When L1 becomes a complete ecosystem, will DeFi protocols still need native tokens?

TechFlow Selected TechFlow Selected

When L1 becomes a complete ecosystem, will DeFi protocols still need native tokens?

L1 tokens are the only tokens that should be invested in, and DeFi protocols should almost never launch their own tokens.

Written by: c-node

Translated by: TechFlow

Over the past few months, liquidity in the DeFi markets on copycat L1s has dried up. The community believes this is due to a lack of tokens people want to trade, and thus calls for developers to launch more tokens—such as protocol governance tokens or meme coins.

My view is that L1 tokens are the only tokens worth investing in, and DeFi protocols should almost never launch their own tokens. Protocols with governance are the worst kind, while those minimizing governance are generally better. You might object—concerned about contract immutability, changes in risk parameters, or oracle management.

You might also argue that protocol developers need incentives through token issuance, or must raise venture capital funding to enable token trading. Regardless, I aim to dispel all such concerns in this article.

How can DeFi be saved without a flood of new tokens?

For a DeFi ecosystem on a blockchain, nothing is better than having a strong native L1 token. Some claim deflationary economics are bad because they “encourage staking and discourage usage.” This is wrong—in blockchains and DeFi, staking is usage.

Users lock up their long-term holdings on-chain, often using DeFi to gain liquidity via collateralized decentralized stablecoins, synthetics, and derivative positions. DeFi enables them to do so without taking on centralized risks—like leaving long positions on exchanges or lending platforms such as Celsius—or bridge risks when moving assets across chains.

A major problem is solved: users can self-custody their long-term holdings while still engaging in many useful and interesting activities. This is an excellent outcome for long-term holders of the L1 token.

One might argue DeFi remains useful even without a strong native token. Indeed, you can use DeFi with wrapped and bridged assets, but it’s far less valuable than DeFi built around native assets.

Remember how SBF stole Bitcoin from Ren and Sollet? Even if you could avoid such risks, competing as the best place for non-native assets means going head-to-head with CeFi—and an endless stream of new L1s and L2s.

Some believe there’s still great value in decentralizing other parts of the financial supply chain—like execution and settlement—even without self-custody, benefiting from transparency and accountability, even if we can’t force CeFi intermediaries to comply. That’s true—but you don’t need something as complex as a public blockchain with decentralized validators and a native crypto token to achieve this.

What makes a native token strong?

aeyakovenko made a compelling argument that a blockchain will lose to competitors unless its fees are as low as possible. Low-fee chains earn revenue by selling priority access at a premium during high congestion, while near-zero base fees attract developer and user activity, creating hotspots and driving more chain revenue.

This is clever, but in practice, many popular transaction types create no state contention. Chains cannot extract maximum revenue from these, and base fees may rise significantly before users flee to cheaper alternatives. Base fees should be as high as possible—but clearly not so high that people can’t afford them.

It’s reasonable to expect users will always flock to the cheapest option, but a blockchain without a strong native token is far less useful. A decentralized stablecoin with a $0.01 transfer cost is more useful than a centralized one with zero fees, because the latter fails to free users from centralized financial intermediaries—their purpose remains unproven and speculative.

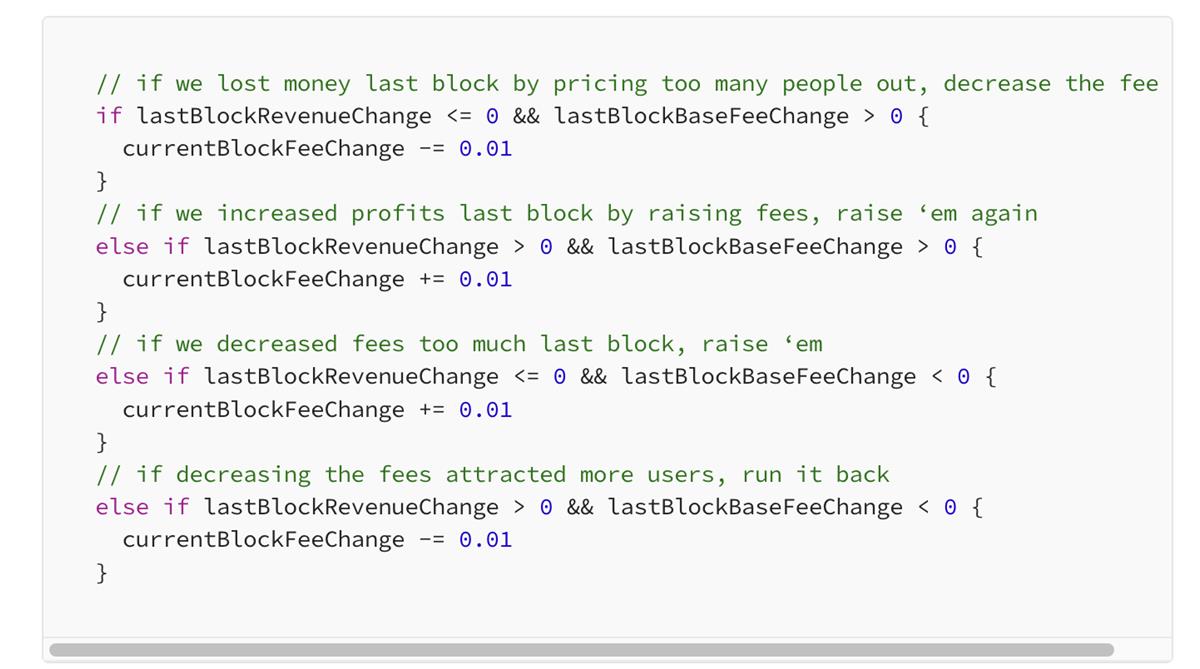

Base fees could be dynamically priced to maximize revenue per block. Control theory should guide the design of such pricing algorithms. A naive example (ignoring control theory) might look like this:

Secondly, if all value accrues to stakers rather than non-staked tokens, it becomes difficult to leverage that native value within DeFi. Staked tokens can be reused in DeFi via Liquid Staking Tokens (LSTs), but current LST designs have issues. Some of the most popular LSTs are closed-source and controlled by multisigs or oligarchic DAOs. While decentralized LST proposals exist and work in principle, it’s a hard problem due to varying risk profiles across different validator stakes.

Fun fact: If a chain is a sovereign rollup, it doesn’t need validators or staking, and all revenue can accrue directly to non-staked tokens.

Don’t protocols need tokens to create value?

On-chain governance is inherently oligarchic. Cryptocurrencies should be autonomous and independent, requiring no human intervention to govern them. The best approach is to minimize governance. MakerDAO voted to make USDC—a centralized asset—its primary collateral, turning DAI into a token resembling a CeFi platform. In contrast, the immutable, governance-free LUSD perfectly combines the utility of USD with the functionality of decentralized crypto.

Some protocols, like Aave, use a DAO to control key risk parameters. I have no perfect answer—this may be unavoidable, which is unfortunate, but automation of these parameters might eventually be feasible.

A frequently overlooked downside of launching protocol tokens is misalignment with the L1 and the creation of perverse incentives for developers. The cycle is clear: create a protocol, issue a token with incentives, insiders dump, users complain, resentment builds, and everyone moves to the next protocol with new insiders. This loop is destroying the space.

How many lending protocols exist now? It seems a new lending and DEX protocol launches every month. Imagine if every Microsoft Word update were released as a brand-new word processor—absurd. The real motivation behind launching new protocols is rarely to fix prior flaws, but because some developers weren’t insiders in the last rug pull and now want to be insiders in the next one to profit from dumping.

It would be far better if all DeFi developers on an L1 united around standardized versions of DEXs, lending, synthetic stablecoins, etc., fully aligned with the L1—without accruing value to unnecessary tokens. This would eliminate incentives for fragmented ecosystems, reduce complexity, and curb the uglier aspects of human nature.

Once protocols are truly fully aligned with the L1, they could be embedded directly into the blockchain. While this may sound extreme, it solves many critical problems and should be explored as a potential solution to DeFi’s biggest challenges.

First, it allows protocols to be governed and upgraded without governance tokens. Off-chain governance, similar to EIPs, is more meritocratic, autonomous, and voluntary—contrasting sharply with token-based governance.

Second, it makes protocols more resilient to code bugs in smart contracts, as they benefit from client diversity. Protecting smart contracts from vulnerabilities is hard. Formal verification is slow and difficult; regular security audits are not a silver bullet. Hacks are devastating and remain a major unresolved issue in crypto, attracting negative attention. While extreme, perhaps it’s time to explore embedding DeFi into the blockchain itself as a solution to this persistent problem.

How can developers profit from building L1-aligned protocols?

Simply: they profit by holding the L1 token long-term. They could receive L1 token grants from whales, who are incentivized to fund such development to boost their own investment value. They could also raise cash from institutional-level L1 whales, or these whales could directly hire developers to build embedded protocols—profiting from increased utility for their L1.

Asking “If I can’t get rich issuing a token, why build a protocol?” is meaningless. If I could gain asymmetric benefits from visiting my grandmother, I’d visit her more often—but the world doesn’t work that way. Just because you wish protocol development were a path to wealth doesn’t mean it is or ever will be. A few lucky developers got rich during past irrational bubbles via token issuance—sometimes dishonestly—while consistently fragmenting the L1 ecosystem.

While governance rights over risk parameters may hold significant value—justifying high valuations of governance tokens—most DeFi tokens are essentially meme coins, filled with incoherent narratives.

Beyond governance rights, DeFi protocols have no need for tokenized scarce resources (DePIN might be an exception). Compared to L1 tokens—which have clear utility and purpose—there’s little reason not to rally around the L1 token and grow wealthy together.

“You’re describing a Ponzi scheme.”

Yes, as I’ve described so far, that’s correct.

But don’t forget: cryptocurrencies existed and held value for years before DeFi emerged. They served as convenient digital payment solutions, often offering better privacy, censorship resistance, and borderless transactions than centralized alternatives.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News