Bitget UEX Daily Report | Circle Completes $222M ARC Presale; U.S. CPI Data Released; U.S.-Iran Ceasefire Agreement on Shaky Ground

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Circle Completes $222M ARC Presale; U.S. CPI Data Released; U.S.-Iran Ceasefire Agreement on Shaky Ground

Overall, the market is seeking balance between inflation data and geopolitical events, and the technology and commodities sectors may continue to diverge.

I. Top News

Federal Reserve Updates

U.S. April CPI data released today; Morgan Stanley warns of “more explosive” figures

- This week marks the U.S. “Inflation Week,” with the April CPI, PPI, and import price data all scheduled for release. Morgan Stanley’s Global Macro Strategy Head forecasts that today’s CPI month-on-month figure may exceed expectations, with particular focus on its implications for the PCE inflation trajectory.

- Markets broadly anticipate a 0.6% month-on-month rise in headline CPI and a 0.3% increase in core CPI, driven primarily by energy and rent factors. This data will directly test market expectations for Fed rate cuts; a higher-than-expected print could delay easing plans, delivering near-term headwinds to risk assets while strengthening the U.S. dollar.

Global Commodities

Trump calls Iran’s response “foolish”; U.S.-Iran ceasefire agreement hangs in the balance

- Trump reiterated that Iran must not acquire nuclear weapons and hinted at potentially expanding the Strait of Hormuz “freedom of navigation” initiative. Iran stated its “14-point proposal” remains non-negotiable and that passage through the strait remains restricted.

- Aramco warned that sustained closure of the Strait could reduce global oil supply by approximately 100 million barrels per week. Geopolitical tensions have directly pushed up oil prices, providing short-term support to energy stocks but intensifying global inflationary pressures—gold, silver, and other safe-haven assets rose concurrently.

II. Market Recap

Commodities & FX Performance

- Spot Gold: +0.38%, at $4,753/oz.

- Spot Silver: +0.19%, at $86/oz.

- WTI Crude Oil: +0.51%, at $98/barrel.

- Brent Crude Oil: +0.49%, at $104/barrel.

- U.S. Dollar Index: Slightly fluctuating near 98.063.

Cryptocurrency Performance

- BTC: +0.1%, currently trading around $81,549.

- ETH: -0.74%, currently trading around $2,330.

- Total Cryptocurrency Market Cap: +0.2%, at approximately $2.81 trillion.

- Liquidations: ~$221 million liquidated in the past 24 hours, including $112 million in long positions.

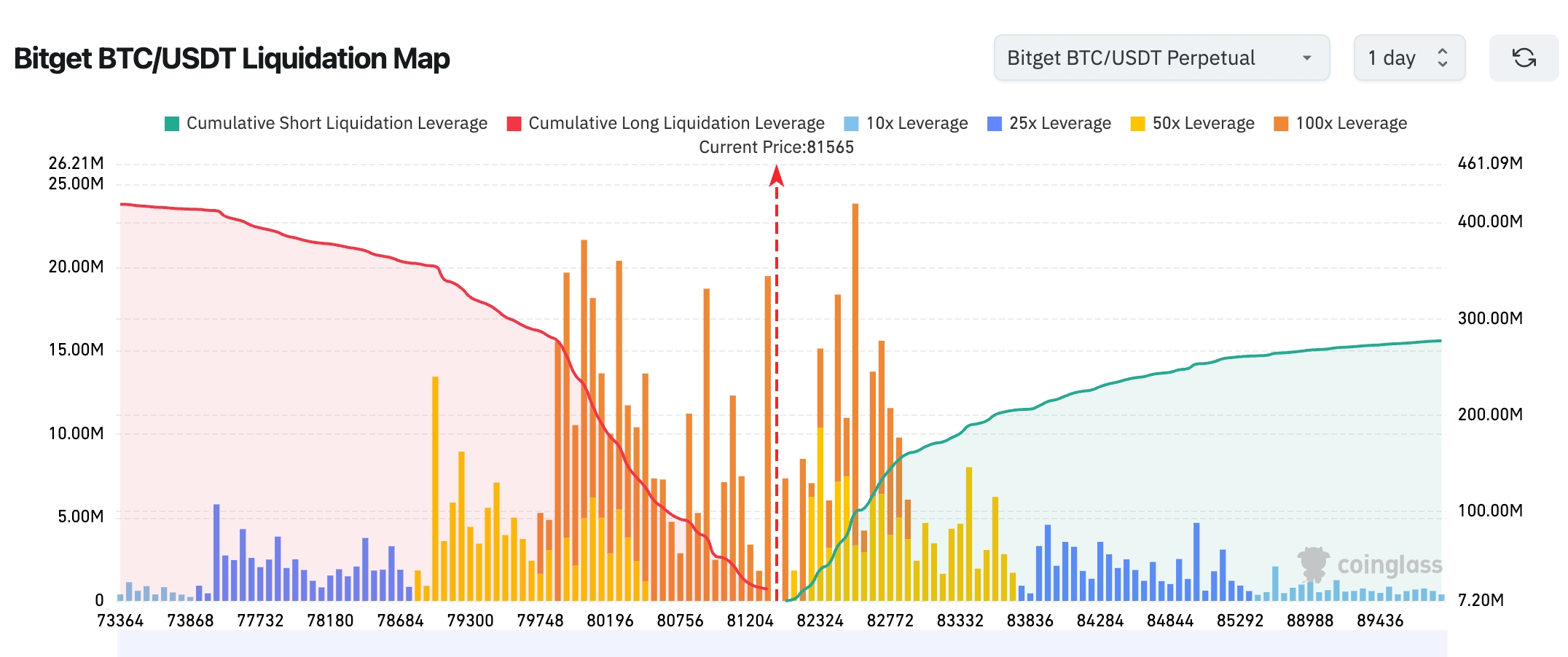

- Bitget BTC/USDT Liquidation Heatmap: BTC is currently trading near $81,565. A large cluster of high-leverage short positions faces liquidation pressure above the $82,200–$83,000 range; a further upside move may trigger cascading short liquidations. Conversely, a denser concentration of long-position liquidations exists between $80,000–$81,000; a break below this zone could spark long-position capitulation and amplify downside volatility.

- Spot ETF Net Flows: BTC spot ETFs recorded modest net inflows of ~$34.6 million yesterday; ETH spot ETFs saw modest net outflows of $17.9 million.

- BTC Net Flows: $193 million net outflow from BTC spot markets yesterday; $1.35 billion net outflow from BTC derivatives markets.

U.S. Equity Index Performance

- Dow Jones Industrial Average: +0.02%, closing at 49,609 points, continuing cautious consolidation.

- S&P 500: +0.84%, closing at 7,399 points—a new all-time high.

- Nasdaq Composite: +1.71%, closing at 26,247 points, driven continuously by AI-related sectors.

Tech Giants’ Updates

- Apple (AAPL): +2.05%, at $293.32

- Amazon (AMZN): +0.56%, at $272.68

- Google Class A (GOOGL): +0.71%, at $400.80

- Meta (META): -1.16%, at $610

- Microsoft (MSFT): -1.34%, at $415.12

- NVIDIA (NVDA): +1.75%, at $215.20

- Tesla (TSLA): +4.02%, at $428.35 — Tech giants posted mixed results overall. Tesla was notably boosted by news that Elon Musk would join Trump’s U.S. delegation to China. NVIDIA continued benefiting from robust capital expenditures in AI data centers, while Meta and Microsoft pulled back amid profit-taking and sector rotation.

Sector Highlights

Memory Stocks surged 6–8%

- Key names: Qualcomm (+8%+), Western Digital (+7%+), Micron Technology (+6%+)

- Catalyst: Sustained high capital spending in AI data centers is driving strong memory demand, pushing the sector to a record closing high.

Optical Communications surged 10–26%

- Key names: POET Technologies (+26%+), Applied Optoelectronics (+24%+), Lumentum (+16%+)

- Catalyst: Surging demand for optical modules amid the AI wave; Lumentum received additional tailwinds from its upcoming inclusion in the Nasdaq-100 Index.

III. In-Depth U.S. Equity Analysis

1. Lumentum (LITE.US) – Added to Nasdaq-100 Index

Event Summary: Lumentum’s stock surged 16.52% on Monday, closing at $1,053.09—a new all-time high—after announcing it will be officially added to the Nasdaq-100 Index on May 18, replacing CoStar. Year-to-date gains now stand at 186%; over the past 12 months, shares have soared 1,368%. The company continues to benefit from AI data center buildouts and rapidly rising capex by hyperscale cloud providers. Market Interpretation: Analysts expect passive fund inflows following index inclusion, further amplifying AI supply-chain premium valuations. Investment Takeaway: The AI infrastructure theme retains long-term conviction; investors should monitor valuation expansion potential among similar optical communications names.

2. Circle (CRCL.US) – Strong Q1 Results and USDC Growth

Event Summary: Circle reported Q1 revenue up 20% year-on-year to $694 million, while net income declined 15% YoY to $55 million—primarily due to a 76% surge in stock-based compensation expenses post-IPO. USDC circulation grew 28% YoY to $77 billion, serving as the key growth driver. Circle completed a $222 million presale for its ARC ecosystem and advanced its Agent Stack platform into AI agent payments. Full-year guidance remains unchanged. Market Interpretation: Institutions remain bullish on the long-term growth potential of stablecoin businesses, viewing AI-powered payments as a key new growth vector. Investment Takeaway: USDC ecosystem expansion provides reliable underpinning for crypto infrastructure; consider long-term allocation to stablecoin-related assets.

3. Tesla (TSLA.US) – Musk Joins Trump’s China Delegation

Event Summary: Tesla’s stock rose nearly 4% on Monday after Bloomberg reported Elon Musk would join Trump’s U.S. delegation to China. Market Interpretation: Markets interpret this as potentially favorable for Tesla’s operations and policy environment in China. Investment Takeaway: Cross-border opportunities for auto and tech giants warrant attention amid high-level U.S.-China engagement—but geopolitical variables require close monitoring.

4. Moderna (MRNA.US) – Limited Commercial Impact from Hantavirus Incident

Event Summary: Although WHO emphasized low risk of widespread transmission of Andes hantavirus, Moderna briefly spiked early in the session. Evercore ISI analysts noted the company is unlikely to generate meaningful revenue from the incident, and shares ultimately closed down nearly 3%. Market Interpretation: Institutions stress that pandemic-related trades often exhibit far greater volatility than actual commercial impact. Investment Takeaway: Biotech stocks are prone to news-driven swings in the short term; long-term value remains anchored in pipeline progress and commercial execution.

IV. Cryptocurrency Project Updates

1. MARA released its Q1 FY2026 financial and operational results, reporting a net loss of $1.3 billion ($3.31 per diluted share), compared to a net loss of $533.4 million in the prior-year period. The increased loss stemmed primarily from a $1 billion unrealized loss tied to changes in the fair value of digital assets. During the quarter, MARA mined 2,247 BTC at an average cost of $76,288 per coin and sold 20,880 BTC at an average price of $70,137.

2. 21 Shares US announced its Hyperliquid ETF (THYP) will launch on May 12, 2026 (U.S. Eastern Time). Per its prospectus, THYP is a passive spot HYPE ETF designed to track the FTSE Hyperliquid Index. Subject to compliance and tax-risk considerations, the fund intends to stake a portion of its HYPE holdings.

3. The Ethereum Foundation is restructuring its Protocol team. Core developers Barnabé Monnot and Tim Beiko plan to step down, and Alex Stokes will take a leave of absence. Will Corcoran, Kev Wedderburn, and Fredrik will assume joint leadership responsibilities.

4. Bitcoin miner CleanSpark reported Q2 FY2026 results, posting a net loss of $378.3 million—up 173% from $138.8 million a year earlier—with $224.1 million attributed to losses on its Bitcoin holdings. At quarter-end, CleanSpark held $925.2 million worth of Bitcoin. Bitcoin mining revenue totaled $136.4 million, down 25% YoY. CleanSpark is accelerating its strategic pivot toward AI and high-performance computing infrastructure.

5. Circle published the Arc whitepaper. The mainnet is expected to launch in summer 2026, with the testnet having launched in October 2025. As of May 5, 2026, Arc has processed 244.1 million transactions. Positioned as a public Layer-1 blockchain for institutions, Arc is EVM-compatible, natively integrates USDC, supports sub-second settlement finality, stablecoin-denominated gas fees, and configurable privacy features. Cross-chain transfers are executed via Circle’s Cross-Chain Transfer Protocol (CCTP).

V. Today’s Market Calendar

Data Release Schedule

Key Event Preview

Tuesday, May 12

- U.S. April CPI data release; market expects YoY rise of 3.8%; ★★★★★

- New York Fed President Williams participates in a monetary policy panel discussion;

- Oklo Inc. (OKLO) reports earnings after market close.

Wednesday, May 13

- U.S. April PPI data release at 20:30 (UTC+8);

- Alibaba (BABA) reports earnings before market open; Nebius and Cisco (CSCO) report Q1 earnings after market close.

Thursday, May 14

- Trump may visit China May 14–15; the U.S. government has invited CEOs from NVIDIA, Apple, ExxonMobil, Boeing, and others to accompany him; ★★★★★

- Applied Materials (AMAT) reports earnings after market close; Cerebras Systems is expected to list on Nasdaq.

Friday, May 15

- Jerome Powell’s term as Fed Chair officially ends; Christopher Waller is expected to succeed him;

- 13F institutional holdings filing deadline; Berkshire Hathaway and others will disclose latest U.S. equity positions.

*This week’s core themes include Powell’s departure/Waller’s succession, U.S. CPI/PPI data, Trump’s potential China trip, and earnings from Circle, Oklo, and AMAT—expect heightened market volatility.

Institutional Views:

Wall Street analysts broadly agree that this week’s CPI data will serve as a critical market barometer; an upside surprise could temporarily dampen risk appetite, though the AI “super-cycle” narrative remains the dominant long-term thesis. JPMorgan Private Bank notes “the AI super-cycle may just be getting started,” maintaining optimism on tech equities. Goldman Sachs Chief Economist Jan Hatzius describes the global economy as “bending, not breaking”—while Iran-related tensions introduce short-term volatility, they do not alter the broader growth trajectory. In crypto, advancing Clarity Act legislation is viewed as a regulatory tailwind, and sustained BTC ETF inflows suggest that near-term geopolitical risks and inflation data will jointly define the volatility range—yet the long-term trends in AI and crypto infrastructure remain intact. Overall, markets seek equilibrium between inflation data and geopolitical developments, with technology and commodities likely to continue diverging.

Disclaimer: The above content was compiled using AI search tools and verified manually prior to publication. It does not constitute investment advice. Data presented herein may contain unavoidable discrepancies; please refer to real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News