Obstacles, Banks, and Breakouts

TechFlow Selected TechFlow Selected

Obstacles, Banks, and Breakouts

How blockchain developers previously attempted to build solutions for institutions.

By Prathik Desai

Translated by Block Unicorn

I love exploring how crypto changes the way money flows. It feels great—but reality is far more complex. Just look at how large institutions have moved money over the past decade, and you’ll quickly see why.

Transatlantic bank wire transfers still take one to two days. They pass through intermediary banks, generating reconciliation records at every step—and customers pay $25–$45 in fees. This system’s architecture is nearly identical to that of the 1970s, except email replaced phone calls and SWIFT replaced a tangled web of cables. Sure, databases now run faster—but that’s it. Time hasn’t meaningfully improved.

You might think this is a technology problem—but I believe it’s primarily a coordination problem.

Blockchains and stablecoins have existed for over a decade. Yet they’ve never solved all the problems at once. Some blockchains and stablecoins deliver the speed institutions need—but sacrifice “transparency” by exposing all data publicly. Others balance speed and privacy—but create isolated systems that can’t communicate with each other.

The trouble with new technologies is that they easily intimidate large institutions operating in highly regulated industries—like banks. To get them to migrate, every pain point must be resolved *in advance*. Any “fix-it-after-migration” approach simply won’t work.

Though it took time, this situation is finally changing. Ironically, banks are now turning to blockchain technology—not to lead innovation, but to avoid losing ground to digital assets.

Last month, five U.S. banks jointly launched the Cari Network—collectively holding over $750 billion in assets. The system converts ordinary deposits into digital tokens that settle instantly, operate 24/7, and remain FDIC-insured.

In today’s deep dive, I’ll walk you through how blockchain developers previously attempted to build institutional solutions—and what makes this time different.

Swinging and Missing

Roughly a decade ago, consortia like R3 and Hyperledger built private blockchains for institutions, backed by ambitious roadmaps and membership rosters including BNP Paribas, Citigroup, and Barclays—the world’s top financial institutions. Though these blockchains functioned correctly and updated ledgers accurately, they remained siloed—unable to interact with anything outside their closed infrastructure.

These efforts eventually faded. Others pivoted to alternative approaches.

Banks then began experimenting with public blockchains—primarily Ethereum. This immediately solved composability: a shared, neutral ledger accessible to all enabled banks to interact across ecosystems. But solving one problem created another. On public chains, anyone who knows where to look—using only a browser—can see every counterparty, every transaction, every balance.

What banks needed was a single system delivering privacy, compliance, speed, and connectivity.

What Changed

Two breakthroughs emerged in 2025—one technological, the other demand-driven.

First, the technology: zero-knowledge proofs (ZK proofs) have gained attention for their unique advantages. ZK proofs are cryptographic methods allowing you to verify a transaction’s validity *without revealing its details*.

Though ZK tech has existed for years, only recently has it become cheaper and faster. Previously, generating such proofs was prohibitively expensive—making commercial deployment impractical.

Transactions per second have surged from as low as 400 to at least 15,000. Finality time has shrunk to under one second—all while preserving transaction privacy and counterparty confidentiality. By contrast, traditional financial infrastructure takes at least one day to process such transactions.

ZK proofs also addressed another barrier enterprises perceived.

In 2018, a bank evaluating blockchain had to hire engineers to build a chain from scratch, figure out proof generation, run its own servers—and then verify whether any of it translated into business value. At the time, it wasn’t even clear the system would work.

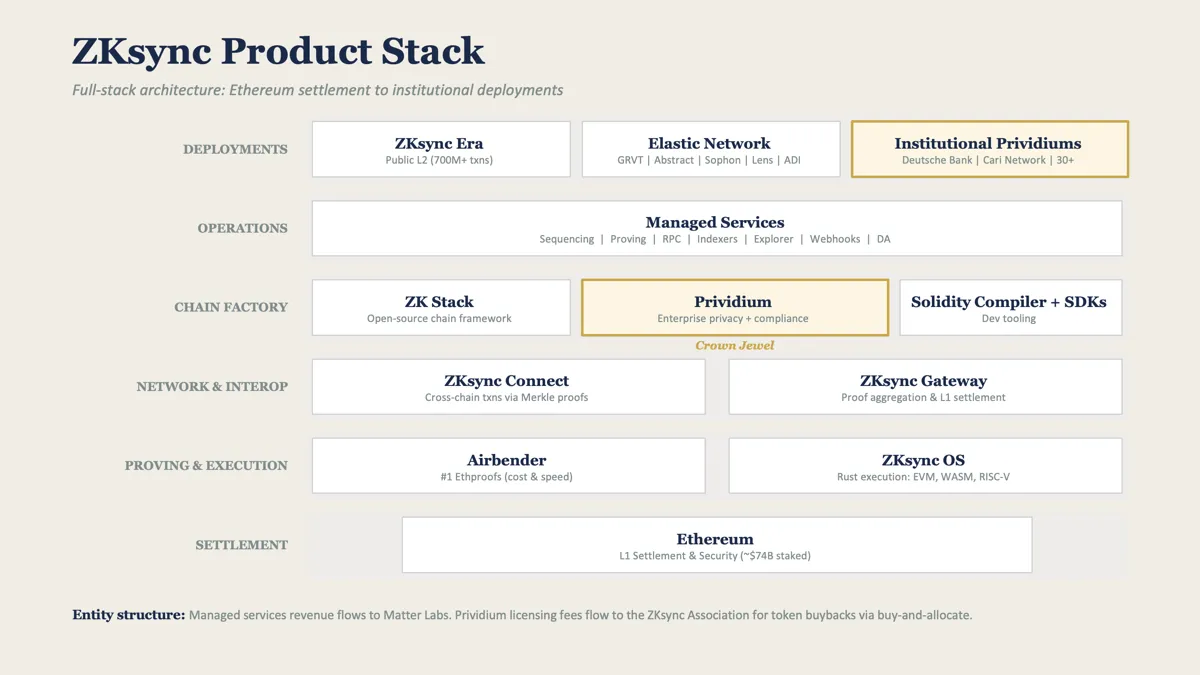

ZKsync—a Matter Labs–built Ethereum scaling platform—solves this by offering enterprises a blockchain equivalent of AWS. Its institutional suite—including Prividium, Connect, and Gateway—provides chain deployment, transaction processing, proof generation, compliance tools (KYC checks, role-based access control, login controls), and cross-chain connectivity.

This tech stack lets enterprises customize configurations and begin deploying immediately—think “blockchain-as-a-service.”

ZKsync isn’t the only company offering such solutions. Canton Network—backed by Goldman Sachs, DTCC, Citadel, and BlackRock—takes a different path. Instead of ZK proofs, it uses a permissioned model where authorized validators coordinate private transactions between known counterparties.

Both are building the connectivity layer institutions require—but they disagree on how trust should be established: via cryptographic proofs or via contractual governance among known participants.

In my view, the distinction between permissioned and permissionless approaches is increasingly irrelevant today. Both aim to solve the same institutional problem. In fact, Canton’s institutional partners may even surpass ZKsync’s.

Yet certain ZKsync features could tip the scales. Canton’s permissioned network works well when fund interactions occur between known parties within familiar jurisdictions. But when enterprises expand across borders—and transact with participants outside Canton’s walled jurisdiction—ZKsync enables cross-jurisdictional composability.

It’s precisely this technological breakthrough that’s driving banks’ adoption of blockchain.

But why would banks abandon their long-standing, battle-tested systems—even if those systems are slow? Is it merely because a cheaper, faster alternative exists?

Do you really believe banks will pivot from “blockchain is interesting but not practical” to “blockchain is commercially meaningful” just because a technology they barely understood suddenly becomes economically viable? Interestingly, every technology gains “strategic importance” the moment enterprises start losing money.

The Gold Rush Under Siege

Over the past decade, the stablecoin market has grown to $300 billion. They’ve achieved what banks refused to do for years: move money rapidly. Today, every circulating digital dollar has exited the banking system.

The infrastructure I mentioned above—ZKsync’s Prividium and Canton’s permissioned payment systems—is precisely what helps banks reclaim market share in digital assets. With blockchain-as-a-service (BaaS), banks can tokenize existing deposits and move them just like stablecoins—processing and settling transactions at the same speed and finality. And there’s an added benefit: banks achieve all this while offering depositors the regulatory protections and balance-sheet advantages only banks can provide.

This is already happening in the real world.

Last month, five U.S. regional banks—Huntington Bank, First Horizon Bank, M&T Bank, KeyCorp, and Old National Bank—launched the Cari Network, tokenizing bank deposits on ZKsync’s Prividium platform. These deposits remain on the banks’ balance sheets, retain FDIC insurance, and settle in seconds.

The Cari Network isn’t an isolated event.

In February 2026, the Central Bank of the UAE approved DDSC—a dirham-backed stablecoin running on ADI Chain and built using ZKsync’s proof engine.

In June 2025, Deutsche Bank began building a tokenized platform on a ZKsync-supported chain—cutting new fund setup time from months to weeks.

The Future of Institutional Finance

When writing about finance, I often return to a core question: “How will money flow in the future?” It’s worth asking—because it reveals how individuals and enterprises behave financially.

I believe most people—regardless of affiliation—don’t deeply care about crypto’s foundational principles. Banks care even less. I’m certain bank leadership teams aren’t gathered in conference rooms debating decentralization vs. centralization. They certainly don’t care whether their transactions settle on Ethereum, Solana, or some private network in Timbuktu.

What they *do* care about is privacy, composability, and speed. If a system saves them a few dollars while meeting those needs, it grabs their attention. And if adopting new tech comes with a “strategically critical” rationale—like a stablecoin revolution threatening to disrupt their business—that’s even better.

So I expect the convergence of Web2 and Web3 finance to center on technologies that move money more efficiently—whether via ZKsync- or Canton-supported blockchains tokenizing fiat currencies, or via dedicated payment blockchains being built by firms like Circle (Arc), Stripe (Tempo), and Stable.

I see little difference between these options. For banks reluctant to adopt stablecoins, ZKsync’s blockchain-as-a-service is clearly the more natural evolution. Banks already integrating stablecoins into payments will opt for blockchains supporting digital dollars.

But I’m certain of one thing: the biggest losers will be those clinging to legacy systems that still move and settle funds based on calendar dates and clock times.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News