Circle's silver lining: cracking the puzzle of declining USDC supply in an era of rising interest rates

TechFlow Selected TechFlow Selected

Circle's silver lining: cracking the puzzle of declining USDC supply in an era of rising interest rates

This article will analyze the loss of USDC supply and its impact on Circle.

Written by: Matías Andrade & Kyle Waters

Compiled by: TechFlow

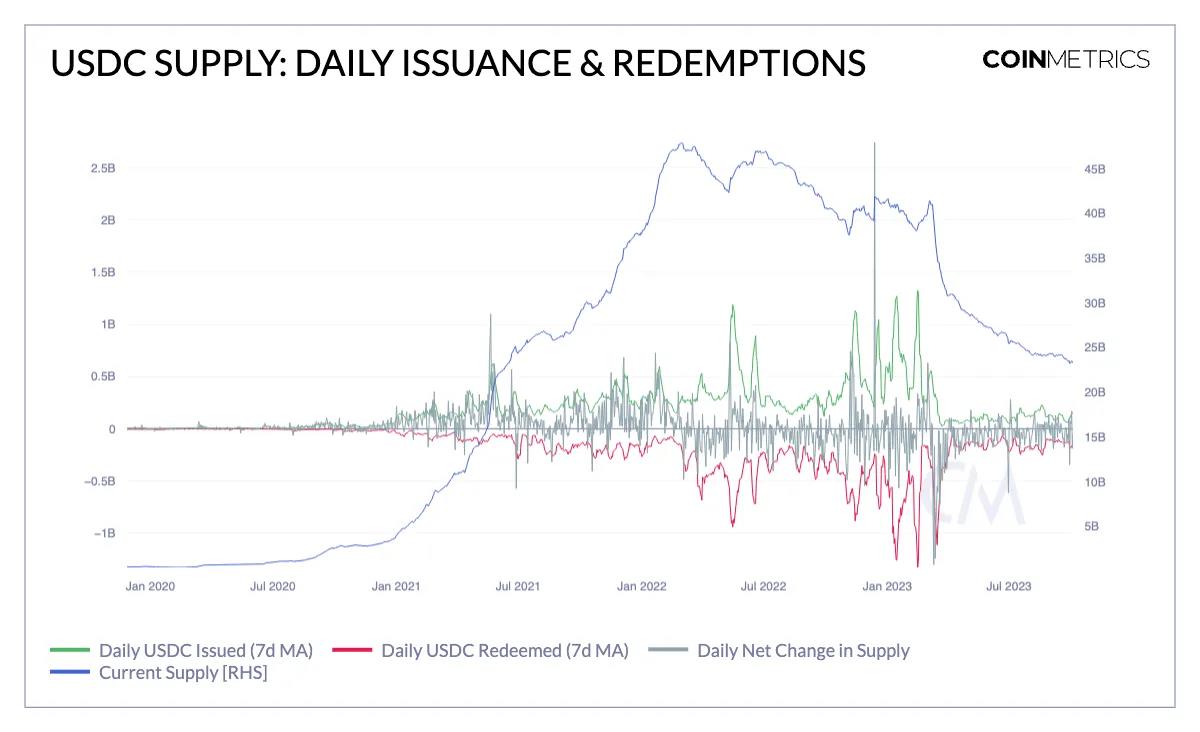

The strong momentum in stablecoin growth powerfully indicates surging demand for digitized U.S. dollars on public blockchains—platforms that operate 24/7, 365 days a year, transcending borders and time zones. Among stablecoin giants, Circle, operator of the largest domestic stablecoin USDC, has seen remarkable ascent. However, 2023 started with a series of new challenges. The supply of USDC on Ethereum—accounting for the majority of total USDC—has declined from $41.5 billion at the beginning of the year to around $23 billion today, a drop of 44%, as redemptions have exceeded new issuances.

In this article, we analyze the decline in USDC supply and its implications for Circle. We break down the current USDC supply into various categories to pinpoint where depletion has been most pronounced. A pressing question remains: Is this supply contraction concerning? Further, can this business model remain resilient amid a macroeconomic environment of rising interest rates?

By combining on-chain analysis with off-chain financial insights—primarily from publicly available SEC filings and Circle’s attestation reports—we offer a comprehensive view of the impact not only on the blockchain ecosystem but also on Circle as a corporate entity, particularly in light of its ambitions for public listing. Through this synthesis of off-chain and on-chain data, we assess crypto-native dynamics and broader business implications for Circle.

The Missing $18 Billion in USDC

Although currently at $23 billion, the USDC supply landscape is complex. This still represents nearly a tenfold increase compared to just three years ago, yet it marks a significant drop from its peak of over $47 billion in early 2022. The most dramatic phase of USDC supply loss occurred in Q1 2022, coinciding with the collapse of Silicon Valley Bank (SVB)—an event we previously analyzed in depth. In the aftermath, USDC supply dropped by an astonishing $10 billion in March alone.

But SVB was not an isolated incident; escalating government and regulatory scrutiny of domestic stablecoin operators (some call it “Operation Choke Point 2.0”) adds another layer of complexity. Offshore issuers like Tether have benefited significantly, increasing their supply from $70 billion to $77 billion within just the month of March 2023.

The current rising interest rate environment is also a critical variable. For USDC holders, this shift introduces a clear opportunity cost. Existing stablecoin operators like Circle do not pass the interest generated from reserves directly to on-chain USDC token holders—a point we will explore further later.

However, the massive outflow of USDC appears to be slowing, as shown in the chart below. Nevertheless, daily trading volumes of redemptions and issuances remain far below pre-SVB levels.

The structure of USDC supply contraction in 2023 tells a multifaceted story, but several trends stand out. Here, we break down the supply by category:

-

Split Between EOAs and Smart Contracts

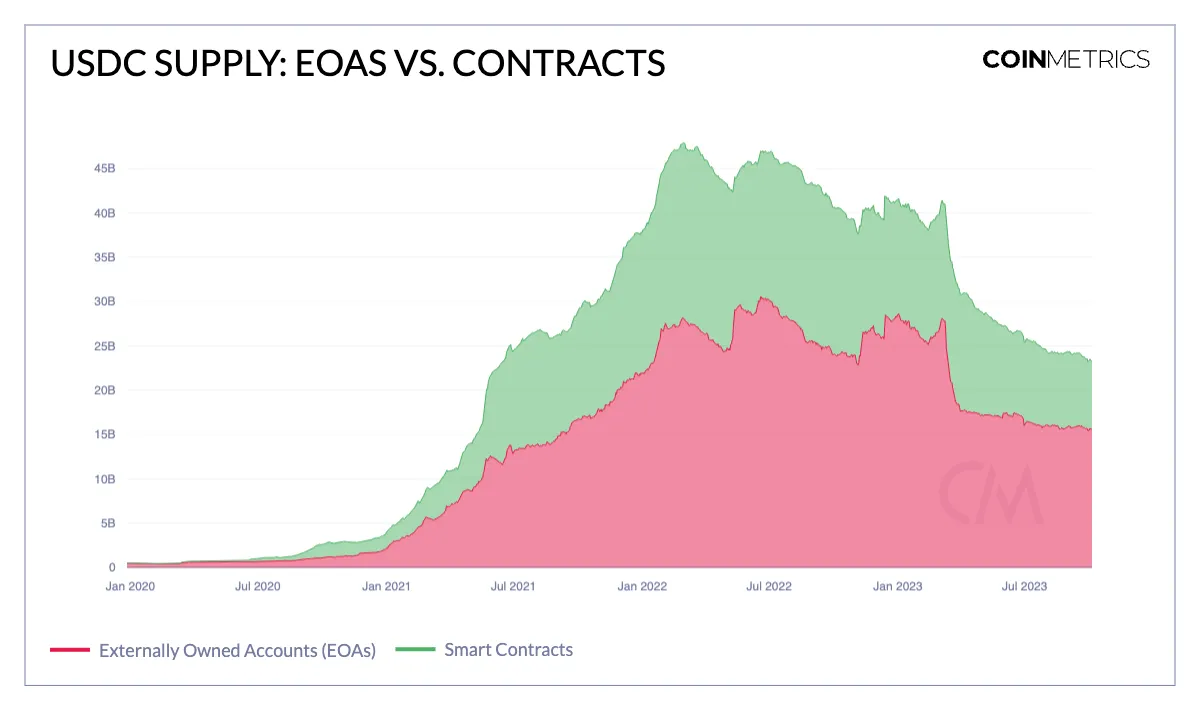

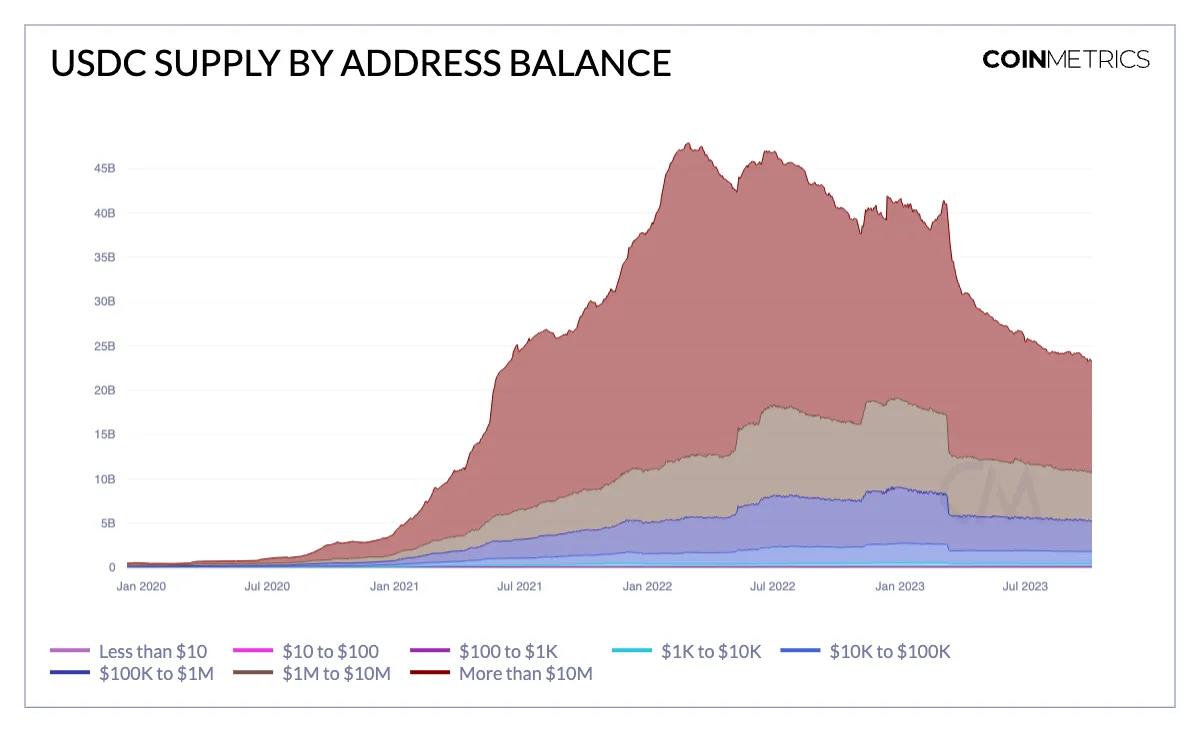

First, we compare USDC held in smart contracts versus externally owned accounts (EOAs), which are standard Ethereum user wallets. Currently, about $7.6 billion in USDC—roughly one-third of the total—is held in smart contracts. This marks a 44% decline from $13 billion at the start of 2023. EOAs have experienced a similar contraction, falling from $28 billion to $15 billion. Interestingly, since the immediate aftermath of the SVB crisis eased, a larger share of supply losses has come from smart contracts.

-

By Wallet Size Tier

We can also segment USDC supply by wallet size. As expected, the largest tiers have suffered the heaviest losses. Wallets holding over $10 million in USDC now account for $12.5 billion, down from $22.5 billion earlier this year. While this decline partly reflects the skewed distribution of holdings, in percentage terms, the largest wallets have seen the most significant contraction. In contrast, wallets holding between $100 and $1,000 in USDC have collectively increased their share of the supply by 28% year-to-date. Most of the losses in large-tier wallets occurred during the SVB collapse, which logically prompted large holders to diversify.

-

Top Holders

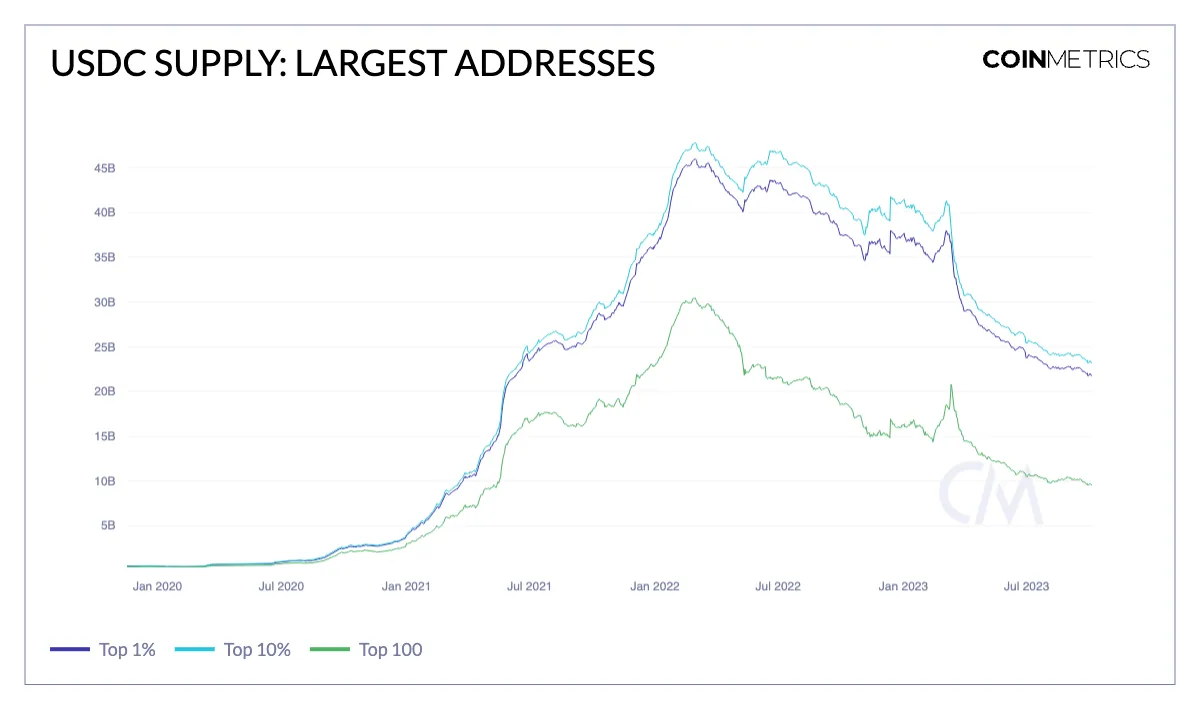

We further examine USDC’s top holders. The top 1% and top 10% of addresses now hold a larger share of the total USDC supply than they did at the beginning of 2023. This concentration peaked around the SVB crisis, possibly due to USDC being funneled into decentralized exchange pools or exchange wallets. However, the total number of USDC-holding accounts has grown from 1.6 million to 1.8 million this year.

The 2023 USDC supply landscape is complex, driven primarily by two overarching trends: post-SVB migration toward offshore stablecoins and rising interest rates incentivizing capital to chase higher yields. While supply-side dynamics may cast uncertainty, rising rates are simultaneously boosting Circle’s operational performance.

Circle's Treasury

One advantage of stablecoin design is transparency of supply, which is auditable in real time—at least regarding on-chain data. However, when we also consider Circle’s financial statements and monthly attestation reports, we can begin constructing a model of Circle’s USDC treasury and how it operates, especially its profitability.

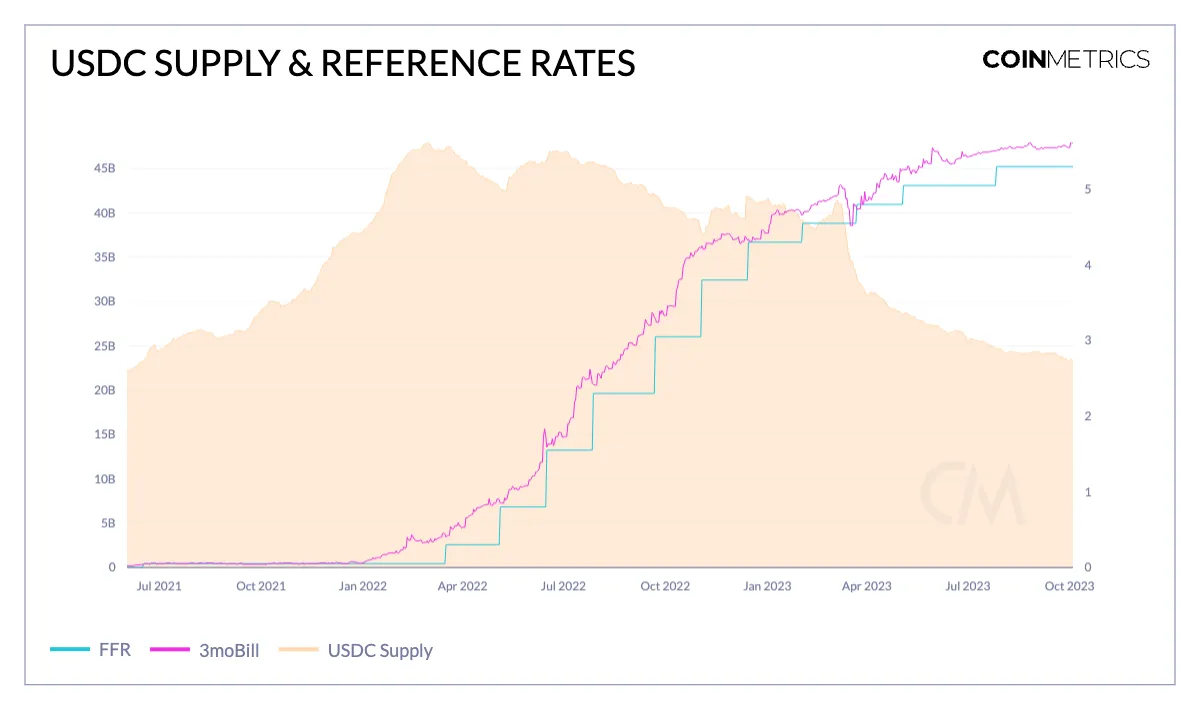

Looking at BlackRock’s Circle Reserve Fund, we find the portfolio broken down by asset maturity, with all holdings maturing within two months, and 65% maturing within 1–7 days. This estimate assumes a constant allocation split between overnight reverse repos and 4-week Treasury bills at 70% and 30%, respectively.

The portfolio size is estimated to match the current USDC supply, which may not fully reflect Circle’s treasury operations—particularly redemption flows—but should be proportionally consistent. Still, this provides a naive estimate of expected daily returns from these investments, ignoring transaction costs, rollover fees, and management expenses inherent in running such a portfolio.

Using data from FRED, we can estimate returns from these securities: the effective federal funds rate for overnight repo returns and the 4-week Treasury rate for the remainder, weighted at 70% and 30%, respectively.

As shown above, daily returns are highly correlated with interest rates. Although USDC supply peaked in early 2022, estimated daily income actually peaked in early 2023—after a nearly $7 billion reduction in supply. Even today, with supply $18 billion lower than earlier this year, interest income remains well above 2021 levels, when USDC supply was comparable. This clearly illustrates the fiat-collateralized stablecoin business model, highlighting increasing sensitivity to interest rates as a key driver of profitability.

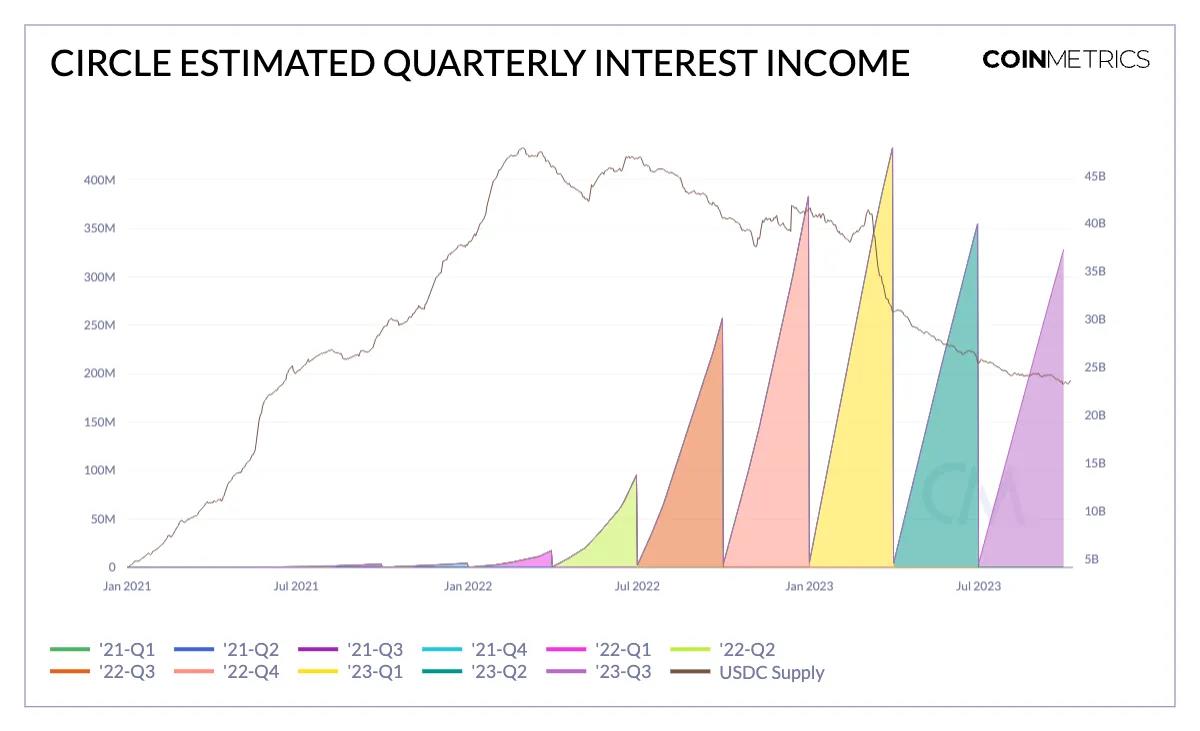

Using quarterly data from the chart above, we can compare it with reserve interest income disclosed by Circle in its financial reports. We see that they reported $274 million in interest income for Q3 2022, close to our estimate of $240 million. However, when considering full-year data and redemptions, this simple model begins to diverge. The lack of public financial statements after 2022 hinders full model validation. Nevertheless, it’s notable that Circle reportedly generated more revenue in the first half of this year ($779 million) than in the entire previous year ($772 million), across all its business lines.

Even amid news-driven excitement around PayPal’s stablecoin, structural factors driving stablecoin adoption are shifting—with rising interest rates at the forefront. The growing opportunity cost of holding cash may push stablecoin users toward yield-generating instruments like money market funds, which now offer over 5% returns—compared to less than 2% annualized in recent years. Moreover, yield-bearing stablecoins like sDAI and sFRAX are gaining traction, and Coinbase is already offering 5% yield on USDC.

Conclusion

The volatile USDC supply in 2023—including fallout from the SVB crisis and intensified regulatory scrutiny—has created a challenging environment for the business. Despite a significant supply decline, Circle has successfully leveraged the very same interest rate dynamics to boost its operational performance. Changing macroeconomic conditions and an evolving stablecoin landscape, highlighted by yield-bearing alternatives, underscore the need for adaptability and innovation. Circle’s strategic partnership with Coinbase, which offers competitive returns on USDC, demonstrates the necessity of proactive measures in this rapidly changing environment. As Circle considers going public, its ability to navigate these turbulent waters will test both its business acumen and its vision for the future of digital money.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News