OKX Ventures: Embracing All Markets – How RWA Helps DeFi Eat the World

TechFlow Selected TechFlow Selected

OKX Ventures: Embracing All Markets – How RWA Helps DeFi Eat the World

Amid the loud proclamations of "models will ultimately rule the world," DeFi is quietly whispering about devouring all markets.

Content provided by Sally Gu, researcher at OKX Ventures. Not intended as investment advice.

Introduction

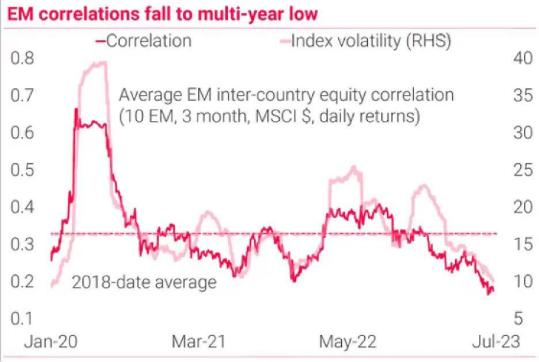

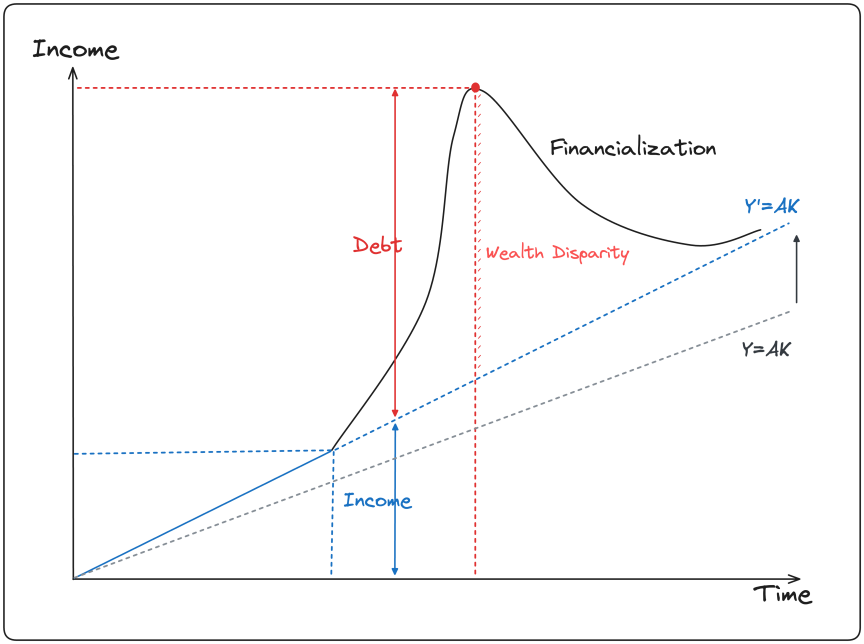

The combination of pandemic impacts and consecutive rate cuts by the Federal Reserve under Powell led financial markets into the largest asset bubble since World War II, characterized by high inflation and low real interest rates. However, the foundations of globalization built over the past 40 years have begun to unravel due to the China-U.S. trade war, Russia-Ukraine tensions, and the rise of European populism. The era of liquidity expansion and high leverage since 2018, which fueled financial wealth effects, is over. Amid rising wages at the lower end and deflationary pressures at the top, the excess returns previously driven by declining interest rates and valuation expansion appear irreversibly reverting to the mean.

Source: TS Lombard

Source: Bloomberg

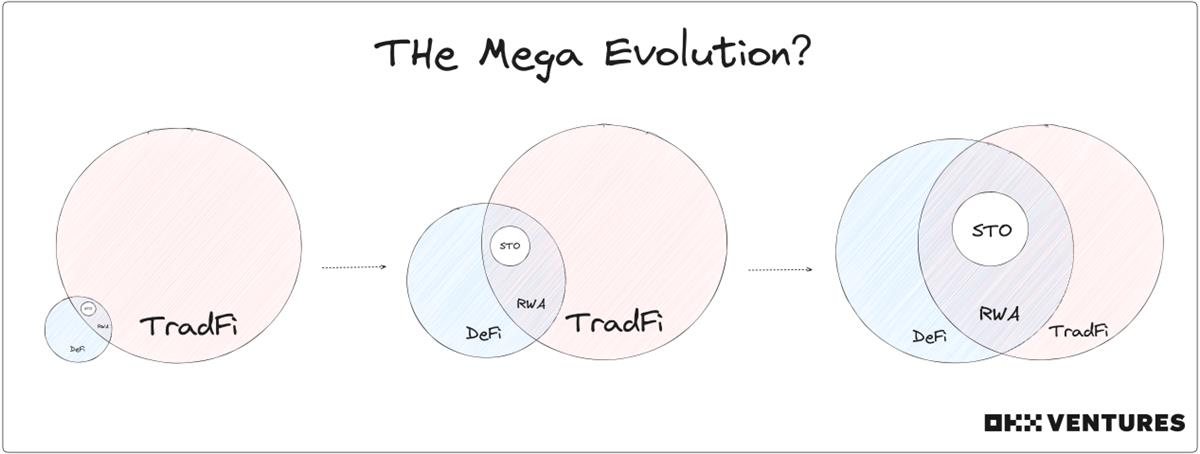

With the U.S. yield curve deeply inverted for over 50BP amid a prolonged hiking cycle, and purely speculative narratives like metaverse PFP NFTs fading due to lack of intrinsic value, DeFi—or crypto-economics—reconnecting with real-world assets (RWAs) and traditional finance (TradFi) may be a natural evolution during this period of economic downturn and deleveraging.

To better understand the convergence between DeFi and TradFi, we provide a breakdown and analysis below of the RWA sector, which is gaining increasing attention.

TL; DR

Logic:

-

From a TradFi perspective: Reduce transaction costs, improve transparency and capital efficiency; enhance composability of financial primitives; offer new hedging instruments; unlock capital from potential speculators and institutions.

-

From a DeFi perspective: Sustain and amplify DeFi's speculative loops; inject massive liquidity; expand user base; stablecoin markets have already proven viable.

-

Drivers of sector growth: Macro cycles driving capital back to USD-denominated assets; growing interest from legacy institutions; crypto needs new users.

-

Barriers to growth: Uncertain regulatory environment, limited traction, scarcity of high-quality underlying assets.

-

Evaluation criteria: Product fundamentals, risk management, protocol design, partnerships.

Classification:

-

By asset form: Standardized vs. non-standardized.

-

By asset class: Fiat, fixed income (bonds, credit), equities, alternatives (real estate, collectibles, commodities).

-

Projects mentioned (46): Centrifuge, ONDO, Maple, OpenEden, BondbloX, FortunaFi, CredeFi, Goldfinch, TrueFi, Defactor, Credix, Clearpool, Bru Finance, Resource Finance, Backed Finance, Sologenic, Swam, AcquireFi, Horizon Protocol, Hamilton Lane, RealT, Parcl, LABS Group, Propy, Atlant, ELYSIA, Tangible, Blocksquare, Milo, Figure, LandShare, Lingo, HOME Coin, Theopetra, EktaChain, Robinland, Homebase, 4K, Arkive, mattereum, Codex Protocol, PAX Gold, Tether Gold, Cache Gold, Agrotoken, LandX.

Key Views:

-

Most RWA products currently lack product-market fit (PMF): Short-term momentum is driven more by narrative FOMO than genuine innovation or strong growth drivers. Monitor regulatory developments in the U.S., Hong Kong, and Singapore closely to minimize policy risk.

-

Alternative and non-standardized RWA protocols are emerging: Non-standard assets can be tokenized via ERC-721/1155. ERC-20 may not dominate long-term. NFTs for bills, REITs, and collectibles hold significant potential.

-

Treasury RWAs remain dominant; equity RWAs gaining attention: U.S. Treasuries are widely accepted in the crypto community. Equity-like RWAs meet real demand but face major compliance hurdles.

-

Crypto community acceptance is crucial; native integration harder than expected: Fixed-income RWAs struggle with loan-side integration. DeFi DAO members vary widely in understanding off-chain assets—complex ones are hard to gain consensus on.

-

Areas worth further exploration: On-chain Ponzi mechanics like RWA Fi and RWA options; middleware, SaaS providers, compliant issuers, and intermediaries matching lenders/borrowers; coexistence and segmentation between regulated RWA DeFi and native DeFi.

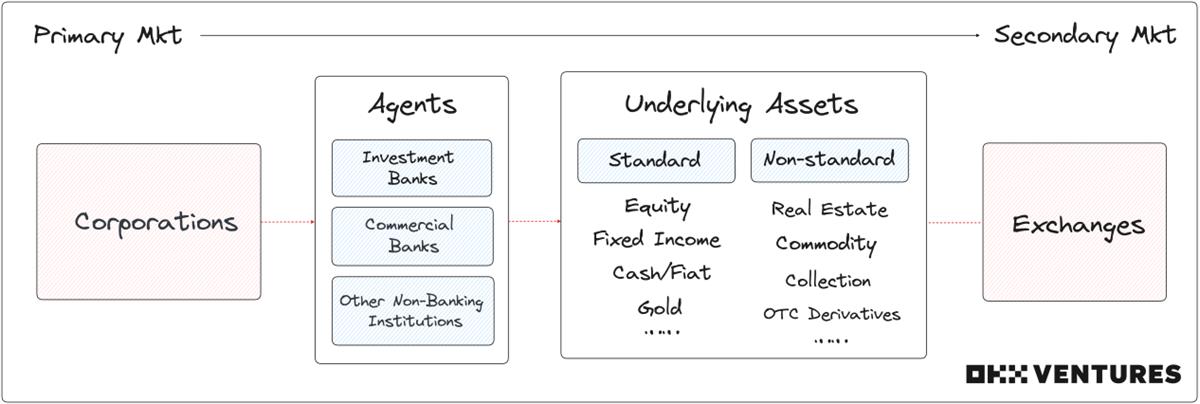

Basic Concepts

-

RWA — Tokenization of real-world assets;

-

STO — Security Token Offering, corporate bond financing;

Difference: RWA covers broader asset classes across primary and secondary markets, enabling more diverse yield structures.

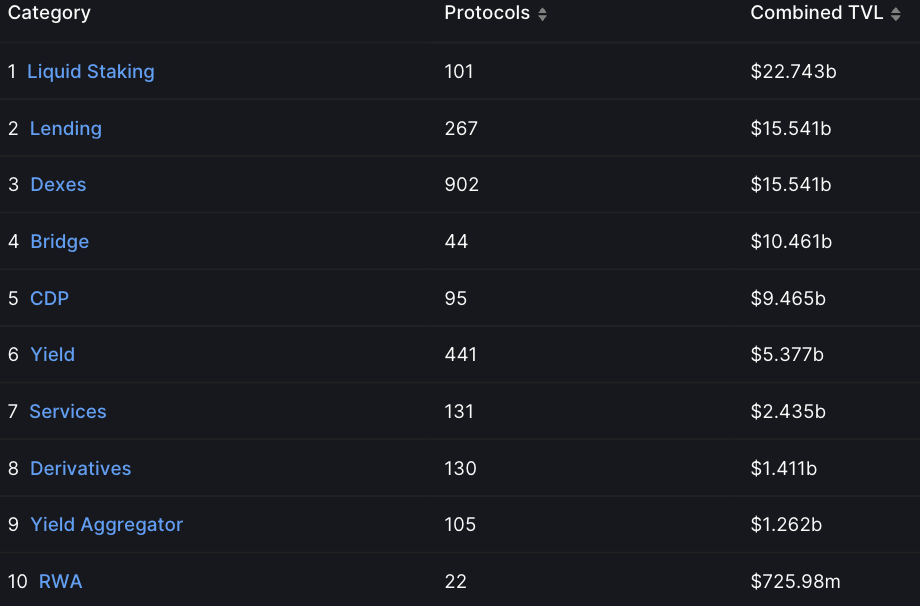

Market Data

-

Latest data shows RWA has entered the top 10 DeFi categories by TVL, with a 257% increase year-to-date.

Source: Defillama

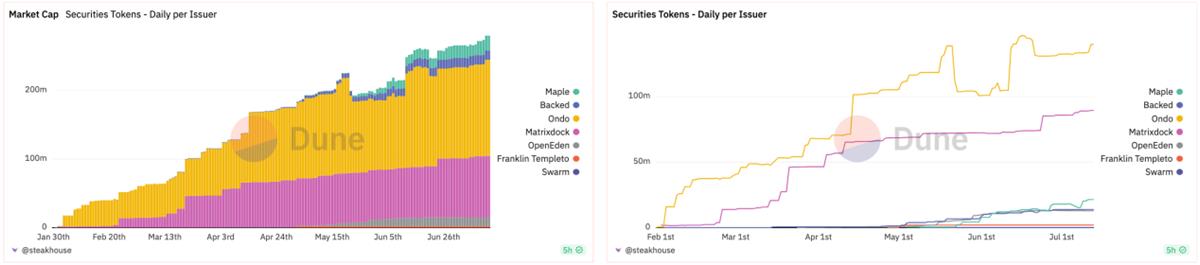

-

Since January, the market cap and daily issuance volume of sovereign bond RWA tokens have steadily increased. The combined market cap of the top seven projects is now nearly $300M.

Source: Dune

-

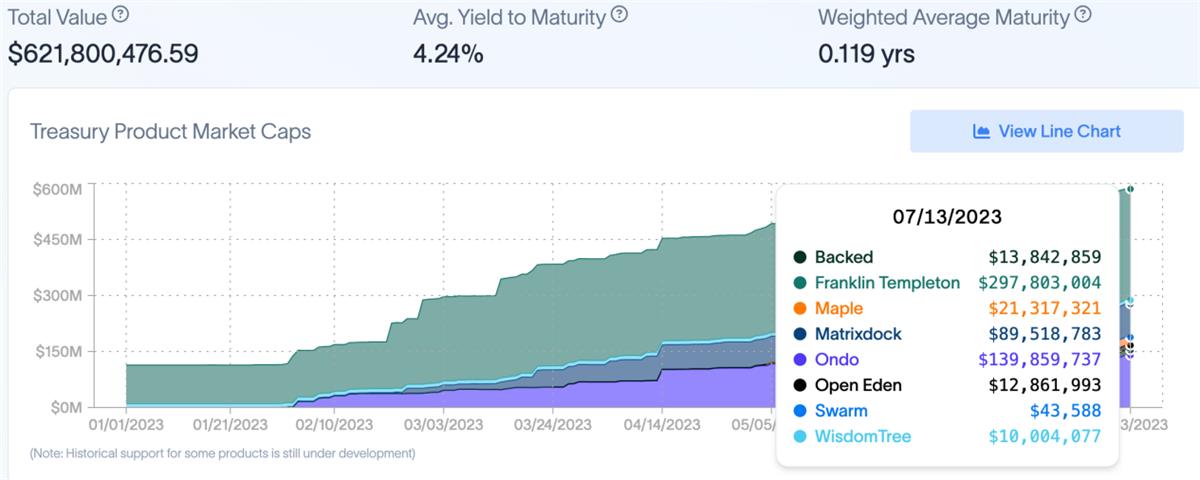

U.S. Treasury RWA tokens now exceed $600M in total value. Holder count has grown from 28k to 40k (+43%), with nearly 20k holding for over 12 months.

Source: rwa.xyz

-

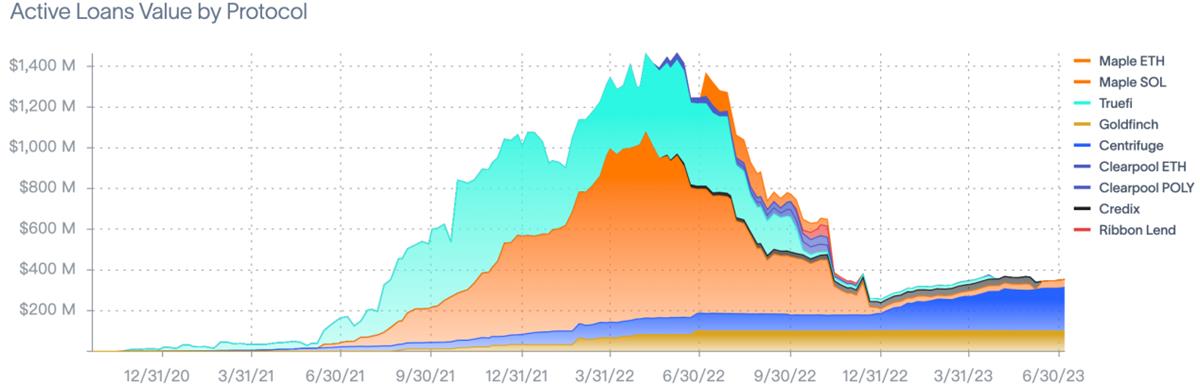

Private credit RWA protocols currently manage around 1,553 loans, with ~$500M in active loans and ~$4B in total locked value—significant room for growth compared to last year’s peak of $1.5B in total loans.

Source: rwa.xyz

-

MakerDAO’s June report shows RWAs continue to dominate its stability fee generation. In May, RWAs accounted for 79.7% of all stability fees generated—up 7% MoM from April.

Source: MakerDAO

Sector Logic

From a TradFi Perspective

Reduce transaction costs and intermediaries; enhance transparency and capital flow efficiency

-

Illiquid assets such as real estate and art can be fractionalized via tokenization, enabling faster resale, trading, collateralization, and financing in secondary markets.

-

Large-scale investments like infrastructure, railways, and power grids can issue tokens to accelerate cost recovery. SMEs can crowdfund globally via token offerings.

On-chain alternative assets and synthetic structures enhance composability of financial primitives and expand hedging toolkit

-

Enable diversified portfolio construction with extended asset class spectrum and reduced risk exposure.

-

On-chain assets can serve as hedges against volatility in traditional assets and fiat currencies within a single fund or structured product.

Unlock capital from restricted foreign speculators and institutional investors

-

Financial inclusion narrative—larger TAM means greater profit potential.

-

Capital that escaped banks may return to TradFi in new forms.

-

Further enhances global capital mobility, benefiting some local institutional investors—but may exacerbate regional inequality and liquidity imbalances, leading to sharper social divides.

From a DeFi Perspective

Sustain and amplify DeFi’s speculative cycles

-

DeFi creates a token speculation market where value accrual depends on the protocol’s ability to generate revenue from speculative activity.

-

RWA can shorten this speculative loop by anchoring tokens to liquid, debt-backed, or collateralized real-world assets—effectively building a foundational layer beneath DeFi.

Inject massive liquidity and expand DeFi’s user base

-

TradFi rules are more familiar to mainstream users, lowering the learning and entry barrier for DeFi.

-

Institutional capital dwarfs DeFi in scale, density, reach, risk capacity, distribution channels, participant ratio, and professionalism.

-

BCG & ADDX estimate the tokenized market could reach $16T by 2023 (including $3T real estate, $4T public/private assets, $1T bonds/funds, $3T alternatives, $5T others).

-

Citi estimates digital securities and blockchain trade finance could reach $5–6T by 2030.

Source: Chainlink

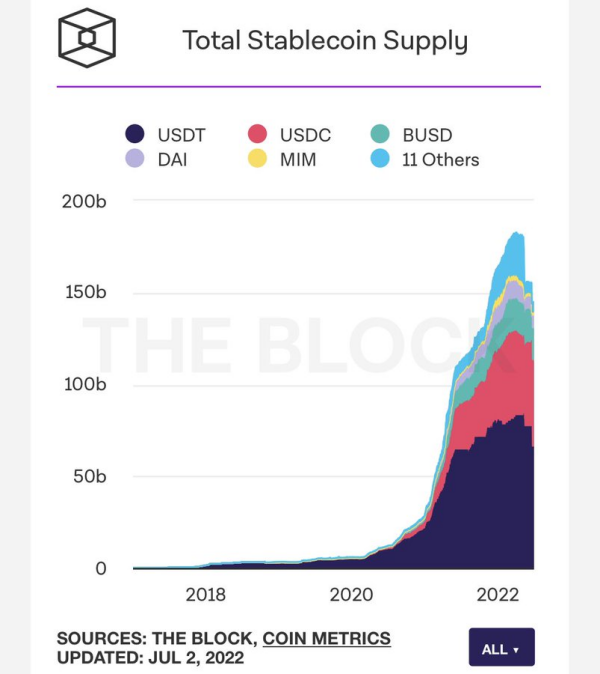

Stablecoin markets have already been validated

-

USDC and USDT are essentially RWAs backed by fiat.

-

Stablecoin market cap peaked at $180B in 2022.

Source: The Block

Momentum Drivers

Macro cycle drives capital back to USD-denominated assets

-

Regulatory tightening and improved compliance frameworks.

-

Higher yields on traditional USD assets—rising rates pushed short-term Treasury yields to 4% (latest 2-year yield: 4.64%, slightly narrowed but still elevated).

-

Post-SVB crisis, most idle funds avoid risk and remain parked in safe assets like U.S. Treasuries.

Source: Alliance Bernstein

Growing interest from legacy institutions

-

Push for BTC ETF approval signals fading alpha opportunities in traditional markets—mainstream players now focus on beta (passive) returns rather than outperforming benchmarks.

-

TradFi faces stagnation, seeking transformation—see past trends like Internet+Finance, AI adoption, fintech innovations like Aladdin.

-

Legacy players believe crypto-native teams lack deep TradFi understanding and market insight—RWA is better suited for traditional firms to explore and position themselves.

Crypto needs new users

-

Repeated blowups (LUNA, FTX, etc.) severely damaged market confidence.

-

On-chain liquidity dried up; NFTs collapsed.

-

Crypto-native infrastructure suffers from inverted primary/secondary markets and lackluster Lego-like innovation.

Handicaps and Barriers

Uncertain regulatory climate

-

Taxation, asset classification, licensing, and claims processes depend heavily on local financial regulations.

-

Global regulatory fragmentation—no unified standard for digital assets across jurisdictions.

-

Protocol survival often hinges on central bank, banking, and SEC attitudes—high risk of sudden collapse.

Limited traction

Contradicts crypto-native ethos; lacks PMF

-

Early crypto users strongly resist centralized oversight and banking systems, favoring independent DeFi ecosystems.

-

Many DeFi participants dislike KYC/AML (even with ZKP privacy solutions), preferring fully permissionless interactions.

-

High-risk-tolerant DeFi users find RWA yields unattractive—even equity RWAs may underperform simple Uni pool farming (especially with v4 hooks increasing flexibility).

-

Low-risk-tolerant DeFi users are a small base and can just stake major coins or buy ETFs for passive income.

Traditional institutions hesitant to enter; still evaluating

-

On-chain liquidity remains tiny vs. TradFi; insufficient depth to generate major wealth effects. Likely only hot money from TradFi flows into crypto—not vice versa.

-

How much effort will TradFi commit to chasing speculative alpha? How large a percentage will they allocate? Currently, unlikely to exceed 0.01% on balance sheets—insignificant vs. other operations.

-

Discussions with traditional fund managers show most won’t consider trading on-chain or synthetic assets soon: (1) ample substitutes and hedging tools exist in traditional equity markets; (2) LP backgrounds and risk profiles limit crypto allocations to avoid disrupting existing portfolios.

Limited high-quality underlying assets

-

High-quality assets like U.S. Treasuries are limited. Niche assets (e.g., New Zealand stocks) lack liquidity and T+0 settlement. Small-cap or penny stocks, like altcoins, are loosely tied to macro trends—hard to build sound strategies. Unlikely to be tokenized.

-

Tokenizing similar assets leads to low protocol differentiation and commoditization.

-

Sector will inevitably follow a Matthew effect, similar to LSD.

Evaluation Criteria

-

Product Fundamentals

1) Diversity and competitiveness of offered RWA products and yield ranges. Service scope (what assets are being handled, where, and do they have long-term qualifications?)

2) TAM stickiness, user retention, pool depth and liquidity, discount rate.

3) Protocol revenue and net profit, token value, and circulation efficiency.

-

Risk Management Capability

1) Team: Any experience in investment/commercial banking or securities? Strong ties with legal systems? No history of crypto-related violations or bad reputation?

2) Compliance: Does the company comply with local securities laws? Is the regulatory environment crypto-friendly? Are asset classifications clearly defined or banned? KYC/AML, default settlement, compliance cost, credit assessment?

-

Protocol Mechanism

1) Tokens representing RWAs must interact across multiple blockchain backends—interoperability is key.

2) Is the onboarding process decentralized? What trust-minimized mechanisms are used? Are off-chain cash flows and debt positions regularly disclosed? Which oracle network and node selection mechanism is adopted?

3) Protocol security: Protection against address leaks, oracle manipulation, hacking, etc.?

-

Partnerships

1) Partnerships with major DeFi communities like MakerDAO or Aave? Stable on-chain lending partners?

2) Trusted third-party custodians for on-chain assets (e.g., SPVs controlling off-chain collateral)?

3) Long-term collaborations with top-tier banks, trusts, or TradFi intermediaries in terms of reputation, scale, and service scope?

Underlying Asset Classification

By Asset Form

Standardized (S)

-

Semi-fungible or fungible, easily tradable assets with financial and monetary value.

-

Traded publicly and on-exchange.

-

Typically regulated by the SEC.

Non-Standardized (N)

-

Illiquid, non-fungible, hard-to-price, hard-to-trade assets.

-

Usually traded privately and OTC.

-

More likely under CFTC jurisdiction.

Brief overview of U.S. regulators and their scope:

By Asset Class

-

Fund attributes determine trader behavior, which in turn shapes asset allocation choices.

-

Investor tolerance for risk and uncertainty defines their allocation across asset classes.

1. Fiat RWA

Common: USD, EUR, JPY, GBP, CNY, etc.

Watchlist: AUD, CAD, KRW, CHF, ZAR, MXN, etc.

Key tool: Collateralized stablecoins.

Projects: Circle, Tether, Frax, MakerDAO, etc.

-

The earliest RWAs were fiat-backed stablecoins like Circle’s USDC and Tether’s USDT.

-

Transaction costs, channels, and currency options are currently limited.

-

If more fiat currencies become on-chain assets—like those from Russia, Malaysia (weak equity correlation), or Canada, Australia, South Korea (negative correlation)—they might serve as useful hedges (setting aside depth concerns for now).

2. Fixed-Income RWA

2.1 Bonds

Common: Sovereign bonds (U.S., EU, Japan, Australia, China), central bank bills, government bonds, corporate bonds, foreign debt, credit bonds, convertible bonds, etc.

Key tools: ETFs, bond derivatives.

Projects: Centrifuge, ONDO, Maple, OpenEden, BondbloX, FortunaFi, CredeFi, etc.

-

Sovereign bonds/T-bond ETFs dominate RWA due to low risk, often seen as safe-haven assets.

-

Despite modest yields, top DeFi communities still use bond and corporate RWA to hedge risk—e.g., MakerDAO allocated 500 million DAI to U.S. Treasury RWAs in early 2023.

-

There’s still room to explore bill, corporate, and credit bond RWAs—project teams can differentiate based on their expertise and networks.

2.2 Credit

Common: Personal loans, business loans, structured finance, mortgage loans, auto loans, etc.

Projects: Centrifuge, Maple, Goldfinch, TrueFi, Defactor, Credix, Clearpool, Bru Finance, Resource Finance, etc.

-

Enables global credit access, offering both institutions and retail investors stable returns.

-

Corporate lending helps ease SME financing pressure, gaining broader social and governmental support.

3. Equity RWA

Major markets: U.S., EU, Japan, China, Hong Kong, Australia.

Emerging focus: BRICS nations.

Key tools: ETFs, index derivatives, blue-chip stocks.

Common: Equity, private shares (primary), public shares (secondary).

Projects: Backed Finance, Sologenic, Swam, AcquireFi, Horizon Protocol, Hamilton Lane, etc.

-

Individual stocks require less macro focus—more about company-specific performance.

-

Demand for such assets is real but heavily constrained by regulation. Platforms like BackedFi enabling 24/7 U.S. stock trading could become arbitrage havens.

-

Synthetic assets combining crypto and equities may be more attractive.

4. Alternative RWA

4.1 Real Estate

Common: Residential, commercial properties.

Key tool: REITs.

Projects: RealT, Parcl, LABS Group, Propy, Atlant, ELYSIA, Tangible, Blocksquare, Milo, Figure, LandShare, Lingo, HOME Coin, Theopetra, EktaChain, Robinland, Homebase, etc.

-

Tokenizing real estate enables easy property-backed lending; fractional ownership allows retail participation.

-

REIT tokenization is mature, but cost control (management, maintenance, location diversity, property types) depends on project execution.

-

Trade-off exists between asset diversification/global operations and scalability/cost.

4.2 Collectibles

Common: Art, jewelry, coins, etc.

Projects: 4K, Arkive, mattereum, Codex Protocol, etc.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News