Short positions have been squeezed out: Will Seoul take over as the next hub for the U.S. AI stock rally?

TechFlow Selected TechFlow Selected

Short positions have been squeezed out: Will Seoul take over as the next hub for the U.S. AI stock rally?

The driving force behind AI-related stock trading in the U.S. market is shifting from “short squeezes” to “retail FOMO.”

Author: Claude, TechFlow

TechFlow Introduction: On May 11, Nomura released a research report containing a key assessment: “At least for U.S. equities, the AI rally may be catching its breath.” On that same day, the KOSPI surged 4.32% to close at 7,822.24—triggering a buy-sidecar circuit breaker—and SK Hynix jumped 11.98%, surpassing Eli Lilly in market capitalization to rank 14th globally. The report’s prediction—“the next leg is Korean FOMO”—unfolded almost simultaneously with the Korean equity surge. The momentum behind the U.S. AI trade is shifting from “short-covering” to “retail FOMO.”

The U.S. AI rally is not over. The S&P 500 rose approximately 16.6% over 28 trading days—but where the money driving the index higher came from, and how much fuel remains, is undergoing subtle change. Nomura’s assessment is that the phase driven by short covering and institutional restocking is nearing its end; for the AI trade to continue, a new wave of capital must step in. Korea delivered precisely such a case study on the very day the report was published: the KOSPI breached three major thresholds—7,000, 7,400, and 7,800—within one week; retail investors plunged into “hynix FOMO”; and foreign funds piled into chip stocks via DRAM ETFs. The narrative is pivoting from the Nasdaq to the KOSPI.

U.S. equities appear unchanged on the surface—but the anomalous combination of “spot up / volatility up” has already flashed red

The surface-level readings of the U.S. AI trade remain robust. Saxo’s May 11 options briefing showed the VIX closing at 17.19, up 0.64% on the day. While this level sits below the historical average, the fact that the VIX rose even as the index hit record highs is itself an anomalous signal. The CBOE SKEW Index climbed to 138.21 (+1.54%), and the VVIX—the measure of VIX volatility—rose to 96.78 (+3.39%). All three indicators rising concurrently signals that institutional investors are not easing their hedges despite the index’s new highs.

In its May 11 report, Nomura described this configuration as the “anomalous posture” of U.S. tech stocks. It noted that the Nasdaq displayed the “spot up / volatility up” pattern: while the VIX continued falling, the VXN (Nasdaq Volatility Index) rebounded sharply. The Nasdaq options skew—defined as the difference between the implied volatility of 1-month, 25-delta put options and that of 25-delta call options—has rapidly declined to near-historic lows, reverting to levels last seen around October 2025. A declining skew means the premium for downside protection relative to upside calls has been compressed, indicating increasingly crowded pricing for tech-stock upside.

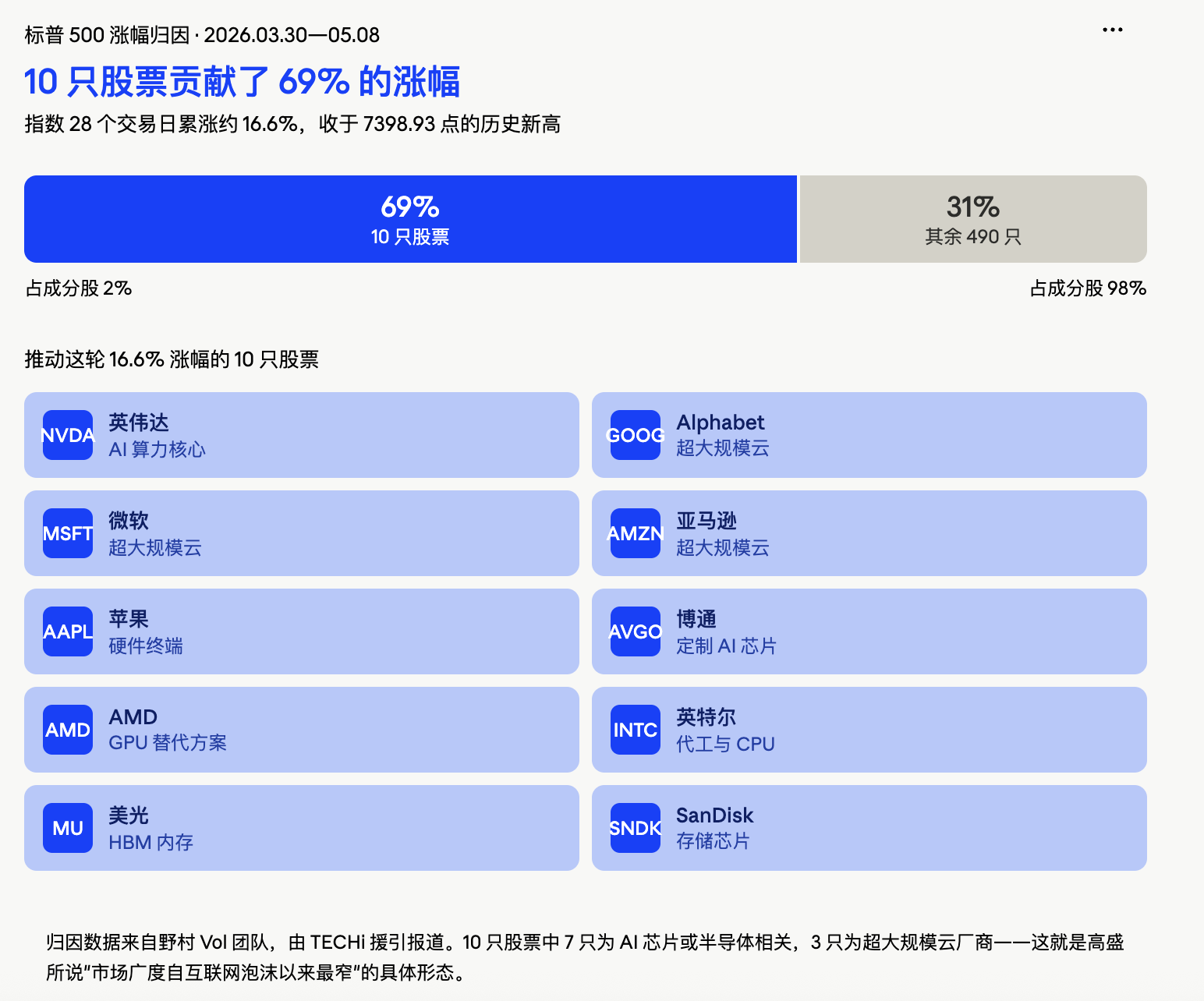

More noteworthy is the structure of this rally. According to TECHi’s citation of Nomura’s Vol team’s return attribution chart, 10 stocks contributed 69% of the S&P 500’s ~16% gain since March 30: Alphabet, NVIDIA, Amazon, Broadcom, Intel, Micron, Apple, AMD, Microsoft, and SanDisk. The remaining 490 constituents contributed just 31%. Ben Snider, Goldman Sachs’ Head of U.S. Equity Strategy, also pointed out that market breadth has narrowed to one of the tightest levels since the dot-com bubble era. Goldman Sachs lists “AI infrastructure buildout” and “Iran conflict” as the two clearest equity-market risks over the coming weeks.

The shorts have been squeezed out—so who pushes the next leg?

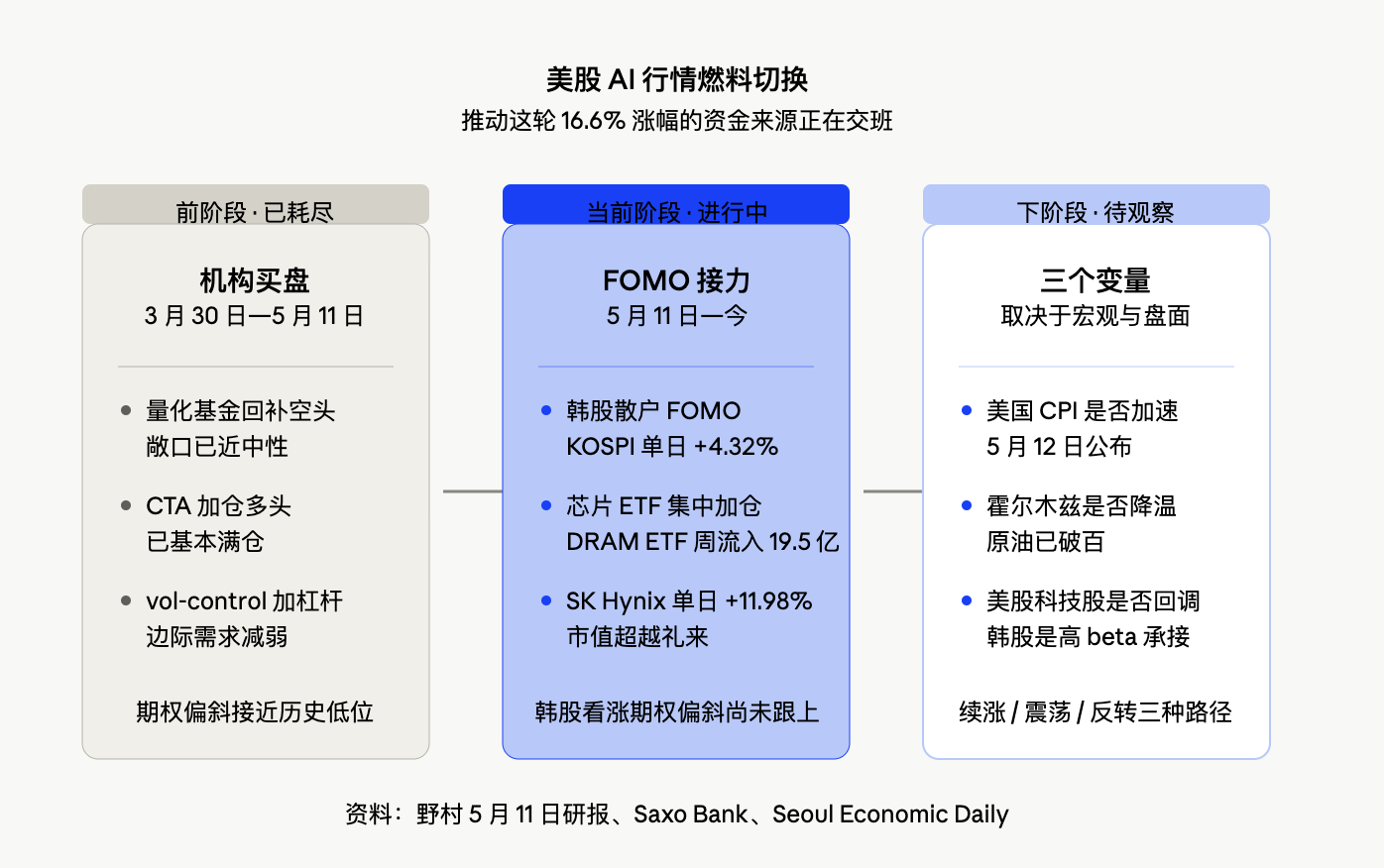

The truly decisive insight in Nomura’s report lies not in the “anomalous combination” itself, but in its dissection of funding flows: quantitative funds’ equity exposure has reverted nearly to neutral, meaning the forced buying and short-covering process is largely complete. Commodity Trading Advisor (CTA) funds have essentially returned to full long positions, and marginal incremental demand from volatility-control strategies is also waning.

In other words, the three main sources of buying pressure that propelled AI stocks higher over recent weeks—short squeeze, CTA accumulation, and leverage expansion driven by falling volatility—are now approaching exhaustion. If AI stocks are to rise further, they can no longer rely primarily on “shorts being forced to buy.”

Note that Nomura’s estimates of positioning across quant funds, CTAs, and macro funds are model-based, not direct holdings data. This distinction makes them better suited as thermometers of marginal shifts—not precise position statements. Yet even so, the directional signal is unambiguous: institutional systematic buying has neared its limit, and future upward momentum must rely more heavily on retail and sentiment-driven capital.

Goldman Sachs’ trading desk aligns closely with Nomura’s view. Rich Privorotsky, Head of Goldman’s One-Delta Trading Desk, previously characterized the current pace as “semi-irrational chasing,” drawing parallels to 1999—when surging telecom equipment orders provided a “real-world bottleneck narrative,” analogous to today’s AI compute scarcity logic. Goldman’s Volatility Trading Desk has classified the recent dynamic—“spot up / volatility up”—as one that constrains further systematic strategy accumulation.

This assessment implies the U.S. AI trade hasn’t collapsed—but the script of “rising further via short squeezes” is nearing its final act.

Korea delivers the answer: KOSPI surged 4.32% and triggered buy-sidecar on the day Nomura’s report dropped

Another judgment in Nomura’s report: if the AI trade is to extend further, the true continuation signal will be whether Korea experiences renewed FOMO.

On the day the report was published, Korea responded with an explosive breakout. The KOSPI closed at 7,822.24, up 4.32% on the day, and briefly touched 7,899.32 intraday—triggering the buy-side sidecar. SK Hynix surged 11.98% to ₩1.888 million per share, overtaking Eli Lilly in market cap to become the world’s 14th-largest company; Samsung Electronics rose 6.33% to ₩285,500. Together, the two companies surpassed ₩3,000 trillion in combined market cap—nearly half the KOSPI’s total. The combined market cap of the KOSPI and KOSDAQ exceeded ₩7,000 trillion for the first time—just eight trading days after breaching ₩6,000 trillion on October 27.

On May 12, the KOSPI pushed past 3,900 points (i.e., the 7,900-point level), setting yet another all-time high. Yet same-day data revealed FOMO’s flip side: of the KOSPI’s 948 constituent stocks, only 186 rose while 696 fell; roughly 30% of components were down year-to-date. Gains were entirely concentrated in the two semiconductor heavyweights—Samsung and SK Hynix.

Retail FOMO has spawned new market jargon. Korean financial media coined “hynix FOMO” to describe the fractured mindset among retail investors—simultaneously regretting missed opportunities (“I should’ve bought at ₩800,000!”), debating whether to jump in now, and worrying about an imminent correction. Online communities buzzed with discussions about “Samjeon-nix”—a portmanteau of Samsung and Hynix. This is a textbook retail-driven momentum-chasing pattern, highly consistent with Nomura’s definition of a “FOMO signal.”

Foreign fund flows tell an even more telling story. According to the Seoul Economic Daily’s May 10 report, the iShares MSCI Korea ETF (EWY) saw net outflows of $1.0145 billion between May 1–7—a sign of passive funds withdrawing from Korea. Meanwhile, the Roundhill Active DRAM ETF posted net inflows of $1.9538 billion over the same period. Within that ETF, SK Hynix accounts for 25.94% and Samsung Electronics for 21.62%—a combined 48%. Foreign capital isn’t selling Korea—it’s selling broad-based exposure and buying chips. This is precise, thematic AI allocation.

One detail warrants caution. In its May 11 report, Nomura noted that the KOSPI 200 also exhibited “spot up / volatility up,” yet call skew did not rise accordingly—suggesting volatility expansion wasn’t driven by call-buying demand. That is, as of the report’s publication, Korea had not yet entered the classic “fear-of-missing-out, rush-to-buy-calls” state. Whether this signal flips quickly following the KOSPI’s massive rally will be key to judging FOMO’s sustainability going forward.

Korean equities are an extension of the U.S. AI capex chain—the longevity of the next leg depends on the “top of the pyramid”

Korean FOMO is no isolated event; it’s essentially a high-beta extension of the U.S. AI capex narrative.

Data directly anchors this transmission chain. Bridgewater estimates that Alphabet, Amazon, Meta, and Microsoft will collectively spend ~$650 billion on AI-related infrastructure in 2026. Goldman Sachs cites data showing consensus capex estimates for the largest cloud infrastructure providers jumped $130 billion last quarter—to $67 billion—equivalent to over 90% of their projected operating cash flow. Microsoft’s Q3 capex reached $31.9 billion; Alphabet’s Q1 property and equipment purchases totaled $35.7 billion; and Meta raised its 2026 capex guidance to $125–145 billion.

This capital flows into data centers, GPUs, memory, networking, power systems, and cloud capacity. SK Hynix and Samsung sit squarely at the heart of this capital flow—HBM4 memory and high-bandwidth HBM are being fiercely contested by hyperscalers. According to Reuters, SK Hynix recently received “unprecedented” order proposals from major tech firms, with some customers volunteering to finance new production lines and ASML lithography tools. Chip capacity is effectively exhausted. This explains why the KOSPI’s 4.32% single-day surge is fully coherent within the narrative framework—Korean equities represent the “second derivative” of the U.S. AI story.

Yet this linkage also implies fragility. Should U.S. tech stocks undergo a full reversal, Korean equities would absorb the most direct, high-beta sell-off pressure. Another risk path flagged by Nomura is resurgent inflation forcing global central banks more hawkish—the U.S. CPI release on May 12 (this week) is pivotal, and current options markets still price low premiums for this event, suggesting the market hasn’t yet paid a high insurance premium for this risk.

A further macro variable: the Strait of Hormuz. WTI crude closed at $100.09 (+4.89%) on May 8; Brent crude closed at $105.66 (+4.31%). Tensions near the Strait of Hormuz continue escalating. Nomura’s assessment: so long as the strait remains disrupted and the U.S. and Iran remain divided on ceasefire terms, the AI-dominated market environment may persist longer than expected. Energy-price disruptions lift inflation expectations—but also make investors more reluctant to abandon “the AI story that’s actually generating returns.”

Layering these threads together: the U.S. AI rally’s short-squeeze-driven phase is nearing exhaustion; Korean FOMO has ignited, with synchronized retail and foreign chip-ETF buying—but options skew hasn’t yet caught up; the longevity of the next leg hinges on whether U.S. tech stocks correct, whether the U.S. CPI signals accelerating inflation, and whether the Strait of Hormuz ultimately cools. Nomura’s analytical framework is being validated step-by-step by market action—Seoul is emerging as the new epicenter of this AI trade.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News