On-Chain RWA Report: U.S. Treasuries Drive Yield Growth, a Small Number of Crypto-Native Users Lead Sector Demand

TechFlow Selected TechFlow Selected

On-Chain RWA Report: U.S. Treasuries Drive Yield Growth, a Small Number of Crypto-Native Users Lead Sector Demand

The growth of RWAs and the introduction of new types of RWAs on-chain are primarily driven by the demands of native crypto users, rather than new adopters of crypto.

Written by: Zack Pokorny

Translated by: TechFlow

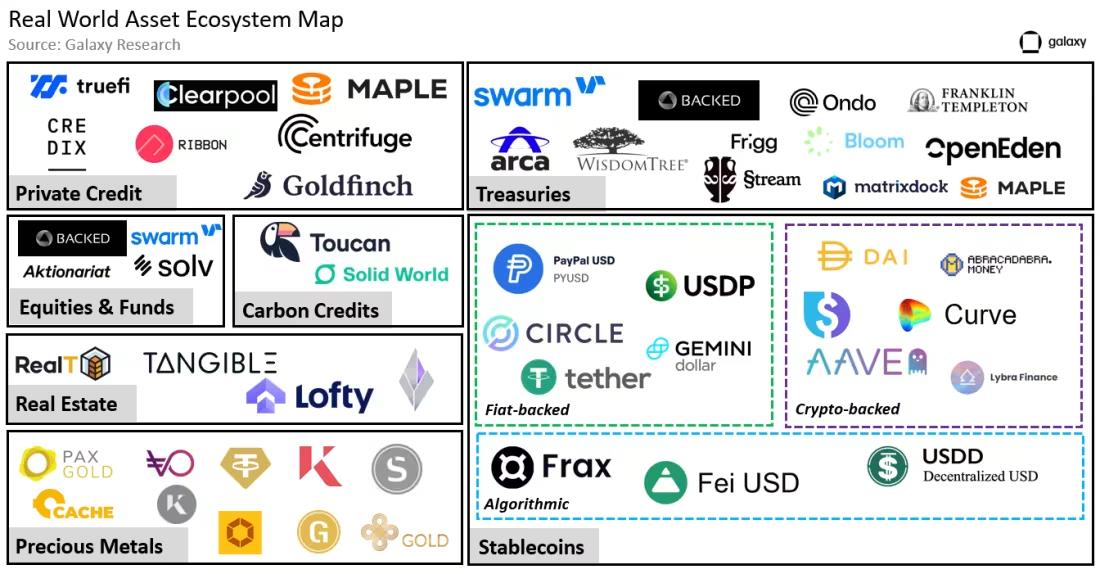

Several distinct types of real-world assets (RWA) exist on blockchains, each with unique characteristics and use cases. While certain RWA categories—such as stablecoins and tokenized gold—have existed for years, others like tokenized U.S. Treasuries have recently emerged amid rising interest rates. This article provides a brief overview of the following income-generating RWA types:

-

Real estate

-

Private credit

-

Government bonds

Note: The following analysis focuses on these tokenized RWA assets and their market capitalization. This report does not include information about the underlying protocols (e.g., Ethereum, Polygon, Stellar) that host RWAs or blockchain-native services facilitating RWA trading and financial management. Additionally, stablecoins—which represent the largest and oldest RWA category with a market value of $125 billion—are excluded from charts and RWA TVL calculations to avoid obscuring growth in smaller-market-cap RWAs or underestimating the momentum behind RWA adoption.

Integrating the Real World with the Digital World

RWAs are created by issuers who perform one or more of the following activities:

-

Acquire physical-world assets

-

Tokenize those assets onto a blockchain

-

Distribute RWA tokens to on-chain users

Without issuers—whether centralized firms, decentralized protocols, or hybrid models—RWAs would not exist on-chain.

Notable RWA issuers include:

-

Centrifuge ($238 million in active RWA issuance)—the largest issuer of on-chain private credit loans.

-

Franklin Templeton ($310 million in active RWA issuance)—a traditional financial institution issuing tokenized government bond tokens.

-

WisdomTree ($110 million in active RWA issuance)—an institutional capital markets firm issuing treasury-tracking funds.

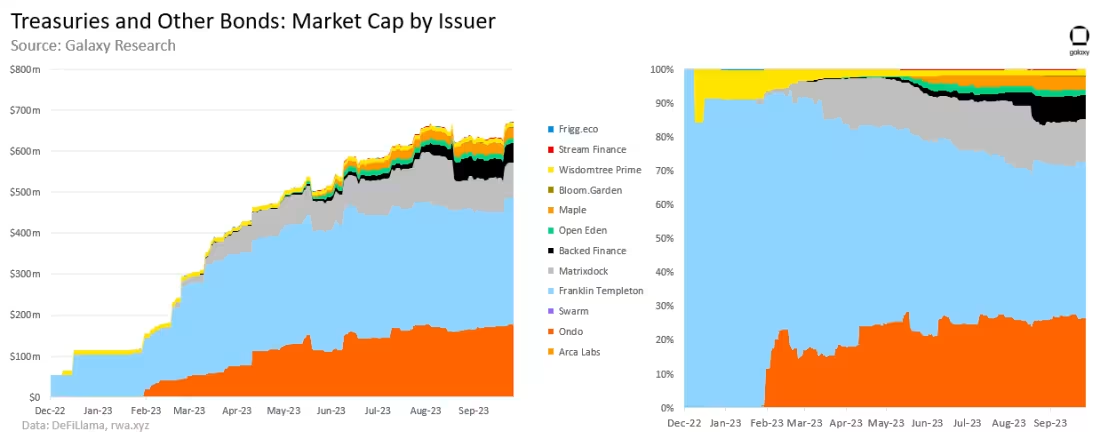

This short list, along with other issuers shown in the chart above, highlights how off-chain entities back on-chain RWAs. Franklin Templeton and WisdomTree are both established traditional finance companies whose core businesses are unrelated to cryptocurrency and blockchain technology. Franklin Templeton is a 76-year-old global investment firm offering mutual funds, ETFs, and other fund products to individual and institutional clients. It manages over 100 ETFs and mutual fund products, with total assets under management (AUM) exceeding $1.5 trillion. WisdomTree, founded in 1985, is a global financial innovation company providing diversified exchange-traded products (ETPs), models, and solutions. It currently manages $95.948 billion in AUM.

Over the past few years, Franklin Templeton and WisdomTree have begun experimenting with RWAs by tokenizing various traditional financial instruments—such as equity funds and government bonds—to meet institutional client demand. Although these efforts remain in early stages, the entry of traditional financial firms into RWA issuance holds catalytic potential to attract vast numbers of new users who have never previously engaged with blockchain technology.

Growth of Yield-Bearing RWAs

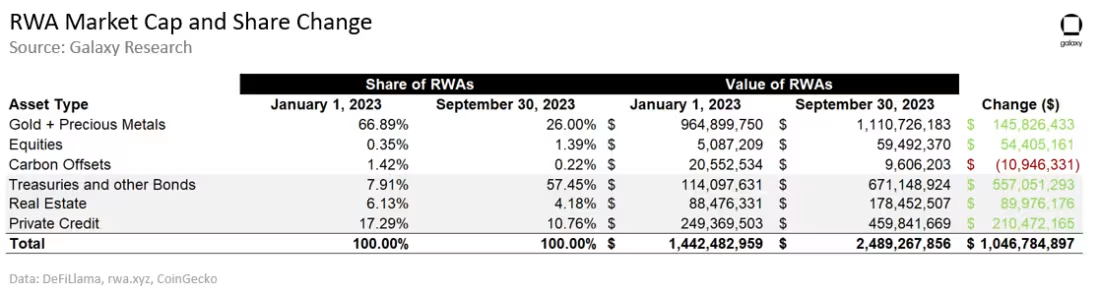

As of September 30, the RWA market cap reached $2.49 billion, down 9.6% from its peak of $2.75 billion on April 19. Despite strong growth in Treasury-related RWAs, a significant decline in active lending by private credit issuers over the past 18 months has kept overall RWA market cap below historical highs.

From January 31 to September 30, non-stablecoin RWA value grew by $1.05 billion. Of this, $855.7 million in new growth over the past three quarters came from government bonds and other debt securities, real estate, and private credit.

Private Credit

Private credit is a form of lending where financing is provided by non-bank institutions. Since the 2008 financial crisis, increasing bank regulations have driven substantial growth in the private credit market as borrowers seek alternative sources of capital. This trend has accelerated further in the current interest rate cycle, as bank balance sheets face particular constraints—as evidenced by bank failures earlier this year. Private credit solutions benefit both borrowers and lenders. They offer borrowers greater flexibility than traditional bank loans, while floating interest rates provide lenders protection against rate fluctuations unavailable in fixed-rate alternatives. As of August 2023, the global private credit loan market was valued at $1.5 trillion.

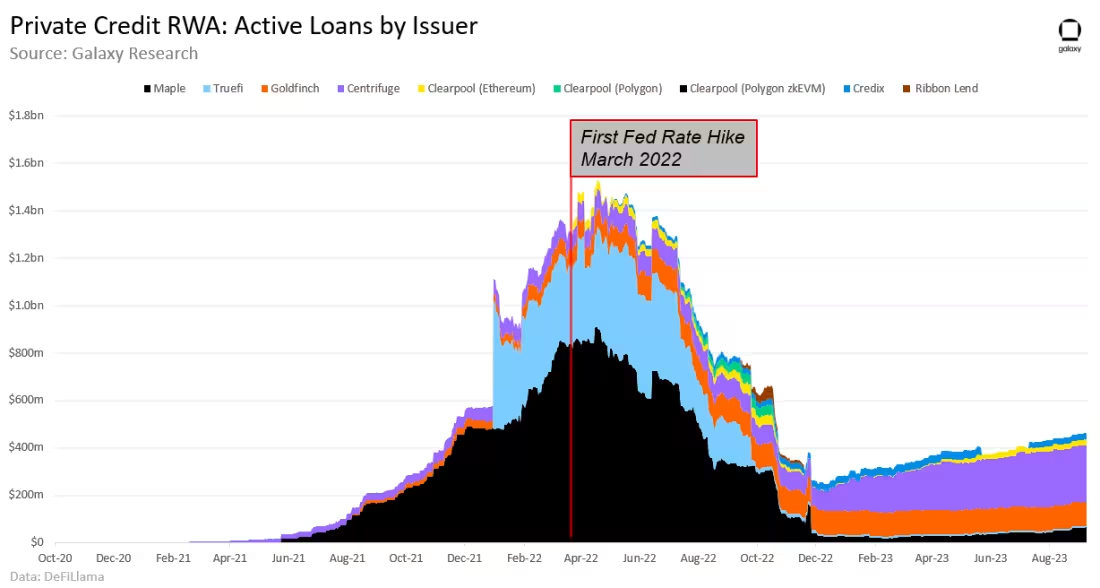

From January 1 to September 30, the outstanding value of on-chain private credit loans increased by $210.5 million (84% growth). The majority of this growth (74%) came from Centrifuge, whose outstanding loan balance rose by $155.7 million. Clearpool, a decentralized credit marketplace, experienced the largest relative change over the past three quarters. From January 1 to September 30, the platform’s loan balance surged 966%, reaching $23.96 million by September 30. Throughout its history, Clearpool has cumulatively issued over $400 million in private credit loans across three blockchains: Polygon, Polygon zkEVM, and Ethereum.

Despite growth in 2023, the total value of on-chain represented private credit loans remains 70% lower than the all-time high of $1.54 billion reached in May 2022. Aggressive Federal Reserve rate hikes led to a sharp contraction in active loans, with yields rising within nine months after the first hike in March 2022.

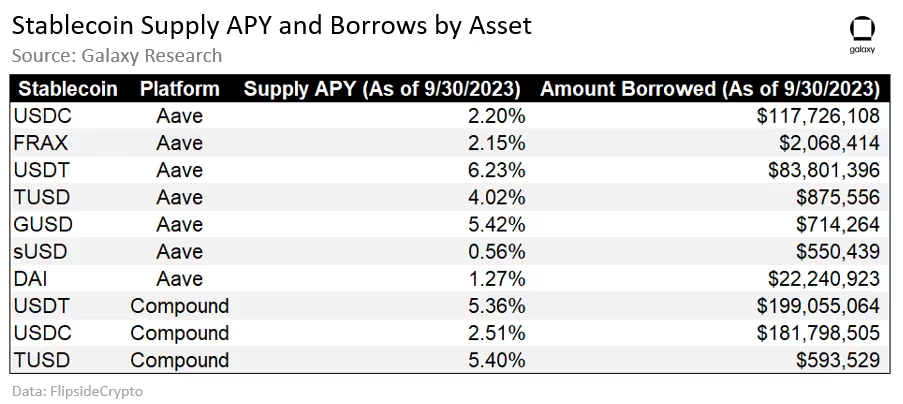

Yields available to users depositing stablecoins into on-chain private credit loans are significantly higher than those earned through stablecoin deposits on DeFi lending protocols such as Aave and Compound. From January 1 to September 30, the average daily yield spread between tokenized on-chain private credit loans and the weighted average supply rate of stablecoins on Aave and Compound was 7.7%. Stablecoin deposit rates were calculated using the weighted average of borrow amounts for the following assets on Aave and Compound:

It should be noted that depositing stablecoins into decentralized lending protocols such as Aave and Compound carries different risk profiles compared to investing in tokenized real-world private credit loans via platforms like Centrifuge and Clearpool. While most loans on decentralized lending protocols are overcollateralized, tokenized private credit loans may not be.

Real Estate

Real estate is a tangible asset class comprising properties such as residential homes, commercial buildings, and land. It is particularly attractive to investors due to its potential to generate positive cash flow through passive income streams like rental payments. In 2023, real estate became the world's largest asset class, valued at approximately $613 trillion.

Among all yield-bearing RWA categories covered in this report, on-chain real estate saw the smallest dollar-denominated growth. From January 1 to September 30, the total value of these tokenized assets stood at $178 million, representing fractional ownership stakes in real estate in some cases. RealT tokens are the largest issuer of tokenized real estate, holding 49% market share. Tangible is another real estate-focused RWA issuer that demonstrated the strongest growth this year. Total value locked (TVL) in Tangible tokens grew from $100,000 to $64 million during the first three quarters of 2023.

Government Bonds and Other Debt Securities

U.S. Treasury securities are debt instruments backed by the government. They are widely regarded as the safest and most reliable type of yield-bearing asset—the so-called “risk-free” benchmark (though clearly, the risk lies in potential U.S. government default). In contrast, corporate bonds are debt securities issued by companies, offering potentially higher yields but also carrying greater risk than Treasuries. In 2022, the global bond market was valued at $133 trillion, with U.S. corporations alone issuing $1.02 trillion in corporate bonds during the first three quarters of 2023.

The value of tokenized Treasuries and other bonds grew by $557.05 million from January 1 to September 30. Ondo Finance, Franklin Templeton, and Matrixdock are the top three Treasury RWA issuers. Together, they issued $572.05 million in assets (accounting for 85% of the tokenized Treasury and other bond category) and launched $468.5 million in Treasury RWA offerings this year.

Frigg.eco differs from other issuers in this category by issuing bonds tied to sustainable infrastructure developers. These instruments resemble corporate bonds more closely than the Treasury-backed RWAs issued by others. Frigg.eco’s bonds allow token holders to earn returns by funding development projects and enable developers to issue debt to finance their initiatives.

Another approximately $1.8 billion worth of tokenized treasury assets comes from stUSDT. stUSDT was the first RWA project launched on the TRON blockchain. Recently, this asset has faced criticism for lacking transparency regarding its backing and yield sources.

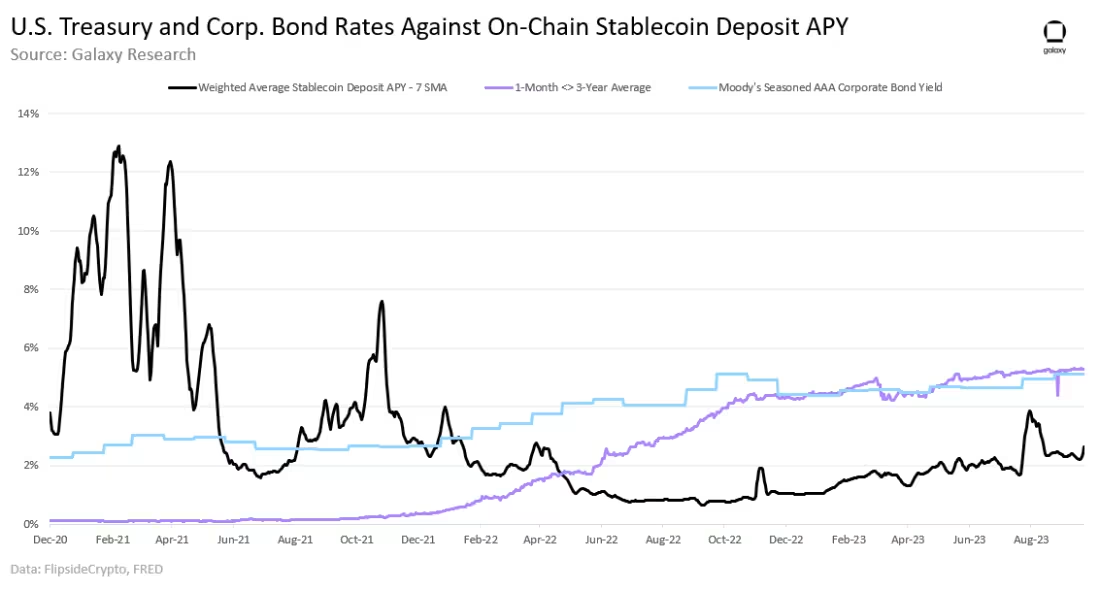

For nearly 18 months, the average yield on U.S. Treasuries with maturities under three years—the most widely adopted duration on-chain—has exceeded the average yield on stablecoin deposits. In 2023, the average daily yield spread between these Treasuries and the weighted average stablecoin rate on Aave and Compound was approximately 3% (Treasury yield minus on-chain rate). By comparison, the average yield spread between Moody’s AAA-rated corporate bonds and on-chain stablecoin rates was 2.7% (corporate bond yield minus on-chain rate).

Outlook

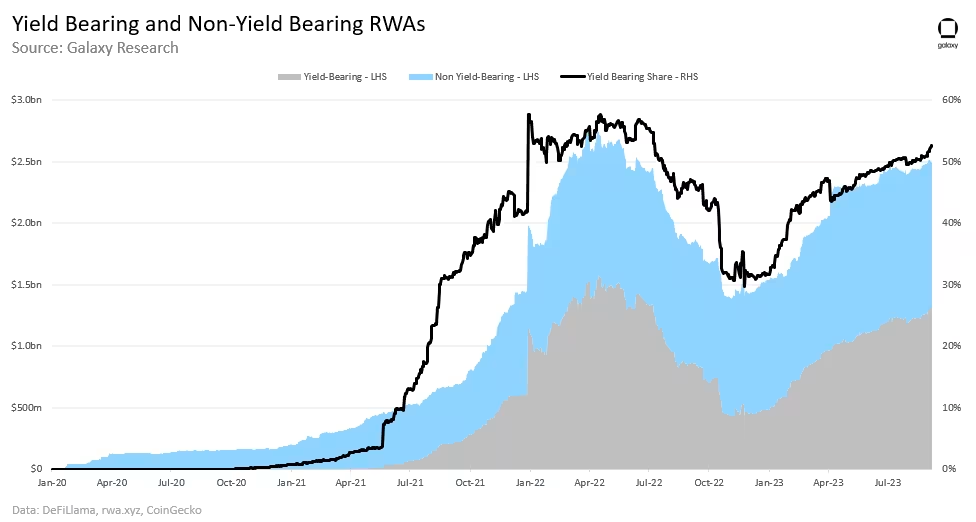

Demand for yield among native crypto users has driven the growth of on-chain RWAs. Approximately 82% of the new value created in the RWA space this year came from yield-bearing RWAs such as tokenized private credit, real estate, and government bonds. Within total RWA market cap, the share of yield-bearing RWAs nearly doubled—from 31% on January 1 to 53% on September 30—approaching the all-time high of 57% (just 4 percentage points away). This compares to non-yielding RWAs such as gold, equities, and carbon offsets.

Between 2021 and 2023, aggressive shifts in Federal Reserve monetary policy pushed benchmark interest rates to levels unseen since 2007. This created new demand from RWA-native decentralized finance users seeking higher yields.

Most RWA Users Are Crypto-Native

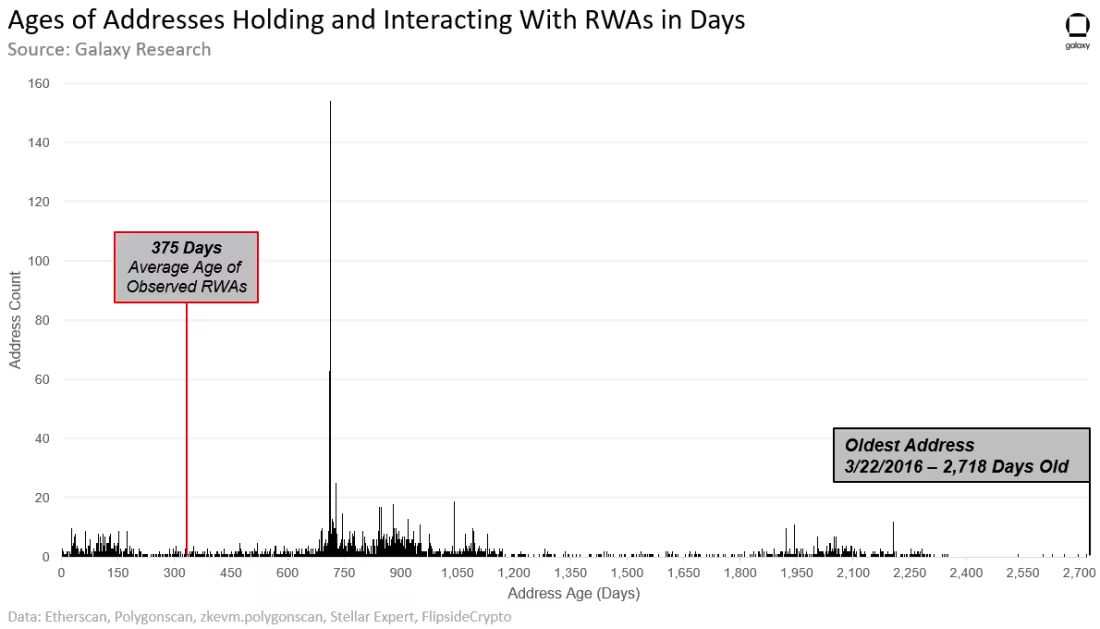

The majority of on-chain RWA demand comes from a small group of crypto-native users, rather than new crypto adopters or traditional investors. The fact that the average user address interacting with RWA tokens was created before the assets themselves went live on-chain underscores that typical RWA holders have been active in blockchain ecosystems for some time.

The chart below shows the age distribution of unique user addresses holding RWA tokens issued by the following companies and protocols. The ticker symbols for these assets are listed below (in parentheses). Together, these assets account for nearly 70% of yield-bearing RWA TVL:

-

Ondo (OUSG)

-

Matrixdock (STBT)

-

Maple (MPLcashUSDT and MPLcashUSDC)

-

OpenEden (TBILL)

-

Backed (bIB01 and bIBTA)

-

Arca Labs (RCOIN)

-

WisdomTree (WSTY)

-

Swarm (TBONDS13 and TBONDS01)

-

Stream Finance (US4W)

-

Bloom (TBY-Feb1924, TBY-Mar24(a), and TBY-Mar24(b))

-

Franklin Templeton (FOBXX)

Note: The snapshot of holders of these assets was taken on August 31, 2023. Therefore, address age is calculated as the number of days between an address’s first on-chain transaction and August 31, 2023. Addresses holding multiple RWAs are counted once. Multiple addresses determined to be controlled by a single user are also counted once, using the earliest transaction date. Data tracks address ages across all chains where these assets were issued: Ethereum, Stellar, and Polygon. The following data also includes user address ages for tokenized representations of private credit issued by these three protocols:

-

Clearpool on Ethereum and Polygon zkEVM

-

Maple on Ethereum

-

Goldfinch

As of August 31, 2023, there were 3,232 unique addresses holding RWA assets issued by the companies and protocols listed above. The average age of addresses interacting with or holding RWAs was 882 days, or 2.42 years—indicating that the average address has been active on-chain since April 2021. In contrast, the average age of RWA assets was 375 days. For tokenized treasury assets, RWA age is calculated as the number of days from the first token mint date to August 31, 2023. For assets issued by private credit platforms like Clearpool, Maple, and Goldfinch, asset age is based on the number of days from protocol launch to August 31, 2023. Using protocol launch date as the starting point for private credit RWA age accounts for the rolling nature of on-chain private credit (i.e., loans maturing/pools closing, new loans opening).

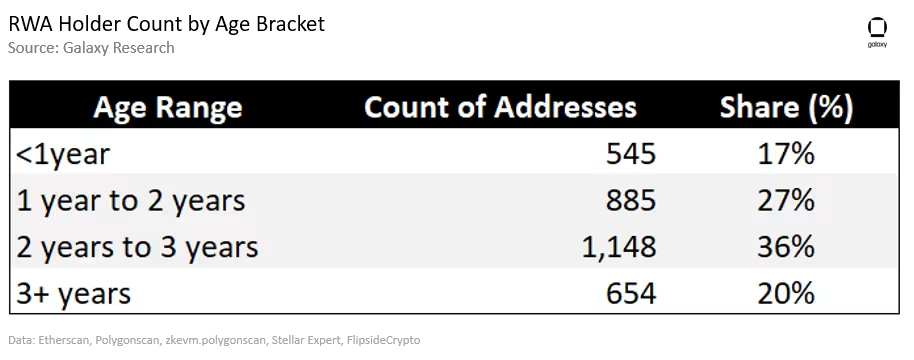

Twenty percent of addresses that interacted with or held the above RWAs began conducting on-chain transactions in 2023 or more than three years before RWAs emerged on-chain. The table below summarizes the age ranges of user addresses holding RWAs as of August 31, 2023:

Many of the RWA holders highlighted above who executed their first transaction less than a year ago are holders of assets issued by Franklin Templeton and WisdomTree (34%, or 188 addresses), suggesting that RWA products created by established financial firms may be successfully attracting new user segments into crypto—although the majority of RWA users still appear to be crypto-native.

RWAs Carry Real-World Risks and Limitations

Although many RWAs are issued on public blockchains, they do not grant users frictionless access to financial products and services. In most cases, users interacting with RWAs on-chain must complete KYC/AML checks or whitelisting, undergo credit verification, and may need to meet minimum balance requirements to mint, purchase, deposit, or redeem RWAs. RWAs are subject to similar—or in some cases even stricter—restrictions than their traditional financial counterparts. This means that RWAs do not meaningfully expand access to financial tools by enabling individuals to participate in financial activities otherwise unavailable to them.

Furthermore, RWAs carry unique risks beyond the technical risks associated with all on-chain applications and services. For example, because private credit loans in traditional finance can sometimes be unsecured, their tokenized representations must reflect this reality. If an off-chain borrower defaults on a loan, on-chain depositors could lose funds. To mitigate such risks, RWA private credit issuers must find ways to position assets appropriately—through risk-return spectrum allocation and transparent governance processes conducted by decentralized autonomous organizations (DAOs) when reviewing new loans.

Federal Reserve Policy Is Critical

Federal Reserve actions have significantly influenced RWA adoption this year. As interest rates rose, off-chain yields became more attractive to on-chain users. Moreover, the most valuable types of RWAs shifted as rates increased. For instance, in Q2 2022, private credit-backed RWAs accounted for 56% of total RWA TVL, while Treasury-backed RWAs accounted for 0%. In Q3 2023, private credit-backed RWAs’ share of total RWA TVL declined to 18%, while Treasury-backed RWAs rose to 27%. Federal Reserve policy remains a key driver shaping the expansion and structure of the RWA DeFi landscape.

Conclusion

The growth of RWAs and the introduction of new RWA types on-chain are primarily driven by demand from crypto-native users, not new crypto adopters. However, the adoption of RWAs by major traditional financial firms such as Franklin Templeton and WisdomTree signals the potential of this emerging DeFi sector to attract future new users. RWAs gained strong momentum in 2023, with market caps of many such assets trending toward new all-time highs. Shifting macroeconomic conditions will continue to shape the evolution of this space, as will sustained demand from both native and non-native crypto users for these assets.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News