The Potential and Challenges of Blockchain Payments: Why Haven't They Achieved Mass Adoption?

TechFlow Selected TechFlow Selected

The Potential and Challenges of Blockchain Payments: Why Haven't They Achieved Mass Adoption?

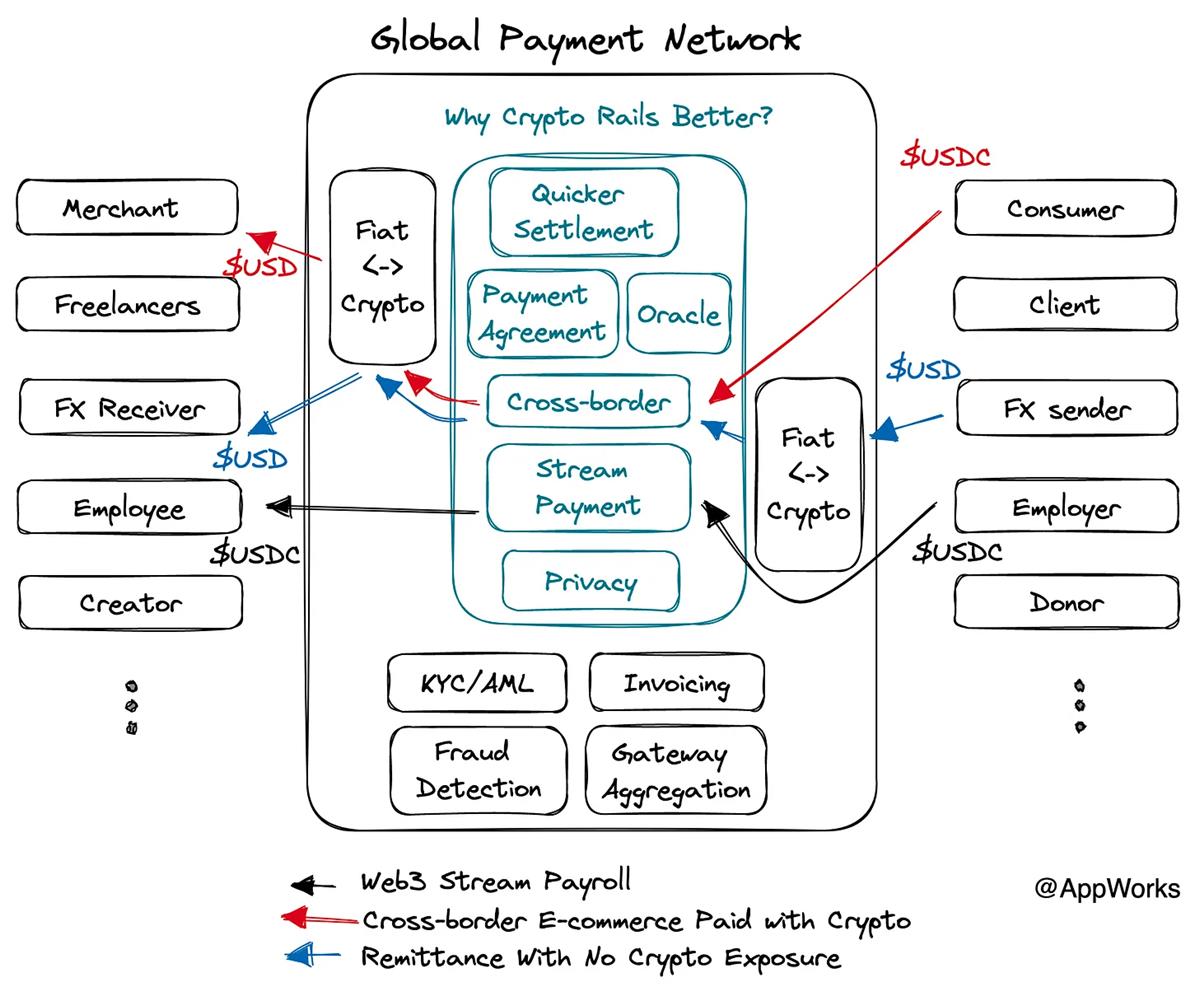

Integrate cryptocurrency payment channels into the global payment network.

Special thanks to Jamie, Joseph, Jessica, Ching, Jack, Johnny, and Donn for their feedback and suggestions on this article.

Many blockchain projects are technology-first, only to later realize they lack real-world applications—like having a hammer and searching for nails, forcing blockchain solutions onto problems without addressing actual pain points.

Recently, there’s been no shortage of online comments like: “You blockchain folks, look at ChatGPT—that’s real useful tech.” It stings, but we can’t really argue.

That’s why the First Principle at AppWorks always urges us to start from first principles—zero-base thinking, user-centric: What problems can blockchain solve ten times better than existing technologies?

Payment is where we see the most potential, because a Web3-based payment architecture is genuinely useful. Payments are universally needed, which ultimately leads to mass adoption.

Yet we’ve been talking about blockchain transforming payments for years—even since the Bitcoin whitepaper—but why hasn’t it scaled yet? That’s the question we’ll explore here.

The “usefulness” of blockchain in payments can be broken down into four key features:

-

Instant settlement—depending on chain performance, transactions settle in seconds to minutes.

-

Low-cost instant settlement enables Stream Payments.

-

Settlements are borderless, unrestricted by geography.

-

Smart contracts enable programmable payments.

Next, let’s dive deeper into how these four features can solve specific problems ten times more effectively. Among them, we’re most excited about tackling the following three.

Problem 1: SWIFT is slow, expensive, and geographically limited

SWIFT connects thousands of financial institutions globally to transfer payment messages, but it’s a 1970s system with serious flaws: slow speed (especially cross-border, taking multiple business days), high costs (multiple intermediary banks charging $10+ each), and geographic limitations (some regions still lack SWIFT access).

In the short term, completely replacing SWIFT is unlikely. Adoption requires broad institutional buy-in. JP Morgan launched Onyx in 2020 as an interbank settlement network, but progress has stalled due to competitive concerns among banks. Fully decentralized networks (like BTC/ETH) face even greater hurdles due to regulatory, compliance, and reporting challenges.

A more plausible path is integration into Visa or Mastercard’s Payment Processing Networks—private, global players already benefiting from strong network effects. And indeed, they’re already exploring this. In February 2023, Visa’s crypto lead Cuy Sheffield announced: “The current SWIFT network limits how frequently we can move funds due to its constraints. Today, I’m announcing that Visa has been testing settlement using USDC stablecoin on Ethereum.”

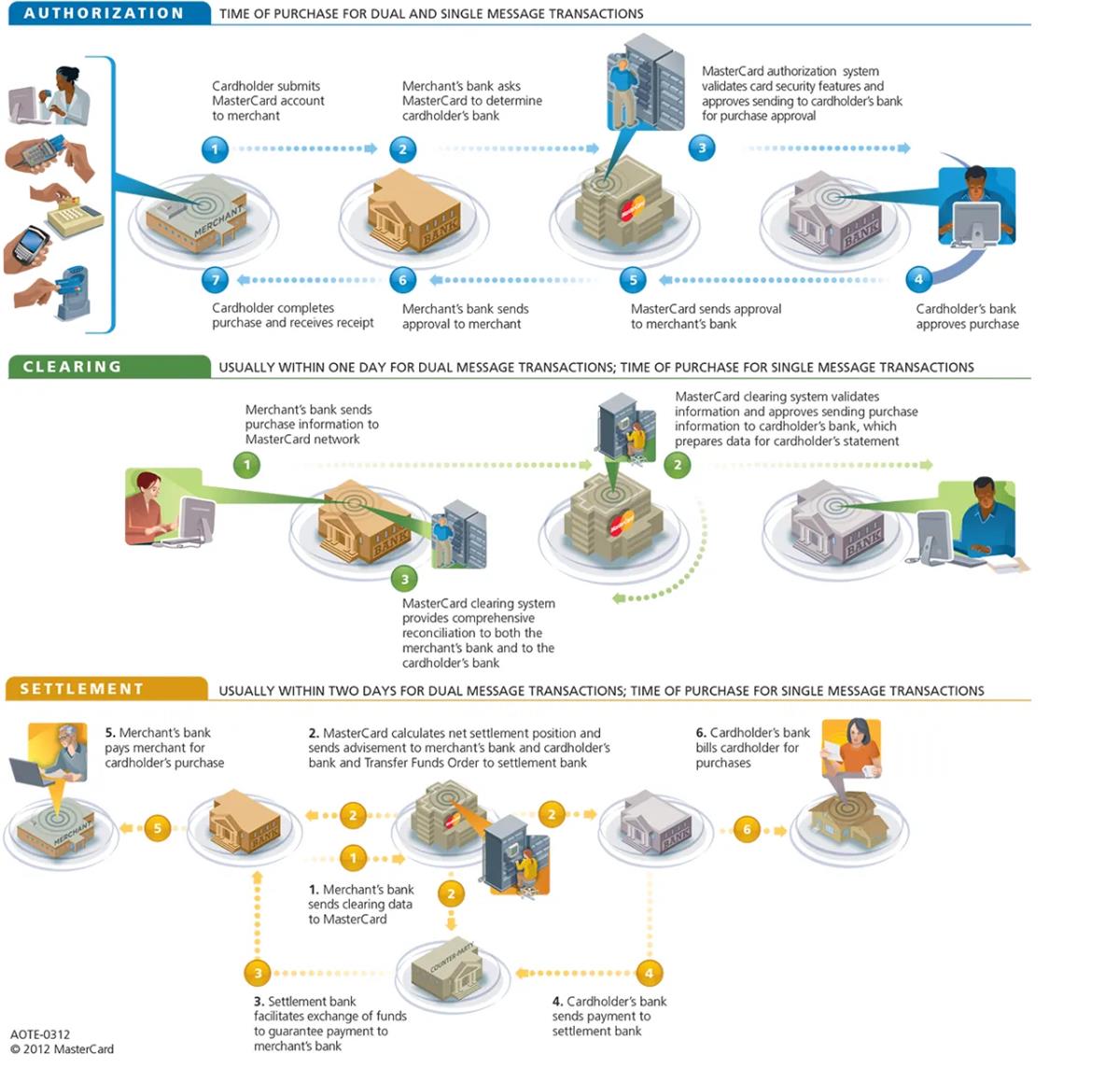

Here’s a quick primer: a credit card transaction involves three steps:

-

Authorization: At purchase, the acquirer and issuer verify the transaction via Visa to prevent fraud or overdrafts.

-

Clearing: Visa calculates net positions between issuer and acquirer.

-

Settlement: Visa sends instructions to clearing banks,

- which then transfer funds between acquirer and issuer accounts.

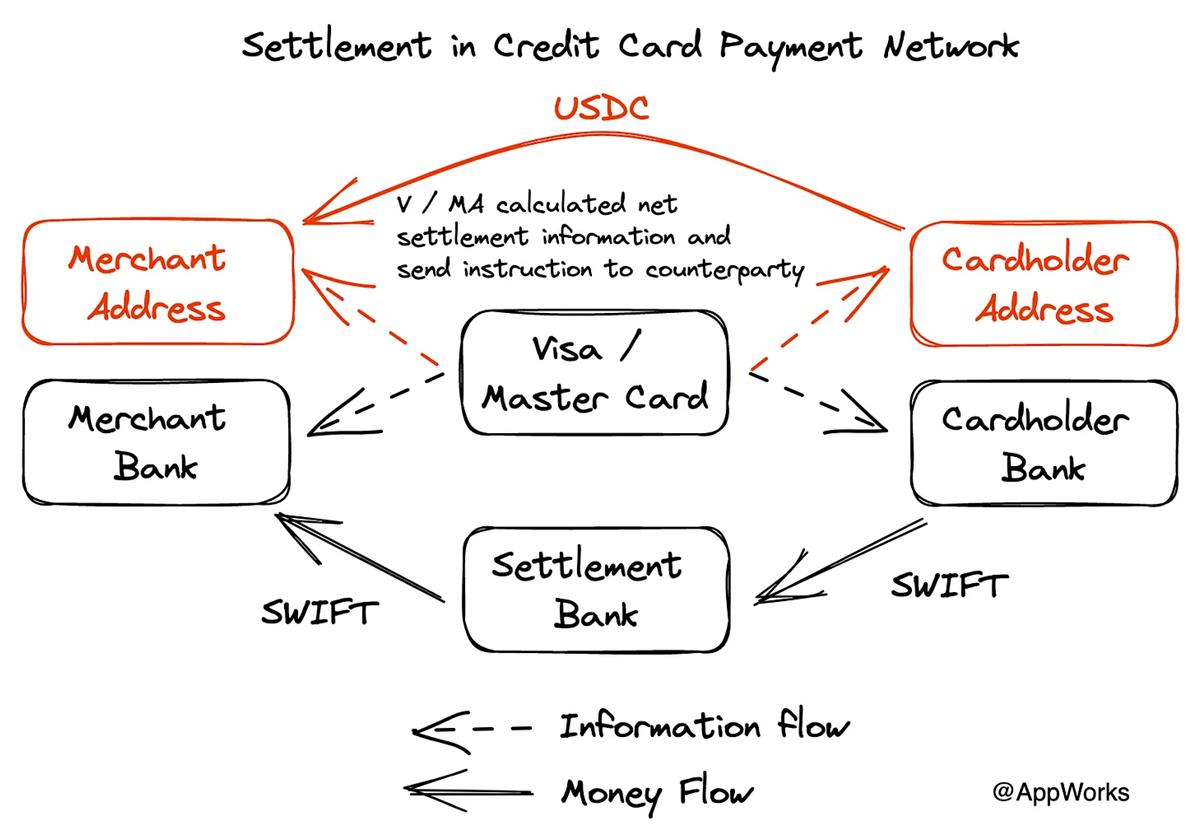

Visa aims to use blockchain specifically for Settlement. To address SWIFT’s shortcomings, Visa is actively testing USDC for faster, cheaper settlements—especially for cross-border payments. Sending $100 from the U.S. to Europe via PayPal incurs ~$7.75 in fees (including $4.80 transfer + $2.95 FX). Using USDC on a Layer 2, gas fees drop to ~$0.20. While FX costs remain, the pure transfer cost advantage is clear—not to mention vastly improved settlement speed.

If Visa widely adopts blockchain for settlement, settlement parties could shift from issuing/acquiring banks to simply “issuing addresses” and “acquiring addresses.” Clearing banks become unnecessary. Issuers don’t need to be banks or wait for banks to accept stablecoins on their balance sheets. Card issuance accelerates, off-ramp issues fade, and crypto liquidity flows more freely. A January 2023 Visa research paper on “Crypto Pull Payments using Account Abstraction” hints at this future—using addresses or smart contracts directly. Pull payments resemble credit cards, but today’s blockchain infrastructure struggles to support them. Account abstraction may offer a solution.

Visa and Mastercard’s true value will lie in fraud detection and prevention—leveraging bank data, user/merchant locations, spending history, and amounts to score risk, triggering 2FA/MFA when thresholds are exceeded.

So what stands in the way of Visa and Mastercard adopting stablecoin settlements? Key areas still needing development:

Issuers willing to support crypto/stablecoins—or Web3 projects (ideally wallets) capable of risk management—to issue more cards. Palladium (aiming to be a crypto-native neobank) and Stables (recently partnered with Mastercard) are good examples.

On-chain data tools for anti-fraud and AML services tailored to payment networks. Chainalysis and TRM Labs focus on AML, but payment networks need systems to detect stolen cards—i.e., compromised private keys or suspicious outgoing transfers—triggering 2FA/MFA. This space is still nascent, though teams are building such features into smart contract wallets. Sardine, dubbed Web3’s anti-fraud warrior, offers risk control for on/off ramps based on crypto/NFT fraud patterns. Chainsight, a Taiwan-based YC startup, is also active here.

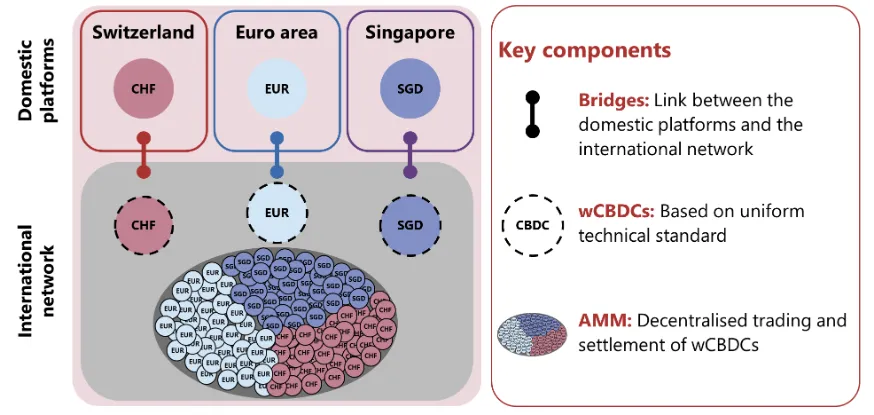

Liquidity for settling between stablecoins, USD, and local currencies. Visa and Mastercard sourcing USDC/USD liquidity from Circle isn’t an issue, but USDC-to-local-currency liquidity is. Insufficient liquidity increases slippage and costs. You could convert to USD first, but that drags traditional finance back in. Better: direct USDC/local currency swaps, or native on-chain versions of local currencies settled via blockchain, with DeFi providing liquidity. The Bank for International Settlements (BIS), known as the “central bank of central banks,” is exploring similar ideas in Project Mariana—see below, showing EUR, CHF, SGD liquidity via AMMs.

Problem 2: Payment agreements involve frequent disputes and high administrative costs

As we move past the pandemic into an AI-assisted era, the gig economy is maturing, and freelance markets are expected to grow rapidly. Freelancers and employers increasingly adopt formal payment agreements—Escrowed, Milestone, Recurring—to clarify terms, avoid disputes, and protect rights. These agreements are becoming common not just on freelance platforms, but also in e-commerce, DAO/Web3 community contributions, donations, and beyond.

Yet current payment agreements suffer from several issues:

- Unclear terms cause 64% of freelancers to experience delayed payments due to acceptance disputes.

- Freelance platforms charge 5–20% service fees plus 2.5–5% payment processing fees—very costly.

- Off-platform freelancers often face scams or frozen funds.

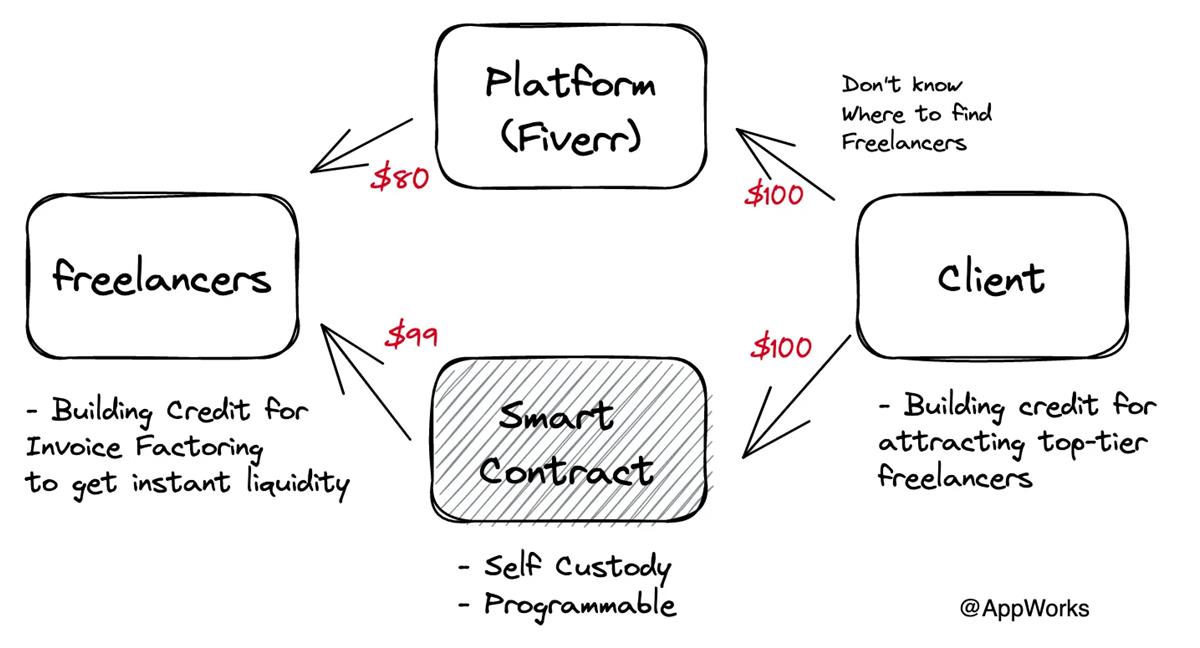

But if terms are encoded in smart contracts, payment triggers become instantaneous. With robust oracle integration, we could achieve automated milestone payments—e.g., performance payouts based on metrics like TVL growth—reducing freelancer payment delays. Using blockchain for settlement or escrow in smart contracts also slashes payment processing costs.

Blockchain-settled invoices can be minted as NFTs, serving as portable, platform-agnostic credit data. They can seamlessly integrate with social platforms, allowing employers to tap smaller communities. Once a credit system emerges, the tradability of NFT invoices opens doors to invoice factoring.

In short, blockchain reduces payment agreement costs—lower execution and escrow fees via smart contracts, higher efficiency through oracle automation. It also creates a portable reputation system tightly linked to cash flow and business data, enabling future financial services.

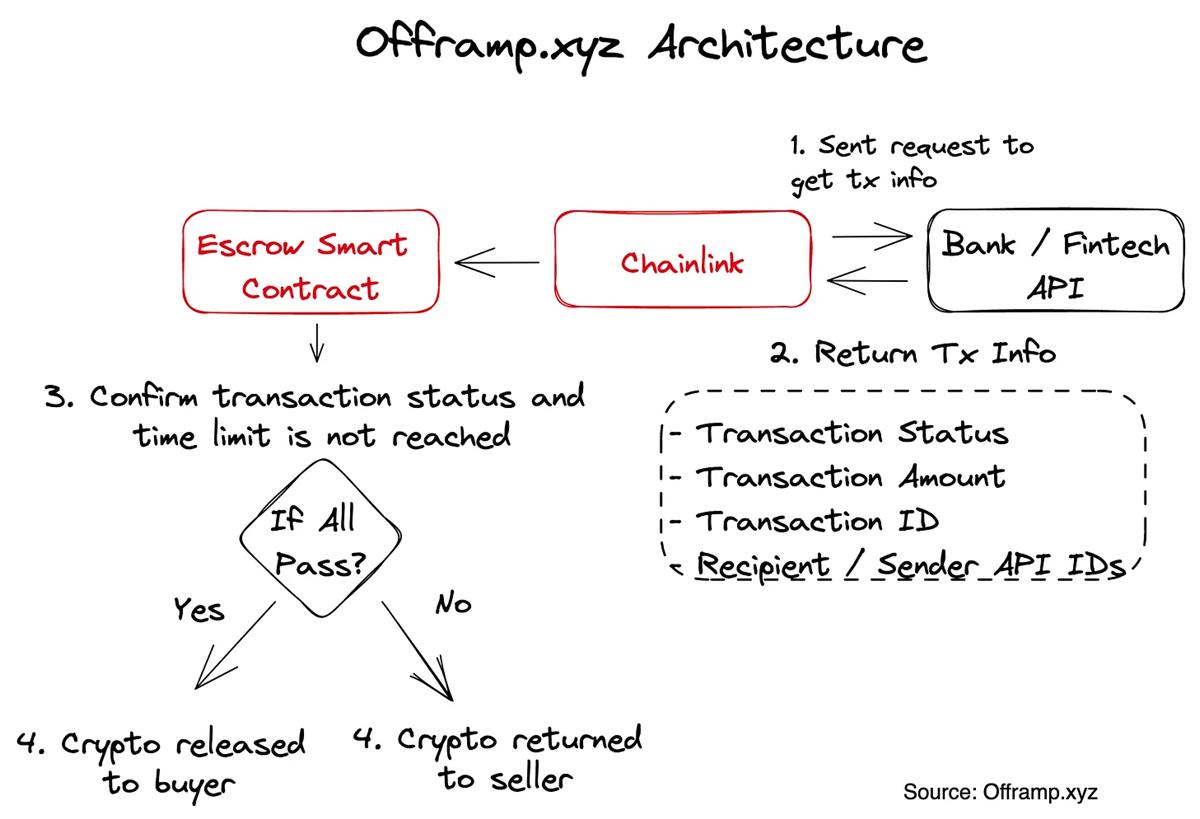

Beyond freelancers, we see promising integrations like Offramp.xyz, which combines Web2 data with Chainlink APIs to trigger escrowed smart contracts—an elegant off-ramp platform. As shown below, Offramp uses WISE’s API to confirm fiat receipt, feeds data on-chain via Chainlink, and triggers automatic crypto payments if conditions match. The entire payout takes just 20 seconds—a seamless experience. This is a great example of smart contracts + oracles for payment agreements. With broader bank and fintech API integration, liquidity could expand dramatically.

Still, challenges remain:

- How to enable more offline condition triggers for complex payment agreements? Chainlink offers data feeds beyond token prices—weather, sports, supply chains, IoT, and custom enterprise APIs. Offramp successfully used WISE’s data, but only benefits WISE users. Broader reach requires bank APIs or a universal Open Banking standard.

- Dispute resolution: If platforms auto-execute payments, they assume validation risk. This complexity makes dispute resolution services like Kleros (acting as juries) crucial. More reliable oracle data also reduces ambiguity in milestones, lowering dispute rates. Credit-building mechanisms can further reduce conflicts.

Problem 3: Recurring Payments are costly and administratively heavy

According to Stripe, about 18% of global online transactions are recurring payments—used for subscriptions, payroll, supplier payments (AR/AP), typically on annual, quarterly, or monthly cycles. Yet recurring payments face issues:

- Inflexible timing strains cash flow for employees and suppliers, leading to extra borrowing costs.

- Most online recurring payment infrastructure relies on credit card networks, charging 2–3% per transaction.

Crypto payments, with fast and cheap settlement, enable Stream Payments—allowing merchants, employees, suppliers, and investors to receive funds or tokens by the second, accelerating capital circulation and improving cash flow.

Of course, payers prefer to delay payments while recipients want them early—creating tension. So Stream Payments aren’t universally superior, but they add value in specific scenarios:

- Simplified company finance operations. Many crypto companies/DAOs use Request or Zebec to stream salaries to contributors—set once, run forever, eliminating monthly admin work.

- “Living paycheck to paycheck” individuals get paid instantly, reducing reliance on payday loans. In the U.S., one in five blue-collar workers borrows from payday lenders before next payday—at average interest rates of 200–700%. Streamed salaries could cut demand for such loans or at least reduce overdraft fees. A White House economic report estimates faster settlement could save low-income households $7 billion annually.

- Shorter subscription options—from monthly to per-second—could boost conversion. Flexible pricing and cycles meet diverse customer budgets. Short trials lower perceived risk, encouraging trial—e.g., Superfluid helps crypto businesses run crypto subscription models. Non-crypto businesses can join too, if seamless fiat onboarding is solved.

- Streamed token vesting lets investors receive tokens every second instead of monthly/quarterly. This reduces sell pressure and project liquidity management costs.

That said, most of these use cases are niche or offer marginal benefits. Stream Payments feel more like a “nice-to-have”—unlikely to drive mass adoption alone. To achieve 10x improvement, they must be integrated with other compelling features.

However, most Web2 services rely on Pull Payments (e.g., credit cards), where payees “pull” funds after authorization—requiring multiple verification steps (2FA/MFA) and generating significant fees. Crypto enables easy Push Payments for recurring billing. At scale, this could bypass Visa/Mastercard networks entirely, avoiding 2–3% fees. Given that 18% of global online transactions are recurring, the market opportunity is enormous.

Conclusion: Integrating Crypto Rails into Global Payment Networks

Crypto rails offer advantages: fast settlement, programmable payments under complex conditions, borderless clearing, cheap micropayments, and Stream Payments. But listing these perks won’t drive mass adoption.

We must dig deeper into unmet needs across different users. What do payers, payees, and merchants truly lack today?

Examples include: reducing reliance on payday loans via streamed wages; lowering cross-border e-commerce and remittance costs; simplifying milestone payments between platforms and freelancers; enabling efficient investor trading strategies via Stream Payments; faster interbank settlements via crypto rails.

But these are point solutions. The payment industry is mature. To compete with traditional players, crypto must not only offer rail advantages but also replicate existing services—AML, fraud detection, invoicing—and go further: on-chain fraud detection, comprehensive credit scoring from invoice data, privacy-preserving payments via ZK tech. Only then can we build 10x better products that truly solve real pain points!

If you’re a founder working in this space, believing blockchain can fix payments, please reach out to AppWorks or me! Industry veterans with differing views—your comments are welcome too!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News