Coinbase: Opportunities in Tokenization and the New Market Cycle

TechFlow Selected TechFlow Selected

Coinbase: Opportunities in Tokenization and the New Market Cycle

Under a high-interest-rate environment, the benefits of tokenization—capital efficiency, faster settlement, increased liquidity, reduced transaction costs, and improved risk management—are evident.

Authors: David Duong, David Han

Translation: Block unicorn

The progress, benefits, challenges, and outlook for the future of tokenization. Asset tokenization—long pursued by the crypto industry—is gradually gaining momentum and adoption among institutions.

In 2017, the hype around tokenization primarily revolved around creating digital assets on blockchains that represent ownership of illiquid physical assets such as real estate, commodities, art, or collectibles. However, today’s high-yield environment has given tokenization a different meaning—digitizing financial assets like sovereign bonds, money market funds, and repurchase agreements (repos).

We believe this could be a significant use case for traditional financial institutions and may become an important part of the next crypto market cycle, although full implementation might take another one to two years. Compared to 2017, when opportunity costs were close to 1.0–1.5%, we believe today's nominal interest rates above 5.0% make capital efficiency from instant (versus T+2) settlement much clearer to financial institutions. Furthermore, in our view, the ability to operate around the clock, automate intermediary functions, and maintain transparent audit trails can make simple on-chain payments and settlements highly powerful.

However, infrastructure and legal (jurisdictional) issues remain core challenges. Most institutions rely on private blockchains because they are concerned about risks associated with public networks—such as smart contract vulnerabilities, oracle manipulation, and network failures. But we believe private networks could eventually make interoperability more difficult, potentially resulting in fragmented liquidity, which would hinder realization of tokenization’s full benefits, including functional secondary markets.

Tokenization Failed to Deliver on Its Initial Promise

During the 2017 crypto winter, tokenization appeared to fall short of its original promise—to bring trillions of dollars worth of real-world assets (RWA) on-chain. The prevailing idea at the time was that issuers would convert ownership rights of illiquid physical assets—like real estate, commodities, art, and other collectibles—into digital tokens residing on distributed ledgers. Benefits included fractional ownership of these assets, enabling broader access to otherwise hard-to-reach investments and democratizing asset ownership.

Even today, real estate remains a particularly promising opportunity for tokenization, especially considering ongoing concerns about housing affordability, particularly for younger generations. Yet despite a well-defined use case, tokenization failed to gain meaningful traction in 2017. Instead, the next crypto market cycle was driven by experimentation in decentralized finance (DeFi), while tokenization’s disruptive potential was clearly sidelined.

We believe the recent resurgence of interest in tokenization is partly due to the 2022 crypto sell-off, during which many advocates emphasized the fundamental value of blockchain technology over token speculation. This echoes the now-familiar refrain “blockchain, not Bitcoin”—a dismissive phrase often used by skeptics in the crypto space, suggesting current enthusiasm for these projects may only last until crypto price action recovers.

What Has Changed in the Market?

While we acknowledge some validity to this criticism, the current crypto cycle differs from previous bear markets in several key ways. Most importantly, the global interest rate environment has shifted dramatically. From early 2017 to late 2018, the Federal Reserve gradually raised rates from 0.50–0.75% to 2.25–2.50%, while keeping its balance sheet relatively stable. In contrast, during the current hiking cycle (beginning March 2022), the Fed has increased rates by a full 525 basis points to 5.25–5.50% and reduced its balance sheet by over $1 trillion in the past 18 months.

From a consumer perspective, higher short-term bond yields have prompted retail and individual investors to seek better returns. This demand has been channeled into protocols aiming to access tokenized U.S. Treasury markets in ways that did not exist in 2017. (The two largest stablecoins—USDT and USDC—do not natively earn interest.) The regional banking crisis in March 2023 further highlighted the unattractive yields on existing customer deposits. Thus, in our view, tokenized products have the potential to drive on-chain activity, but regulatory hurdles could impede broad development and adoption, potentially disadvantaging U.S. consumers.

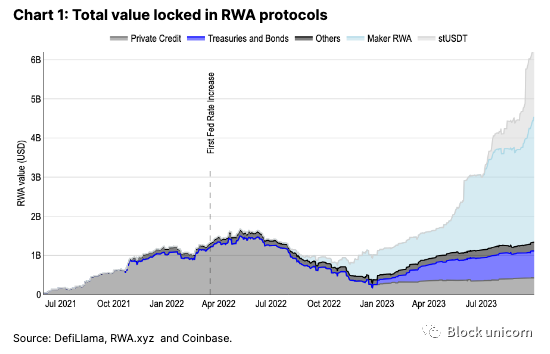

Over the past year, rising interest rates have been reflected in RWA (real-world asset) protocols shifting allocations from private credit toward U.S. Treasuries (see Figure 1). Notably, the amount of RWA collateral held within Maker DAO has grown significantly, backing the issuance of over $3 billion in DAI stablecoins. As long- and short-term yields rise in traditional finance, increasing borrowing costs there, DAI’s relatively low borrowing rate (around 5.5%) is becoming increasingly competitive.

Meanwhile, for institutional investors, the cost of capital lock-up in high-rate environments is far higher than in low-rate ones. Currently, most traditional securities transactions settle in two business days (T+2), during which funds are locked between buyer and seller, leading to inefficient capital utilization. In 2017, when nominal yields hovered near 1.0–1.5%, market participants effectively paid negative real interest rates for this delay. Today, nominal yields above 5% translate into pre-tax real yields of approximately 3% annually. Therefore, for markets with daily trading volumes ranging from hundreds of billions to over a trillion dollars, capital efficiency has become significantly more important. We believe the value of instant settlement versus T+2 is now much clearer to traditional financial institutions—a distinction that may not have existed previously.

Over the past six years, many misconceptions about tokenization have also been clarified among senior leadership at major institutions. They now better understand the advantages of tokenization—including 24/7 operability, automation of intermediaries, and the ability to maintain transparent audit and compliance records. Additionally, because transactions can be settled atomically under delivery-versus-payment (DvP) and delivery-versus-delivery (DvD) conditions, counterparty risk is minimized. Moreover, many traditional market participants involved in tokenization today have dedicated teams that both understand existing regulations and develop technology compliant with them.

Business Cases and Outlook for Tokenization

Therefore, we believe the business case for tokenization has shifted from placing illiquid assets like real estate on-chain to capital market instruments such as U.S. Treasuries, bank deposits, money market funds, and repos. Indeed, in a 5% interest rate environment, we find JPMorgan’s tokenized intraday repo offering (for example) far more compelling than it would have been two years ago when rates were near zero. That said, many benefits of tokenization—such as improved unit economics, lower costs, faster settlement—are not new; they simply require broad-scale distribution to become effective.

Estimates of the potential size of the tokenization opportunity vary widely—from $5 trillion by 2030 according to Citigroup to $16 trillion according to Boston Consulting Group. These figures may not be as exaggerated as they initially appear. First, they include projections for central bank digital currencies (CBDCs) and stablecoin growth. In reality, the key variable explaining these differing estimates is the potential percentage of global money supply that tokenized assets might encompass.

Indeed, stablecoins today represent one of the clearest potential use cases for tokenization, whose reserves could eventually include customer deposits and liquid cash equivalents. We believe stablecoin liquidity may be one of the clearest intersections between tokenization and the broader crypto economy in the next market cycle.

Legal and Regulatory Uncertainty

Nonetheless, legal clarity regarding asset status in the U.S.—and who bears responsibility for those assets—remains unresolved. Even beyond the U.S., numerous legal and regulatory barriers continue to hinder most tokenization efforts, as many relevant laws are still nascent. Due to the market’s early-stage nature, there are no widely accepted legal precedents or templates, making the establishment of these frameworks time-consuming and expensive.

For instance, Luxembourg was one of the first countries to adopt tokenization legislation, passing its initial law in March 2019 allowing blockchain-based securities trading. Since then, it has enacted several additional laws, most recently in March 2023, permitting tokenized collateral. The EU’s Distributed Ledger Technology (DLT) pilot program only became effective in March 2023, paving the way for broader tokenization initiatives.

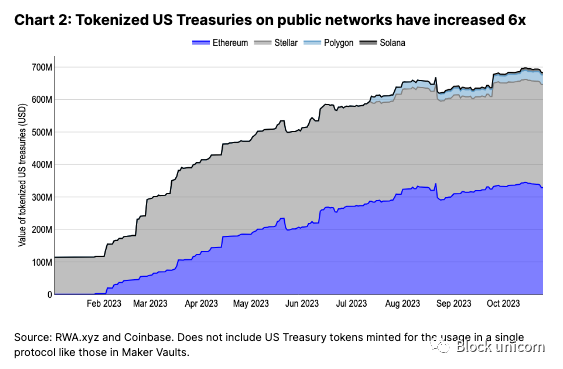

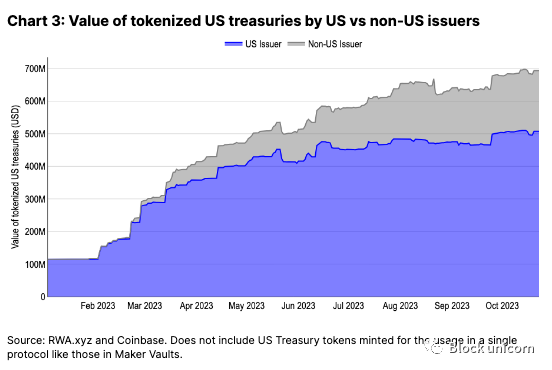

Due to this regulatory ambiguity, multiple platforms are often required to handle asset tokenization across different jurisdictions. Many on-chain tokenized treasury platforms—including OpenEden, Backed, Matrixdock, and Ondo—restrict participation to qualified investors and often exclude U.S. persons. An increasing number of U.S. Treasury token issuers are registering in non-U.S. jurisdictions (see Figure 3). The jurisdiction of issuing entities is not always clear to end users, ranging from highly regulated regions like the U.S. and Switzerland to jurisdictions like the British Virgin Islands—adding an extra layer of counterparty risk atop existing smart contract risks.

The legal structures and investor requirements for private blockchains are equally complex and only beginning to be addressed. The November 2022 issuance of the euro-denominated European Investment Bank (EIB) bond was the first digital bond issued under Luxembourg law, while the February 2023 Hong Kong Monetary Authority (HKMA) bond denominated in Hong Kong dollars was the first product regulated under Hong Kong law. The process of digitizing securities onto distributed ledger technology varies across jurisdictions, and the interaction between cryptographic ownership, physically decentralized networks, and jurisdiction-specific securities regulation remains in its early exploratory phase.

Financial Fragmentation

A direct consequence of the aforementioned legal challenges is impaired secondary market liquidity, as investors must establish new trading channels for each distinct platform. This can be time-consuming, since Know Your Customer (KYC) and Anti-Money Laundering (AML) checks across protocols and institutions are typically not shared.

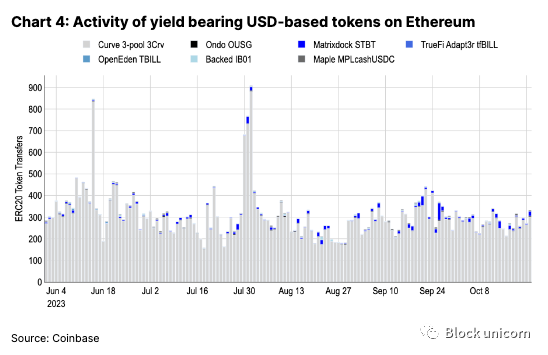

As a result, many tokenized assets struggle to achieve transparent price discovery through decentralized finance (DeFi) channels such as automated market makers (AMMs). On Ethereum, activity in tokenized Treasuries lags behind comparable non-KYC assets. See Figure 4. For example, the market cap of Curve’s DeFi-native 3Pool (3Crv) token shows no significant gap compared to Ondo Finance’s institutional-grade OUSG tokenized U.S. Treasury (USD 199 million vs. USD 140 million), despite the former having nearly 200 times more holders (i.e., 56 holders vs. 9,254). Despite its higher market cap, 3Crv has far fewer participants.

The 3Crv token sees the highest daily trading volume, despite its lower yield (as of October 24, 2022), and according to Etherscan data, attracted over 100 unique daily traders within less than a month of launch in 2020. In contrast, tokenized U.S. Treasuries on Ethereum have seen fewer than ten average daily transfers overall even nearly a year after launch. Thus, we believe investor barriers severely hinder liquidity and adoption of these assets, although controversial KYC measures introduced in Uniswap V4 could alter their future adoption and liquidity trajectory.

Permissioned Chains and Private Tokens

Additionally, many institutions opt to build their own private blockchains for tokenization, fearing risks tied to public networks—such as smart contract bugs, oracle manipulation, network outages, and key compromise. Moreover, private chains offer benefits like privacy, fee-free transactions, and mandatory KYC for all network participants.

Technology providers in the private blockchain space appear to be consolidating around four main solutions: (1) Hyperledger’s suite of platforms, (2) Consensys’ Quorum, (3) Digital Asset’s Canton, and (4) R3’s Corda. Each platform has its own unique ecosystem, but projects built on the same tech stack do not automatically interoperate due to physical network isolation. This fragmentation negatively impacts the ability to conduct atomic settlement transactions—one of tokenization’s key advantages.

Notably, some platforms only record transaction details on the blockchain without involving actual cash settlement. In these cases, cash flows through traditional banking channels (thus still relying on separate cross-bank solutions), leaving the real-time settlement process incomplete. Furthermore, using multiple platforms can fragment liquidity across different chains—a problem similar to what occurs across various public blockchain networks.

Our latest report discusses cross-chain interoperability technologies in detail, and many private blockchain providers are actively working on interoperability initiatives within their ecosystems. However, achieving interoperability between chains—especially permissioned ones—is not merely a technical issue but also involves legal and business considerations. Therefore, we believe fragmentation in interoperability and liquidity will persist in the short to medium term as platforms consolidate and the sector continues to gain legal clarity.

Conclusion: A Long Road Ahead

We expect institutional interest in tokenization to carry into the next crypto market cycle, as the benefits—capital efficiency, faster settlement, increased liquidity, lower transaction costs, improved risk management—are evident in today’s high-interest-rate environment. However, what has changed is the focus on the underlying assets being tokenized: traditional financial institutions are now prioritizing U.S. Treasuries, money market funds, and repos.

How this is implemented is crucial. We believe the next one to two years will be a period of platform consolidation across three dimensions: (1) financial verticals, (2) jurisdictional boundaries, and (3) technology stacks. Interoperability remains central because tokenizing safe assets on one chain and payment currencies on another greatly increases complexity and risk, extends settlement times, and reduces transparency. Without consolidation, the tokenization space will continue to face challenges of fragmented liquidity and difficult investor onboarding—especially in secondary markets.

However, traditional firms typically transition slowly, and many have already committed to building their own tokenization platforms. Therefore, we believe it is too early to identify likely winners, although we are confident that a flywheel effect of adoption will emerge, driven by early-mover network effects and the ability to adapt flexibly to evolving legal and technological landscapes.

Ultimately, we believe growing interest in tokenization reflects a shift in the industry—from a focus on pure decentralization toward practical combinations of centralized entities and semi-decentralized networks capable of onboarding more users. As more jurisdictions establish legal frameworks for tokenization, we expect a gradual unlocking of tokenized liquidity over the long term, driven by integration and interoperability.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News