Bitcoin spot ETFs are volatile, but miners have nowhere left to lament

TechFlow Selected TechFlow Selected

Bitcoin spot ETFs are volatile, but miners have nowhere left to lament

The arrival of spot ETFs has not yet happened, but it has essentially shattered the computing power pricing system that miners built over many years.

Author: Zuo Ye

Will Bitcoin Spot ETFs Spell the End for Miners?

With the arrival of Bitcoin spot ETFs, the SEC has successfully captured market sentiment. Attention is now focused on BlackRock and the battle between bulls and bears, while the miners' sorrow goes unnoticed.

Inscriptions Boom, Miners Profit

In 2023, amid the backdrop of Bitcoin halving, miners chose to support inscriptions to increase fee-based income beyond block rewards. However, the arrival of spot ETFs does not harm miners' interests in terms of price—in fact, it may even boost their passive income:

-

Approval of spot ETFs allows more traditional investors and retail participants to legally purchase Bitcoin, supporting its market price;

-

Layer-2 protocols like the Lightning Network receive legitimacy boosts, increasing small and frequent on-chain activities that raise mainnet transaction fees, thus stabilizing the ecosystem.

Unlike Ethereum’s transition to PoS, where miners were powerless and projects like ETHW ultimately fizzled out, the triad of Bitcoin ASIC manufacturers, miners, and mining pools remains strong. In past battles over block size expansion and the recent inscription wars, miners have demonstrated influence over Bitcoin no less than core developers or protocol creators.

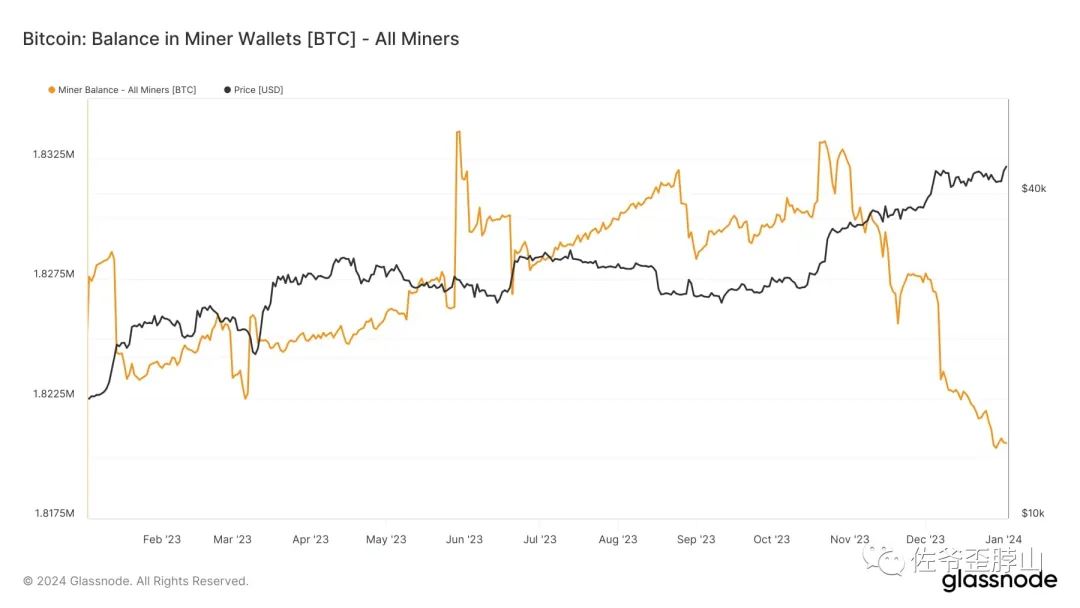

Yet against giants like BlackRock, the entire crypto market—valued in trillions—is dwarfed. While miners may stay silent publicly, their on-chain behavior tells a different story: for the past two months, they’ve been steadily selling off holdings. This trend reflects not only concerns over ETF approval being priced in and subsequent price drops, but also a growing long-term awareness among miners of deeper structural shifts.

Pricing power is shifting from on-chain + miners to off-chain + Wall Street.

The Migration of Pricing Power: East → West, Satoshi → Miners → Wall Street?

The core of Bitcoin's pricing power lies in hash power.

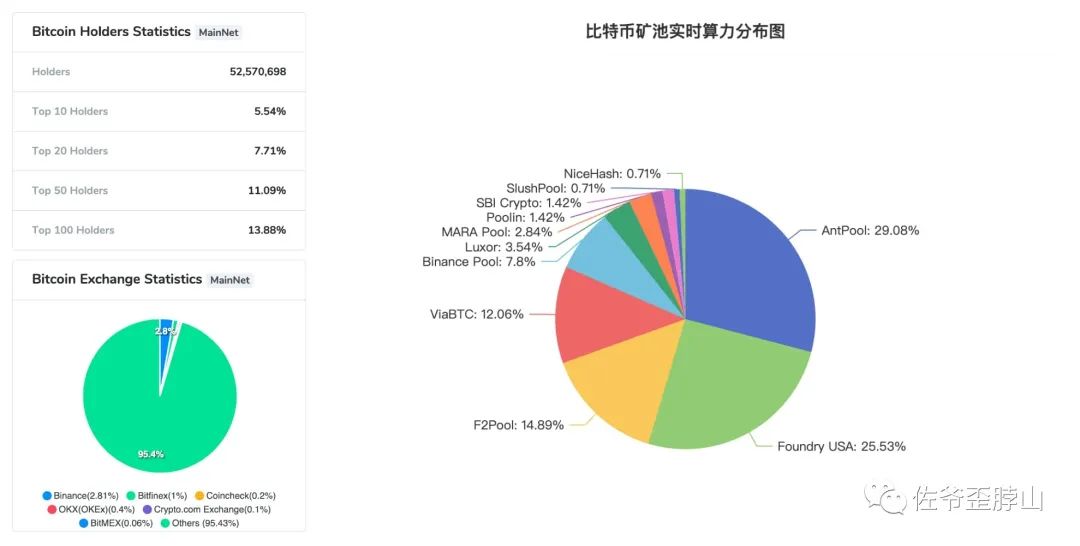

After the 2021 regulatory crackdown in China, hash power inevitably shifted westward—especially to the United States—a point well established. Alongside this geographic shift is an ongoing centralization of mining pools. Driven by capital efficiency, miners and pools form alliances with clear roles: miners retain control over hardware, while pools manage daily operations. The logic is simple:

Miner Revenue = (Hardware Value - Electricity Cost - Pool Fee) × Number of Machines × Depreciation Rate

Throughout bull and bear cycles, the so-called shutdown price poses the greatest risk to mining pool operators and ASIC manufacturers. Miners can endure paper losses and wait for the next bull run to sell at breakeven, but pool operators and hardware makers are in the business of providing services ("selling water"). If revenues fall short of costs, they face existential threats.

Ultimately, miner losses stem from insufficient revenue to cover expenses—but electricity is usually the only major cost. Even in distress, selling coins can bring back some liquidity.

Mining Pool Centralization, the Crowd Comes Ashore

Fifteen years since Bitcoin’s genesis block, about ten years since large-scale ASIC mining began—Satoshi’s PoW mechanism, though environmentally costly, has proven robust enough to carry miners through at least five market cycles, earning immense credit.

Early miners weren’t purely capitalists. Many came from society’s fringes—gamblers, internet cafe owners, crypto geeks, and random pioneers. The raw chaos of the early market created instant millionaires. MicroStrategy entered at four- or five-digit prices; some early adopters paid single-digit dollars. Either way, massive profits were guaranteed.

But everything is about to change.

Bitcoin’s price will shift from being driven by hash power to being driven by markets, sentiment, and Wall Street.

Bitcoin spot ETFs differ fundamentally from futures ETFs or mining company ETFs—they will alter Bitcoin’s pricing and operational logic at its core.

Driven by capital appreciation, the concentration of existing Bitcoin holdings will intensify further. Compared to other cryptocurrencies, Bitcoin already has relatively decentralized ownership. Combined with its massive hash power, achieving a 51% attack on the network is practically impossible under PoW.

But this is PoW logic. With massive institutional capital flooding in, Bitcoin could become functionally similar to a PoS system—not in how new coins are minted, but in how token concentration creates backward causality. In theory, spot assets price derivatives. But with long transmission chains, feedback and pricing mechanisms can become unbalanced.

Recall the 2007 subprime crisis: lenders repackaged bad loans into securities, until the original mortgages lost their market signaling role. Bitcoin has the objective conditions to repeat such a scenario.

Spot listing, corporate war, miner death—how smooth that sounds.

Bitcoin Still Lacks an Ecosystem

The boom in inscriptions and Layer-2 activity is still just patching up old mechanisms.

Bitcoin’s original purpose has been repeated endlessly until people grow tired of hearing it—peer-to-peer electronic cash. During bear markets, small-payment innovations based on the Lightning Network were tested in Latin American countries like Argentina.

Now, people embrace Bitcoin’s sacredness, yet abuse block space like force-feeding ducks.

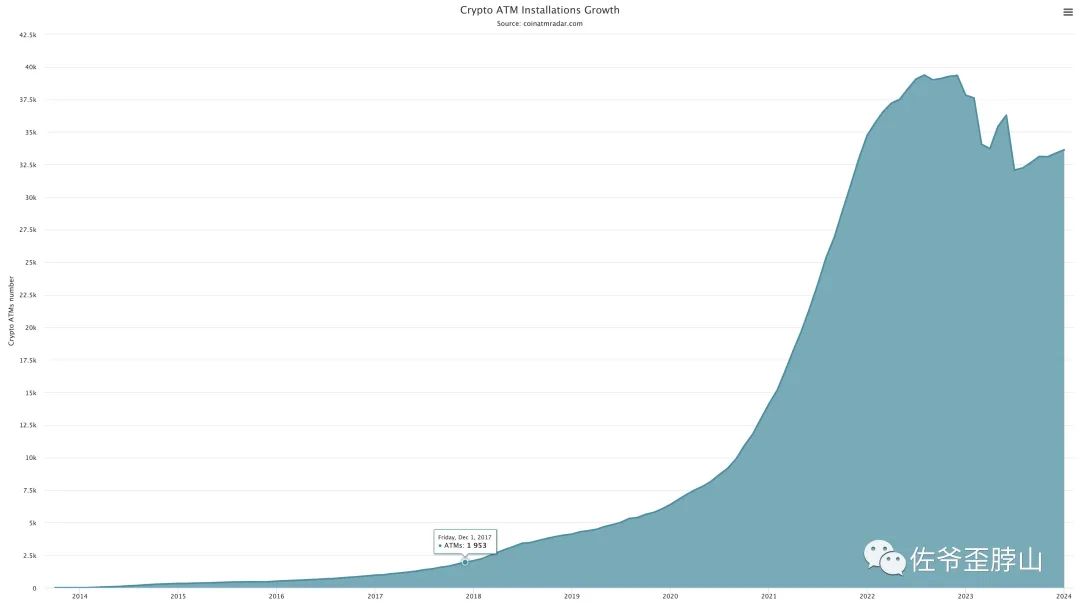

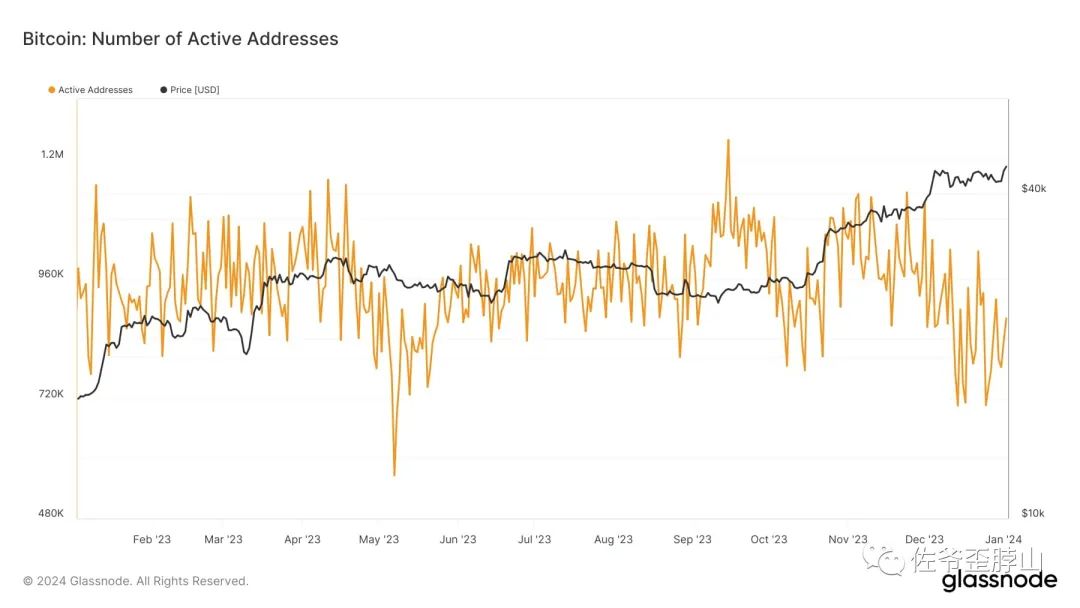

Regarding adoption, Bitcoin ATMs and active on-chain addresses have slightly declined recently. Bitcoin needs physical hardware to establish real peer-to-peer connections in the physical world—a need that may expand significantly with ETFs.

On active addresses, Bitcoin has gradually fallen below the psychological threshold of 1 million, creating a strange phenomenon of “on-chain decline, off-chain hype.” Everyone talks about Bitcoin, yet fewer actually use it. How can a currency circulate if no one uses it?

Herein lies a logical paradox: lack of ecosystem leads to low usage; low usage undermines price support; weak prices push miners to sell; miner selling enables off-chain accumulation; off-chain holders gradually seize pricing power.

This mirrors internet-era strategies of burning money to capture market share. Once monopoly is achieved, players extract "rent," harvesting industry after industry—from the group-buying wars to Didi-Kuaide consolidation—all following the same playbook.

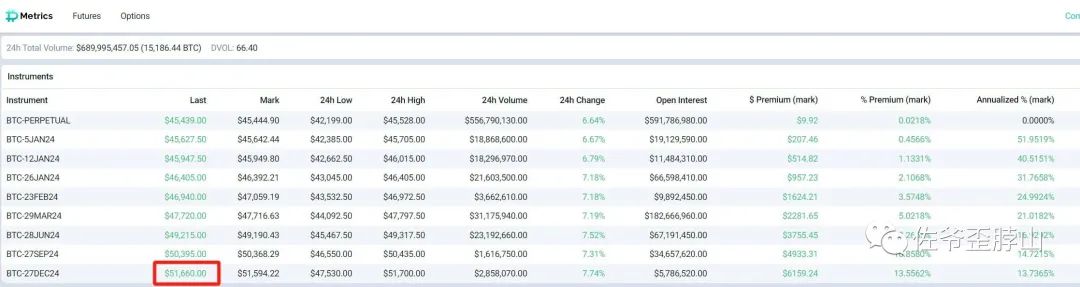

Today, fueled by ETF optimism, Bitcoin’s year-end options briefly soared above $51,000, severely deviating from spot prices. Bitcoin’s price is now largely disconnected from its utility and miner hash power—it has become the ultimate meme coin. Nothing matters more than sentiment.

Then, within moments, the price plunged from $45,000 to below $40,000—volatility rivaling that of altcoins.

Conclusion: Sacredness Will Eventually Collapse

Even before spot ETFs officially arrive, they’ve already shattered the hash-power-driven pricing system miners spent years building. People often say Bitcoin is unlike any other coin—a unique spark that developed religious-like sacredness among believers. Now, the dream shatters. Dust to dust. Look around—you don’t hear a single miner’s voice. Maybe they’re still caught up in the joy of inscription profits and cashing out.

Bitcoin spot ETFs move freely in and out. But will the last bastion of PoW miners fade into history?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News