Exploring the Impact of the Shapella Upgrade on ETH Staking Yields, Competitive Landscape, and the Influence of LSDfi on Its Ecosystem

TechFlow Selected TechFlow Selected

Exploring the Impact of the Shapella Upgrade on ETH Staking Yields, Competitive Landscape, and the Influence of LSDfi on Its Ecosystem

This article will discuss potential future changes in ETH staking yields, the competitive landscape within the staking sector, and the potential impact of LSDfi on the ETH staking ecosystem.

Author: Lawrence Lee

On April 13, 2023, Ethereum's Shapella upgrade—comprising the Shanghai execution layer and Capella consensus layer—officially launched, primarily enabling the withdrawal of staked ETH. With this upgrade, Ethereum’s transition to Proof-of-Stake (PoS) can finally be considered “complete.” In this article, we will explore potential future changes in ETH staking yields, examine competitive dynamics within the staking sector, and analyze the potential impact of LSDfi on the ETH staking ecosystem.

The Past and Present of ETH Staking

Before proceeding, let us briefly review ETH staking. Unlike most existing PoS blockchains, Ethereum does not support native delegation and limits the maximum economically viable stake per validator node to 32 ETH. This design clearly aims to minimize the risk of any single entity controlling consensus by operating a large number of nodes, thereby preserving Ethereum’s decentralization. However, due to the high operational complexity of running a node, beyond solo staking (where users manage everything themselves), three additional staking models have gradually emerged in practice: staking pools, liquid staking, and CEX staking. The characteristics of these four methods are as follows:

-

Solo staking requires users to handle all aspects of staking setup and maintenance. Its main drawback is the high barrier in terms of hardware, capital, technical knowledge, and network stability.

-

Staking pools reduce the need for users to manage networking and hardware. Users pay a fee to professional staking service providers who stake their 32 ETH on their behalf. Withdrawal private keys remain under the user’s control, ensuring strong custody over funds. However, this method still demands significant capital and technical understanding from users. In some classifications, this model is referred to as Staking-as-a-Service (SaaS).

-

Liquid staking goes further than SaaS by aggregating users’ ETH into a shared staking pool, allowing participation with any amount. In return, users receive a liquid staking derivative (LSD)—a token representing their staked position. These LSDs have become widely used across DeFi, which we will detail later. However, since all staked ETH belongs to the pool’s smart contract, users must trust the liquid staking protocol. This approach is sometimes called Pooled Staking.

-

CEX staking involves centralized exchanges handling the entire staking process. It allows staking of any amount and typically issues staking tokens (e.g., Coinbase’s cbETH, Binance’s bETH) to users.

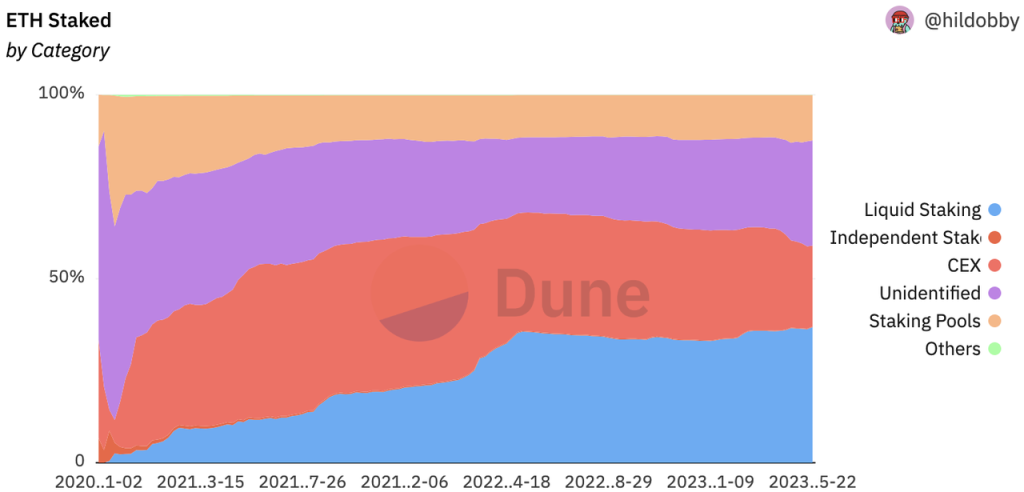

Below: Historical distribution of ETH staking share by provider

Source:https://dune.com/hildobby/eth2-staking (Note: Due to statistical complexity, solo staking share is difficult to measure directly. Most staking categorizations include an "Unidentified" category—as shown above. According to recent analysis by Rated, approximately 6.5% of total staked ETH comes from solo stakers.)

From the chart, we can clearly see that aside from the first two months after the Beacon Chain launch, CEX staking quickly became dominant until April 2022—largely because centralized exchanges already held vast amounts of user ETH and offered staking as a natural yield-generating option. This trend was not what the Ethereum Foundation or community members desired. However, with institutional backing such as Paradigm investing in Lido, and stETH building strong liquidity and composability in DeFi, Lido rapidly gained traction, catalyzing broader growth in the liquid staking sector. Today, liquid staking remains the leading model.

After the successful Shapella upgrade, CEX staking market share declined noticeably, with many users migrating their stakes to liquid staking platforms and solo staking (reflected in the "Unidentified" category).

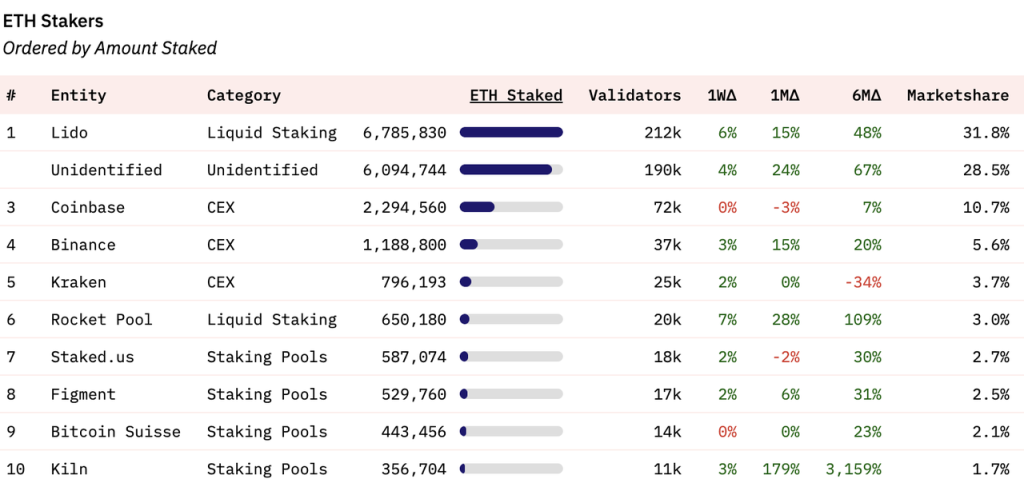

In terms of specific staking entities, Lido currently holds 31.8% of total staked ETH, ranking first. Positions 3–5 are occupied by three centralized exchanges. Rocket Pool, another liquid staking provider, ranks sixth, while positions 7–10 are held by staking pools.

Source:https://dune.com/hildobby/eth2-staking

Future of ETH Staking Yields

Staking yield is a key factor influencing user participation. To understand the future of ETH staking, we must examine how staking rewards are structured and how they may evolve. After The Merge, validators earn rewards from both the consensus layer and the execution layer. Currently, the combined APR stands at around 5.4%.

Source https://ethereum.org/en/staking/

Consensus layer rewards come from newly minted ETH, increasing in total issuance as more ETH is staked—but the APR decreases as total staked ETH rises. Currently, consensus layer APR is about 3.4%. Market estimates suggest ETH staking rates will reach 25–30% by year-end. At 30% staking, consensus layer APR would drop to roughly 2.4%. This is significantly lower than most other PoS chains and reflects the Ethereum Foundation’s principle of minimizing ETH issuance.

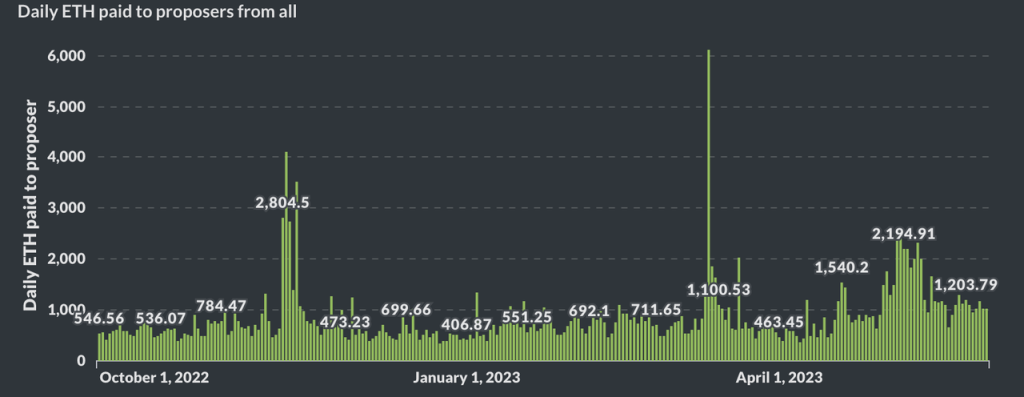

Execution layer rewards consist of two components: priority fees (the portion of gas fees not burned) and MEV (Maximal Extractable Value). Crucially, these do not scale with the amount of staked ETH—they represent the primary variable in staking returns, warranting deeper analysis.

Source https://transparency.flashbots.net/

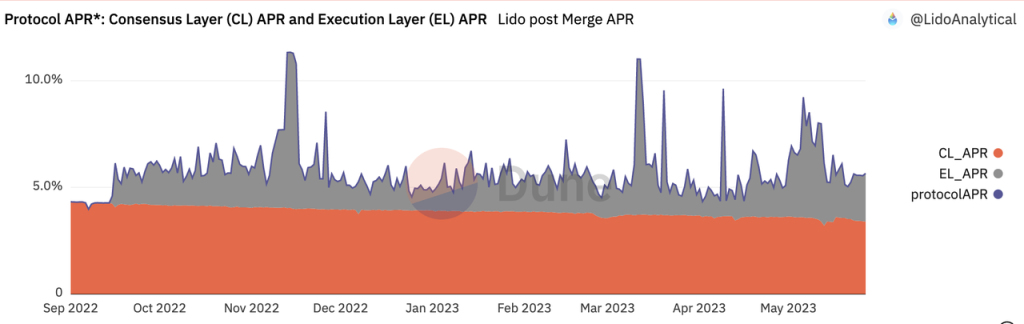

Source:https://dune.com/LidoAnalytical/lido-execution-layer-rewards CL_APR represents consensus layer yield; EL_APR represents execution layer yield.

Flashbots has tracked proposer (validator) total income since The Merge. Lido also provides data on its consensus and execution layer APRs, showing similar trends. Using Lido’s data for deeper analysis: post-Merge, consensus layer APR has slowly declined with rising staked supply, while execution layer APR fluctuates more widely, averaging around 1.5%, bringing total staking yield to ~5%. During periods of high on-chain activity (e.g., May’s meme coin season), execution layer APR can even exceed consensus layer rewards, pushing total staking APR close to 10%. As the de facto “risk-free rate” of Ethereum (see Mint Clips | How Should We Define the Native Risk-Free Rate in Crypto?), staking yield holds immense appeal for ETH holders.

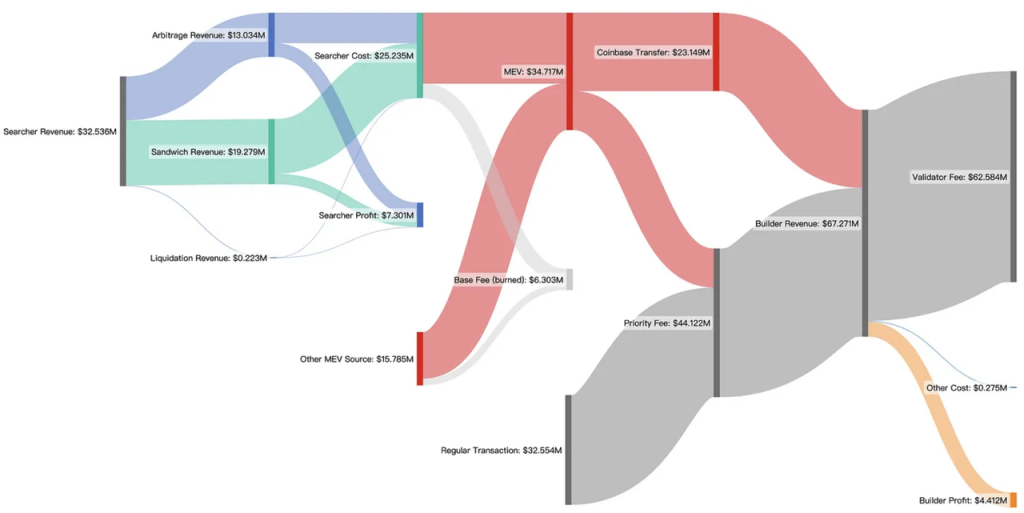

How might execution layer rewards evolve? First, we examine the breakdown between priority fees and MEV. Consider Eigenphi’s detailed analysis of Ethereum’s execution layer revenue distribution from January to February 2023:

Source:https://eigenphi.substack.com/p/value-allocation-in-mev-supply-chain

Over two months, priority fees and MEV contributed roughly 55% (44.12M) and 45% (34.72M) respectively to validator execution layer income.

Now let us assess future trends in priority fees and MEV.

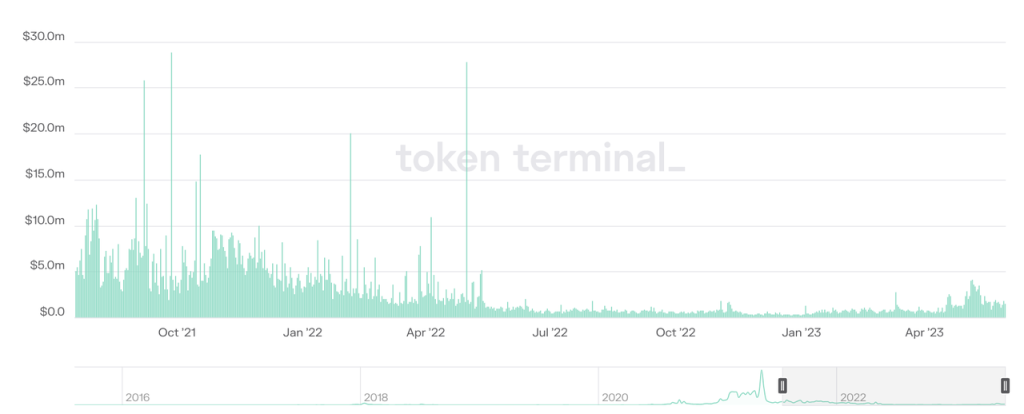

Ethereum Priority Fees Source:https://tokenterminal.com/terminal/projects/ethereum

Priority fees have closely followed market cycles since EIP-1559. During the 2021 bull run, daily priority fees approached $10M. In the 2022 bear market, they averaged ~$800K/day. During May 2023’s Meme Season, they reached ~$3M/day. Going forward, priority fees will continue to fluctuate with market activity and remain denominated in ETH.

MEV is more complex. Beyond opaque on-chain flows, it mainly consists of arbitrage, sandwich attacks, and liquidations. There is limited public data on MEV trends post-Merge. However, the Ethereum Foundation has long expressed skepticism toward MEV. A year ago, they proposed PBS (Proposer-Builder Separation), partly to mitigate MEV’s disproportionate impact on small stakers. Recently, Ethereum researcher Justin Drake introduced MEV burn, proposing to fully burn MEV over the next 3–5 years, turning it into a deflationary force. While still conceptual and involving major trade-offs, Ethereum’s successful shift from PoW to PoS demonstrates its ability to align key stakeholders behind long-term roadmap goals—even at short-term cost.

Thus, MEV—which currently accounts for ~20% of total staking rewards—is likely to shrink or disappear in the medium to long term, as it contradicts the Ethereum Foundation’s values.

Another marginal but important factor is Layer 2 (L2). Under Ethereum’s rollup-centric roadmap, increasing transaction volume will migrate from L1 to L2, inevitably reducing MEV and priority fees on the mainnet. Currently, L2-generated MEV and fees are retained by L2s and do not benefit Ethereum validators. Especially after the upcoming Cancun upgrade reduces L2 costs further, L2 adoption may accelerate, potentially lowering total L1 fee+MEV income.

In summary, factoring in MEV burn and L2 migration, when ETH staking reaches 30%, total staking yield could fall to around 3% (2.4% consensus layer + 0.6% execution layer). Such a low yield would significantly dampen user enthusiasm for staking.

Liquid Staking Will Remain Dominant, Possibly Becoming Even More Concentrated

The Shapella upgrade enabled ETH withdrawals, granting liquidity to ETH staked via solo staking and staking pools. Liquid staking rose to prominence during 2021–2022 precisely because LSDs provided liquidity—effectively enabling pseudo-withdrawals. Thus, Shapella diminished one of liquid staking’s core advantages. While solo staking remains technically demanding, tooling for solo stakers is improving, lowering barriers. Moreover, solo staking is ideologically aligned with Ethereum’s decentralization ethos and enjoys strong support from the Ethereum Foundation.

Why then do we believe liquid staking will retain—and possibly strengthen—its dominance?

The answer lies in composability. LSDs offer superior composability, enabling higher yields and capital efficiency. Staking participants are inherently yield-sensitive and tend to choose options offering better returns. Thanks to their composable nature, LSDs effectively deliver higher net yields.

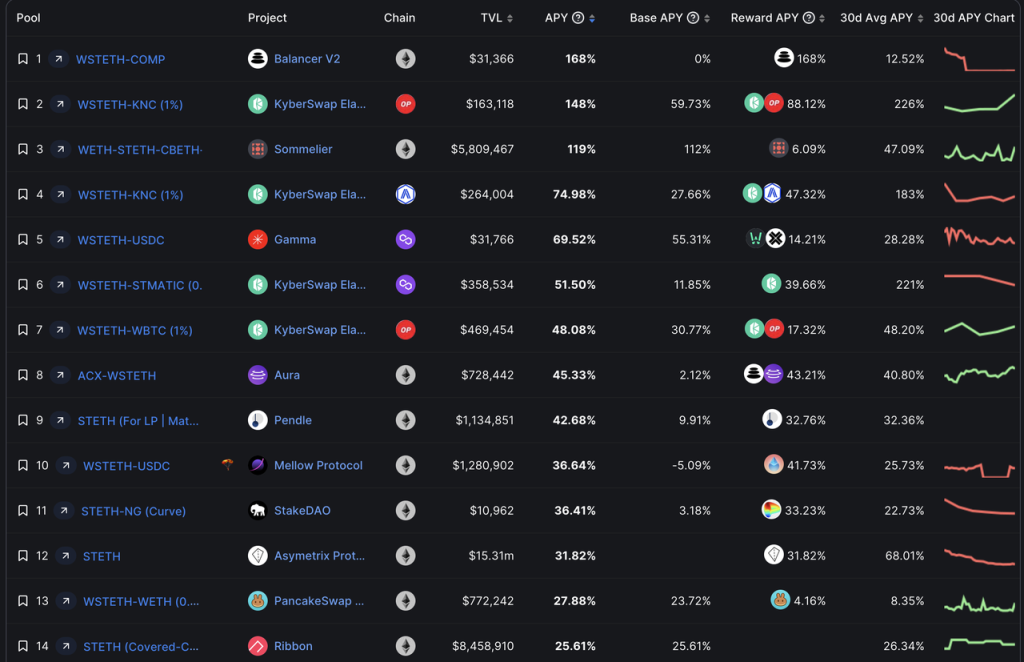

At a base staking APR of 5.6%, LSDs can easily achieve 10%+ APR. Take Lido’s stETH as an example:

Source:https://defillama.com/yields?token=STETH

Currently, stETH LP positions can easily generate over 50% APR. Even accounting for paired asset exposure, net APR exceeds 25%. Single-sided stETH positions on platforms like Asymetrix (an LSD-themed Pool Together) and Ribbon (options protocol) also yield over 25% APR (albeit with certain risks). When combined with stETH’s base 5.6% staking yield, total returns via Lido can reach ~30%.

Beyond high yields, stETH is deeply integrated into blue-chip DeFi protocols: Maker, Aave, and Compound all accept stETH (or wstETH) as collateral with parameters close to ETH. The Curve stETH-ETH pool maintains over $1.1B in liquidity, making it easy to swap or borrow against stETH.

These advantages are absent in solo staking and staking pools. Particularly if staking yield drops to 3% as projected, users may find the effort required for solo or pooled staking unjustifiable compared to simpler, higher-yielding alternatives.

Ethereum community members value decentralization—but they also consider opportunity cost. “Maintaining Ethereum’s decentralization is important and cool—but I’d still rather earn 30%.”

LSD and LSDfi

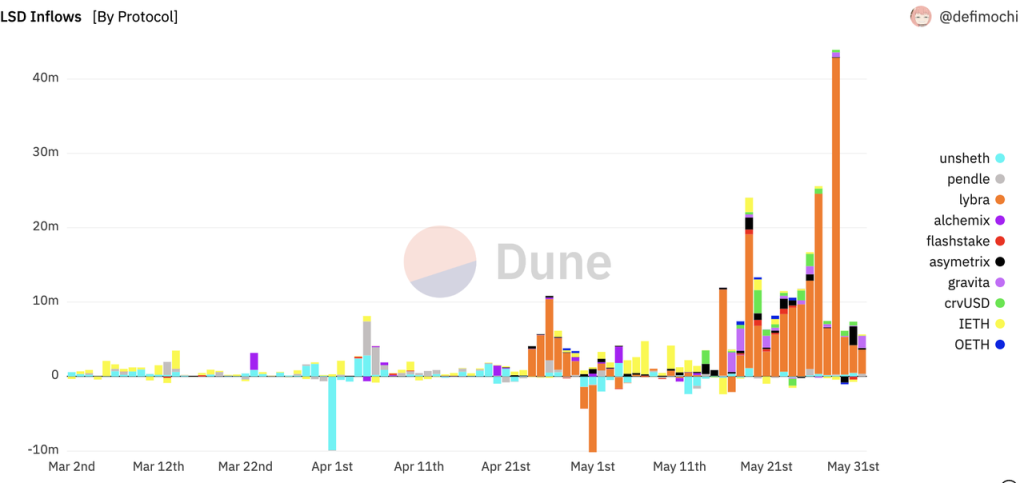

After Shapella, numerous LSDfi projects emerged, attracting LSD deposits for various financial applications. Many anticipate an “LSDfi summer.”

Source:https://dune.com/defimochi/lsdfi-summer

We won’t evaluate individual LSDfi projects here, as LSDfi doesn’t introduce fundamentally new business models—it simply enables LSDs as collateral across existing ones. These protocols still operate in stablecoins, yield aggregation, DEXs, or interest rate markets. Their success depends on their understanding of those respective markets. Among launched LSDfi projects, few have moved beyond forks or basic yield farming mechanics. That said, many promising LSDfi projects remain unreleased, and we look forward to future innovation built on LSDs.

What we want to discuss is LSDfi’s impact on the broader staking industry.

LSD holders share two traits: they hold ETH on-chain and understand DeFi; and they are yield-sensitive (hence their decision to stake). These traits make them ideal target users for any DeFi entrepreneur: they can interact on-chain and understand new products; they respond strongly to incentives. In today’s relatively mature DeFi landscape, many ETH holders still only hold ETH on centralized exchanges.

Source:https://etherscan.io/accounts

This LSDfi wave will bring new LSD projects online, each launching with fresh tokens and marketing budgets. What happened on unshETH, Agility, and Lybra may replay across multiple LSDfi platforms in the next 3–6 months. LSDs may consistently offer APRs far exceeding ETH’s on-chain yield, creating a self-reinforcing flywheel: more LSDfi → higher yields → greater incentive for ETH holders to convert to LSD → more LSD attracts more DeFi protocols seeking user acquisition → even more LSDfi. Eventually, nearly every DeFi protocol could be considered a form of LSDfi, as most already integrate LSDs to some degree. Clearly, LSDs capture the beta of LSDfi’s growth. The rise of LSDfi will further consolidate liquid staking’s dominance in the overall staking landscape.

The Ethereum Foundation’s Stance

Regarding staking, the Ethereum Foundation’s stance includes the following points:

-

It does not want too much ETH staked. Excessive staking increases ETH issuance, contradicting Ethereum’s long-standing principle of “minimal viable issuance.” It also reduces Ethereum’s economic bandwidth (a concept introduced by Bankless), referring to the Layer 1 circulating market cap that supports all dApps above it.

-

It views MEV negatively. For each validator, MEV represents rare but massive windfall gains. Without intervention, this could lead to coercive centralization (as seen in PoW mining pools for BTC and ETH), forming new alliances atop Ethereum’s consensus (e.g., MEV-boost), introducing unnecessary and potentially unsafe complexity. In the medium to long term, the Foundation aims to burn MEV, transforming it from a privilege of select validators into a shared benefit for all ETH holders.

-

It does not want any single LSD to become so dominant that it effectively replaces ETH on Ethereum. This would introduce new security risks.

Underlying these positions is a desire to preserve a decentralized consensus layer, maintain ETH as the primary native collateral asset, and prevent Ethereum’s consensus from being influenced by higher-layer protocols.

Source https://ultrasound.money/

stETH is currently the largest non-native, non-stablecoin asset on Ethereum. USDT and USDC rank higher but rely on off-chain credit (Tether and Circle). If they fail, they could harm Ethereum—but not erode Ethereum’s own credibility.

stETH is different. It is now nearly universally accepted across DeFi protocols as collateral comparable to ETH. Consider a thought experiment: if Lido Finance’s contracts were hacked and all Beacon Chain withdrawal keys compromised, would Ethereum need to hard fork, as in the DAO incident?

No one wants that scenario. This explains why the Ethereum Foundation actively supports solo staking, why the community debates limiting Lido’s size, and why Lido prioritizes decentralization. But the emergence of a dominant liquid staking provider isn’t due to malicious centralization—it’s the natural outcome of market dynamics. Even if the Foundation or core community restricts Lido, another “Mido” or “Nido” would emerge as the new Schelling point for staking.

We face two possible worlds:

-

The world envisioned by the Ethereum Foundation: moderate ETH staking sufficient for security, with most ETH remaining liquid on L1 to power dApps, and solo stakers forming the backbone of consensus.

-

The world we are likely to see: driven by one or a few dominant LSDs, more ETH flows into liquid staking. These LSDs become the primary collateral across dApps—effectively becoming “ETH” in practice.

Judging from current trends, the second scenario is far more probable.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News