Derivatives DEX Chronicles: Kwenta and Level Surpass GMX in Weekly Trading Volume

TechFlow Selected TechFlow Selected

Derivatives DEX Chronicles: Kwenta and Level Surpass GMX in Weekly Trading Volume

In the DEX for derivatives using the liquidity pool model, GMX has been challenged by Kwenta and Level. This week, Kwenta and Level surpassed GMX in trading volume.

Author: Duo Duo, LD Capital Research

The derivatives DEX sector is currently highly competitive, with overall market trading volume declining while new protocols continue to launch. In this low-volume environment, traders are increasingly sensitive to various incentives and yields, intensifying the competition among derivatives DEXs for users.

Since late March, the total trading volume of derivatives DEXs has been on a downward trend. Among six major derivatives DEX protocols, five have seen declining volumes, with only Kwenta showing counter-trend growth.

Kwenta is a perp frontend built on Synthetix and accounts for over 95% of Synthetix's trading volume and revenue growth. Synthetix itself is a liquidity provision protocol with over $400 million in TVL, supplying liquidity pools to frontends like Kwenta.

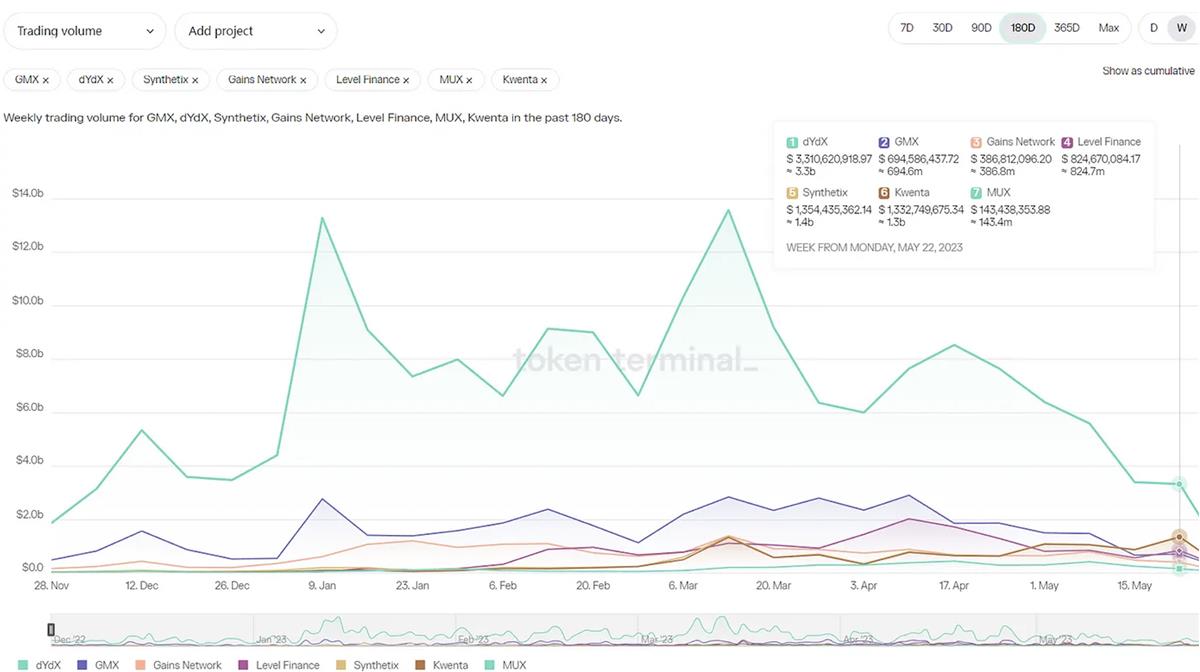

Chart: Weekly trading volume of major derivatives DEXs

Source:tokenterminal

Data in this article primarily comes from tokenterminal. Due to different measurement methodologies, statistics may vary across platforms.

DYDX, which uses an orderbook model, still accounts for nearly half of the entire market’s trading volume. However, within the pool-based derivatives DEX segment, GMX faces increasing competition from Kwenta and Level. This week, Kwenta and Level surpassed GMX in trading volume.

Table: Weekly trading volume of major derivatives DEXs since April (in mln USD)

Source:tokenterminal

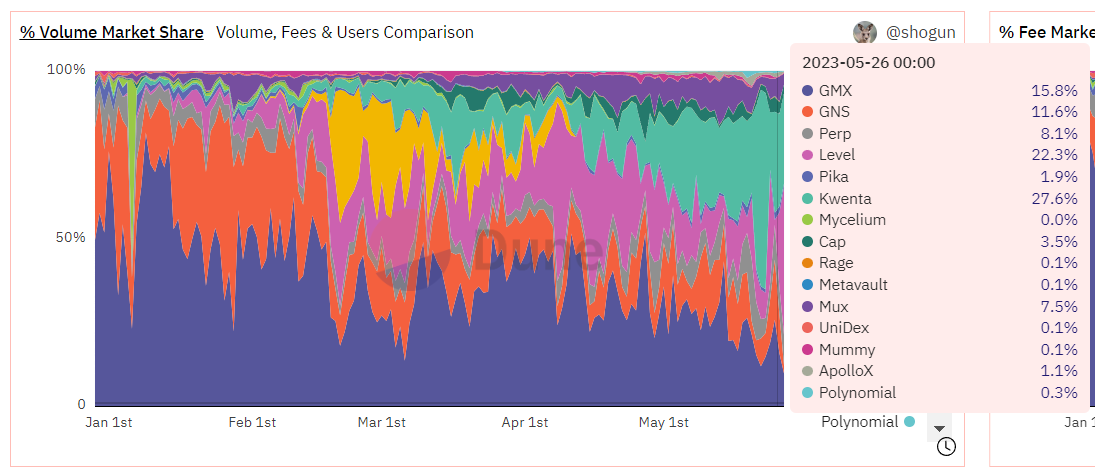

Chart: Market share distribution of pool-based derivatives DEXs

Source:Dune Analytics

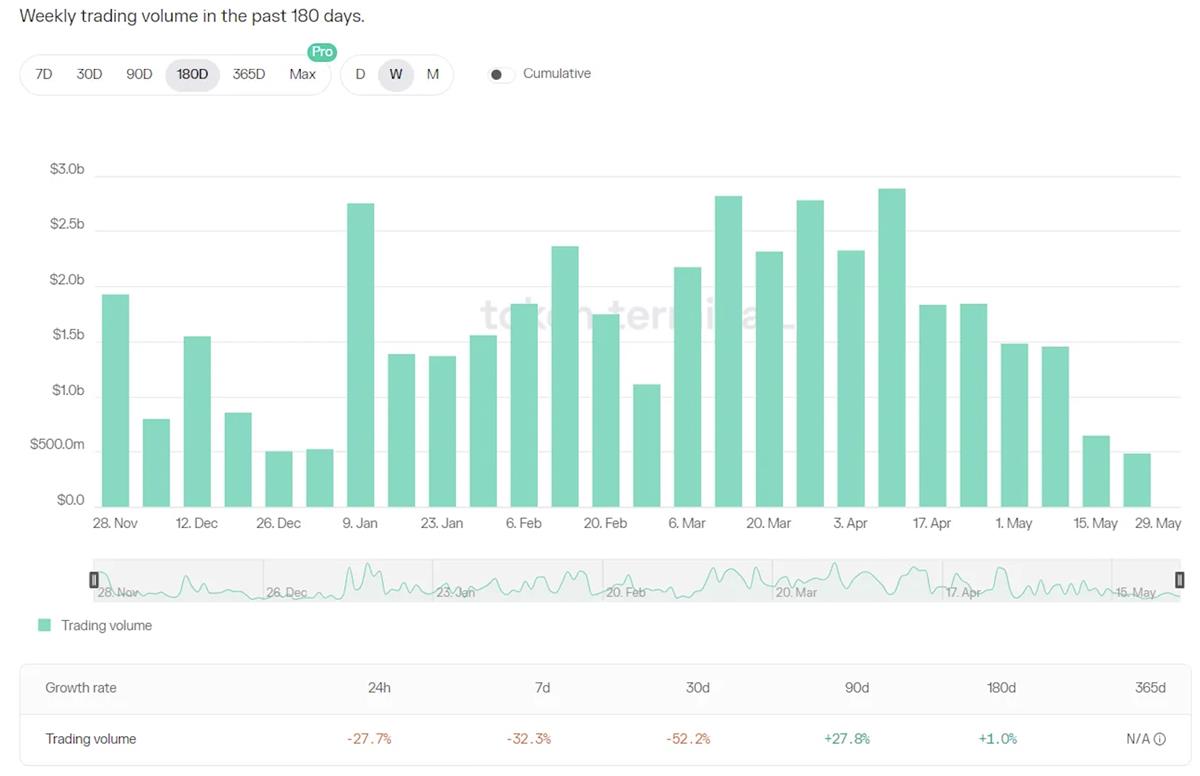

GMX’s trading volume peaked in mid-April and has since shown a continuous decline, now comparable to levels seen at the end of 2022.

Chart: Weekly trading volume trends for GMX

Source:tokenterminal

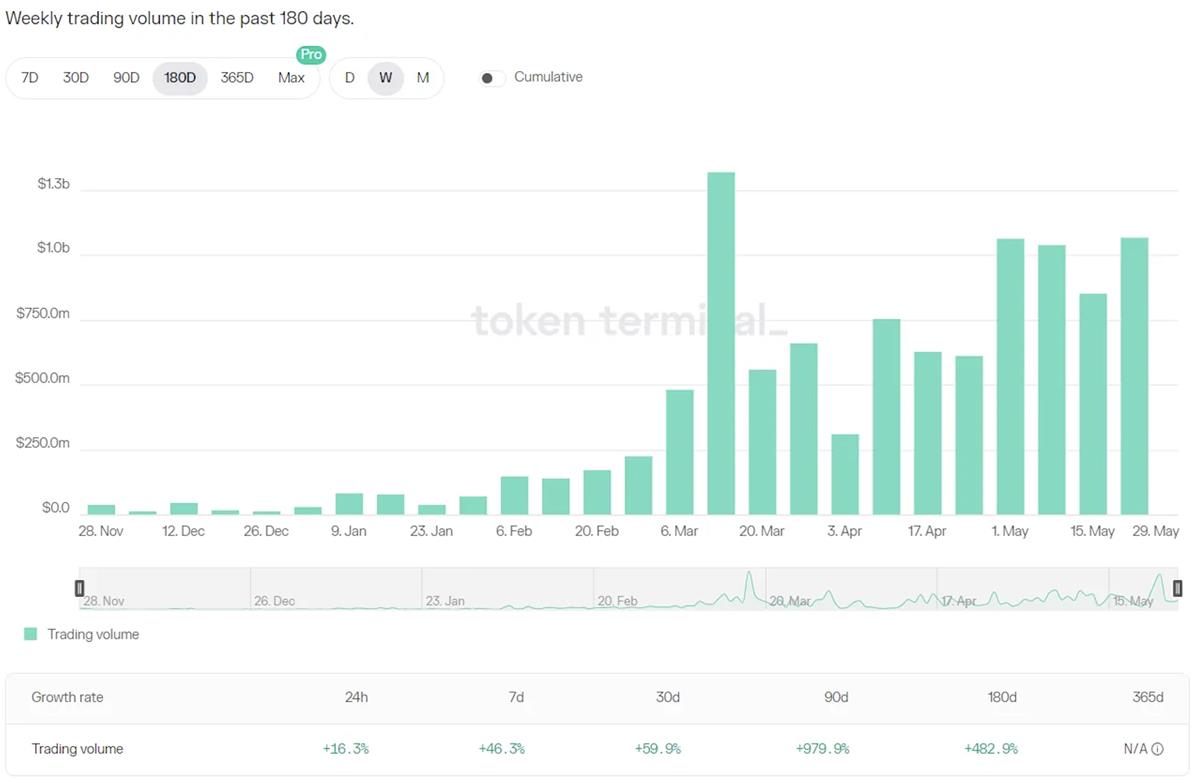

Kwenta, launched at the end of 2022, began running trading incentive campaigns starting mid-February, leading to significant volume growth. From late April, it started using OP tokens as incentives, resulting in noticeable volume growth in May.

Chart: Weekly trading volume trends for Kwenta

Source:tokenterminal

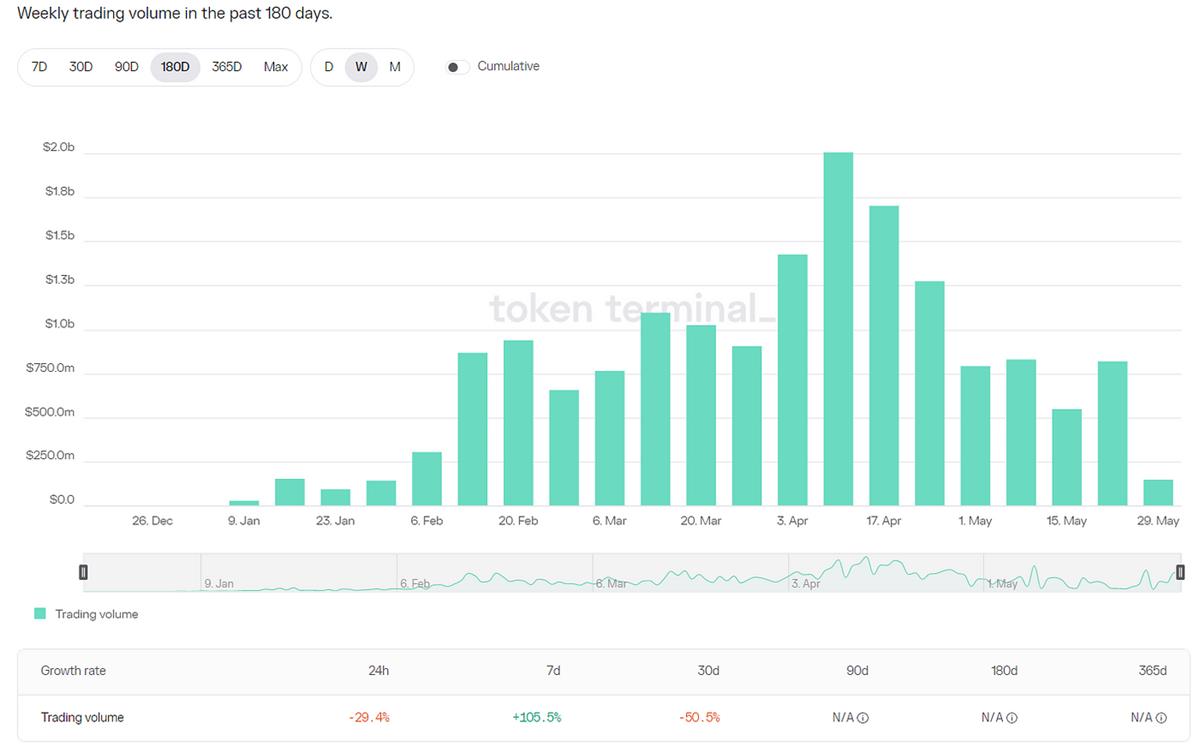

Level also reached its peak trading volume in mid-April, hitting $2 billion in weekly volume before declining. However, it rebounded during the week of May 22.

Chart: Weekly trading volume trends for Level

Source:tokenterminal

Reasons Behind Volume Growth: Higher Incentives, Lower Costs

Kwenta’s counter-trend volume growth may be attributed to two main factors: first, substantial trading incentives. In addition to its native token rewards, Kwenta began distributing 130,000 OP tokens weekly starting April 26, increasing to 330,000 OP per week from May 10 to August 30—worth approximately $500,000 weekly.

Second, Kwenta offers lower trading fees than GMX—currently ranging from 0.02% to 0.06%, depending on taker or maker status. GMX charges a flat 0.1% fee plus funding rates based on position holding. After excluding purely bot-driven volume, real users face significantly lower trading costs on Kwenta.

Chart: Kwenta trading incentive structure

Source:mirror.xyz/kwenta.eth

Level also implements trading incentives. For every $1 paid in trading fees, users receive one LEVEL Loyalty token (lyLVL). A total of 10,000 LVL tokens are distributed daily based on each user’s proportion of total lyLVL holdings. Rewards must be claimed within 24 hours.

In addition to base rewards, there is a Ladder reward mechanism. When daily platform revenue exceeds certain thresholds, additional LVL tokens are allocated as extra incentives. These accumulate and are distributed weekly.

Note: Tier n = (Revenue - $100,000) / $50,000

Source: LD Capital

The Ladder rewards target the top 20 traders on the weekly leaderboard. Rankings are determined by points earned through fee contributions, multiplied by a boost factor. The boost depends on the total amount of LVL staked on the platform—each 1,000 LVL staked increases the boost by 1%.

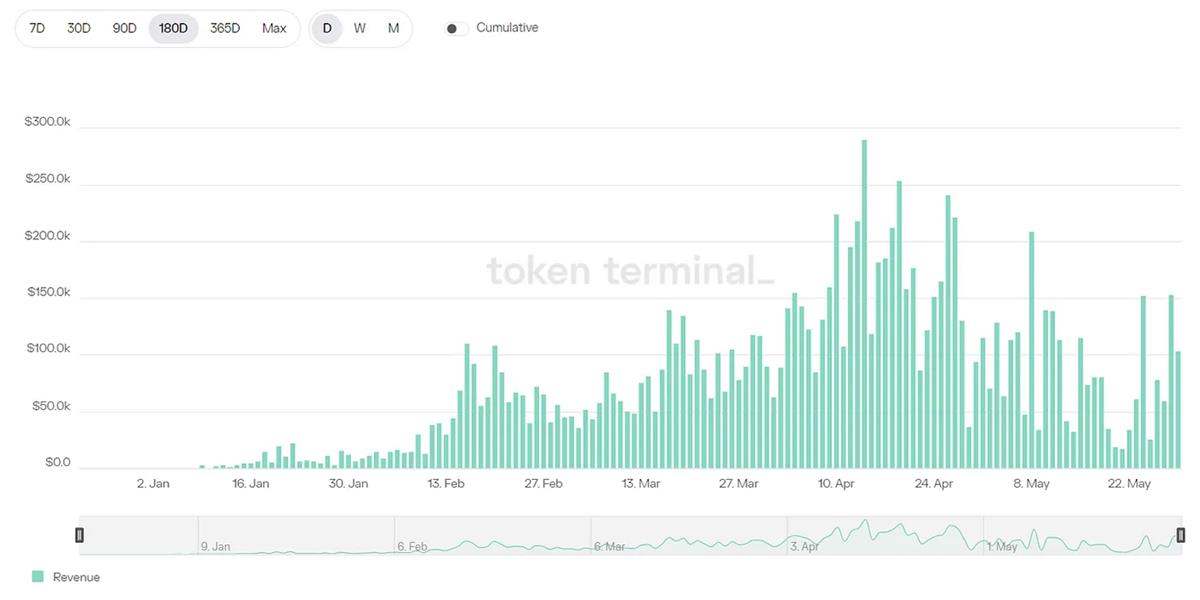

Over the past six months, there were 46 days when revenue exceeded $100,000 (25% of all days), including 19 days above $150,000, 8 days above $200,000, and 2 days above $250,000.

Chart: Daily revenue trends for Level

Source:tokenterminal

Additionally, orderbook-based DYDX has maintained high trading incentives since launch. Although the incentive amount has been reduced twice, each epoch still provides around 1.58 million DYDX tokens—valued at approximately $3 million, or $100,000 daily—among the highest in the current derivatives DEX landscape.

It is important to consider the impact and sustainability of these incentive programs on protocol token selling pressure.

In Kwenta’s case, OP ecosystem tokens make up the majority of incentives, while protocol token rewards are gradually decreasing, resulting in less direct selling pressure. Moreover, Kwenta’s incentives are claimable on a weekly basis with vesting periods; early unlocking requires partial token burning. However, the OP incentive program ends on August 30. Without follow-up measures, trading volume could sharply decline afterward.

Level, in contrast, distributes only its own protocol tokens daily without lockups, leading to significant token selling pressure. Furthermore, its Ladder rewards heavily favor the top 20 users, offering disproportionately high incentives compared to regular users, contributing to extreme concentration in trading activity.

DYDX also faces ongoing market scrutiny due to large token emissions and unlocks, with investors waiting for the launch of DYDX Chain and updates to its tokenomics.

Analysis of Real Trading Volume

Given the presence of trading incentives, it is necessary to analyze trading volume to understand the underlying reality. A brief analysis was conducted on several pool-based derivatives DEXs regarding user count, trading volume, concentration, and position size.

Table: Quality analysis of trading volume for pool-based derivatives DEXs

Source: LD Capital

GMX has 4–5 times more users than other projects, with far larger position sizes—three times that of Kwenta and five times that of Gains Network.

Kwenta and Level show significantly higher average transaction volumes per user compared to non-incentivized platforms.

Kwenta’s 30-day average trading volume per user is about $1.6 million—four times that of GMX. The top five traders account for 33.35% of total volume, indicating relatively low concentration. With 2,986 users, it leads the second-tier projects. Position size fluctuates between $40M and $60M.

Level’s 30-day average trading volume per user reaches $5.76 million—15 times higher than GMX. However, trading is highly concentrated: the top five traders account for nearly 75% of volume. With only $2.6M in positions and fewer than 600 users, a large portion of interactions appear to be volume-padding.

Overall, GMX remains the leader in the sector with clear advantages in user count and position size. Kwenta attracts more genuine users with less concentrated volume; after drawing users via incentives, it may retain them through better liquidity depth and lower fees. Level, however, suffers from high levels of artificial volume and inflationary tokenomics.

Recent Development Plans

GMX

According to community insights, GMX attributes the decline in volume and yields primarily to broader market downturns.

GMX’s current focus is launching its V2 version. The V2 testnet went live on May 17, allowing user participation. Key changes include:

GLP will transition from a single pooled structure to individual pools per trading pair. This isolation allows inclusion of higher-risk assets.

Two asset types will exist: pairs backed by native assets like BTC and ETH, and synthetic asset pairs fully backed by USDC. Traders can choose liquidity from different pools.

With multiple pools, LP participation becomes more complex, requiring analysis of utilization rates and yield variations to determine optimal pool selection.

Introduction of funding rates and price impact factors to balance long and short positions.

Kwenta

Kwenta’s development is closely tied to Synthetix. Both belong to the same ecosystem—Synthetix provides strong liquidity, while Kwenta delivers frontend services and acquires users.

On May 25, Synthetix founder Kain Warwick shared ideas for future development, including:

Using SNX for trading incentives, allocating 5–10 million SNX to the program.

Introducing passive SNX staking to broaden participation and increase the capital pool. Previously, Synthetix used active staking, where stakers had to outperform the overall pool to earn good returns or use hedging tools to manage risk. Passive staking would offer a stable baseline return, simplifying participation.

Subsidizing frontend operators’ costs. Currently, frontend revenues largely go to SNX stakers, creating insufficient long-term incentives for frontend teams. For example, Kwenta’s protocol revenue is fully distributed to SNX stakers. It is proposed to allocate a portion (e.g., 10 million SNX) from the treasury to stake on behalf of frontends, generating 3–5% base fee income.

These proposals address relationships between users, capital providers, and product development. If implemented, they could significantly boost projects built on Synthetix.

Level

In May, Level passed a community vote to expand cross-chain and migrate to Arbitrum. LVL token liquidity pools are already deployed on Arbitrum, enabling trading. The frontend is expected to go live by mid-June. Given Arbitrum’s large active user base and capital depth, this migration could attract new users and funds.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News