Can on-chain real estate revolutionize traditional transaction and rental markets?

TechFlow Selected TechFlow Selected

Can on-chain real estate revolutionize traditional transaction and rental markets?

This article reviews existing on-chain real estate projects in the market, identifies common issues among them, and proposes corresponding hypotheses.

Author: Jeff

Summary

-

On-chain real estate enables secondary splitting of property asset structures and rights, allowing separation of ownership, income rights, and usage rights—each tradable independently. Particularly, on-chain real estate can undergo multi-layered time-based fragmentation.

-

Resolving scene fragmentation during the onboarding process is currently the core challenge in the development of on-chain real estate projects. Platform tokens, DID (Decentralized Identifiers), and on-chain streaming payment platforms have the potential to address black-box issues.

-

Current compliance frameworks carry potential risks, as there lacks a solid chain of title between buyers' NFTs and SPV entities.

-

It is recommended to explore bridging uncommon asset classes—such as extremely cheap distressed assets and highly expensive scarce assets—by fractionalizing ownership while binding rights to NFTs, thereby addressing genuine transaction needs for both buyers and sellers.

-

It is advised to segment user communities and refine use cases—for example, by catering specifically to digital nomads’ rental demands, leveraging their native affinity with web3 to build small yet elegant business models.

Amidst the crowded RWA sector, innovation centers on the disassembly and reconfiguration of asset structures. The global real estate market reached $11 trillion in 2022. Bridging this massive market onto blockchain and forming a new ecosystem deserves close attention. This article reviews existing on-chain real estate projects, identifies common problems, and proposes corresponding hypotheses.

I. On-Chain Solutions to South Korea’s Jeonse Housing Crisis

The real estate crisis triggered by South Korea's jeonse housing system fully exposes multiple flaws in traditional real estate transaction chains. Under the jeonse system, tenants pay landlords a deposit equivalent to 60–70% of the property’s value upfront, after which they occupy the home rent-free for a fixed term (typically two years). Due to a lack of transparent oversight, landlords often reinvest these deposits into new properties and reuse the jeonse model to continuously extract cash. The real estate market, operating under high leverage, becomes extremely fragile; any significant drop in prices or disruption in loan repayments could trigger financial collapse. Consequently, many landlords flee when unable to return deposits. Since tenant deposits only constitute unsecured personal debt, compensation occurs only after property auctions, with tenants receiving limited payouts due to low repayment priority.

Can on-chain real estate projects help prevent such crises? Below are key market issues paired with potential on-chain solutions.

-

Deposit default and fund misuse.

By paying deposits on-chain, tenants can track landlords’ fund flows and debt status in real time, enabling early warnings of insolvency. Smart contracts can also set unlock dates, automatically returning deposits to tenants upon lease completion.

-

Lack of background checks between landlords and tenants, especially regarding mortgage status.

If property titles are tokenized on-chain as NFTs, tenants can trace an NFT’s mortgage history and avoid high-debt landlords, reducing unnecessary risks.

-

In case of landlord default, tenants without ownership rights receive lower repayment priority.

If ownership NFTs are further fractionalized on-chain, tenants could receive proportional ownership NFTs when paying deposits. Upon refund, these NFTs would be returned. In case of default and liquidation, tenants could claim proportional compensation based on their ownership NFTs.

-

Real estate markets suffer from geographical limitations.

During forced property auctions, on-chain titling and NFT minting reduce geographic constraints, expanding participation from local buyers to all on-chain users globally.

-

High-value transactions limit accessibility.

Jeonse properties are mostly concentrated in Seoul’s prime areas, where high prices deter average investors. Fractionalizing ownership via NFTs allows partial purchases, significantly lowering investment thresholds.

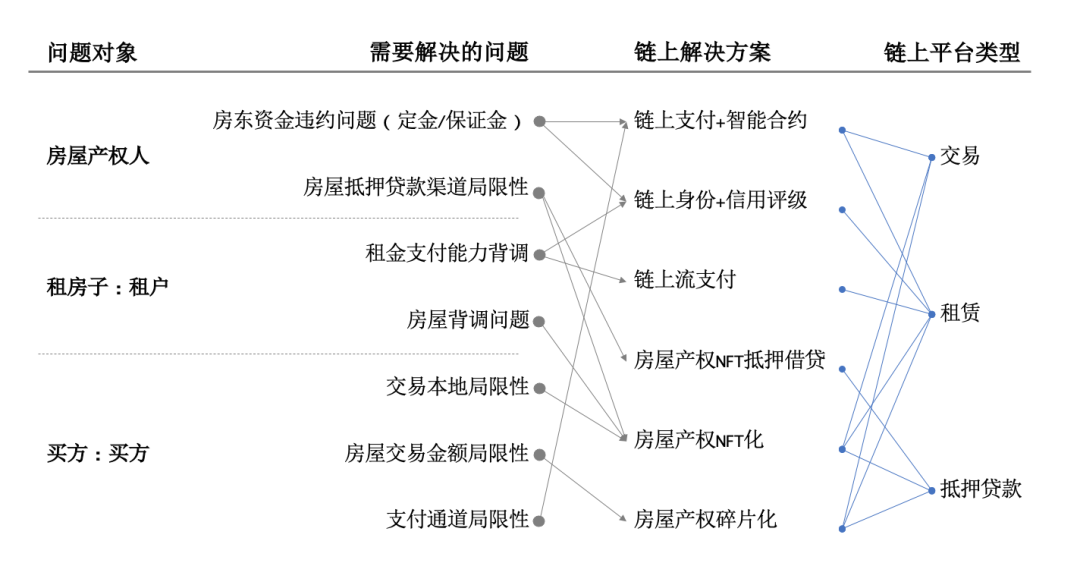

II. Target Pain Points and Core Components of On-Chain Real Estate Projects

Building on the above example, we expand on potential market pain points along the real estate value chain, categorize current on-chain solutions and projects, and analyze them through three core stages: transaction, leasing, and mortgage lending.

Figure: Mapping Market Pain Points and On-Chain Solutions

In the transaction phase, buyer needs are typically prioritized. Existing on-chain real estate projects mainly split ownership and usage rights, recombine them across time dimensions, and employ on-chain payments, identity systems, property NFTs, and fractionalization to tackle underlying market issues.

-

Eliminate local transaction limitations; on-chain property vetting improves listing authenticity.

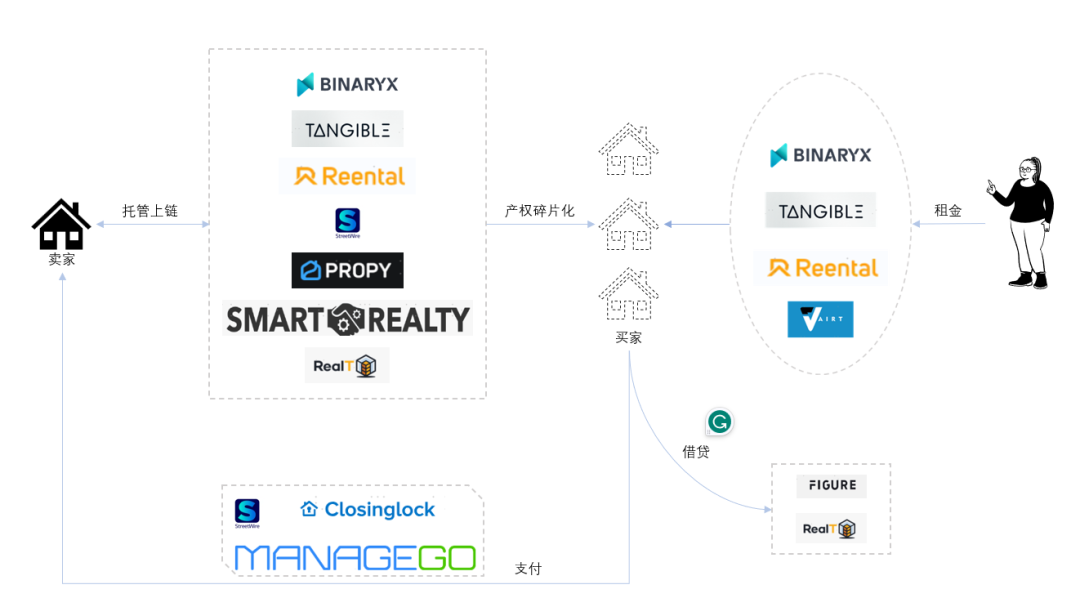

Clearly, on-chain platforms offer global investors direct access. Platforms like Tangible bundle property rights into local SPVs (Special Purpose Vehicles) and mint ownership NFTs containing all title documents and property details. Global investors can purchase these NFTs directly via the platform, effectively acquiring ownership. In this process, Tangible pays the seller a 10% deposit upfront, then opens the property for public subscription. Buyers decide whether to invest after reviewing the property information.

-

Prevent default on deposits and down payments; on-chain payments ensure fund security.

Using on-chain payments for deposits enables smart contracts with time locks, automatically penalizing defaulters. This increases fund transparency and enables early risk detection. For instance, if Tangible fails to complete a sale within the agreed timeframe, the deposit is automatically refunded to the platform.

-

Overcome high transaction value barriers, lowering entry thresholds.

Users can customize investment amounts. To lower cross-border entry barriers, platforms like RealT perform secondary splits of property rights—some fractionalize ownership so small investors can buy shares; others separate ownership from rental income, allowing users to purchase only future rental yields over N years. Additionally, CityDAO registers DAO entities to hierarchically fractionalize land ownership, granting not just property rights but governance rights to buyers.

-

Remove payment channel limitations.

Regulatory hurdles around fiat payments trouble global traders. Thus, platforms like Smart Reality and ManageGo offer cryptocurrency payment channels, holding deposits in escrow. With mutual consent, even full settlements in crypto are possible. Intermediary platforms like Closing Lock monitor fund safety and take commissions.

Problems in the leasing phase primarily revolve around rent collection and property security. Current leasing platforms have not fully moved leasing activities on-chain. Without exception, Tangible, BinaryX, and Reental rely on web2 outsourcing partners to ensure timely rent payments. However, managing leases on-chain offers ample room for innovation.

-

On-chain mutual vetting of tenant’s rent-paying ability and landlord’s property background.

Through on-chain leasing, landlords can observe tenants’ on-chain activity to assess financial standing and repayment capacity, tailoring deposit requirements accordingly. Tenants can verify property legitimacy via on-chain title records. StreetWire is currently developing features in this direction.

-

On-chain deposit payments secure assets; streaming payment platforms enforce rent obligations.

As discussed in the Korean jeonse case, on-chain deposits protected via fractional ownership NFTs safeguard tenant interests. For standard monthly rentals, streaming payment platforms like Sablier use smart contracts to force timely rent payments and ensure automatic deposit refunds upon lease end—already demonstrated successfully.

-

Fractional ownership NFTs enable divisible and composable rental income.

Fractional ownership NFTs allow rental income to be distributed proportionally to all co-owners via smart contracts. External adjustment factors can dynamically modify lease terms based on market demand. This composability lets users freely trade "lease contracts" with time restrictions. Tangible and other leasing platforms have developed rent-yield-splitting functions. Beyond that, platforms like Vairt are experimenting with moving short-term rentals on-chain to reduce vacancy periods.

The mortgage lending phase remains largely unexplored, with only RealT and FIGURE attempting to offer lending against fractional ownership NFTs. However, due to immature price oracle mechanisms and imbalanced supply-demand dynamics, these services haven’t gained broad market acceptance. Moreover, lending platforms aimed at reducing homebuying capital costs remain absent, including BNPL (Buy Now, Pay Later) functionality.

Figure: Breakdown of Core Components in On-Chain Real Estate Projects

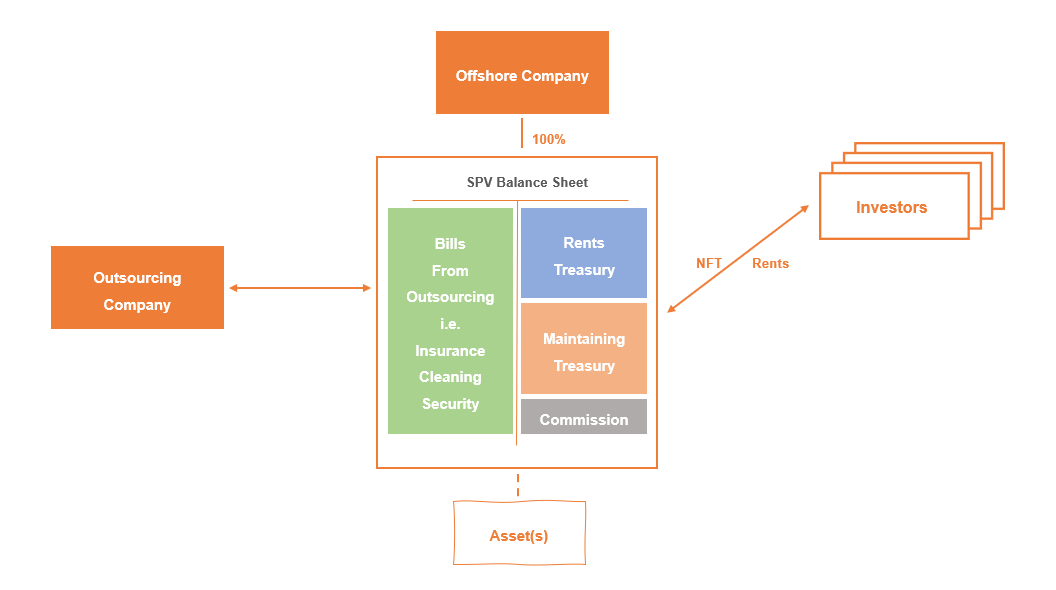

III. Compliance Architecture and Asset Security

Ensuring regulatory compliance of on-chain property rights was my top concern during research. Currently, nearly all on-chain real estate projects use offshore entities to control SPVs, circumventing local regulations. I believe this approach is neither fully secure nor effective.

Figure: SPV Structure Diagram of On-Chain Real Estate Projects

Take Tangible’s compliance model: UK properties sold on its platform are held by individual UK SPVs, each directly controlled by Tangible’s offshore parent entity. Fractional ownership NFTs are issued and sold by the SPVs. While this offers some protection, strictly speaking, these NFTs do not legally represent equity in the SPV. If the parent company or SPV faces debt disputes, since the NFTs cannot directly prove ownership or correspond to any shareholding, buyers may lose everything despite their investment. The very asset security intended to be solved by blockchain ends up relying entirely on the platform, introducing additional risk. Furthermore, if SPVs issue these NFTs, it reignites the debate over whether such tokens should be classified as securities.

Therefore, the only viable solution—to bypass regulation while ensuring asset safety—is stronger oversight of SPVs. CityDAO provides a strong example: registering as a DAO ensures every NFT holder’s interests are protected. We look forward to CityDAO’s expansion beyond geographic constraints.

Are SPVs themselves at risk of debt disputes? Yes—especially in the rental phase, default risks are high.

-

Reserve fund risk: Again using Tangible as an example, the platform sets aside 7% of total property value as vacancy and maintenance reserves. If reserves fall below this level, 20% of rental income is withheld or distributions paused. As off-chain assets, reserve funds lack transparency. SPVs may misuse these funds—for example, using them as down payments for new property auctions or other investments. If properties remain vacant long-term and sales proceeds aren’t timely recovered, SPVs face default risk.

-

Mortgage risk: Since SPVs hold full ownership and users cannot monitor in real time, SPVs might mortgage properties to raise capital for other investments, increasing default exposure.

What Problems Remain Unsolved? What Are Potential Solutions?

In my view, the “black box” problem during onboarding is the most critical issue to resolve: the disconnect between on-chain and off-chain operations creates uncertainty in transactions and leasing. This uncertainty leads directly to:

-

Scarcity of high-quality assets: Prime properties sell easily offline. On-chain listings require due diligence before tokenization—an extra step that may slow transaction speed compared to traditional brokers. As a result, on-chain platforms often list hard-to-sell properties or incur higher operational costs. Improving onboarding efficiency and aligning inventory with user demand remains a key challenge.

-

Actual returns far below projected returns: Platforms often include property appreciation and rental income in ROI projections. But in practice, outsourcing management means landlords cannot control occupancy rates or tenant defaults. In Europe, evicting non-paying tenants can take up to six months through legal proceedings—meaning zero rental income for half a year.

-

Limited liquidity confined to-chain: On-chain purchased properties, being fractionally owned, can only be resold to buyers seeking matching fractions. Liquidity is thus constrained, often trapped entirely on-chain. Meanwhile, on-chain mortgage lending remains undeveloped, creating a critical gap.

Beyond the black-box issue, on-chain real estate platforms lack true web3-native characteristics. Platform tokens are largely underutilized, making the entire ecosystem feel more like a web2 platform operating on-chain.

-

Most platform tokens lack utility. Enhancing token functionality could increase user stickiness and attract non-investment participants. For example, casual website visitors could become contributors or content creators.

-

Heavy reliance on third-party managers undermines user engagement. Introducing fully on-chain leasing components—using user DID and credit accounts to determine deposit amounts, smart-contract-controlled door locks or power switches to prevent overstays, and crowdsourced maintenance with token incentives—could greatly improve retention.

-

Platforms overly depend on regional assets. Over 90% of current on-chain real estate platforms focus on the U.S., whereas global real estate transaction volumes in 2022 ranked the U.S., Japan, the U.K., and Germany. Few platforms serve these latter markets or aim to build global transaction or rental ecosystems. I believe the rental market is a particularly suitable native web3 use case and warrants deeper exploration, elaborated below.

IV. Open Hypotheses for On-Chain Real Estate Projects

Despite the aforementioned challenges—and the fact that most projects fail to meaningfully address real user needs—we remain optimistic about this space, because many niche scenarios and latent user demands remain underserved.

High-quality real estate assets rarely lack liquidity. By broadening asset categories and reclassifying them, we identify more focused segments. Two such categories are highlighted below.

-

Extremely expensive, scarce real estate.

Ultra-high-value properties—such as castles, historic mansions, wineries, and farms—are often out of reach for ordinary individuals. These assets typically command prohibitively high prices and serve non-residential purposes, leaving middle-class investors limited to passive observation without viable investment avenues. They also suffer from prolonged transaction cycles, resulting in poor liquidity. On-chain platforms offer promising solutions by fractionalizing ownership and usage rights. Take a winery: if wine production volume is also split during sale, ownership NFTs could entitle holders to annual wine output. Owners could then resell their allocated wine each year, creating an innovative marketplace. Using smart contracts to distribute ownership and usage rights across time enables users to freely combine and trade them, forming a non-standardized, novel market. This lowers investment barriers while rapidly boosting asset liquidity.

Figure: Conceptual Model of Winery Ownership and Rights NFTs

-

Extremely low-cost distressed assets.

These assets are typically acquired and restructured by specialized firms—such as unfinished construction projects or dilapidated homes needing renovation. While they may have commercial potential post-renovation, they lack safe entry points for retail investors. On-chain platforms can solve this by splitting ownership NFTs and rights NFTs, lowering investment thresholds and providing clear exit paths. For example, a renovated house could be converted into a homestay hotel, granting investors accommodation rights NFTs usable or sellable in secondary markets. Fundraising conducted fully on-chain also enables transparent monitoring of fund usage, reducing mismanagement.

Current on-chain real estate platforms generally lack user segmentation and have coarse use cases. Finer targeting could make rental-focused platforms more precise, better aligned with user needs, and more frequently used. Two potential scenarios:

-

Digital nomads form one of the largest groups in web3 communities, with over 35 million worldwide—and growing. Constantly traveling, they have strong rental needs but cannot sign long-term leases. Short-term rentals, however, come with steep premiums. I believe launching an on-chain rental platform tailored to digital nomads would be highly effective. They are already familiar with on-chain ecosystems, and most can have their asset sources traced on-chain, simplifying landlord verification. Such platforms could lock deposits via smart contracts, allow tenant reviews, and apply DID-based reputation tags to both parties, creating effective mutual accountability.

Figure: Global Distribution of Digital Nomads

-

Launch community-driven real estate projects—leveraging “human mining”—and utilize web3’s 2Earn mechanics to create self-governing communities akin to Aranya or CityDAO. Community members govern legal entities via ownership NFTs, unlock benefits and earnings via platform tokens, and exercise legitimate autonomy. All ownership and rights can be resold or mortgaged on-chain, forming a new paradigm of community-based real estate.

Stay Optimistic

Discussing on-chain real estate projects today may seem premature, and many issues won’t be resolved soon. Yet given the market’s sheer size and genuine user demand, I choose to stay optimistic. I believe on-chain real estate can evolve into a transformative ecosystem.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News