A Detailed Look at the Global Banking Industry's Cryptocurrency Landscape: Redemption or Abyss?

TechFlow Selected TechFlow Selected

A Detailed Look at the Global Banking Industry's Cryptocurrency Landscape: Redemption or Abyss?

As of October 2023, more than 70 banks worldwide have participated in exploring cryptocurrency-related businesses.

Author: OKLink Research Institute

Introduction

Against the backdrop of a global economic slowdown and diverging economic landscapes, the banking industry faces new challenges. High deposit costs, low policy interest rates, and constrained lending potential in certain areas are undermining banks' traditional reliance on generating strong net interest margins. Going forward, banks will prioritize growth in non-interest income businesses to offset gaps in net interest income.

Technology-driven innovations represented by crypto assets are becoming a key area of focus for global banks. Although crypto assets still lag behind traditional financial assets in many aspects, rising institutional demand and improving regulatory environments are accelerating the development of the crypto market, offering new avenues for banking business growth.

According to incomplete statistics from the OKLink Research Institute, as of October 2023, more than 70 banks worldwide have engaged in exploring cryptocurrency-related services. Particularly over the past two years, an increasing number of major banking institutions have begun participating in the crypto market in more active and deeper ways, serving as critical bridges between the traditional financial world and the crypto ecosystem.

What does the current global banking landscape in crypto look like? Through what pathways can banks enter the crypto market? How should they address the risks and challenges posed by crypto assets?

OKLink Research Institute analyzes the crypto strategies of over 70 banks to uncover the answers.

TL; DR

-

Sustained institutional investor interest is the primary driver compelling banks and other financial institutions to take crypto assets seriously.

-

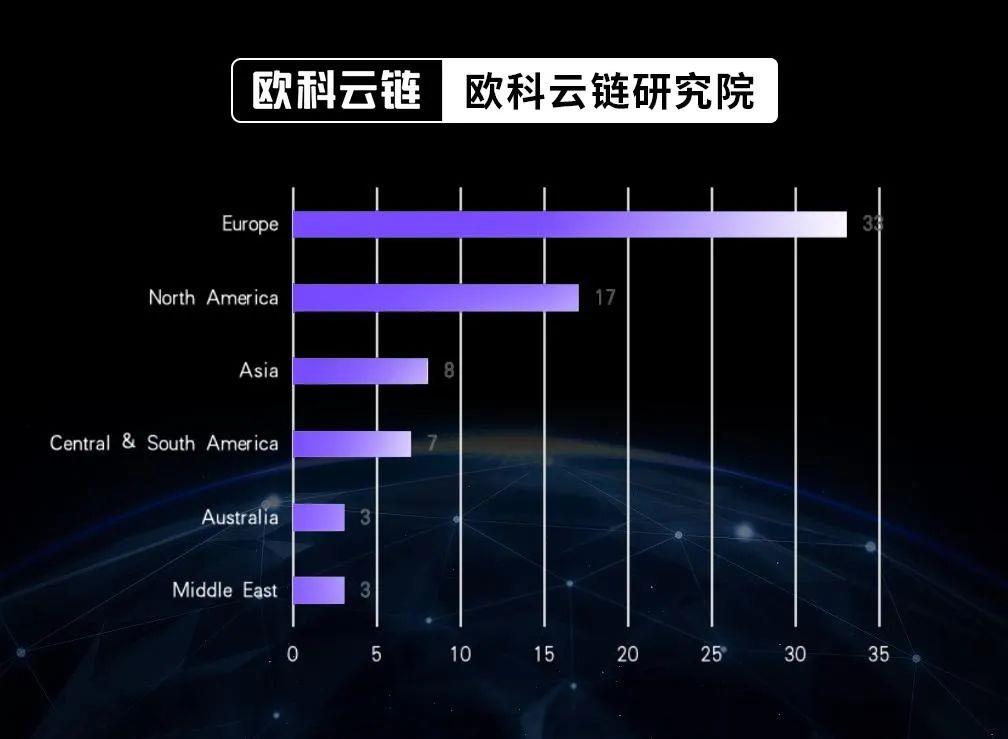

As of October 2023, over 70 banks globally are engaging with or exploring the crypto asset market through various approaches, with more than 70% concentrated in Europe and North America. Banks in Asia and the Middle East are becoming increasingly competitive in the crypto space.

-

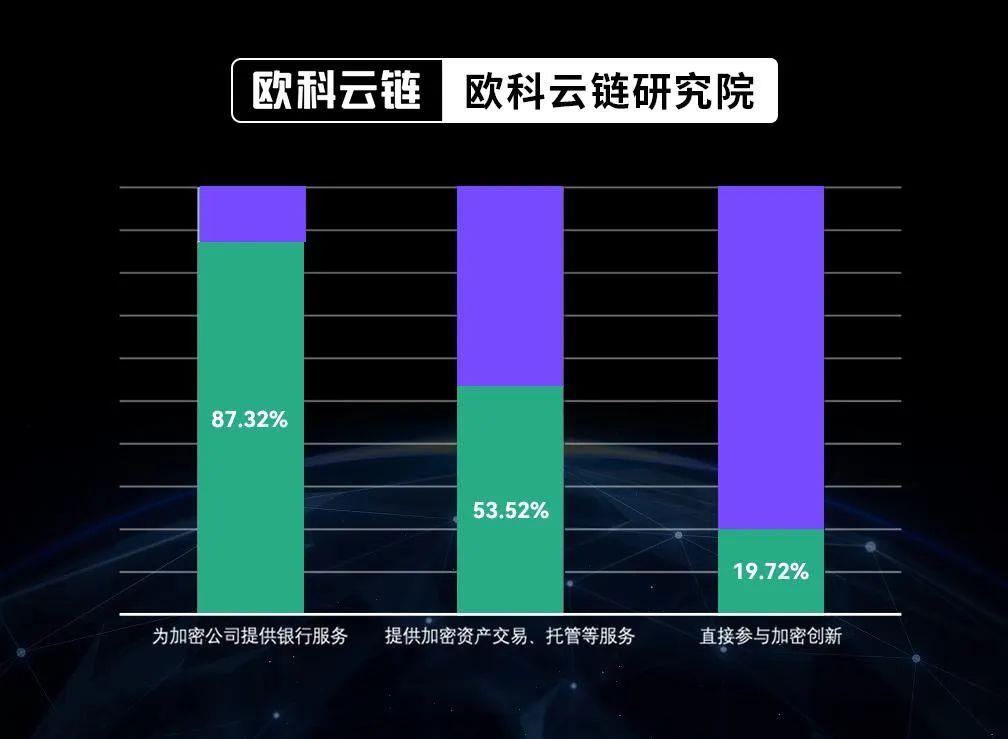

Providing banking services to crypto companies is currently the most common and foundational approach—among the over 70 banks surveyed, 87.32% are offering banking services to crypto firms.

-

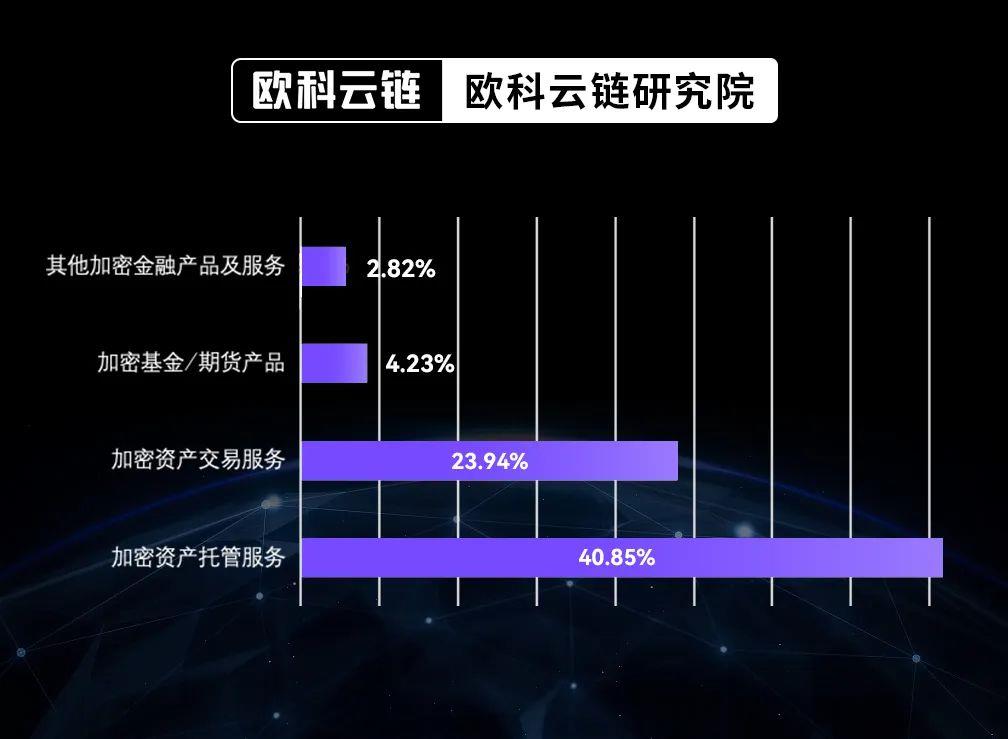

Crypto custody services are emerging as a key battleground in banks’ crypto market strategies—according to OKLink Research Institute, over 40% of banks exploring the crypto market have already launched or plan to launch crypto asset custody services.

-

Collaboration between banks and third-party firms to expand crypto offerings and acquire new customers is becoming standard practice. Nearly 70% of bank crypto custody products and services result from partnerships between banks and native crypto custodians or fintech companies.

-

Major banking institutions are attempting to participate more thoroughly and deeply in crypto innovation through initiatives such as stablecoin payments, tokenized deposits, and pilot programs involving tokenized assets and institutional-grade DeFi.

-

At least nine of the top 20 global banks by ranking have already participated in or planned crypto initiatives. Many other banks await broader adoption of digital assets by governments and mainstream institutions as a signal to fully develop or expand their crypto operations.

-

The enhancement of blockchain data capabilities and integration of on-chain and off-chain data are key determinants of success and scalability for bank crypto initiatives.

-

By integrating data and leveraging the combined strengths of traditional compliance technologies and blockchain analytics providers, banks can implement more effective technological solutions for monitoring and tracking crypto asset transactions, enhancing security and compliance in crypto operations to protect investors and earn customer trust.

1. The Global Banking Crypto Landscape

Crypto assets are transitioning from the periphery to the center of the global financial services industry. While the crypto market remains small compared to traditional asset classes, the timing for exploring crypto-related business appears increasingly favorable. Multiple factors are driving mainstream institutional adoption of crypto assets and related technologies, including clearer regulatory frameworks, the maturation of crypto-centered business ecosystems, and sustained growth in institutional investor interest.

The growing interest from institutional investors is the direct catalyst prompting banks and other financial institutions to recognize the value of crypto assets. Thanks to advantages in transaction efficiency and transparency, crypto assets are seeing rising adoption among both retail and institutional investors and are viewed as having the potential to solve some of the most persistent problems within existing financial systems—elevating levels of openness, trust, and client reach to unprecedented degrees. According to a survey conducted by Laser Digital, Nomura's crypto venture arm, covering over 300 institutional investors across 21 countries, 96% of respondents acknowledged the value of crypto assets and considered digital assets as part of their investment diversification strategy, comparable to traditional asset classes such as fixed income, cash, equities, and commodities.

However, due to regulatory compliance and other risk considerations, only a minority of banks currently engage directly in the crypto market. Following the collapses of Silvergate and Signature Bank, some crypto-friendly banks have temporarily exited the market under pressure from volatility and tightening regulation.

Nevertheless, as crucial gateways for fiat on-ramps/off-ramps and primary vehicles for institutional adoption, banks’ crypto initiatives continue to draw significant attention. According to incomplete statistics from the OKLink Research Institute, as of October 2023, at least 70 banks worldwide are participating in or exploring the crypto asset market via various pathways.

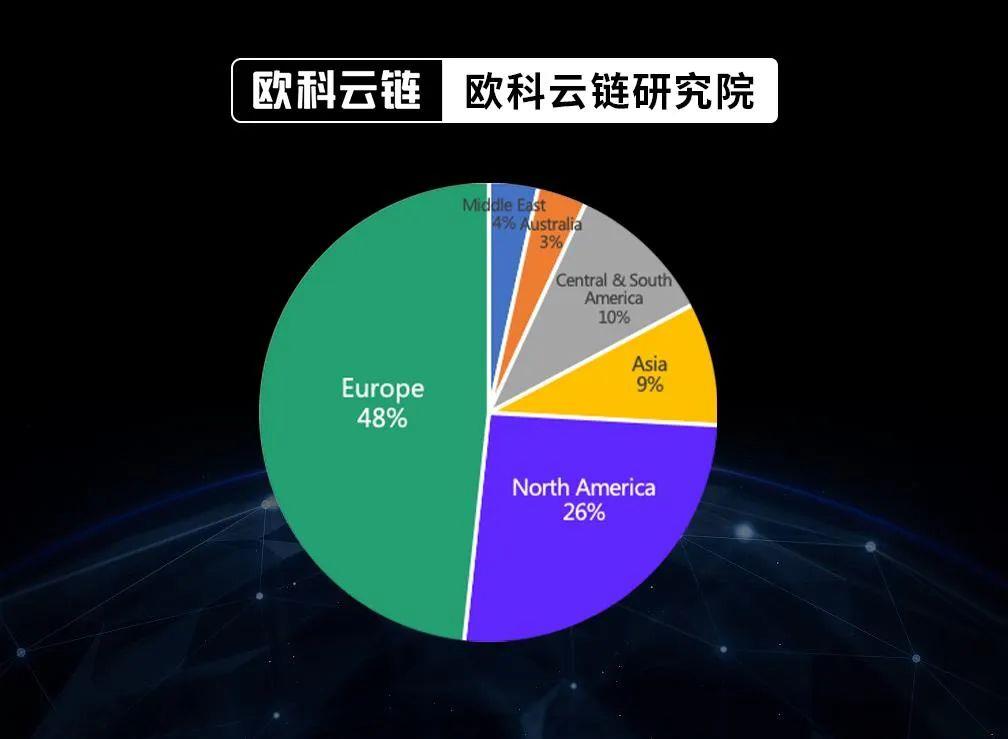

From this sample, over 70% of banks involved in or exploring the crypto market are located in Europe and North America. Specifically:

(1) With the implementation of MiCA regulations, European banks are further solidifying their leadership in the crypto asset space. MiCA establishes a coherent regulatory framework for the European crypto market, encouraging greater participation from banks and financial institutions in crypto innovation and making it easier for them to serve crypto firms from other jurisdictions.

(2) Despite hosting several crypto-friendly banks, the UK has become a difficult environment for crypto firms seeking banking services due to divergence from EU crypto legislation and heightened awareness of crypto-related risks. The few banks still collaborating with the crypto industry now require significantly more detailed documentation and information from crypto firms.

(3) The United States remains a significant player in the global crypto landscape, but its banking sector is no longer leading in crypto innovation. After the failures of Silvergate and Signature Bank, the Federal Reserve, FDIC, and Office of the Comptroller of the Currency have all warned banks to steer clear of crypto assets. Institutions like Metropolitan Commercial Bank and BankProv have chosen to abandon or gradually exit the crypto market amid regulatory and market risks.

(4) Banks in Asia and the Middle East are becoming increasingly competitive in the crypto asset domain. While the absolute number of banks engaged in crypto remains limited, surging regional interest in crypto assets and blockchain technology is driving more banks to explore entry into this space.

Distribution of banks participating in and exploring crypto assets

2. Pathways for Banks Entering the Crypto Market

Based on analysis of over 70 banks, there are currently three main pathways for direct bank participation in the crypto market:

(1) Providing traditional banking services to crypto companies;

(2) Offering clients crypto asset trading, custody, and related services;

(3) Direct involvement in crypto-related innovation ecosystems.

(Note: This analysis excludes indirect participation via investment or equity stakes.)

Pathways for direct bank participation in the crypto market

(1) Providing banking services to crypto companies is currently the most common and fundamental approach in banks’ crypto strategies—among the over 70 banks surveyed, 87.32% are providing banking services to crypto firms, nearly half of which are based in Europe. Aside from major institutions like JP Morgan, Citibank, and BNY Mellon, most U.S. mid-sized and smaller banks enter the crypto market by offering basic banking services to crypto firms.

Globally, however, crypto firms still face difficulties accessing traditional banking services. Beyond regulatory hurdles, banks must ensure all account applicants comply with strict anti-money laundering (AML), know-your-customer (KYC), and counter-terrorism financing (CTF) policies, undergo full due diligence, and avoid violating any financial sanctions. Although the crypto market is rapidly advancing toward compliance, shortcomings remain in these areas. Combined with inherent volatility and security risks of crypto assets, banks often need to dedicate substantial financial and human resources to manage complex and underdeveloped client management systems for crypto clients.

Geographic distribution of banks providing banking services to crypto companies

(2) More banks are entering the crypto market by offering crypto-related financial services such as trading and custody—53.52% of surveyed banks have already launched or are preparing to launch such products and services.

For banks aiming to serve crypto-savvy clients, offering custody services may be their first step into deeper crypto market engagement. While retail users remain a significant force in crypto, more institutional clients are entering and seeking secure, controlled methods for storing and using crypto assets. Traditional banks hold a natural advantage here, given their extensive experience safeguarding other types of assets. More importantly, custody services form the foundation for offering additional financial products such as trading, clearing and settlement, foreign exchange, lending, and investment management. According to the OKLink Research Institute, over 40% of banks exploring the crypto market have already launched or plan to offer crypto asset custody services.

Geographic distribution of banks offering crypto-related financial services

Banks can lead crypto innovation by establishing internal business units dedicated to exploring and building new models. This approach allows banks to gain direct insights into the crypto market, though it may hinder disruptive innovation that could impact core banking operations and comes with high costs.

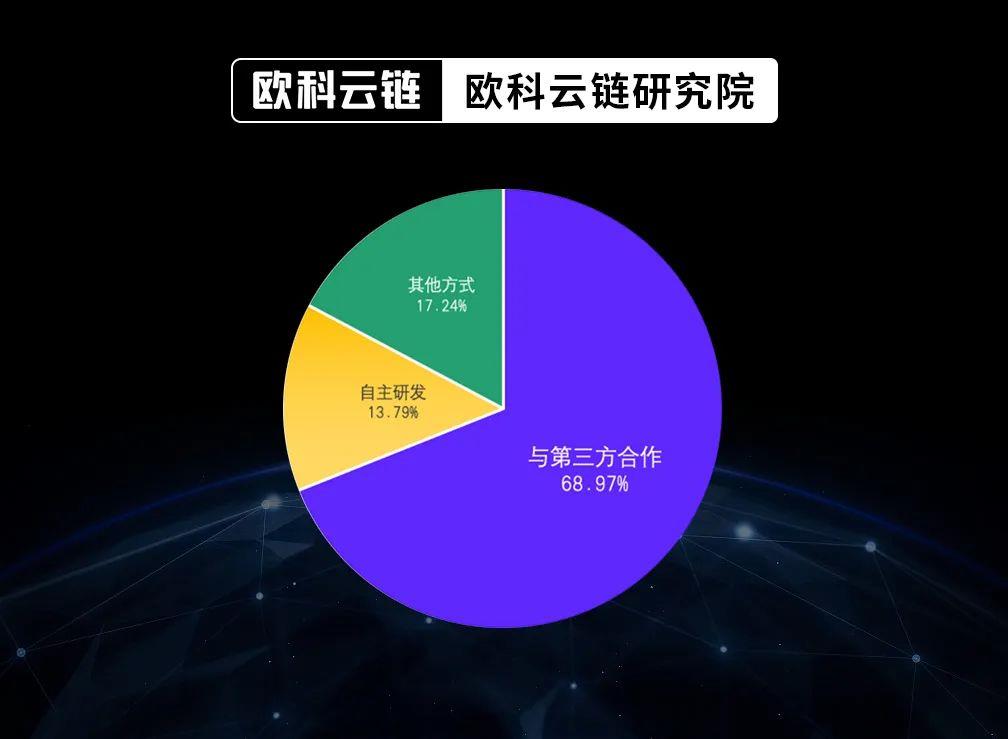

Bank relationships with crypto tech firms are rapidly strengthening. As industry convergence deepens, collaboration between banks and crypto technology/product firms has become commonplace—nearly 70% of bank crypto custody offerings result from partnerships between banks and native crypto custodians or other fintech companies, while only a minority have developed custody services entirely in-house. Collaborating with tech firms to expand crypto offerings and attract new customers is likely to become standard practice.

Methods used by banks to provide crypto asset custody services

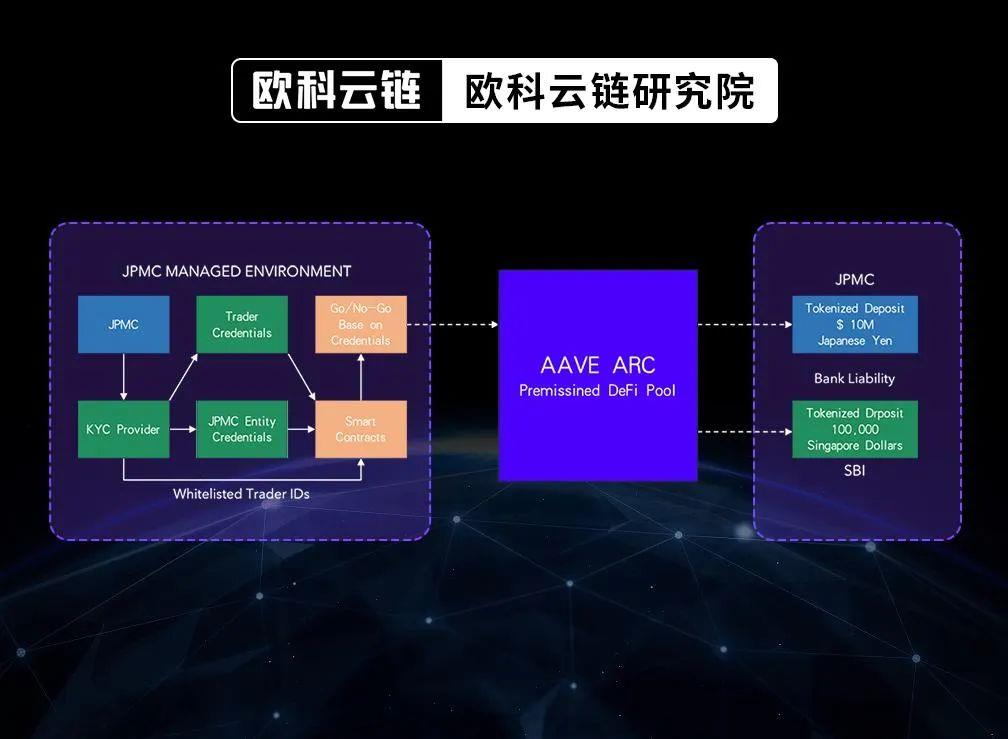

(3) McKinsey previously noted in its Annual Banking Report that to counter threats from fintechs, traditional financial institutions are integrating innovation through partnerships or internal teams. Crypto-centric innovative ventures represent "new species" for banks and similar institutions, yet direct participation in such innovation remains rare—even among the 70+ banks already exploring crypto, fewer than 20% are actively involved. However, this is changing. Major banks like JP Morgan and Citibank are conducting deeper explorations into crypto innovation, seeking more comprehensive and profound engagement through payment stablecoins, tokenized deposits, and pilot programs in institutional-grade DeFi and tokenized assets.

Some of the world’s best-known banks and financial institutions are now building their own digital asset trading platforms and blockchain systems, or supporting and incubating independent crypto firms to maintain operational independence. However, most direct innovation efforts by banks today occur within government-led pilot projects or inter-institutional trials, with few real-world user-facing applications.

JPMC's institutional-grade DeFi foreign exchange trading diagram

Bringing the focus back to the present, according to the latest World Bank rankings published by The Banker magazine, at least nine of the top 20 global banks have already engaged in or planned crypto market initiatives.

(Note: Among the top 20 banks in 2023, 10 are Chinese banks. Excluding these, one could argue that nearly all of the world’s largest banks are now exploring or positioning themselves in crypto.)

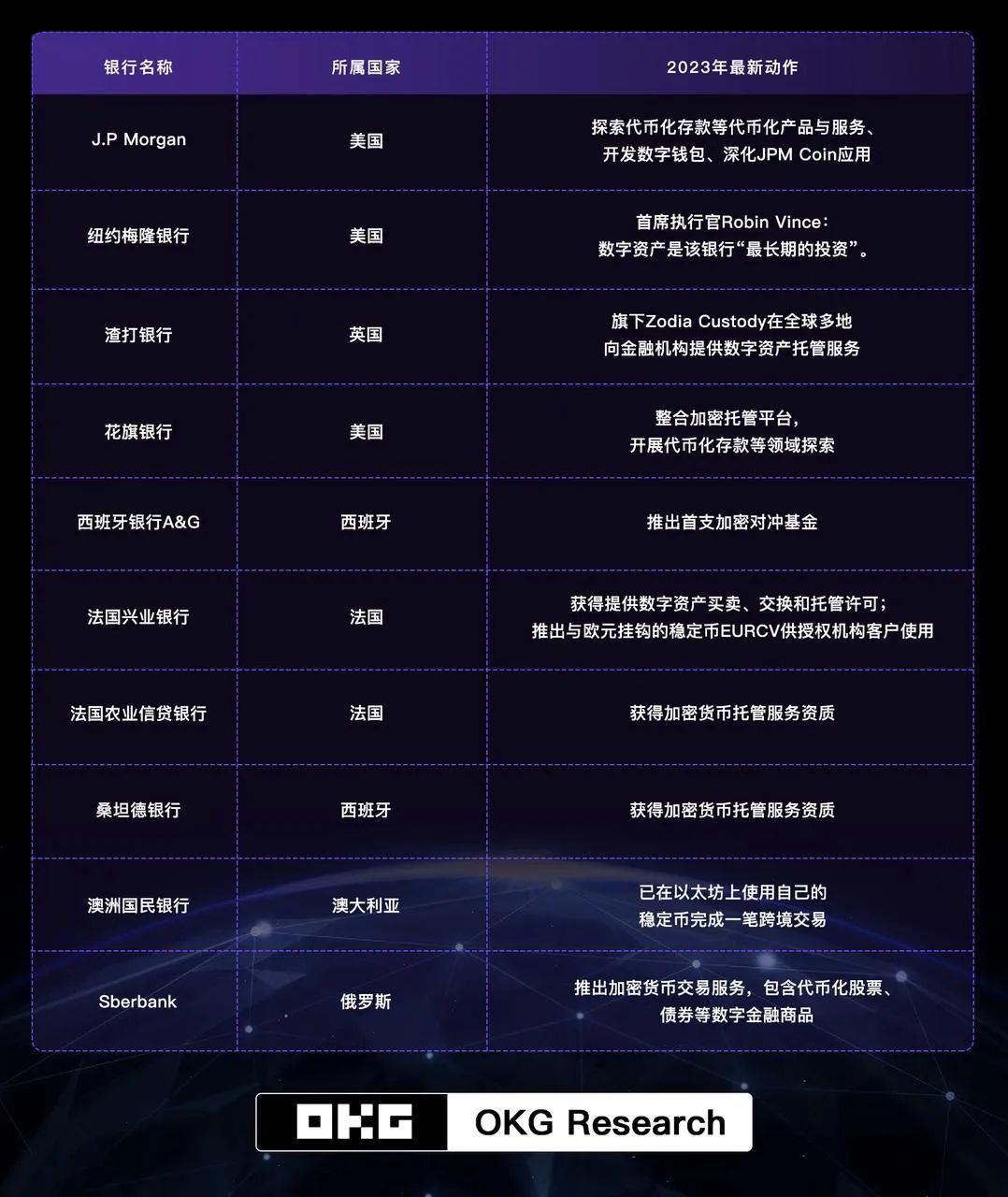

In 2023 alone, we’ve seen giants like JP Morgan, Citibank, Crédit Agricole, and Banco Santander actively involved in blockchain and crypto markets. JP Morgan leads in blockchain and crypto operations—its JPM Coin system had processed over $300 billion in transactions by June 2023, achieving notable success in inter-institutional clearing and settlement and cross-border payments, and deeply participating in the Monetary Authority of Singapore’s Project Guardian to explore institutional-grade DeFi and asset tokenization.

Key observations from 2023 include:

1) European banks have emerged as the main drivers in crypto business exploration;

2) Despite being in a bear market, banks are adopting more diverse and deeper approaches to blockchain and crypto market engagement;

3) Asset tokenization, crypto custody, and cross-border payments are defining themes in current bank crypto strategies.

Crypto business exploration and positioning by select banks in 2023

3. Accelerating Data Integration for Deeper Crypto Innovation

With rising global adoption and maturing technologies, banks are accelerating their integration into crypto innovation, driving advancements in core banking products and services such as custody, brokerage, trade clearing, settlement, payments, and lending. Crypto assets are increasingly moving into the mainstream through banking channels, potentially leading to exponential growth in asset scale and user adoption, ultimately enabling interaction with the real economy.

Each bank is gradually identifying the optimal path for engaging with blockchain and crypto businesses based on its unique circumstances. However, since the crypto market remains in early development and many regions lack detailed regulatory guidance, banks often pioneer new services without clear rules, resulting in higher compliance costs for innovation.

With the implementation of the EU’s MiCA regulation and the gradual refinement of crypto regulatory frameworks in jurisdictions like Singapore and Hong Kong, global crypto compliance is accelerating. To address risks that crypto activities may pose to banks, the Basel Committee on Banking Supervision—the global standard-setter for banking compliance—finalized its “Prudential Treatment of Cryptoasset Exposures” framework in December 2022, establishing a baseline for how banks should manage crypto asset exposures. Recently, the committee proposed disclosure requirements mandating banks to report their crypto holdings, complementing earlier standards. These evolving regulatory frameworks and standardized practices are boosting confidence among banks considering crypto market engagement.

Meanwhile, many banks are waiting for broader adoption of digital assets by governments and mainstream institutions as a signal to fully expand or scale up their crypto operations. Given recent governmental initiatives and strong signals of interest in digital assets from places like Hong Kong and Singapore, we believe the awaited signal will soon materialize.

When that moment arrives, banks aiming to capture valuable digital opportunities in the growing crypto market must offer innovative and competitive products and services. However, if the crypto market continues growing at its current pace, traditional banking infrastructure may soon become obsolete. Banks must begin now to build next-generation operational infrastructures capable of supporting crypto innovation, laying the foundation for risk resilience and sustainable growth. This includes upgrading legacy banking systems, processes, and technologies to securely manage client assets and conduct business, as well as implementing appropriate technological solutions to address data integration, security auditing, and compliance reporting.

Among these, on-chain data integration is the most urgent yet often overlooked challenge. While blockchain networks contain detailed histories of every confirmed transaction, expanding use cases mean on-chain data is increasingly encrypted and compressed, fundamentally different from data generated and used by traditional systems, posing significant challenges for standardization and utilization.

Enhancing data capabilities has become a top priority for global banks. Access to accurate data and ensuring its timely availability and sharing across all business functions are key to winning customer favor and gaining competitive advantage. Although banks have long invested in data capabilities, the pressure to derive actionable insights to better understand and serve customers has never been greater. Customers, especially institutional ones, are increasingly demanding real-time data and are more sensitive to risk. These trends require banks to leverage traditional and alternative data sets more effectively and forge new partnerships with third parties to deliver superior data-driven products and services.

For banks already involved in or planning crypto initiatives, enhancing blockchain data capabilities and integrating on-chain with off-chain data are critical determinants of both success and ultimate scalability. A lack of blockchain data capability not only weakens regulators’ ability to oversee crypto assets but also undermines trust with crypto clients, particularly institutions.

When mapping out their crypto strategies, banks must strengthen the collection and analysis of crypto transaction data in a rigorous and robust manner, focusing on integrating public blockchain data with internal business data to support core operations and establishing unified views and management systems for clients’ on-chain and off-chain transactions to achieve holistic business, compliance, and risk management goals.

To bridge gaps in blockchain data capabilities, banks are partnering with on-chain data providers such as OKLink and Chainalysis, combining technical strengths to improve crypto operational efficiency and compliance. In 2022, BNY Mellon completed integration with an on-chain data product, becoming the first globally systemically important bank to incorporate on-chain data into its risk management program. Other major and crypto-friendly banks like Cross River Bank and Barclays have also procured related products and services from third-party on-chain data providers.

Once on-chain data integration is achieved, banks can significantly accelerate the expansion of crypto services, using on-chain insights to assess market trends and inform strategic decisions. More importantly, mature on-chain data solutions enable banks to monitor and defend against crypto-related risks. While banks typically maintain robust AML, KYC, and BSA compliance programs, managing crypto risk exposure requires enhanced technologies and processes to improve agility and comprehensiveness in risk identification. By building on integrated data and combining traditional compliance tools with the expertise of blockchain analytics providers, banks can deploy more effective technological solutions to monitor and trace crypto asset transactions, enhancing the security and compliance of crypto operations to protect investors and earn customer trust.

4. Conclusion

Rapid advances in generative AI, embedded finance, blockchain, and cryptocurrencies, along with converging trends, are profoundly reshaping global banking operations and service models. Among these, the spread of crypto technologies presents the most direct and evident challenges and opportunities. While the absence of a clear, unified global regulatory framework may hinder crypto asset applications in certain contexts, the foreseeable regulatory trajectory and compliance progress have greatly enhanced the credibility of crypto-related banking activities. In the coming years, banks will accelerate their entry into the crypto market, significantly influencing the pace and direction of crypto innovation.

Assuming no major external disruptions, we believe:

(1) European banks will continue consolidating their leadership in crypto, while banks in Asia and the Middle East will grow increasingly active due to policy and market drivers;

(2) Banks will gradually develop differentiated competition in crypto services—crypto trading and custody will be the most fiercely contested and attractive short-term segments, while the long-term potential of asset tokenization markets is even greater;

(3) Banks should begin now to plan scenarios and pilot projects around the impact of asset tokenization on business models and new value creation opportunities, placing greater emphasis on blockchain data throughout the process and accelerating integration between blockchain data and traditional business data to better formulate short-term responses and long-term transformation strategies.

Appendix: Crypto Strategies of 50 Global Banks

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News