Bitcoin Mining's Race Against Time in a Bear Market: Analysis and Investment Insights on Marathon Digital Holdings (MARA)

TechFlow Selected TechFlow Selected

Bitcoin Mining's Race Against Time in a Bear Market: Analysis and Investment Insights on Marathon Digital Holdings (MARA)

This article primarily analyzes the current operations and investment risks of Marathon Digital (MARA) and compares it with other mining companies to determine whether Mara is the strongest candidate for a short position.

Author: Yilan

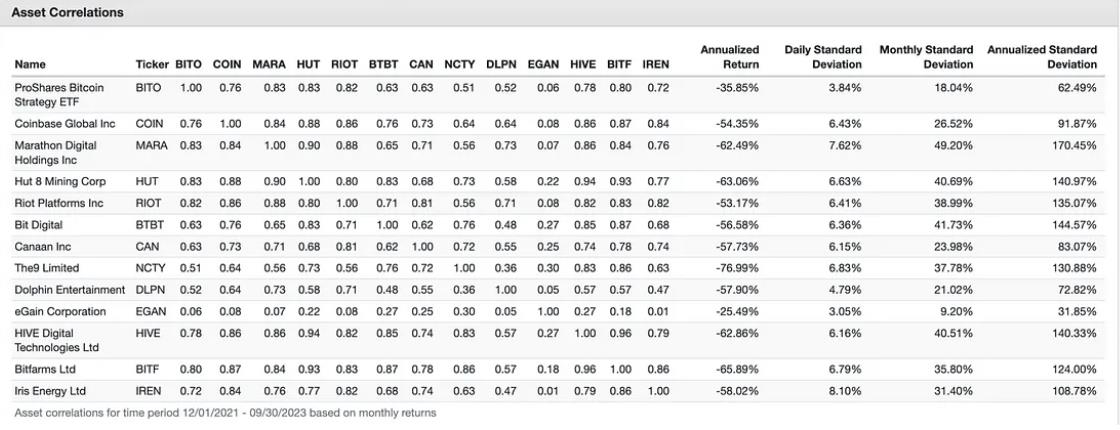

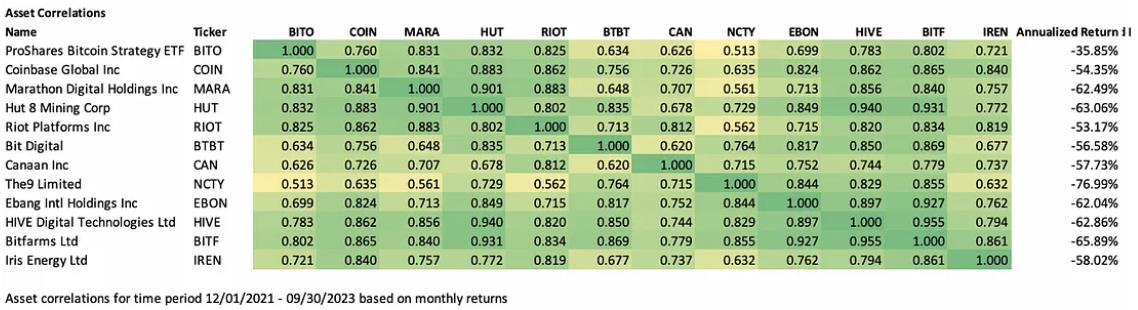

Listed blockchain-related companies operate in various sectors including mining, miner sales, chip manufacturing, digital asset management, blockchain technology provision, payment, and trading platforms. Due to differing business models, these companies exhibit varying degrees of BTC leverage, meaning their stock price fluctuations are typically more volatile than the Bitcoin spot market, with different amplification factors. Among them, mining stocks (e.g., Mara, Riot, BTBT) serve as more effective BTC price amplifiers compared to miner manufacturers or other business models. For instance, MARA demonstrates higher correlation and price elasticity to BTC prices than COIN (COIN vs. MARA correlation: 0.76 vs. 0.83; annualized standard deviation: 92% vs. 170%).

Price correlation and standard deviation of mining stocks and BITO (BITO fitted to BTC price)

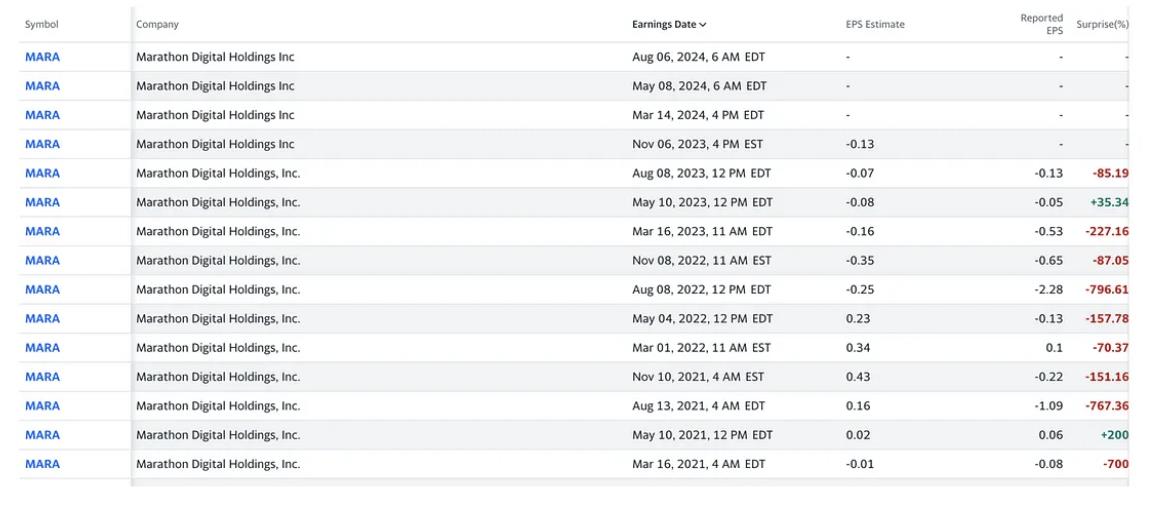

During the rebound from June 15 to July 13, MARA's share price rose by 100%, while BTC increased only 30%. However, during BTC’s subsequent correction, MARA dropped by 55% (in addition to BTC’s decline, its Q2 earnings released on August 8 showed EPS of -0.13, significantly missing expectations of -0.07, which also contributed to the downward pressure), while BTC fell by 12%. Thus, MARA’s amplification factor relative to BTC price movements this year is close to 300%, despite its annualized standard deviation being only 170%.

MARA vs. BTC price changes

Mara EPS history

This article primarily analyzes the operational status and investment risks of Marathon Digital (MARA) compared to other mining firms, assessing whether MARA is the strongest short-selling candidate.

I. Investment Thesis

1. Business Model and Operational Status

Marathon’s primary business is self-operated Bitcoin mining. Its strategy involves raising capital to purchase miners and deploy mining facilities, holding mined Bitcoin as a long-term investment after covering cash operating costs. The difference between buying miners to mine and hold Bitcoin (Mara, Hut 8, Riot) versus producing and selling mining hardware (Canaan) lies in lower R&D expenses but much higher capital expenditures. Revenue lacks resilience, relying solely on improved BTC mining efficiency and BTC price appreciation for profit. This results in high leverage and debt levels, making revenue from listed mining companies highly correlated with Bitcoin prices and subject to greater volatility. In bear markets, such firms face potential insolvency threats.

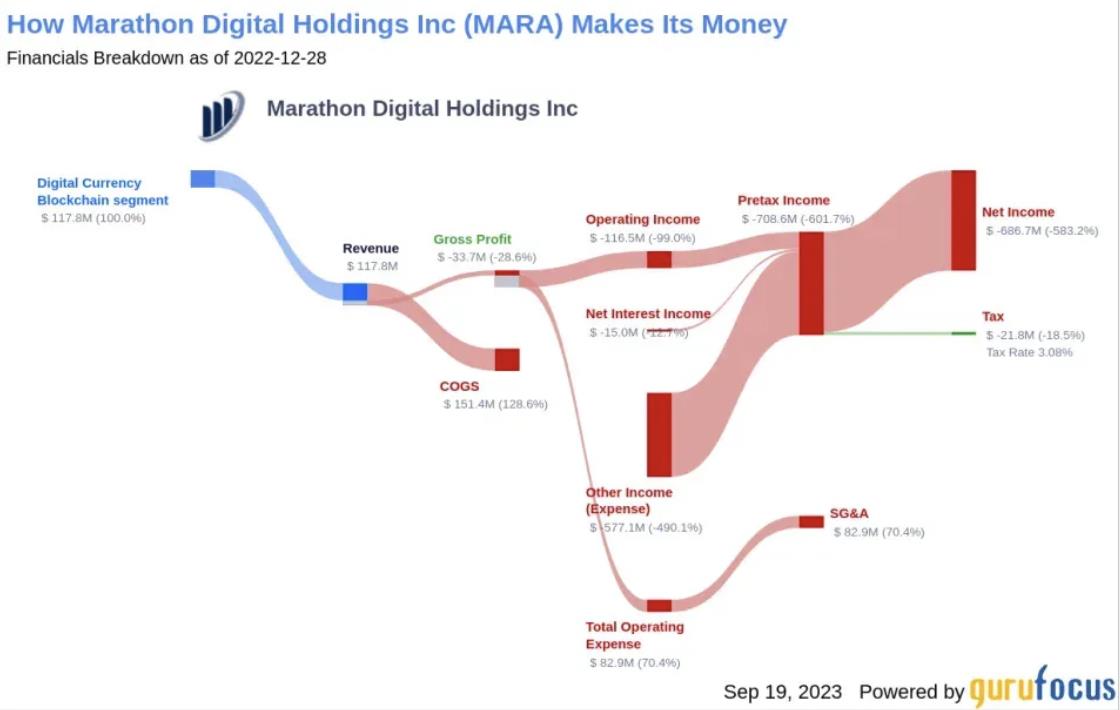

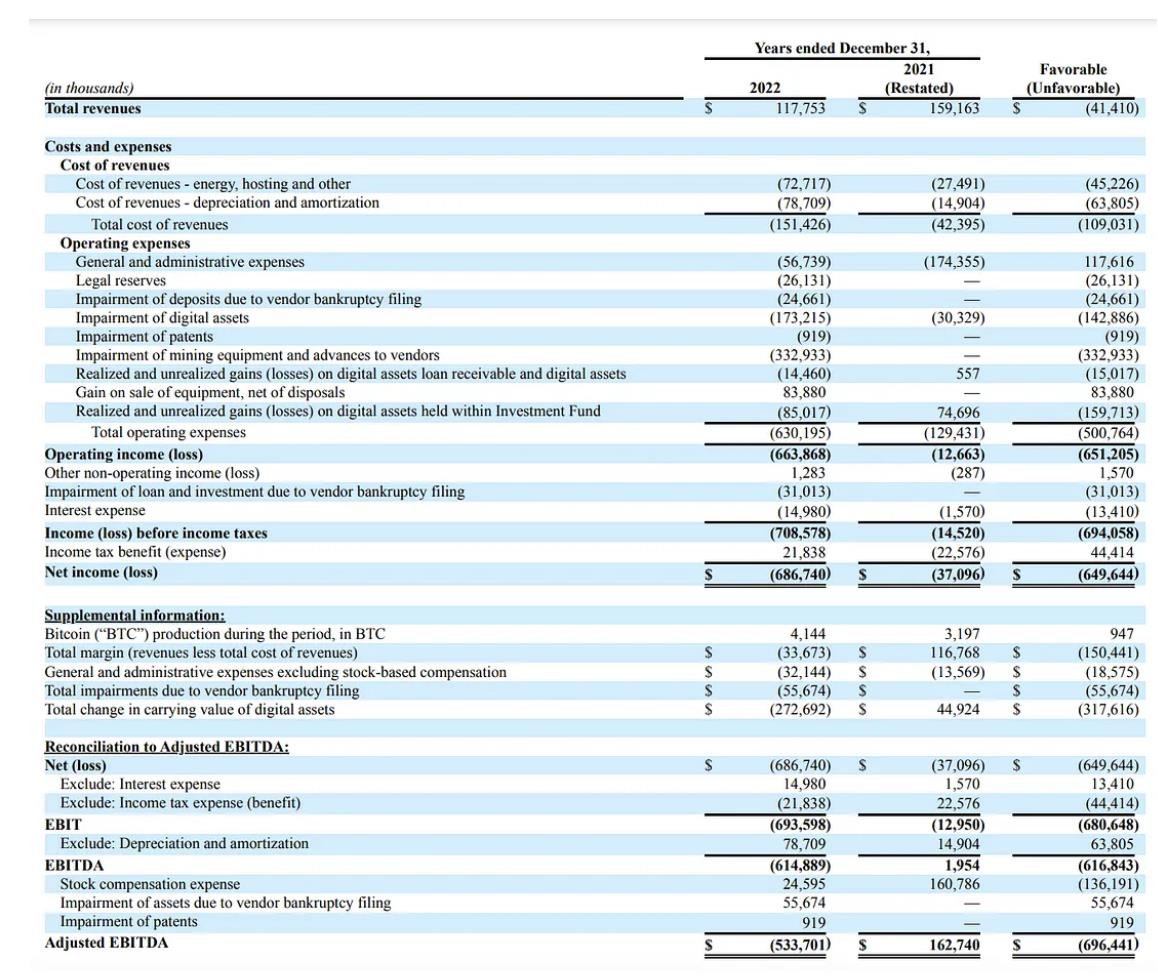

Marathon's financial position in fiscal year 2022

In terms of revenue, Marathon produced 4,144 BTC in FY2022, generating $117 million in revenue. However, this revenue was insufficient to cover expenses: $72 million in energy and mining costs, $78 million in miner depreciation and amortization, and $630 million in operations including personnel and maintenance, resulting in a net loss of $687 million. Therefore, the business model of financing miner purchases for Bitcoin mining is extremely demanding on cash flow management during bear markets.

Regarding mining efficiency and operations, Marathon’s hashrate launched in Q2 increased by 54% from 11.5 EH/s at the end of last year to 17.7 EH/s. Faster hashrate growth and improved uptime have boosted Bitcoin output (producing 2,926 BTC in Q2, approximately 3.3% of total Bitcoin network rewards during that period). Operationally, the company’s high leverage (insolvency in 22Q4) has already impacted balance sheet health. Although Q1 and Q2 saw improved stock performance due to rising BTC prices and increased deployed computing power, BTC prices remained depressed throughout 23Q3 and are expected to stay weak at least into next year. As a result, Marathon prepaid most of its convertible bonds in September to reduce interest burden on cash flow. The remaining principal amount of these notes stands at $331 million.

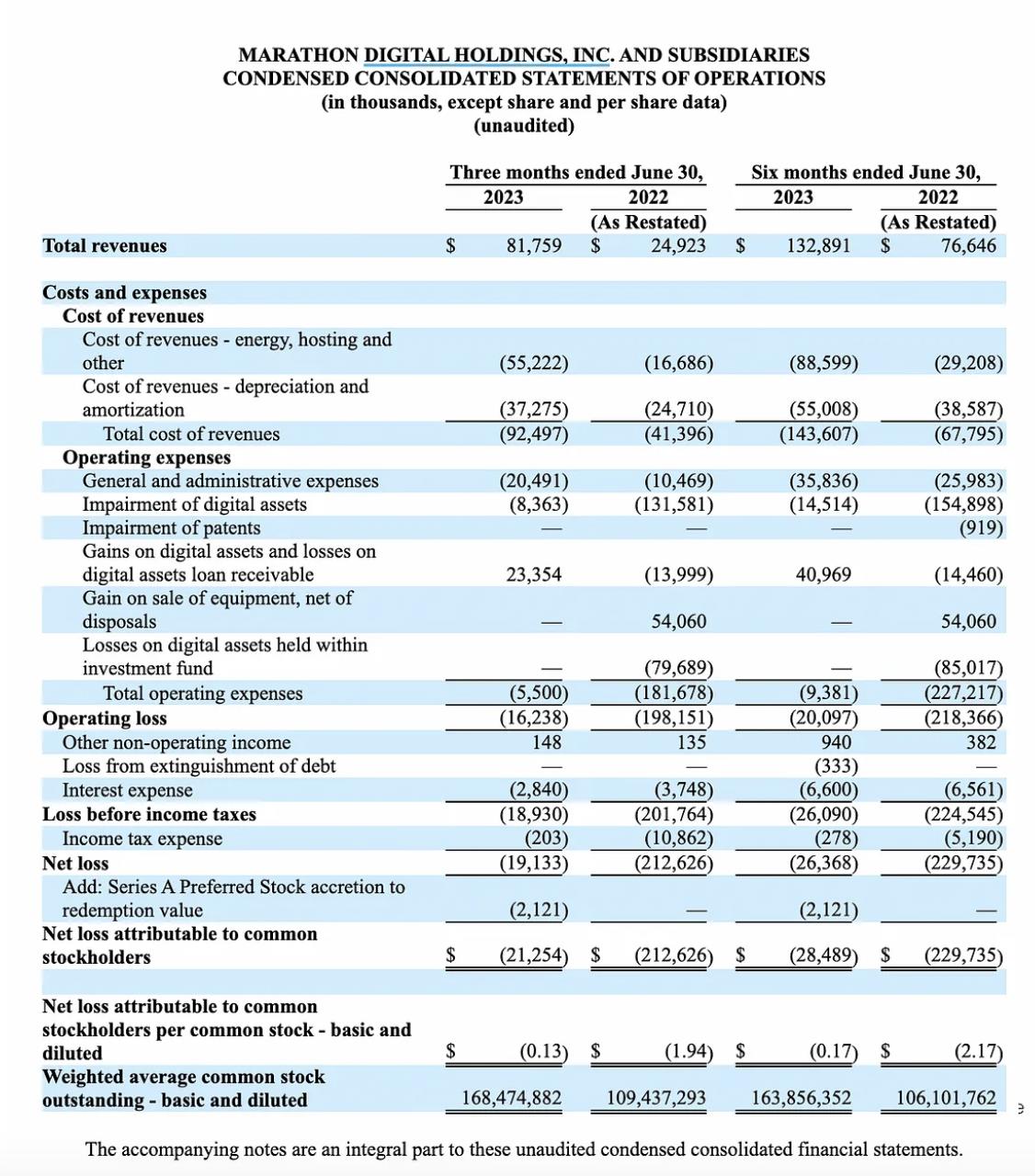

Although increasing hashrate has improved BTC output and revenue, Marathon reported a loss of $21.3 million ($0.13 per share) for the three months ended June 30, 2023, an improvement from a net loss of $212.6 million ($1.94 per share) in the same period last year. However, it remains unprofitable, and significant electricity and facility deployment costs continue to erode Marathon’s balance sheet under tight cash flow conditions.

2. Cash Flow and Cash Burn

From Marathon’s cash flow statement, we see that all cash inflows come from financing activities. In Q4 2022, operating cash flow was -$92 million, investing cash flow was -$22 million, and financing cash flow was $163 million, leaving a net cash inflow of $48 million to cover taxes and interest in the following quarter. This financing cash flow came entirely from issuing new common stock. Continuous equity issuance may lower market valuation, leading to higher future capital costs. Additionally, issuing more shares could dilute EPS as profits are spread across more shareholders, negatively impacting Marathon’s valuation.

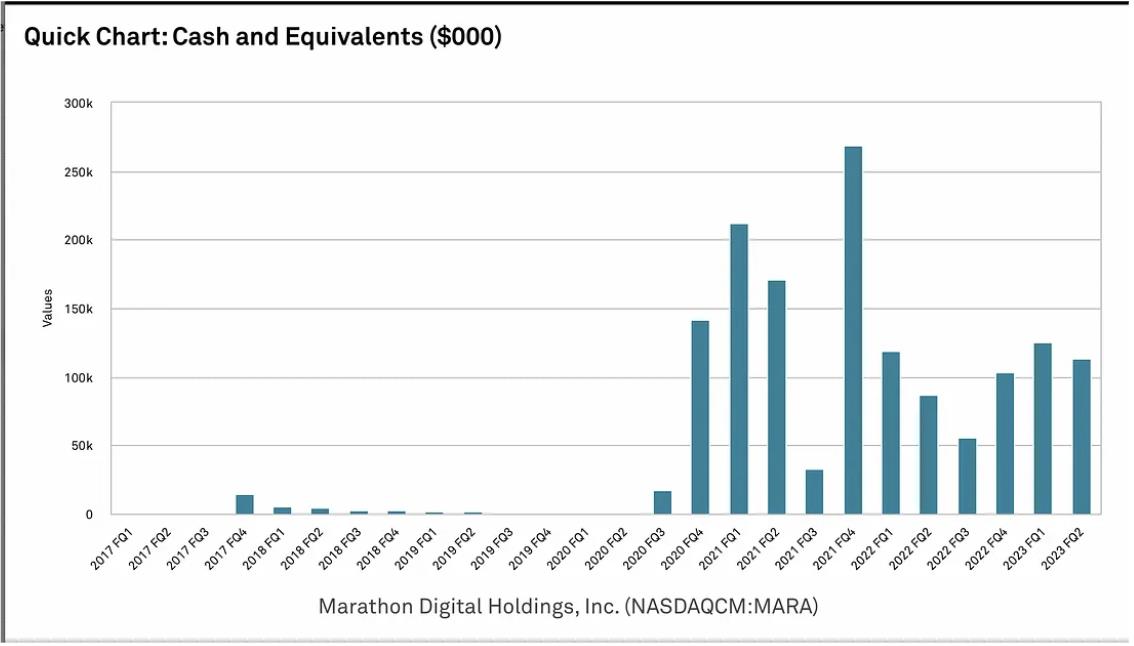

As of the end of Q2 2023, Marathon held $113 million in cash and cash equivalents, including 12,538 BTC. In 2023 Q2, Marathon paid $3 million in interest—nearly equal to its available net cash ($3 million, even after raising $163 million and $65 million through share issuances in Q1 and Q2 respectively). This indicates excessive use of cash in operations and investments without sufficient new inflows. Consequently, apart from actively repaying debt to reduce interest burdens, Marathon must also sell BTC to fund operations. Indeed, in Q2 2023, Marathon sold 63% of its mined BTC, totaling $23.4 million.

3. Bull Market Expansion Fuels Bear Market Concerns – Acquisitions and Mine Deployment

In early August, Marathon installed new S19 miners, achieving its domestic installed hashrate target of 23 EH/s. The newly installed site in Garden City, Texas, is nearing activation according to the hosting provider. Marathon’s joint venture in Abu Dhabi has begun contributing hashrate and producing Bitcoin. However, at an electricity cost of $0.12/kWh, current deployments would merely break even—or even incur slight losses—based solely on variable electricity costs given today’s BTC price.

Moreover, overall mine construction investment costs remain high. In 2021, valuations for acquired mining sites reached up to $1 million/MW, with miner unit prices ranging between $55–105 USD/T. Under falling cryptocurrency prices and rising electricity costs, earlier asset investments have depreciated significantly, while revenues have clearly declined, making it difficult for many mining companies to sustain operations.

Marathon plans to continue expanding its leadership in Bitcoin mining over the coming quarters. However, such expansion raises further concerns about its cash flow sustainability during a bear market—the ability to keep raising funds will determine whether its expansion plan can proceed smoothly (though equity dilution reduces per-share value).

4. Marathon’s Debt and Current Operations

Market downturns negatively affect heavily indebted companies, especially in a high-interest-rate environment. Marathon’s liabilities impose additional interest burdens on its cash flow. To address low coin prices and anticipated operational pressures from the upcoming BTC halving next year, Marathon chose to prepay most of its convertible notes (approximately $417 million in convertible notes were exchanged at around a 21% discount, saving Marathon about $101 million in cash, excluding transaction costs. This transaction added approximately $0.55 per share in value for existing shareholders), enhancing its financial and funding flexibility. With reduced debt burden, the company is better positioned to withstand short-term turbulence.

During bear markets, falling coin prices, outstanding miner orders, capital expenditures on mines, and debt place immense pressure on company operations. Beyond this, intense competition among miners and rising energy prices further exacerbate survival challenges. Despite selling 63% of its Q2 production, Marathon’s CEO indicated during the Q2 earnings call that the company would continue selling BTC to maintain operations.

5. Miners’ Current Bear Market Situation

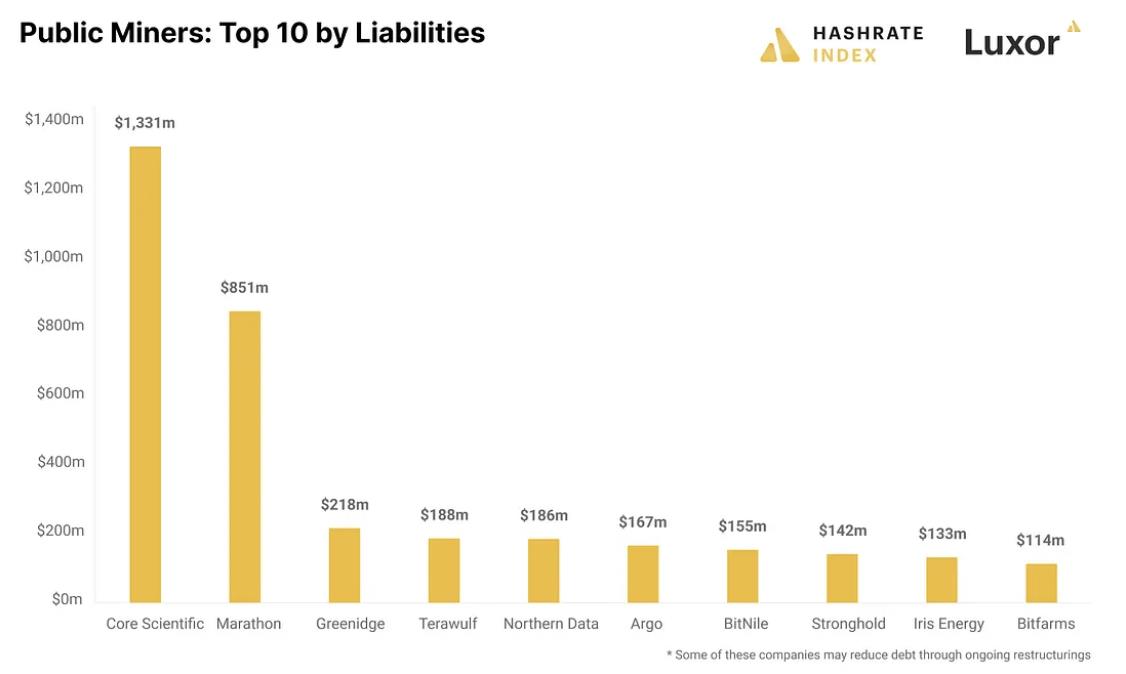

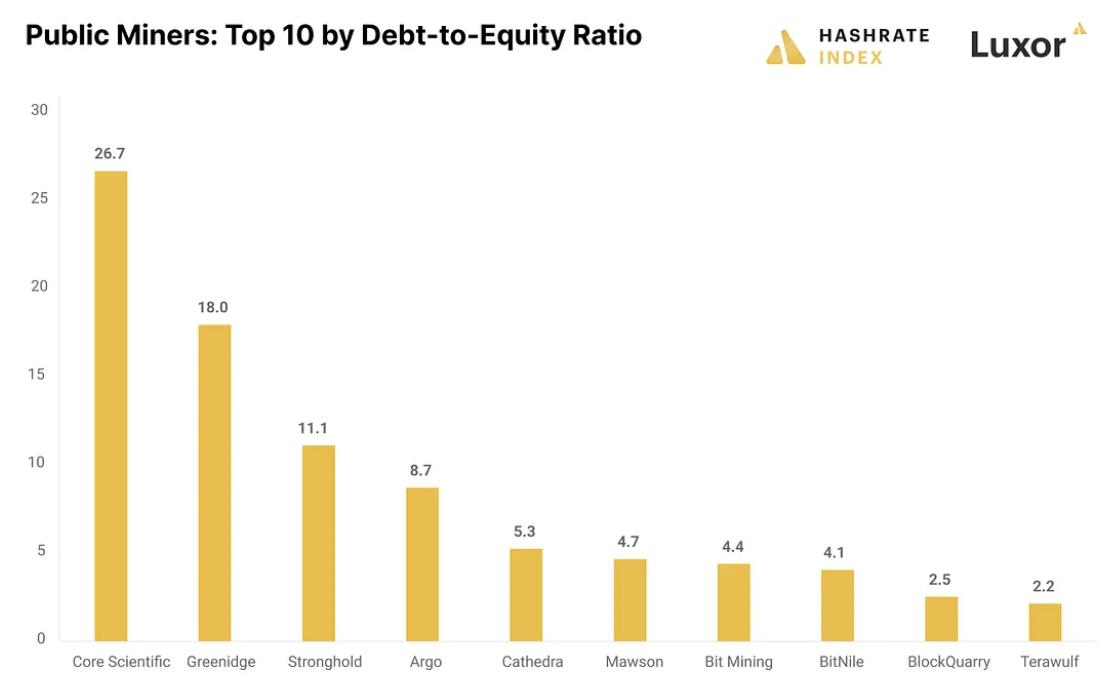

Mining stocks face severe challenges in bear markets. Their strong correlation with BTC and high elasticity lead to greater downside pressure on prices. Due to leveraged operations and single-source revenue streams, mining companies face bankruptcy risks. Many Bitcoin mining firms took on substantial loans during the 2021 bull market, severely affecting profitability during the subsequent bear market. In fact, Core Scientific, the most indebted mining company with the highest debt-to-asset ratio, sought bankruptcy protection and debt restructuring at the end of 2022. Throughout 2022, Core Scientific had been selling BTC to cover costs related to miner purchases, building proprietary mining farms, massive electricity bills, and loan interest payments—but ultimately collapsed due to its aggressive 2022 expansion plan (deploying over 320,000 miners by year-end, losing $53,000 daily just in electricity) and the Celsius incident.

Bitcoin price and network difficulty show a clear divergence. During bull markets, rising future computing power incentivizes miners and supports fundraising narratives. But in bear markets, falling Bitcoin prices make miners’ economic conditions extremely challenging, as they must fulfill prior miner purchase commitments even as BTC prices drop sharply while network hashrate continues growing. Since miners have already paid for capital expenditures, continuing expansion makes sense as long as marginal mining costs remain positive. This trend has further driven down hashprice significantly since the beginning of this year.

With the sharp decline in Bitcoin prices, most mining stocks have seen severe valuation drops. Some mining companies are raising capital by selling BTC and issuing common stock—significantly diluting existing shareholders’ equity. Raising equity is highly dilutive, and debt financing is expensive. Under tight liquidity, miners are exploring alternative solutions such as offering hosting services for higher income, selling equipment for immediate cash, or considering mergers and acquisitions. Those who were conservative and avoided excessive leverage during the bull market now have opportunities to act opportunistically—miners with sound cash flow management may acquire distressed competitors at bargain prices.

Given Marathon’s poor debt-to-capital ratio (increasing probability of bankruptcy), its correlation with upward BTC moves may weaken. If recent debt management allows Marathon’s balance sheet to survive until the next BTC bull market, given current macro trends (continued downtrend), Marathon’s debt situation (excessively high debt-to-equity), and valuation (P/B still has significant downside room, MC/hashrate above peers), the investment recommendation is a strong sell over the next 12 months, targeting a P/B of 1, implying a target price around $3. At the current price of $8, it is overvalued by 166%. However, due to its highest price elasticity, traders can capture short-term rebounds for higher returns than holding BTC directly. Two scenarios could drive share price increases: acquisition activity or a short-term BTC rebound within the bear market.

II. Company Background and Business Overview

Marathon Digital Holdings, Inc. and its subsidiaries ("Company" or "Marathon") is a digital asset technology company focused on the blockchain ecosystem and the generation, or "mining," of digital assets.

-

The company was incorporated on February 23, 2010, in Nevada under the name Verve Ventures, Inc.

-

In October 2012, the company began intellectual property licensing operations and changed its name to Marathon Patent Group, Inc.

-

In 2017, the company purchased digital asset mining equipment and established a data center in Canada for mining digital assets.

-

However, the company ceased operations in Canada in 2020 and consolidated all operations into the United States at that time.Since then, the company has expanded its Bitcoin mining activities in the U.S. and internationally.

-

On March 1, 2021, the company changed its name to Marathon Digital Holdings, Inc.

-

As of June 30, 2023, the company’s main business focuses on Bitcoin mining and ancillary opportunities within the Bitcoin ecosystem.Its strategy is to hold Bitcoin after covering cash operating costs, treating it as a long-term investment. Holding Bitcoin represents a store-of-value strategy supported by a robust, open-source architecture not tied to any national monetary policy, thus serving as a value repository outside government control.

Marathon believes that due to Bitcoin’s limited supply and increasing adoption, it offers additional appreciation potential. The company may also explore participation in other businesses related to Bitcoin mining when favorable market conditions and opportunities arise.

Ancillary businesses refer to those related to the Bitcoin ecosystem but not directly tied to its own mining operations. Ancillary activities directly linked to mining may include, but are not limited to, managing Bitcoin mining facilities owned by third parties, providing advisory and consulting services to third parties seeking to build and operate mining facilities, and engaging in joint ventures for Bitcoin mining projects in jurisdictions including the U.S. and international regions such as the company’s project in Abu Dhabi (UAE).

Marathon also seeks to participate in Bitcoin-related projects, including but not limited to immersion technologies, hardware, firmware, mining pools, and development of sidechains using blockchain cryptographic techniques. It may also engage in power generation projects utilizing renewable resources or methane gas capture for use in Bitcoin mining operations.

Development Timeline

-

February 23, 2010: Incorporated in Nevada as Verve Ventures, Inc.;

-

December 7, 2011: Renamed American Strategic Minerals Corporation, engaged in uranium and vanadium mineral exploration and potential development;

-

June 2012: Ceased mining operations and began investing in real estate in Southern California;

-

October 2012: Renamed Marathon Patent Group, Inc., launching IP licensing business;

-

November 1, 2017: Entered into a merger agreement with Global Bit Ventures, Inc. (“GBV”), focusing on blockchain mining; this marked a turning point where Marathon Digital transitioned from near-bankruptcy to becoming a top-tier mining firm. Through acquiring GBV, Marathon obtained 1,300 Bitmain S9 miners and 1,000 GPU miners owned by GBV. After gaining familiarity with operations, Marathon purchased another 1,400 S9s and rented a 2 MW site for mining. Shortly afterward, the crypto market entered a bear phase, and Marathon terminated its partnership with GBV.

-

September 30, 2019 – December 23, 2020: Acquired blockchain mining equipment via contracts;

-

March 1, 2021: Company renamed Marathon Digital Holdings, Inc.

Key Events in 2022

Major developments in the crypto market made 2022 a challenging year for the entire industry. Macroeconomic conditions—including high inflation and rising interest rates compared to recent years—weakened equities and created widespread risk-off sentiment, negatively impacting Bitcoin prices.

Additionally, the macro environment in 2022 faced a series of unexpected black swan events that shook the entire industry:

-

Second Quarter 2022: $LUNA-UST depegging and collapse led to bankruptcies of key players in the digital asset space, including Three Arrows Capital, Voyager, and Celsius;

-

Fourth Quarter 2022: FTX’s collapse triggered additional credit-related bankruptcies and significant declines in both Bitcoin price and Bitcoin mining equipment values. These black swan events affected Marathon’s operating performance, including impairment of prepayments.

Impairment of Bitcoin Mining Equipment and Prepayments to Suppliers: In Q4 2022, the fair value of Bitcoin mining equipment declined significantly. As a result, the company assessed whether impairments were needed for Bitcoin mining equipment (held as fixed assets) and prepayments to suppliers (classified as current assets representing deposits for future delivery of mining equipment). Marathon recorded impairments on both, totaling approximately $332.9 million.

Digital Assets — Impairment and Decline in Book Value: Marathon incurred $173.2 million in impairments, $85.0 million in realized and unrealized losses on digital assets within investment funds, and $14.5 million in unrealized losses on digital assets held on the consolidated balance sheet during 2022.

Total Profit Decline: Due to falling Bitcoin prices and delays in business expansion, Marathon’s operational profitability declined. Total profit for the year was a loss of $33.7 million, compared to a gain of $116.8 million in the prior year—a decrease of $150.4 million.

Direct Impact of Supplier Bankruptcy Filings: On September 22, 2022, Compute North filed for Chapter 11 reorganization under the U.S. Bankruptcy Code. As a result, the company recorded a $39 million impairment charge in Q3 2022. In Q4 2022, the company estimated an additional $16.7 million in deposits might be impaired, recording a further impairment.

Digital Assets Used as Collateral — Fair Value Decline and Additional Collateral Requirements: On November 9, 2022, amid fears of FTX collapse causing financial instability in the industry, Bitcoin prices fell to a new annual low. Consequently, the company was required to post an additional 1,669 Bitcoins (valued at $16,213 each) as collateral for outstanding borrowings under its Term Loan and Revolving Line of Credit (RLOC) facility with Silvergate Bank, bringing total collateral to 9,490 Bitcoins (fair value of ~$153.9 million). As of November 9, 2022, the company held 11,440 Bitcoins, of which 1,950 (~$31.6 million) were unrestricted. In November and December 2022, the company repaid $50 million of RLOC borrowings, allowing it to reduce the number of Bitcoins used as collateral to approximately 4,416 Bitcoins (fair value ~$73.1 million) by December 31, 2022.

Impact of Bankruptcies and FTX Collapse on Marathon’s Key Lenders: Prior to termination on March 8, 2023, Silvergate Bank served as lender for Marathon’s Term Loan and RLOC facilities, under which Marathon could borrow up to $200 million, provided sufficient Bitcoin collateral.

- March 1, 2023: Silvergate Bank filed disclosures with the SEC regarding its troubled financial condition, including doubts about its ability to continue as a going concern, and notified of delayed filing of its Form 10-K due to significant customer deposit outflows and capital inadequacy. This caused crypto clients to abandon the bank, creating both a credit gap and reputational risk for crypto customers.

- March 8, 2023: Silvergate announced its intention to cease operations and voluntarily liquidate the bank.

- February 6, 2023: Marathon provided Silvergate Bank with a 30-day notice stating its intent to repay the outstanding balance of its Term Loan facility and terminate the Term Loan agreement. Marathon and Silvergate later agreed to terminate the RLOC facility.

- March 8, 2023: The company repaid the Term Loan and terminated the RLOC facility with Silvergate Bank.

Closure of Signature Bank: On March 12, 2023, Signature Bank was closed by its state chartering authority, the New York State Department of Financial Services. On the same day, the FDIC was appointed receiver and transferred all deposits and nearly all assets of Signature Bank to Signature Bridge Bank, a full-service bank operated by the FDIC. The company automatically became a customer of Signature Bridge Bank. As of March 12, 2023, the company held approximately $142 million in cash deposits at Signature Bridge Bank. Normal banking operations resumed on March 13, 2023.

Key Events in 2023

On January 27, 2023, the company signed a shareholder agreement with FS Innovation, LLC (“FSI”) to establish a company in the Abu Dhabi Global Market (“ADGM Entity”), aiming jointly to (a) establish and operate one or more digital asset mining facilities; and (b) mine digital assets (collectively referred to as the “business”).

The ADGM Entity’s initial project will include two 250-megawatt digital asset mining sites in Abu Dhabi. Initial equity ownership will be 80% for FSI and 20% for Marathon, with capital contributions in cash and kind totaling approximately $4.06 million during the 2023 development phase.

FSI will appoint four directors to the ADGM Entity’s board, while the company will appoint one. Unless otherwise required by law, digital assets mined by the ADGM Entity will be distributed monthly to the company and FSI according to their respective equity stakes.

The agreement includes standard market provisions on financial and tax matters. It may be terminated early upon mutual written consent, liquidation of the ADGM Entity, or if shareholders hold all outstanding equity interests of the ADGM Entity. The agreement includes market-standard terms regarding share transfers, rights of first refusal, tag-along and drag-along rights upon sale of the ADGM Entity.

Additionally, the agreement includes a five-year restrictive covenant prohibiting Marathon from competing with the business or FSI or certain related parties in the UAE, and prohibiting FSI from competing with Marathon’s business in the U.S.

On September 20, 2023, Marathon completed the previously announced privately negotiated exchange agreement for its 1.00% convertible senior notes due 2026. On average, these transactions were discounted approximately 21% from par value, saving the company about $101 million in cash before transaction costs.

Marathon converted a total of $417 million in principal amount of notes held by investors into 31.7 million newly issued shares of Marathon common stock. As a result, the company reduced its long-term convertible debt by approximately 56% and saved about $101 million in cash before transaction costs. The remaining principal amount of the notes totals $331 million.

III. Financial Analysis

1. Revenue Growth

Marathon’s business model, based on BTC appreciation and improved mining efficiency, led to negative revenue growth after the crypto market entered a bear phase post-2021.

In 2022, Marathon’s operating revenue was $117.8 million, down from $159.2 million in 2021. The $41.4 million decrease was primarily due to a $77.3 million revenue reduction caused by lower Bitcoin prices in 2022, partially offset by a $44.6 million increase from higher annual production.

In 2022, revenue also declined by $8.7 million due to the company ceasing operations of third-party mining pools. Despite overall annual production increases, the company experienced significant production stagnation in Q2 and Q3 due to delays exiting Hardin and King Mountain electrification projects. Third-quarter production dropped 50% year-over-year. Marathon’s best production quarters in 2022 were Q1 and Q4.

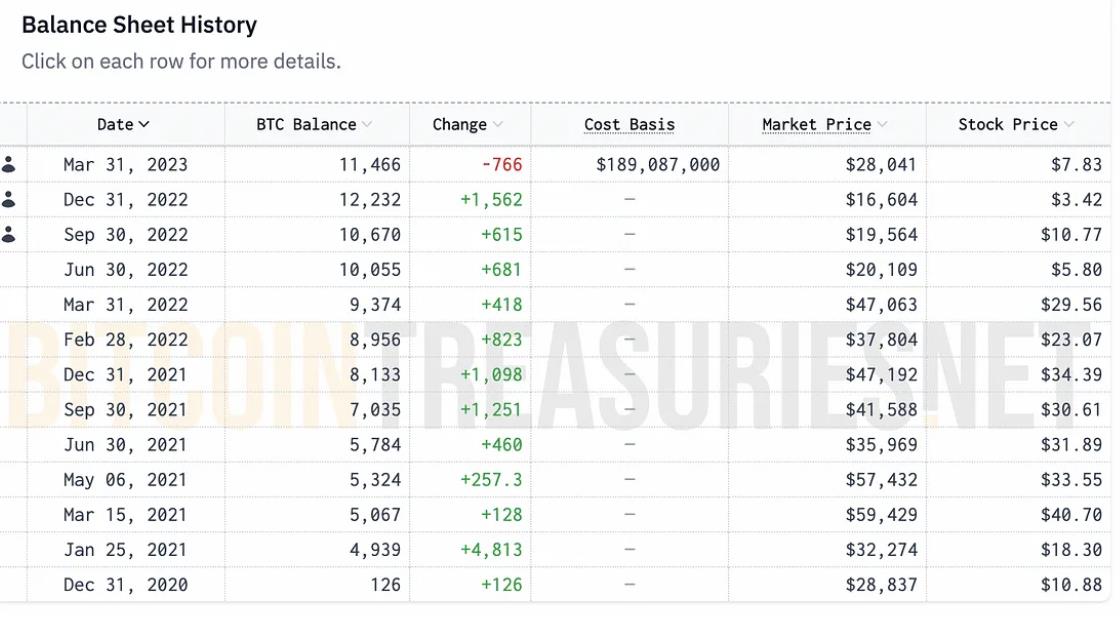

As of December 31, 2022, the company held approximately 12,232 BTC on its balance sheet, with a carrying value of $190.7 million. Of this, about 4,416 BTC ($68.9 million book value) were pledged as collateral for loans and classified as restricted digital assets. The remaining 7,816 BTC, with a book value of $121.8 million, were unrestricted holdings classified as digital assets.

In Q1 2023, Marathon’s BTC balance decreased for the first time by 766 BTC to address deteriorating balance sheet conditions.

In Q2 2023, a 314% increase in Bitcoin production significantly offset a 14% decline in average Bitcoin price year-over-year, resulting in sequential revenue of $81.8 million—far exceeding $24.9 million in Q2 2022. However, operational conditions remain concerning: Marathon sold 63% of its quarterly BTC output (1,843 BTC). For the three months ended June 30, 2023, it recorded a $21.3 million loss, or $0.13 per share, compared to a net loss of $212.6 million and $1.94 per share in the same period last year.

Bitcoin sales generated $23.4 million in proceeds, as the company sold 63% of its quarterly production to cover operating costs. Additionally, due to generally rising Bitcoin prices during the period, impairment of digital assets decreased by $8.4 million. Furthermore, the absence of a $79 million loss from digital asset investment funds and a $54 million gain from equipment sales compared to the prior year also contributed positively to year-over-year comparisons.

Adjusted EBITDA was $25.6 million, compared to a loss of $167.1 million in the same period last year. In addition to the aforementioned gains and lower impairments, gross margin excluding depreciation and amortization rose to $26.5 million, up from $8.2 million in the prior year.

Q2 2023 Production Highlights

Bitcoin production: Q2–23: 2,926 BTC, Q2–22: 707 BTC, +314%; Q2–23: 2,926 BTC, Q1–23: 2,195 BTC, +33%.

Daily average Bitcoin production: Q2–23: 32.2 BTC, Q2–22: 7.8 BTC, +314%; Q2–23: 32.2 BTC, Q1–23: 24.4 BTC, +32%.

Operational/activated hashrate (EH/s): Q2–23: 17.7 EH/s, Q2–22: 0.7 EH/s, +2,429%; Q2–23: 17.7 EH/s, Q1–23: 11.5 EH/s, +54%.

Average operational hashrate (EH/s): Q2–23: 12.1 EH/s, not applicable YoY; Q2–23: 12.1 EH/s, Q1–23: 6.9 EH/s, +75%.

Installed hashrate (EH/s): Q2–23: 21.8 EH/s, not applicable YoY; Q2–23: 21.8 EH/s, Q1–23: 15.4 EH/s, +42%.

Although commissioning of mining equipment has greatly improved mining efficiency compared to the prior year, BTC prices remain low and aggressive expansion has led to excessively high operating expenses, leaving Marathon on precarious ground.

2. Profit and Cost Breakdown

Marathon’s total profit in FY2022 was -$33.7 million, compared to $117 million in the prior year—a decline of $150 million.

Marathon’s cost of revenue in FY2022, including energy, hosting, and other costs, totaled $72.7 million, up from $27.5 million in the prior year. The $45.2 million increase was mainly due to higher production costs—$30 million from increased per-BTC mining costs, $18.2 million from accelerated costs due to early exit from Hardin, and $5.6 million from higher Bitcoin output.

Partially offsetting these increased costs was an $8.7 million decrease in cost of revenue from discontinued third-party mining pools. Depreciation and amortization expenses were $78.7 million in 2022, up from $14.9 million in the prior year—an increase of $63.8 million. This was primarily due to accelerated depreciation of $36.0 million related to Marathon’s exit from Hardin and MT facilities, plus $27.8 million from more mining equipment in operation.

In FY2022, Marathon recorded a net loss of $687 million, compared to a net loss of $37.1 million in the prior year—a $649 million deterioration, primarily due to a $318 million write-down in the book value of its digital assets and $333 million in combined impairments of Bitcoin mining equipment and prepayments to suppliers.

Adjusted EBITDA was -$534 million, compared to $162 million in the prior year. Factors included $86.6 million in depreciation and amortization, $26.1 million in legal reserves, and $18.6 million increase in G&A expenses excluding non-cash stock compensation. Partially offsetting these negatives were $83.9 million in gains from equipment sales and $1.6 million in non-operating income.

In Q2 2023, Marathon recorded a net loss of $19.1 million, compared to a net loss of $212.6 million in the same period last year. This ~91% improvement in net loss was primarily due to gains from digital asset sales and favorable differences in digital asset impairments and losses from digital assets within investment funds, partially offset by lower gross margins.

Marathon’s adjusted EBITDA in Q2 2023 was $25.6 million, compared to -$167 million in the prior year. The increase was primarily driven by positive impacts from digital asset sales ($23.4 million) and reduced digital asset impairments ($12.3 million). Adjusted EBITDA also benefited from the absence of several charges recorded in the prior year, including losses on digital assets within investment funds, gains from digital asset sales, and losses on accounts receivable from digital asset loans. These favorable differences partially offset lower gross margins (excluding depreciation and amortization) and higher G&A expenses excluding stock-based compensation.

Re-analyzing the impact of Marathon’s miner deployment on costs and profits. Currently, all miners are hosted by third parties, to whom Marathon pays fees.

McCamey, TX — Approximately 63,000 S19j Pros currently deployed and operating, with an additional 4,000 S19j Pros scheduled for delivery and deployment in 2023. Marathon’s contract for this facility expires in August 2027.

Garden City, TX — Approximately 28,000 S19 XPs currently installed, awaiting final regulatory approval for power-up. Marathon’s current expansion plan includes deploying 19 MW of immersion equipment in 2023, using new capacity and replacing air-cooled units with immersion systems. The contract for this facility expires in July 2027.

Ellendale, ND — Expected to deploy approximately 57,000 S19 XPs at this location in H1 2023. Power-up expected to begin by end of Q1 2023. Contract for this site expires in July 2027.

Jamestown, ND — Approximately 5,600 S19 XPs currently deployed and operating, with plans to deploy an additional 10,400 air-cooled units in Q1 2023. In addition to installing these air-cooled units, the company plans to deploy 768 immersion units at this site in Q2 2023. Contracts for immersion deployment expire in August 2026, and for air-cooled units in December 2027.

Granbury, TX — Approximately 12,500 S19j Pros and 4,400 XPs currently deployed and powered at this facility. No plans to expand this facility.

Coshocton, OH — Approximately 2,800 S19 Pros currently deployed and operating at this facility. Marathon’s contract for this facility expired in June 2023, and the company does not intend to renew beyond that date.

Plano, TX — Approximately 345 S19 Pros currently deployed and operating at this facility. No plans to expand this facility. Contract for this facility expires in June 2027.

Kearney, NE — Approximately 2,300 S19 J Pros currently deployed and operating at this location. The company plans to deploy an additional 1,300 MicroBT units at this location in 2023.

South Sioux City, SD — Approximately 660 S19 Pros currently deployed at this location. The company’s contract for this facility expired in early 2023, and it has exited the facility. On January 27, 2023, Marathon and FSI signed an agreement to form an Abu Dhabi Global Market entity to jointly (a) establish and operate one or more digital asset mining facilities; and (b) mine digital assets. The ADGM entity’s first project will include two 250 MW immersion-based mining stations in Abu Dhabi, with initial equity split 80% FSI and 20% Marathon. The facility is expected to go online in H2 2023.

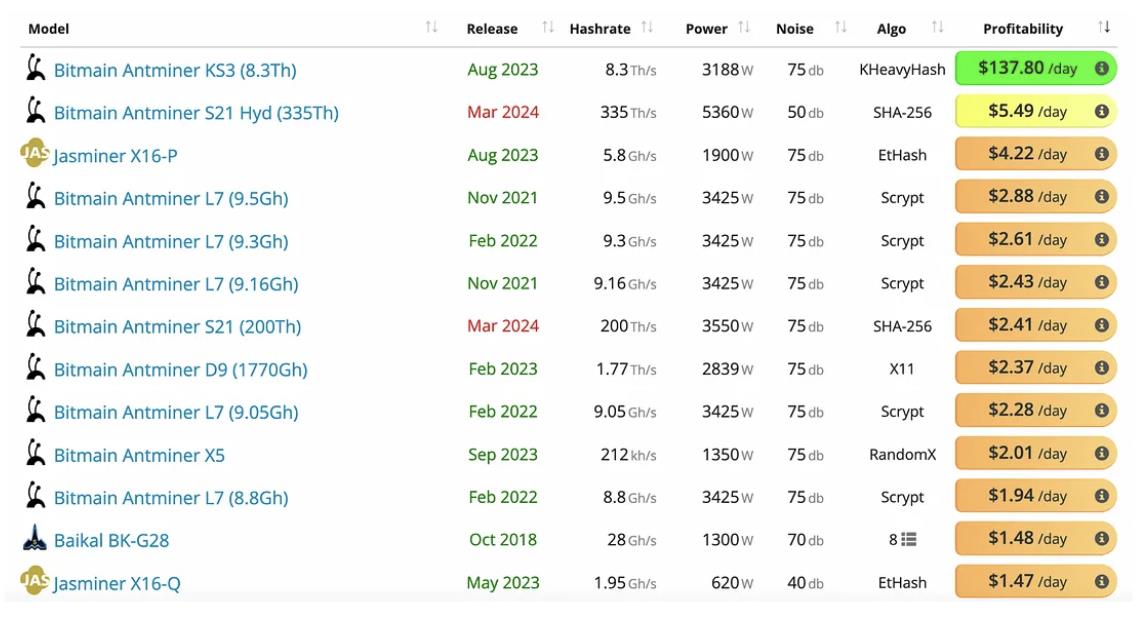

Most of Marathon’s Q1 2023 deployments consisted of S19 XPs. Based on current miner profitability, S19 XPs generate minimal profit—just $0.08 per unit per day. Therefore, increased hashrate may not fundamentally improve Marathon’s profitability this year.

Miner profit = Bitcoin reward × BTC price − Electricity cost − Hashrate cost; therefore, Bitcoin market price, electricity cost, and hashrate cost are critical to Marathon’s profitability.

· Bitcoin Reward

Bitcoin rewards are significantly impacted by halving events. Bitcoin halving occurs roughly every four years as part of the Bitcoin protocol, designed to control total supply and reduce inflation risks associated with Proof-of-Work consensus. At predetermined block heights, mining rewards are halved—hence the term “halving.” For Bitcoin, the initial block reward was set at 50 BTC. Since inception, the Bitcoin blockchain has undergone three halvings:

(1) November 28, 2012, at block height 210,000;

(2) July 9, 2016, at block height 420,000;

(3) May 11, 2020, at block height 630,000, reducing the reward to the current 6.25 BTC per block.

The next Bitcoin halving is expected around March 2024, near block height 840,000. This process will repeat until the total issuance reaches 21 million BTC, theoretically exhausting new supply around the year 2140. The 2024 Bitcoin halving will cut mining rewards, threatening the profitability of marginally profitable miners. Only a significant rise in BTC price can lead to meaningful profitability improvements.

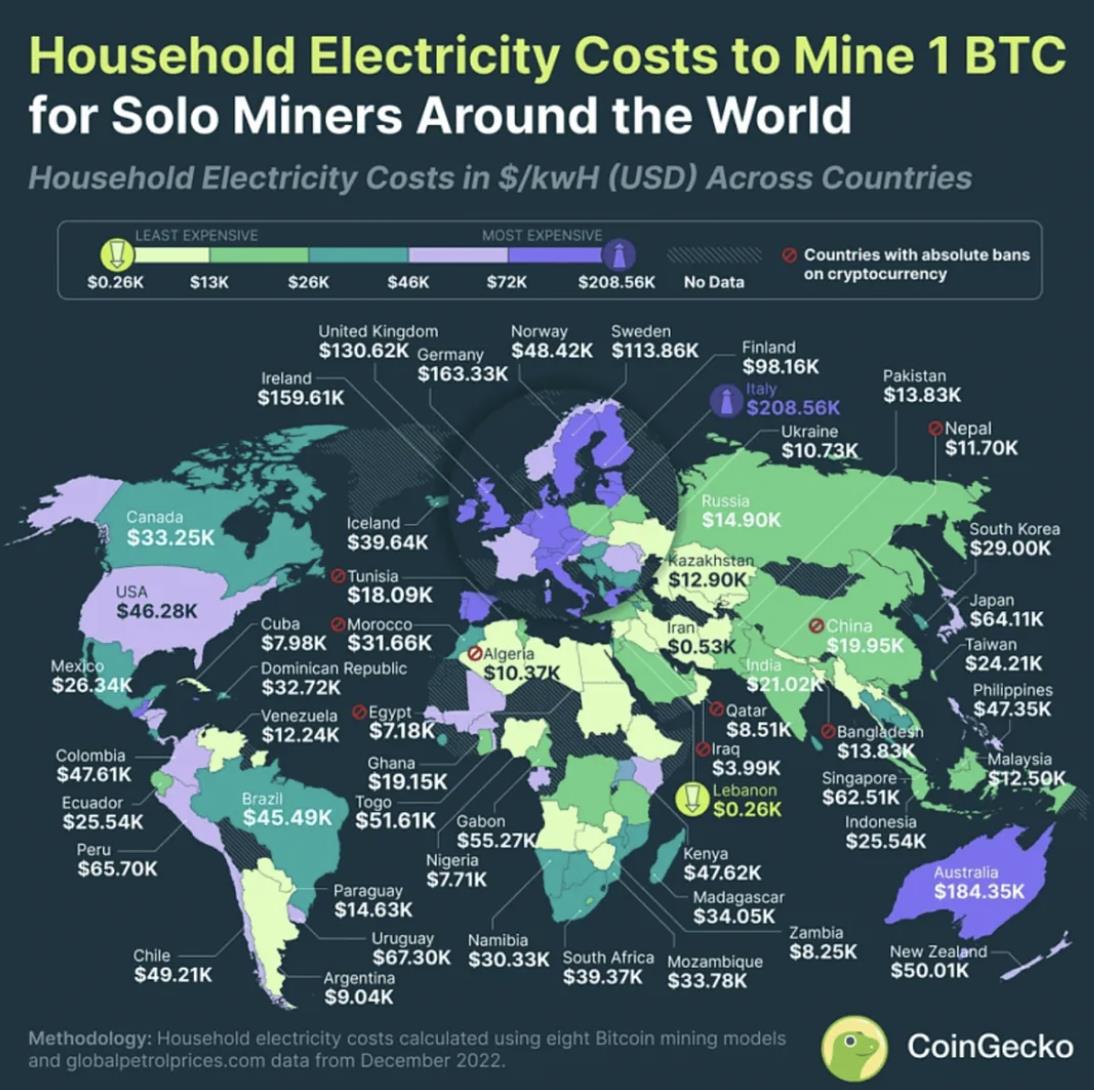

· Electricity Cost

Electricity costs vary widely across countries. European nations face the highest costs due to rising electricity prices. While U.S. miners are less affected than Europeans, energy price hikes still intensify cost pressures. Texas electricity prices at $0.12/kWh are 34% below the U.S. average of $0.18/kWh. Even so, most miner models struggle to breakeven at current electricity and coin prices (without subsidies; some mines may still profit with subsidy advantages).

· Network Hashrate and Difficulty

Generally, a Bitcoin mining device’s chance of solving a block and earning a Bitcoin reward depends on its hashrate relative to the global network hashrate (i.e., the total computational power supporting the Bitcoin blockchain at a given time).

As demand for Bitcoin grows, the global network hashrate increases rapidly. Moreover, as more powerful mining devices are deployed, Bitcoin’s network difficulty rises. Network difficulty measures how hard it is to solve a block on the Bitcoin blockchain and adjusts every 2,016 blocks (approximately every two weeks) to maintain an average block interval of about ten minutes.

Higher difficulty means more computational power is required to solve blocks and earn new Bitcoin rewards, enhancing Bitcoin network security and limiting the possibility of a single miner or pool controlling the network.

Thus, as new and existing miners deploy additional hashrate, the global network hashrate will continue rising. This means that if a miner fails to deploy additional hashrate at pace with the industry, its share of global network hashrate—and hence its chances of earning Bitcoin rewards—will decline. Due to intense miner competition, revenue per TH dropped from $0.25/TH in early 2022 to around $0.06/TH today.

Join TechFlow official community to stay tuned Telegram:https://t.me/TechFlowDaily X (Twitter):https://x.com/TechFlowPost X (Twitter) EN:https://x.com/BlockFlow_News