Deep Dive into the Implementation Path of RWA and Exploring the Future Development Logic of RWA-Fi

TechFlow Selected TechFlow Selected

Deep Dive into the Implementation Path of RWA and Exploring the Future Development Logic of RWA-Fi

RWA Mapping income-generating assets onto the blockchain is only the first step; how to subsequently leverage DeFi's composable Lego-like architecture will be well worth exploring, potentially further unlocking the ceiling of RWA+DeFi.

Authors: Will Wang, Web3 lawyer; Diane Cheung, Web3 practitioner

With the onset of the 2022 crypto winter and a wave of CEX collapses amid tightening regulations, the once sky-high APRs in the crypto market have vanished. Surviving investors are now turning their attention to risk-free yield opportunities. Coinciding with shifts in the macroeconomic environment and rising U.S. Treasury yields, tokenization of real-world assets (Real World Asset Tokenization) has emerged as a key value-capture channel in today’s crypto markets.

This article analyzes the implementation paths of major RWA projects—Compound & Superstate, Franklin Templeton, MakerDAO, Ondo Finance, Matrixdock, and Centrifuge—to clarify the current logic behind the RWA narrative.

TL;DR

-

Debating the definition of RWA is not particularly meaningful. Tokens are carriers of value—the true value of RWA depends on which rights or values of the underlying assets are brought on-chain and how they are applied;

-

In the short term, the driving force behind RWA comes primarily from unilateral demands within the DeFi ecosystem, such as asset management, portfolio diversification, and new asset classes;

-

DeFi protocols capture the yield-generating potential of underlying assets through RWA projects, effectively creating a USD-denominated asset class backed by real yields from those assets—a logic nearly identical to LSD protocols creating ETH-denominated yield-bearing assets;

-

As a result, U.S. Treasury-based RWAs have gained popularity. Depending on how Treasury yields are realized, these fall into two categories: (1) Off-Chain to On-Chain via traditional compliant funds, and (2) On-Chain to Off-Chain led by DeFi protocols—though significant regulatory hurdles remain;

-

Mapping income-generating assets onto the blockchain is just the first step. The real potential lies in integrating them into DeFi's composable "Lego" ecosystem, which could dramatically expand the ceiling for RWA+DeFi;

-

In the long run, RWA should not be one-directional. The future will involve mutual integration: bringing real-world assets on-chain while enabling TradFi to leverage DeFi’s advantages to unlock further potential;

-

Future exploration should focus on how investors can simultaneously benefit from both the beta returns of real-world RWA assets and the alpha returns of the crypto market.

1. The Current RWA Narrative

For today’s $1 trillion crypto market, investor returns largely stem from on-chain activities (e.g., trading, lending, staking, derivatives). The entire market lacks a stable source of real yield.

Since Ethereum’s transition to POS, liquid staking derivatives (LSD) based on ETH represent a native form of real yield in crypto. However, this segment still constitutes only a small portion of the overall market. To truly break through existing limitations, external forces must provide stronger support.

A new source of real yield is now emerging: real-world assets (RWAs), existing off-chain, are being tokenized and brought on-chain, offering a vital source of real yield for the crypto market denominated in USD.

The onboarding of RWAs could be transformative for crypto. RWAs provide sustainable, diverse, and traditionally backed real yields. Furthermore, they bridge decentralized finance (DeFi) and traditional finance (TradFi), meaning RWAs not only bring incremental capital into crypto but also access vast liquidity, broader market opportunities, and immense value capture from traditional financial markets.

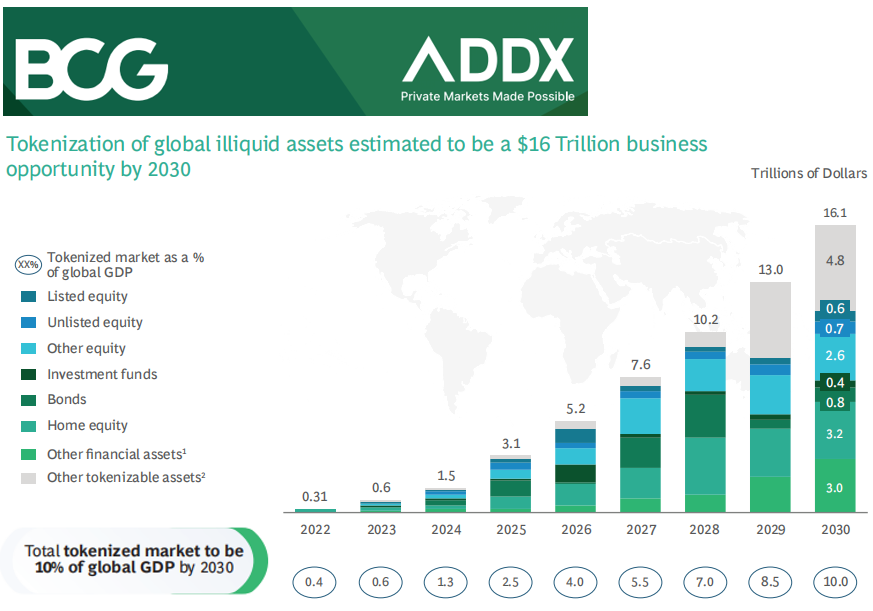

According to research by BCG and ADDX, the global tokenization of illiquid assets could create a $16 trillion market—nearly 10% of the projected global GDP in 2030. Citigroup’s RWA report, “Money, Tokens, and Games,” estimates that $10 trillion worth of assets will be tokenized by 2023.

1.1 What Is RWA?

RWA stands for Real World Asset Tokenization—the process of converting the value of rights (such as ownership, income rights, or usage rights) in tangible or intangible assets into digital tokens. This enables asset storage and transfer without central intermediaries, mapping value onto blockchains for trading and circulation.

RWA can represent many types of traditional assets—both tangible and intangible—including commercial real estate, bonds, automobiles, and virtually any asset whose stored value can be tokenized. Since the early days of blockchain technology, market participants have sought to bring RWAs on-chain. Traditional financial institutions like Goldman Sachs, Hamilton Lane, Siemens, and KKR are actively working to tokenize their real-world assets. Meanwhile, native crypto DeFi protocols such as MakerDAO and Aave are adapting to embrace RWA.

Compared to the narrow fundraising-focused ICO/STO (Security Token Offering) narratives of 2018, today’s RWA narrative is far broader—not limited to TradFi primary markets, almost any asset capable of value representation can now be tokenized. Moreover, unlike in 2018, today’s robust DeFi protocols and infrastructure open up endless possibilities for RWA.

1.2 Drivers Behind RWA

Currently, the main driver behind bringing real-world assets into crypto is the ability of these assets—especially U.S. Treasuries—to offer a stable, risk-free yield in the prevailing macro environment.

Thus, most mature RWA implementations today stem from unilateral demand within DeFi protocols, including:

-

Asset Management Needs: Native on-chain yields come from staking, trading, and lending. However, during the crypto winter, declining on-chain activity has reduced on-chain yields. With U.S. Treasuries now offering higher yields, established DeFi protocols are gradually incorporating Treasury-based RWAs. For example, MakerDAO recently passed proposals to shift its treasury holdings from low- or zero-yield stablecoins to yield-bearing U.S. Treasury RWAs (offering 4%-5% risk-free returns), ensuring treasury safety while generating steady income;

-

Portfolio Diversification: During extreme market conditions, high volatility and correlation among native crypto assets often lead to mismatches and liquidations. Introducing stable, low-correlation RWA assets helps mitigate these risks. Investors can achieve diversification and build more resilient, effective portfolios;

-

New Asset Classes: Integrating RWA with DeFi "Lego" components unlocks further potential. For instance, Flux Finance offers lending against Ondo Finance’s OUSG, Curve allows trading of MatrixDock’s STBT, and Pendle provides AMM pools for yield-bearing assets.

In the short term, this demand is driven solely by crypto’s one-way pursuit of TradFi. Traditional finance shows little interest in entering crypto, with only tentative explorations so far. In the long run, however, RWA should not be one-sided—as it currently is, driven mainly by DeFi’s demand for TradFi. The future lies in mutual integration: bringing real-world assets on-chain while enabling TradFi to harness blockchain’s technological advantages to unlock further potential.

1.3 Capturing Value from RWA Underlying Assets

RWA classifications vary widely depending on the nature of the underlying assets.

In the short term, we narrowly categorize RWA into “yield-bearing RWA” and “non-yield-bearing RWA.” We believe most current RWA projects primarily aim to capture yield value from income-generating assets such as U.S. Treasuries, government securities, corporate bonds, and REITs.

Yield-bearing RWA essentially creates a USD-denominated asset class backed by real yields from the underlying assets—mirroring the logic of LSD protocols creating ETH-denominated yield-bearing assets. While RWA yields may be modest, they can be further composited within DeFi ecosystems.

Non-yield-bearing RWA is better suited to capturing intrinsic commodity value—such as gold, crude oil, collectibles, artworks, or even the tokenized valuation of South American athletes’ market worth.

2. RWA On-Chain Implementation Paths

According to Binance Research, the RWA implementation process consists of three stages: (1) Off-chain formalization; (2) Information bridging; (3) RWA protocol supply and demand.

2.1 Off-Chain Formalization

To bring real-world assets into DeFi, they must first be packaged off-chain—digitized, financialized, and made compliant—to clearly define asset value, ownership, and legal protections for rights.

Key considerations include:

(1) Representation of Economic Value: The asset’s economic value can be represented by its fair market value in traditional finance, recent performance data, physical condition, or other economic indicators.

(2) Ownership & Legitimacy of Title: Ownership can be verified through deeds, mortgages, promissory notes, or other legal instruments.

(3) Legal Backing: Clear procedures must exist for resolving disputes over ownership or rights changes, typically involving asset liquidation, dispute resolution, and specific legal enforcement processes.

2.2 Information Bridging

Next, information about the asset’s economic value, ownership, and rights is digitized and brought on-chain, stored in blockchain’s distributed ledger.

This stage involves:

(1) Tokenization: After off-chain packaging, the information is digitized, brought on-chain, and represented as metadata within digital tokens. This metadata is accessible via blockchain, making asset value, ownership, and rights fully transparent. Different asset classes may map to different DeFi protocol standards.

(2) Regulatory Technology / Securitization: For regulated or securities-like assets, compliant mechanisms integrate them into DeFi. These include licenses for issuing security tokens, KYC/AML/CTF checks, and exchange listing compliance.

(3) Oracles: RWAs require real-world external data to accurately reflect asset value—for example, stock RWAs need access to stock performance data. Since blockchains cannot directly pull external data, oracles like Chainlink bridge off-chain data to DeFi protocols, providing asset valuations and other metrics.

2.3 RWA Protocol Supply and Demand

DeFi protocols focused on RWA drive the entire tokenization process. On the supply side, DeFi protocols oversee RWA formation. On the demand side, they facilitate investor demand for RWAs. Thus, most specialized RWA DeFi protocols serve both as originators and marketplaces for RWA products.

2.4 Specific RWA Implementation Approaches

In implementing RWA on-chain, approaches resemble securitization—using Special Purpose Vehicles (SPVs) to hold underlying assets, providing control, management, and risk isolation. Additionally, the BCG and ADDX report provides a roadmap from the asset originator’s perspective, outlining roles for various ecosystem participants (originators, issuance platforms, custodians, settlement agents, etc.):

3. Current Implementation Paths for U.S. Treasury RWAs

Having established that RWA represents the tokenization of off-chain real-world assets, understanding how asset rights and values translate between the real world and crypto is crucial—how RWA becomes a legally valid representation of real-world assets, or how real-world assets are mapped onto blockchains.

By examining the most mature RWA use case—U.S. Treasuries—we identify two main paths: (1) Off-Chain to On-Chain, led by traditional compliant funds, and (2) On-Chain to Off-Chain, driven by DeFi protocols. Given that current RWA momentum stems primarily from crypto, DeFi-led initiatives are more advanced.

Currently, except for T protocol (a permissionless protocol), all other projects implement strict KYC/AML procedures for compliance. Most U.S. Treasury RWA projects do not support transferability, limiting their use cases and leaving room for further exploration.

3.1 Off-Chain to On-Chain (Traditional Finance)

3.1.1 Superstate by Compound’s Founder

Robert Leshner, founder of Compound, targeting the trending RWA narrative, announced the launch of his new company Superstate on June 28, 2023, aiming to bring regulated traditional financial products on-chain.

According to filings with the U.S. Securities and Exchange Commission (SEC), Superstate will use Ethereum as a supplementary accounting tool and launch funds investing in short-term government bonds, including U.S. Treasuries and agency securities. However, the filing explicitly states the fund will not directly or indirectly invest in any blockchain-dependent assets such as cryptocurrencies (“The Fund will not directly or indirectly invest in any assets that rely on blockchain technology, such as cryptocurrencies”).

In short, Superstate will establish SEC-compliant off-chain funds investing in short-term U.S. Treasuries, using Ethereum to handle fund transactions and record ownership shares. Superstate requires investors to be whitelisted and will not whitelist smart contracts from platforms like Uniswap or Compound, preventing such DeFi applications from interacting with it.

In a statement to Blockworks, Superstate said: “We are creating an SEC-registered investment product that will allow investors to obtain a record of your ownership of this mutual fund, similar to holding stablecoins or other crypto assets.”

3.1.2 Franklin OnChain U.S. Government Money Fund

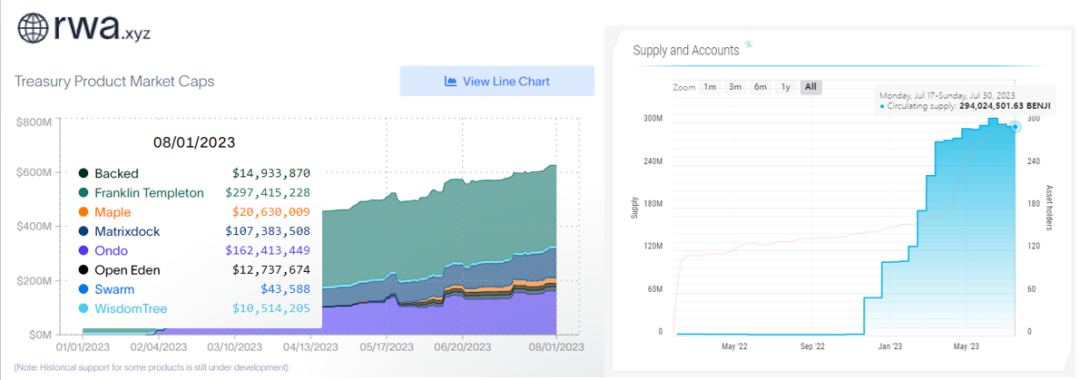

Before Superstate, Franklin Templeton launched the Franklin OnChain U.S. Government Money Fund (FOBXX) in 2021—the first SEC-approved fund using blockchain (Stellar) for transaction processing and ownership tracking. As of now, it manages over $29 billion in assets under management (AUM), offering investors a 4.88% annualized return.

Although each fund share is represented by one BENJI token, there is currently no visible interaction between BENJI tokens and DeFi protocols on-chain. Investors must undergo compliance verification via Franklin Templeton’s app or website to join the whitelist.

3.1.3 Hamilton Lane’s Private Equity Fund Tokenization

Hamilton Lane, a leading global investment firm managing $823.9 billion in assets, has tokenized portions of three of its funds on the Polygon network, making them available to investors via the Securitize trading platform. Through collaboration with Securitize, fund shares form a feeder fund managed by Securitize Capital.

Securitize’s CEO stated: “Hamilton Lane offers some of the top-performing private market products, historically limited to institutional investors. Tokenization enables individual investors to digitally participate in private equity for the first time and co-create value.”

From an individual investor’s perspective, while tokenized funds offer affordable access to elite private equity—lowering minimum investments from an average of $5 million to just $20,000—investors still must pass accredited investor verification via Securitize, maintaining certain barriers.

From a private fund’s standpoint, tokenization clearly offers real-time liquidity advantages (compared to traditional PE lockups of 7–10 years), diversified LP bases, and greater capital deployment flexibility.

3.1.4 Summary

The Off-Chain to On-Chain path reflects innovation by traditional finance within its compliance framework. Given the heavy regulation in TradFi, current efforts merely apply blockchain as an accounting layer for traditional financial products, rather than directly connecting to DeFi. Still, the ownership records ("a record of your ownership of this mutual fund") are functionally equivalent to tokens—imagine the difference between such records and stablecoins.

We look forward to Robert Leshner, Compound’s founder, bringing deeper value exploration to the Off-Chain to On-Chain RWA path from a more crypto-native/DeFi-oriented perspective.

3.2 On-Chain to Off-Chain (Crypto Finance)

3.2.1 MakerDAO’s Monetalis Trust Legal Structure

MakerDAO is a decentralized autonomous organization (DAO) managing the Maker protocol on Ethereum. The protocol introduced DAI, the first decentralized stablecoin (essentially a dollar on Ethereum), along with a suite of derivative financial tools. Since launching in 2017, DAI has maintained its peg to the U.S. dollar.

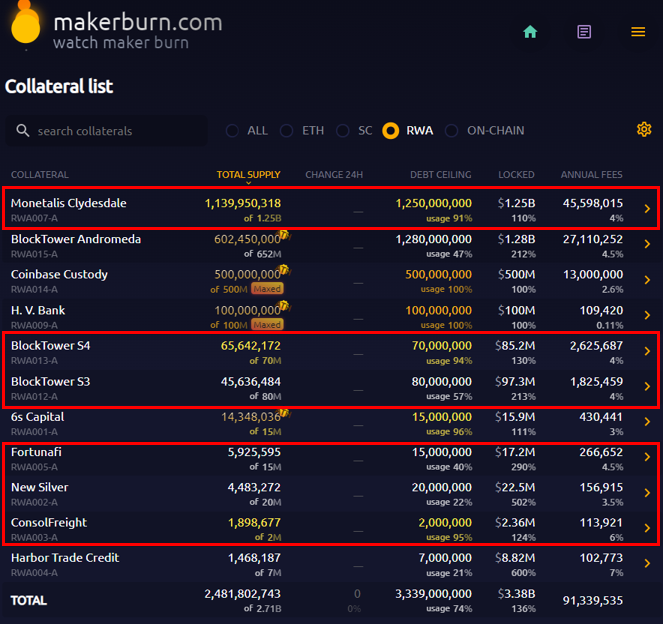

Due to the high volatility of crypto markets, relying on a single collateral type risks mass liquidations. Hence, MakerDAO has long explored collateral diversification, with RWA playing a key role. After years of experimentation, MakerDAO has established two mature RWA pathways: (1) Direct purchase and holding of assets via DAO + trust structures (MIP65 proposal); (2) Direct purchase of tokenized RWA assets through decentralized lending platforms like Centrifuge, including current holdings such as New Silver (real estate loans) and BlockTower (structured credit) vaults.

According to MakerBurn.com, 11 RWA-related projects currently serve as collateral for MakerDAO, totaling $2.7 billion in TVL.

Consider MIP65: Monetalis Clydesdale: Liquid Bond Strategy & Execution. Proposed in January 2022 by Allan Pedersen, founder of Monetalis, this initiative aims to allocate part of MakerDAO’s treasury stablecoins into highly liquid, low-risk real-world bond assets via a trust managed by Monetalis. Approved by MakerDAO community vote, implementation began in October 2022 with an initial debt ceiling of $500 million, raised to $1.25 billion in May 2023.

Under MIP65, MakerDAO delegates Monetalis as the executor, responsible for designing the legal structure and periodic reporting. Monetalis designed a trust legal framework under British Virgin Islands (BVI) law to unify on-chain governance (MakerDAO), off-chain governance (trustee resolutions), and off-chain execution (off-chain trades).

First, MakerDAO and Monetalis appoint a Transaction Administrator to review all transactions, ensuring alignment with MakerDAO proposals. Second, MakerDAO’s on-chain proposals become prerequisites for off-chain entity decisions—any matters outside MakerDAO’s resolutions fall outside the off-chain entity’s authority. Finally, leveraging BVI law’s flexibility ensures coherence between on-chain governance and off-chain governance/execution. The resulting arrangement is illustrated below:

After aligning on-chain and off-chain governance and execution, James Assets (PTC) Limited, a BVI-based trust company, executes purchases of U.S. Treasury ETFs. Purchases include BlackRock’s iShares US$ Treasury Bond 0-1 yr UCITS ETF and iShares US$ Treasury Bond 1-3 yr UCITS ETF. The full process is shown below:

Throughout, James Assets (PTC) Limited acts as the external agent for MakerDAO and Monetalis, executing transactions upon receiving both on-chain and off-chain authorization. Coinbase serves as the fiat on/off-ramp, Sygnum Bank handles trust asset trading and custody, and a separate account covers operational expenses (initial setup costs reaching $950,000).

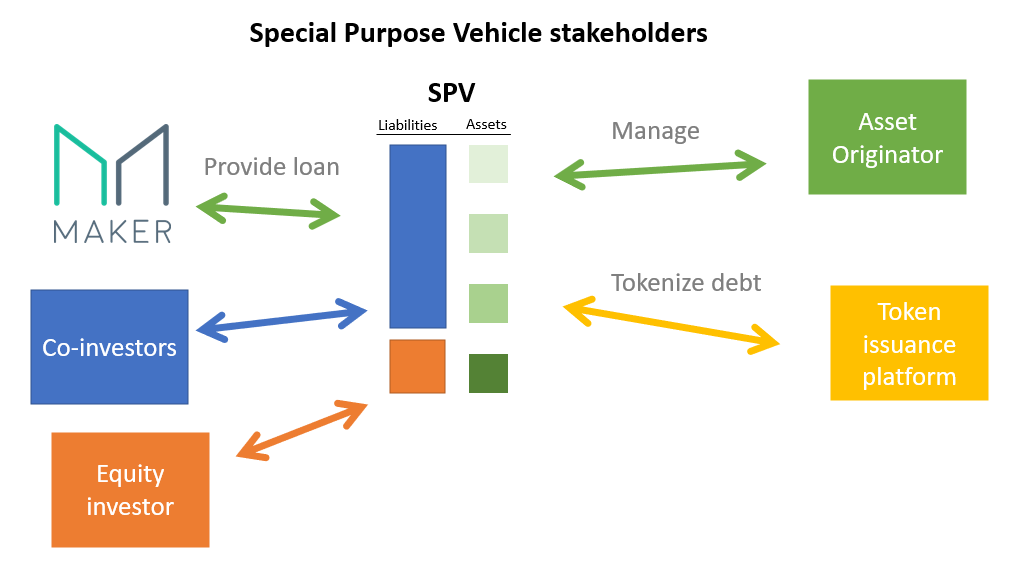

3.2.2 Centrifuge’s SPV Tokenization Path

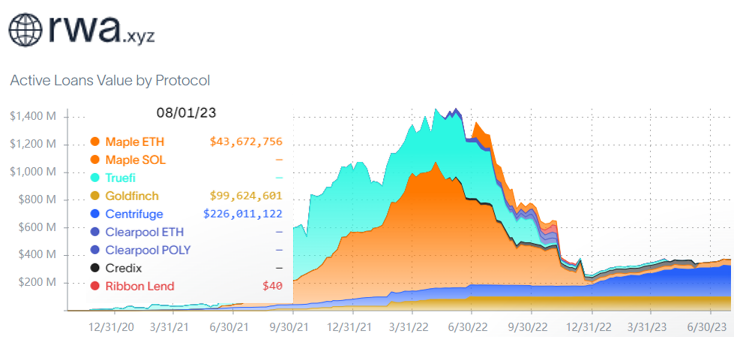

Centrifuge is a decentralized lending platform dedicated to bringing real-world assets into crypto through tokenization, fractionalization, and structuring to unlock new investment opportunities and liquidity. One of the earliest DeFi protocols in the RWA space, Centrifuge also powers major protocols like MakerDAO and Aave. According to rwa.xyz, Centrifuge operates comprehensively in RWA, with its own Centrifuge Chain and flagship Tinlake protocol.

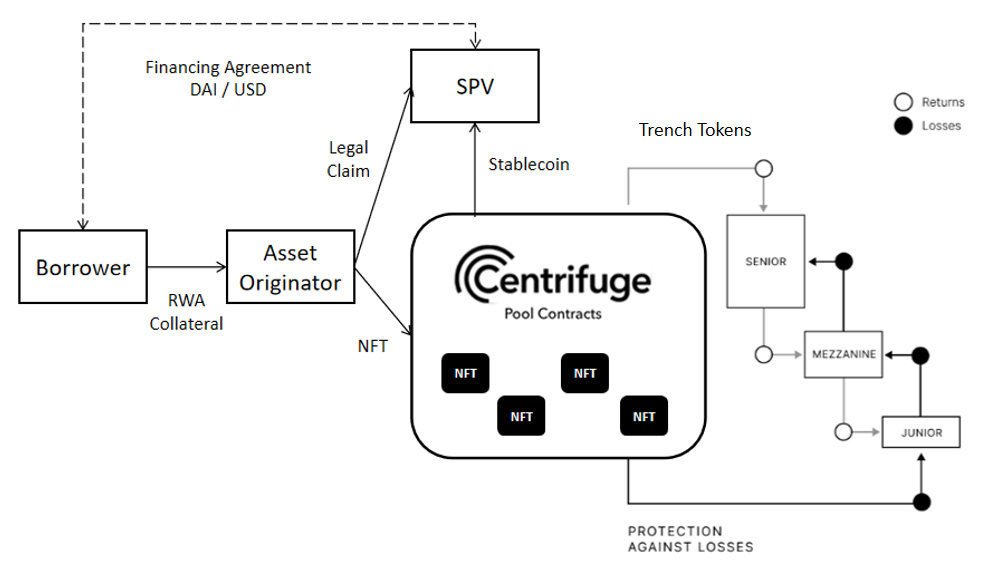

Centrifuge’s RWA implementation can be summarized as: (1) Borrowers, via asset originators (underwriters), tokenize off-chain assets as NFTs locked in Centrifuge’s smart contract pools; (2) Pool multiple borrowers’ NFTs of the same type, funded collectively by liquidity providers rather than individually; (3) Structure the pool into Junior and Senior tranches (represented by different ERC20 tokens), where Junior tranche investors accept higher risk for higher returns, while Senior tranche investors accept lower risk and returns—catering to varying risk appetites.

Centrifuge has done extensive compliance work based on U.S. securitization law (Reg D 506(b)(c) under the U.S. Securities Act), continuously improving. For example, Centrifuge partners with Securitize to complete KYC/AML checks; every asset originator on Centrifuge must establish a corresponding independent legal entity—an SPV—that provides bankruptcy remoteness. Legally, assets are sold to the SPV, protecting investor interests even if the originator goes bankrupt. Investors sign investment agreements with the SPV detailing structure, risks, terms, then purchase DROP or TIN tokens representing different tranches using DAI.

MakerDAO issued its first RWA002 Vault with New Silver on Centrifuge in February 2021. Later larger-scale vaults like BlockTower S4 (RWA013-A) and BlockTower S3 (RWA012-A) followed this path, with BlockTower S4 primarily backed by consumer loan ABS products.

Subsequently, MIP6 improved Centrifuge’s RWA model by introducing a Trustee and LockBox mechanism. MakerDAO believed this structure better protects investors and the DAO. Key improvements include:

1. The asset issuer appoints a third-party Trustee to act on behalf of the DAO and investors. The Trustee safeguards DAO interests and asset independence. In default scenarios, the Trustee manages and distributes assets, removing control from issuers or liquidators;

2. Introduction of a LockBox—an isolated account holding assets outside the issuer’s and SPV’s control. This means SPV assets are controlled by the Trustee, who receives and processes payments into the LockBox, ensuring correct disbursement (e.g., to MakerDAO). This removes the issuer’s control over cash flows from borrowers to MakerDAO’s reserves, reducing risks of fund loss or misuse.

In this enhanced model: underlying assets are sold to the SPV, which pledges them to the Trustee. The SPV then issues DROP and TIN tokens to MakerDAO via the Tinlake protocol. When cash flows occur, payments go directly to a segregated LockBox account independent of both SPV and MakerDAO. Upon receipt, the Trustee instructs the LockBox to pay DROP and TIN holders, which Tinlake then executes.

Notably, neither MakerDAO nor the SPV ever touches the DAI or USD cash flows—all are processed through LockBox and Tinlake. Their sole roles are signing subscription agreements and acting as token holders making governance decisions.

This structure better protects investors and issuers from litigation risks and provides a consistent framework for discussions with regulators, custodian banks, and other third-party service providers. Once widely accepted across the industry and embraced by traditional finance players, this model could more easily onboard TradFi participants into DeFi, expanding the types and scale of RWAs available to MakerDAO and reducing DAI’s volatility.

3.2.3 Ondo Finance’s Exemption Path & Flux Finance (DeFi Lending Protocol)

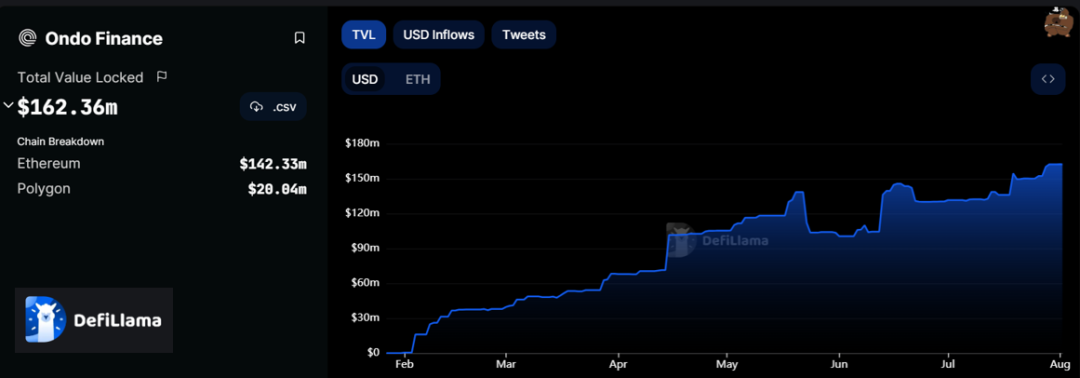

Launched in January 2023, Ondo Finance offers tokenized funds aimed at providing institutional-grade investment opportunities for professional on-chain investors. It brings low- or no-risk rate funds on-chain, allowing stablecoin holders to invest in government and U.S. Treasury bonds. Concurrently, Ondo collaborates with DeFi lending protocol Flux Finance to enable OUSG token holders to borrow stablecoins like USDC and DAI on-chain.

According to DeFiLlama, as of August 1, Ondo Finance’s TVL reached $162 million, with its lending protocol Flux Finance achieving $42.78 million in TVL and $2.802 billion in borrowing volume.

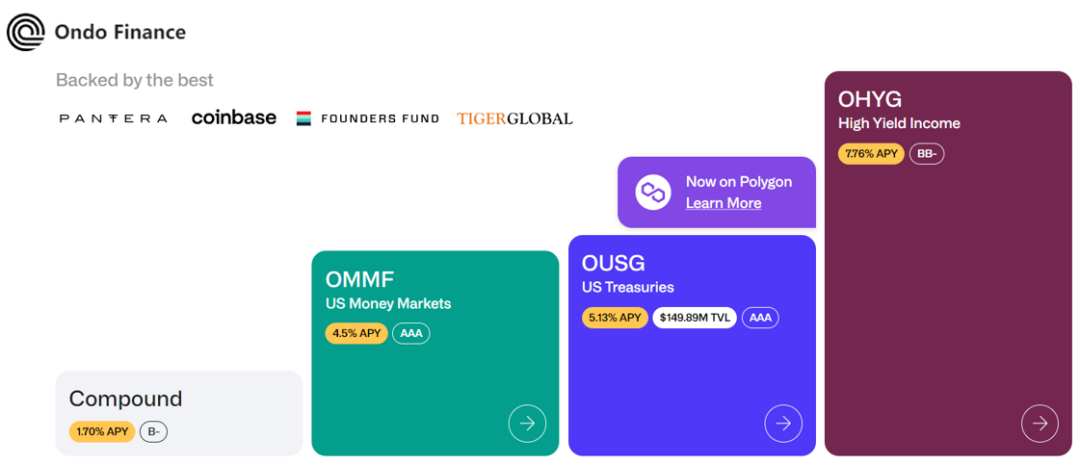

Ondo currently offers four tokenized funds: (1) U.S. Money Market Fund (OMMF); (2) U.S. Treasuries (OUSG); (3) Short-Term Bonds (OSTB); (4) High-Yield Bonds (OHYG). OUSG is the most popular, backed by BlackRock’s iShares Short-Term Treasury Bond ETF. OUSG tokens are dollar-pegged and collateralized by short-term U.S. Treasuries. Holders can use Ondo’s decentralized lending protocol Flux Finance to pledge OUSG and borrow stablecoins like USDC and DAI.

For regulatory compliance, Ondo Finance enforces a strict whitelist system, open only to Qualified Purchasers. The SEC defines a Qualified Purchaser as an individual or entity owning at least $5 million in investments. A fund composed solely of Qualified Purchasers qualifies for exemption under the U.S. Investment Company Act of 1940, avoiding registration with the SEC.

Investors must first pass Ondo Finance’s official KYC and AML verification before signing subscription documents. Eligible investors deposit stablecoins into Ondo’s OUSG fund, which uses Coinbase Custody for fiat on/off-ramps and Clear Street, a compliant broker, to execute Treasury ETF trades.

Note: Qualified Purchaser differs from Accredited Investor, the latter requiring annual income above $200,000 or net assets (excluding primary residence) exceeding $1 million.

3.2.4 Matrixdock & T Protocol (Permissionless On-Chain Treasuries)

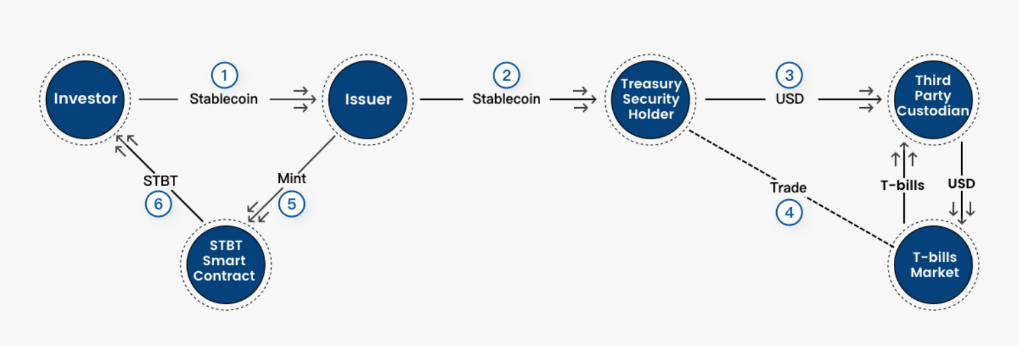

Matrixdock, a Singapore-based asset manager under Matrixport, launched an on-chain bond platform. Its Short-term Treasury Bill Token (STBT) is backed by U.S. Treasuries. Only KYC-verified qualified investors can invest. Investors deposit stablecoins from whitelisted addresses to mint STBT. STBT’s underlying assets are six-month U.S. Treasuries and reverse repurchase agreements collateralized by U.S. Treasuries. STBT transfers are restricted to whitelisted users, including within Curve pools.

STBT’s implementation: (1) Investors deposit stablecoins into the STBT issuer, which mints corresponding STBT via smart contract; (2) The issuer exchanges stablecoins for fiat via Circle; (3) Fiat is held by qualified third-party custodians, who use traditional financial channels to buy short-term Treasuries maturing within six months or invest in the Fed’s overnight reverse repo market.

The STBT issuer is an SPV formed by Matrixport, pledging its Treasury and cash assets to STBT holders, who enjoy first-priority claims on the underlying asset pool.

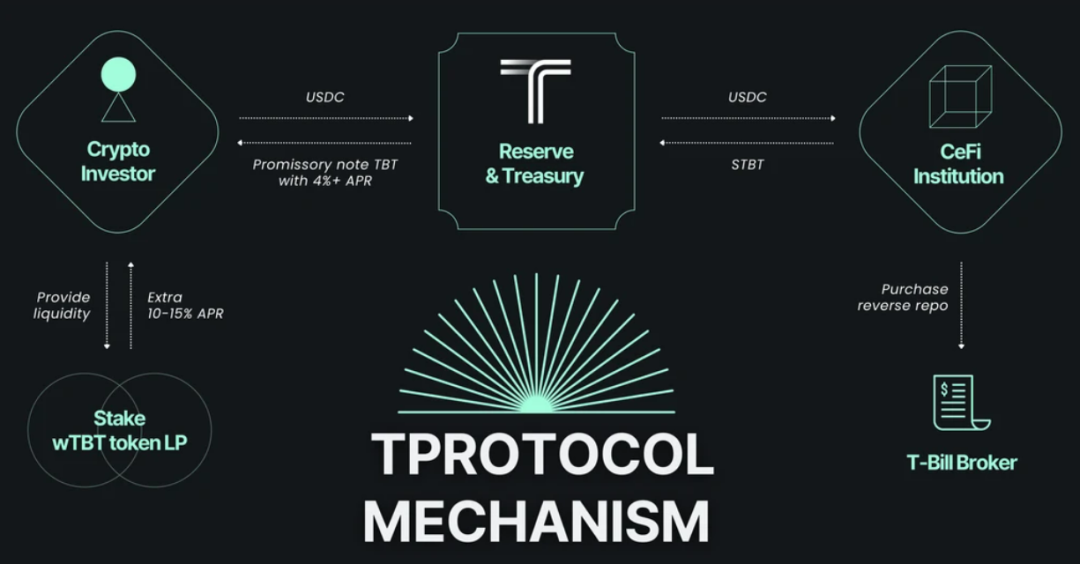

T Protocol launched in March 2023, with its TBT token backed by MatrixDock’s STBT. T Protocol wraps STBT to remove whitelist restrictions, enabling a permissionless U.S. Treasury tokenization product. TBT uses a rebase mechanism to maintain a $1 peg and can be traded on Curve.

TBT aggregates investor stablecoins to meet STBT’s whitelist thresholds, purchasing STBT via partner MatrixDock. Indirectly, TBT achieves permissionless access to Treasury RWA assets.

3.2.5 Summary

In MakerDAO’s case, motivated by asset management needs, part of its treasury stablecoins are converted into RWA assets. Compared to Monetalis’s large-scale Treasury procurement via trust structures, MakerDAO’s current RWA pools from Centrifuge are relatively smaller—BlockTower S4, the largest, barely reaches hundreds of millions. Centrifuge’s advantage lies in simplicity and avoiding complex legal structures for MakerDAO itself.

Matrixdock’s RWA approach closely mirrors Ondo Finance’s, both requiring strict whitelisting for compliance. Given the high barrier, Ondo enhances liquidity by linking OUSG to Flux Finance’s DeFi lending protocol, enabling borrowing. Matrixdock achieves permissionless circulation of Treasury RWAs through T Protocol.

4. RWA Meets the DeFi Lego Ecosystem

We believe the application logic for USD-denominated yield-bearing RWA assets parallels that of ETH-denominated LSD assets in DeFi. Mapping yield-bearing assets on-chain is only the first step (Staked US Dollar). How they integrate with DeFi—how they plug into the DeFi Lego set—is where things get exciting.

We’ve already seen examples: Ondo Finance with Flux Finance, MatrixDock with T Protocol and Curve. Below, we examine stUSDT, TRON’s “Web3 Yu’ebao” product, to understand how yield-bearing assets are applied on-chain, then draw parallels to Pendle—a project in the LSD space—to explore potential RWA+DeFi use cases.

4.1 stUSDT — Web3 Yu’ebao

On July 3, 2023, the TRON ecosystem officially launched stUSDT, a stablecoin yield product branded as “Web3 Yu’ebao,” allowing users to stake USDT to earn real-world RWA yields. The staking receipt, stUSDT, becomes a foundational building block in TRON’s DeFi Lego ecosystem.

Specifically, when users stake USDT, they receive stUSDT at a 1:1 ratio. stUSDT is backed by real-world assets (e.g., Treasuries), and the stUSDT-RWA smart contract distributes yield via a rebase mechanism. Designed similarly to Lido’s stETH, stUSDT is an encapsulated TRC-20 token, enhancing its composability within TRON’s DeFi ecosystem and unlocking infinite possibilities.

In an interview with Foresight News, Justin Sun stated: “stUSDT has strong composability—it can exist across various DeFi lending, yield, and contract protocols, and can be listed on exchanges. stUSDT will become a fundamental yield anchor for the entire $50 billion TRON ecosystem and is critically important for the DeFi Lego set.”

4.2 Pendle — Interest Rate Swap Protocol for Yield-Bearing Assets

Pendle is a derivatives protocol for yield-bearing assets. Through Pendle, users can manage yield strategies based on principal and interest according to their risk preferences. Since Ethereum’s shift to POS, the boom in the ETH liquid staking (LSD) sector has pushed Pendle’s TVL to $145 million.

Pendle defines “Yield-Bearing Tokens” (SY)—any token generating yield, such as stETH earned by staking ETH on Lido. Pendle then splits SY into “Principal Tokens” (PT) and “Yield Tokens” (YT), where P(PT) + P(YT) = P(SY). PT represents the principal portion, granting redemption rights before

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News