in a company building industry-specific data infrastructure).

4. Catalysts & Risks

Catalysts:

1. TGE and Exchange Listing

Post-TGE, $DEUS gains full transferability and enters exchange trading. The resulting first market price will determine whether $DEUS begins trading above or below the $0.06 Genesis price—and becomes the real-world anchor for all subsequent NAV premium discussions.

2. RCM Protocol Launch (Q3 2026)

The launch of the first subDAO markets marks XMAQUINA’s transition from a “holding DAO” to a “protocol-based capital markets platform.” Trading volume in the first 30–60 days post-launch will directly test whether the fee flywheel activates. Even $5M+ monthly volume would preliminarily validate the mechanism and begin generating protocol revenue for the treasury.

3. Portfolio Company IPOs or Exit Events (2027–2028)

Unitree targets a $7B IPO valuation; Figure AI and Apptronik are also viewed as potential listings in this same window. An IPO or acquisition of any existing portfolio company would directly validate XMAQUINA’s ability to capture private-stage returns for token holders.

4. New Equity Allocations

The Northstar Council has locked in multiple potential targets—including FieldAI, Skild AI, Physical Intelligence, Clone Robotics, RoboForce, AgiBot, Unitree, and Sunday Robotics. Per the roadmap, the DAO aims to complete 10 treasury positions by Q3 2026. Each new allocation expands portfolio coverage—and represents a potential new subDAO market.

5. RCM Expansion Phase (Q4 2026)

After validating initial subDAO markets, the protocol is expected to expand into perpetual contracts, prediction markets, and additional subDAO listings. This would transform RCM from a single-asset mapping tool into a more complete robotics capital markets trading layer—expanding fee revenue potential.

6. Second DEUS Labs Incubation Project (Q4 2026)

The roadmap indicates the second undisclosed incubation project will launch in Q4 2026. If the DAO again secures >20% equity at pre-seed terms, this would double DEUS Labs’ incubation portfolio—and test whether it can produce replicable, high-upside investment sources.

Risk Factors:

1. Regulatory Risk

Although subDAO tokens structurally confer no equity rights, regulatory classification remains highly uncertain. XMAQUINA has obtained legal opinions from three law firms concluding $DEUS qualifies as a functional token outside the Howey Test—and covering five jurisdictions. However, these conclusions remain untested in actual enforcement environments. RCM intends to adopt a Reg S framework with KYC/KYB requirements—but subDAO tokens lack direct precedent in regulatory classification. Meanwhile, the SEC/CFTC’s March 2026 guidance reaffirms that investment contract analysis does not disappear merely because a token bears a particular name.

2. Counterparty and Custodial Risk

Andersen LLP has issued attestation letters for six treasury allocations—but timelines for verifying the remaining two positions and future allocations remain unspecified. While SPVs execute through regulated broker-dealers with up to $500K SIPC protection per account, this protection does not cover investment losses or underlying company failure risks.

3. Treasury Concentration and Self-Valuation Risk

Of the $28M nominal treasury, $18M comes from DAO-held $DEUS valued at the $0.06 Genesis auction price—a price not yet validated by public markets. Thus, the operationally meaningful working treasury stands at ~$10M. Further, 84% of the robotics portfolio concentrates in the top three positions—all private companies with immature commercialization and valuations based on latest funding rounds. Notably, Figure AI and 1X common share positions rank junior to preferred shares in liquidation structures.

4. Down-Round Valuation Risk

If portfolio companies raise at valuations below prior rounds, DAO’s book value declines and treasury NAV compresses. This risk is especially acute for Figure AI and 1X common share positions in liquidation or restructuring scenarios.

5. Routing Asset Risk

$DEUS is designed as the base-pair asset for all subDAO trading pairs—but if liquidity fragments across many markets, high slippage may erode its practical utility. Users may then prefer stablecoin-mediated trades, relegating $DEUS to a formal—but functionally inert—base asset. Only sufficient liquidity depth across subDAO markets can resolve this.

6. Key Person Risk

Current deal-sourcing capability remains heavily reliant on the core team and its network. Though risk is mitigated by three co-founders, Scoring Committee advisors, and institutional partnerships with Tier-1 and Tier-2 market platforms, no formal succession plan has been disclosed—leaving key person risk intact.

7. Unlock Dilution Risk

Over the next 48 months, 685.3M tokens will gradually unlock. If treasury growth fails to outpace token dilution, per-token NAV falls from $0.089 (current circulating basis) to $0.028 (fully diluted). Additionally, 99M $DEUS allocated to DAO Treasury will unlock at TGE and may be deployed or sold via governance vote—introducing additional supply pressure at launch.

5. Conclusion

XMAQUINA has accomplished something most on-chain projects still only narrate: it has placed DAO capital onto the cap tables of seven unlisted humanoid robotics companies. These positions are document-backed, the treasury structure is relatively transparent, and at least two allocations have delivered significant appreciation since inception—1X’s position up 119%, Apptronik’s preferred shares up 100%. The current treasury totals ~$28 million—spanning equity, crypto assets, and cash—and is managed by a governance system that has passed 14 proposals with an average quorum of 6.7x.

Yet what truly determines its investment merit isn’t these completed allocations—but whether this model can scale. The RCM Protocol is XMAQUINA’s pivot from a DAO holding tool to a compounding-capable capital markets protocol. If RCM fails to generate real trading volume, $DEUS is essentially a governance claim on a ~$10 million working treasury; but if RCM succeeds, $DEUS gains exposure to protocol fee revenue, structural demand from subDAO trading pairs, and governance premium on an ever-expanding asset pool. That distinction is the core of the entire investment thesis.

XMAQUINA warrants ongoing attention—not only because the humanoid robotics sector is experiencing rapid capital inflows, but because it attempts to build an on-chain mechanism for retail participation in private robotics equity before the IPO window opens.

In 2025, humanoid robotics funding totaled $14 billion—and market consensus expects a wave of IPOs in 2027–2028. Currently, private capital flowing into this sector vastly exceeds channels accessible to ordinary investors. XMAQUINA is not the only project tackling this problem—but it is among the few that has secured real equity, operates a live governance system, and possesses a community-supported protocol roadmap.

Ultimately, buying $DEUS at $0.06 is a bet on a central thesis: Can RCM generate sufficient trading volume and protocol value growth before full token unlock pressure hits—or will underlying equity positions appreciate and realize value first?

This framework is for informational purposes only and does not constitute investment advice. Asset allocation should reflect individual risk tolerance.

Disclaimer

This report was commissioned by XMAQUINA. Khala Research received compensation for producing this report. All analysis, conclusions, and risk assessments were developed independently by Khala Research. This report does not constitute investment advice, an offer to buy or sell any asset, or any form of recommendation. The $DEUS token has not yet been issued. Readers should conduct their own due diligence and consult legal and financial advisors before making any investment decisions.

Appendix

$DEUS Tokenomics

Source: XMAQUINA Documentation, May 2026.

Max Supply: 1B (fixed, no inflation). TGE Circulating Supply: ~31.5%, of which 9.9% is DAO Treasury (locked). ERC-20 standard, cross-chain compatible. Governance: veToken (xDEUS).

Note: 33% of the 300M DAO Treasury allocation (99M $DEUS) unlocks at TGE and may theoretically be deployed or sold via governance vote—potentially intensifying initial supply pressure.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News