ADI's Hidden Victory: The Infrastructure Blueprint for the Traditional Financial Ecosystem

TechFlow Selected TechFlow Selected

ADI's Hidden Victory: The Infrastructure Blueprint for the Traditional Financial Ecosystem

ADI Chain aims to first connect existing capital, assets, and transaction processes from real-world finance to the chain, and then have these flows support $ADI use cases in turn.

Author: ADI Chain

ADI Chain, A Chain Starting from the Backend

Unlike the L2 chains familiar to the public, ADI Chain has a different positioning.

It is not a chain built around a single application, nor is it a trading venue serving only Crypto users. From the start, it has targeted governments, banks, financial institutions, and enterprise-level applications, attempting to undertake stablecoin settlement, real-world asset tokenization, payment networks, and institutional asset infrastructure.

In the past few years, the common path for new public chains often started from within Crypto: first building a developer ecosystem, then attracting DeFi, NFT, meme, airdrops, and points, using TVL, trading volume, and DAU to prove market fit, before moving closer to the institutional world.

The pressure encountered by this path is now becoming increasingly obvious.

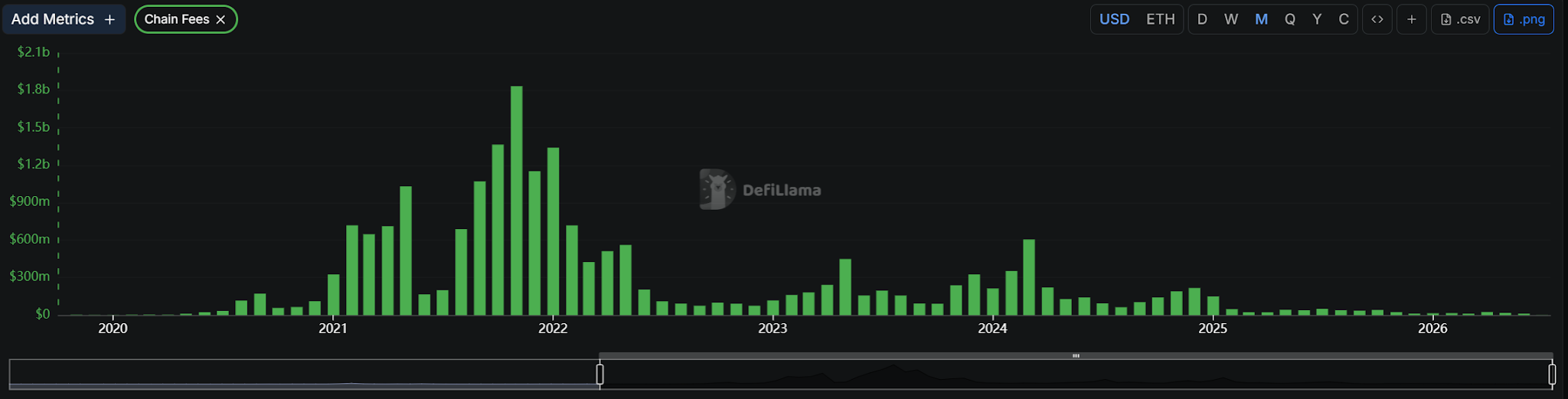

Public chain activity largely depends on asset activity, and a chain's ability to continuously create new assets, new narratives, and new reasons for trading is limited. After the meme craze subsides, trading volume will fall; after airdrop expectations end, users will leave; even foundational networks like Ethereum have long faced the tug-of-war between application growth and asset activity.

ETH network fees fluctuate significantly with the on-chain asset cycle, data source: DeFiLlama

ADI Chain's path is more like the reverse.

It does not first create a round of asset hype on-chain and then wait for capital and institutions to enter; it attempts to move financial activities that already exist in the real world onto the chain: issuance and settlement of stablecoins, tokenization of real assets, custody and circulation of institutional assets, and capital movement within payment networks.

This path is most clearly seen in stablecoins.

What best embodies ADI Chain's path is not $USDT or $USDC, which target global crypto user liquidity, but rather $DDSC, which has more regional and institutional direction.

$DDSC is a stablecoin pegged to the Dirham, backed by connections to FAB, IHC, ADQ, and the UAE Central Bank authorized framework. It does not serve general trading scenarios, but rather payments, settlement, and institutional capital circulation within the UAE local financial system.

A recent large public transaction occurred in May.

IHC showed in Abu Dhabi Securities Exchange disclosure documents that it completed a transaction of 110 million Dirhams, approximately 30 million USD, on ADI Chain via $DDSC. The disclosure document stated:

This is one of the largest single stablecoin transactions in the region.

The same choice also appears with $PUSD.

This stablecoin, issued by Palm Azgar Finance, emphasizes not trading liquidity first, but compliance with Islamic law. According to reports, $PUSD targets corporate treasury departments, exchanges, and payment processing institutions, with a circulation of approximately 2.3 billion USD, targeting a market of the Islamic financial system sized over 3 trillion USD.

At this point, the first layer of ADI Chain's path is already clear: first bring in settlement demands from the regional financial system.

$DDSC corresponds to UAE local institutional capital circulation, while $PUSD corresponds to the larger Islamic financial market. They do not solve the problem of "whether there are stablecoins on-chain," but rather whether money in regional finance can enter on-chain in a way acceptable to institutions.

This is also the premise for the subsequent payment network to be established. Whether it is the Mastercard cooperation targeting Middle East cross-border payments, or M-Pesa covering 8 markets in Africa with over 60 million monthly active users, what is truly needed is not another on-chain asset, but an underlying network capable of undertaking settlement and capital flow.

Only after money comes in first and is able to flow, is the next step assets.

From Regional Settlement to Institutional Assets

But ADI Chain's layout is certainly not limited to the Middle East.

If $DDSC and $PUSD prove its entry into the regional financial system, then international institutions and infrastructure service providers like BlackRock, Franklin Templeton, BNY, and SettleMint correspond to another line: how global assets enter this on-chain financial network.

The first thing that cannot be bypassed in this matter is custody.

In May, BNY announced a partnership with Finstreet and ADI Foundation, planning to provide institutional-grade digital asset custody within ADGM, extending to ADI Chain. For institutional assets, custody is not an ancillary service, but the entry point itself. If assets are not compliantly custodied, there will be no subsequent issuance, trading, and settlement.

Source: Official Press Release

After custody, it is time for issuance.

The cooperation between ADI Foundation and SettleMint falls on the digital securities side. SettleMint is an institution-facing tokenization infrastructure service provider, and the cooperation occurred under the ADGM framework. In other words, what ADI wants to connect is not a packaged RWA product, but the digital securities process within a regulated environment.

Further out, there are asset management institutions.

BlackRock and Franklin Templeton appearing here is not just about adding two familiar big names. If RWA relies only on on-chain protocols to package assets themselves, it will soon reach a dead end. What can truly bring assets in are traditional asset managers, custodians, issuance tools, and settlement networks.

Only when these lines are put together does ADI Chain's asset narrative hold water.

It does not first write an "RWA" label and then stuff partners inside. It starts from the most troublesome places where assets enter the financial system: where assets are placed, who issues them, who manages them, and finally in which network they circulate.

When Real Finance Becomes On-Chain Cost

At this point, ADI's resource puzzle has basically unfolded.

Regional stablecoins, institutional custody, digital securities infrastructure, and asset management institutions appear to belong to different businesses, but they ultimately all point to the same question: can they be continuously put into the ADI Chain network.

This is where $ADI stands.

It is not a token serving a single application, nor is it an accessory to a certain type of asset. The value of $ADI depends on whether ADI Chain can organize these entry points, capital, and assets into a continuously running ecosystem.

If these cooperations are just independent progressions from each other, $ADI gets only associated narratives; if they truly conduct trading, settlement, and asset circulation on the same chain, $ADI serves as the underlying fuel repeatedly utilized during the operation of the ADI ecosystem.

This is also where ADI Chain's path differs from many public chains.

It does not first create a round of asset hype on-chain and then wait for external capital to enter; it attempts to first connect capital, assets, and transaction processes that already exist in real-world finance onto the chain, and then let these flows support $ADI's usage scenarios in return.

What truly determines the value of $ADI is whether these entry points, after being seen, can continue to bring capital, assets, and transactions back to ADI Chain.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News