Outlier Ventures: Understanding the State of Unsecured Lending

TechFlow Selected TechFlow Selected

Outlier Ventures: Understanding the State of Unsecured Lending

This article provides a clear explanation of uncollateralized lending protocols in terms of fund utilization, token valuation, incentive impacts, and market advantages.

Author: Achim Struve

Compiled by: TechFlow

Introduction

This article focuses on a specific sector with significant potential. In the United States alone, the unsecured personal loan market reached $210 billion in the first quarter of 2023, surpassing the total value locked (TVL) in decentralized finance (DeFi), which stood at $61 billion. This indicates substantial growth potential for both the overall DeFi space and the decentralized lending industry. This remarkable growth potential has motivated the creation of current major unsecured lending protocols. This article provides a clear analysis of these protocols in terms of capital adoption, token valuation, incentive structures, and market advantages.

Overview

Lending assets are foundational to any financial system. Lenders earn returns on idle cash, while borrowers gain quick access to working capital.

In the DeFi space, lending markets are typically overcollateralized, meaning borrowers must deposit collateral exceeding the loan value.

For example, a borrower might need to provide $10,000 worth of ETH as collateral for a $5,000 USDC loan. While overcollateralization is standard practice in DeFi, unsecured loans in traditional finance are sometimes partially or entirely uncollateralized. Overcollateralization ensures that lenders can be repaid through liquidation of collateral if borrowers default.

Although overcollateralized lending is safer for lenders, it is inefficient and limits market expansion. Unsecured lending protocols require access to reliable credit data to assess borrower risk without disclosing sensitive information on-chain—addressing this limitation. Oracles combined with zero-knowledge proofs are being developed to reduce the need for borrowers to disclose identity to unsecured lending platforms.

However, unsecured lending is an important sector within DeFi, where higher risks are reflected in higher annual percentage yields (APYs) compared to overcollateralized lending platforms such as Aave and Compound. Unsecured or under-collateralized loans increase the likelihood of default. Off-chain asset and contract liquidations and repayments may also take considerable time.

Regarding lending pool security, lenders must rely on due diligence (DD) conducted by pool managers. Lenders may not have immediate liquidity access, as the amount available for withdrawal depends on the liquidity present in the lending pool.

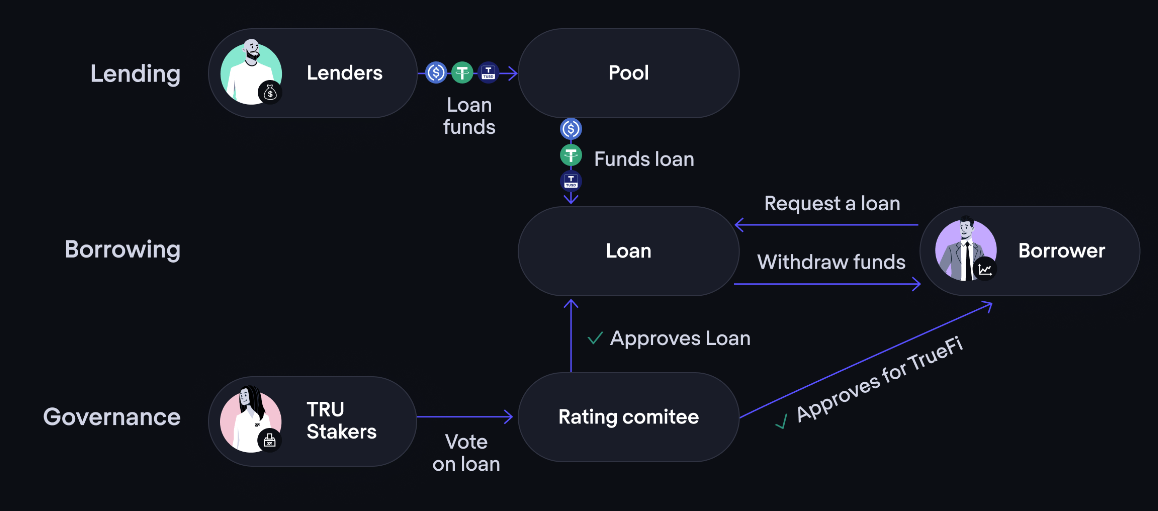

Figure 1 illustrates a representative ecosystem of an unsecured lending protocol. Using TrueFi as an example, lenders fund a lending pool from which borrowers obtain loans. $TRU holders vote on loans, which must also be approved by portfolio managers.

Overview of the Unsecured Lending Market

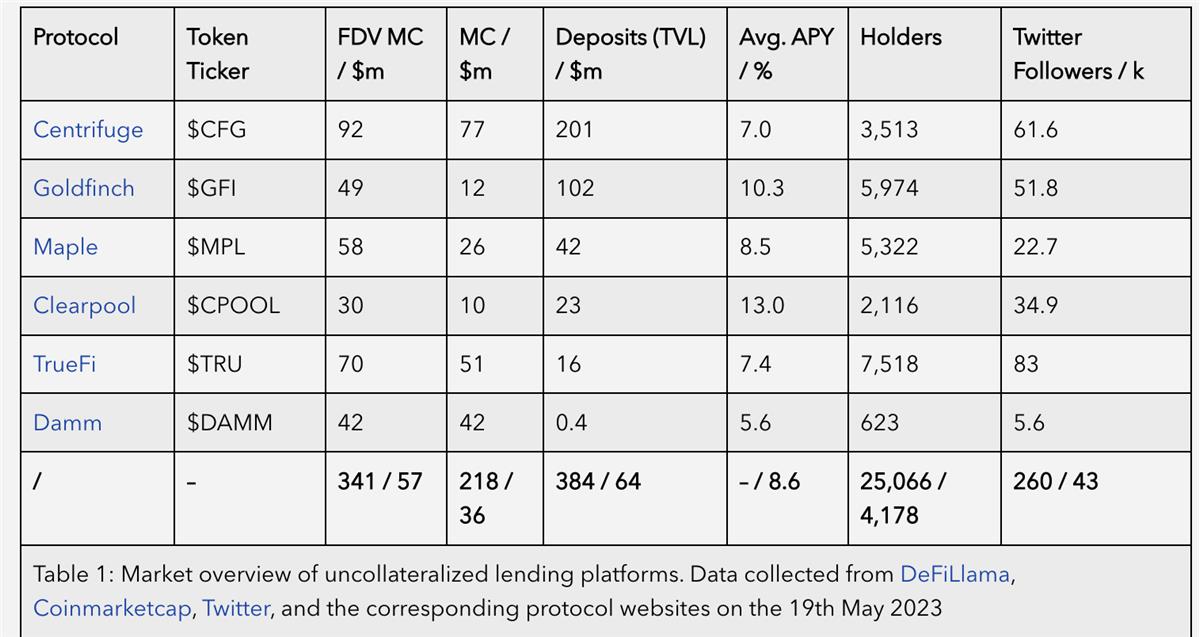

Table 1 provides a snapshot overview of several protocols offering unsecured loans to institutional borrowers. These protocols are ranked by their total value locked (TVL).

The total FDV of native tokens across all unsecured lending protocols listed in Table 1 amounts to $341 million, representing 6.6% of the crypto lending and borrowing industry, 0.7% of DeFi, and 0.03% of the total cryptocurrency market cap.

Additionally, the sum of TVL stands at $384 million, equivalent to 0.6% of DeFi TVL. These figures highlight the small market share of the unsecured lending protocols in Table 1 within the broader DeFi and crypto landscape. On the other hand, given the size of the traditional off-chain unsecured lending market, they also indicate significant growth potential.

The growth potential becomes even more apparent when considering the average competitive loan APY—including native token rewards across all protocols—which stands at 8.6%.

It should be noted that lending to unsecured lending protocols involves higher risk; therefore, the higher lender compensation (APY) compared to overcollateralized lending protocols like Aave is justified.

Token Performance Comparison

Comparing the historical valuation developments of relevant tokens in Table 1 can offer insights into potential future trajectories. However, token valuations measured by FDV depend on numerous factors, including general market conditions, individual protocol adoption, and token design itself. Tokens with weak value capture mechanisms may underperform, while the underlying product (lending platform) could perform well in terms of TVL and loss rates.

Therefore, a multi-layered comparison will be conducted. An overview of token designs and value capture characteristics offers initial insights into their correlation with expected protocol adoption.

For instance, tokens with strong value capture may better reflect overall protocol performance, whereas those with limited value capture mechanisms may be less indicative of the protocol's overall success. Next, key token metrics relationships will be compared based on current snapshots. The final token performance analysis will focus on historical development.

Token Value Capture

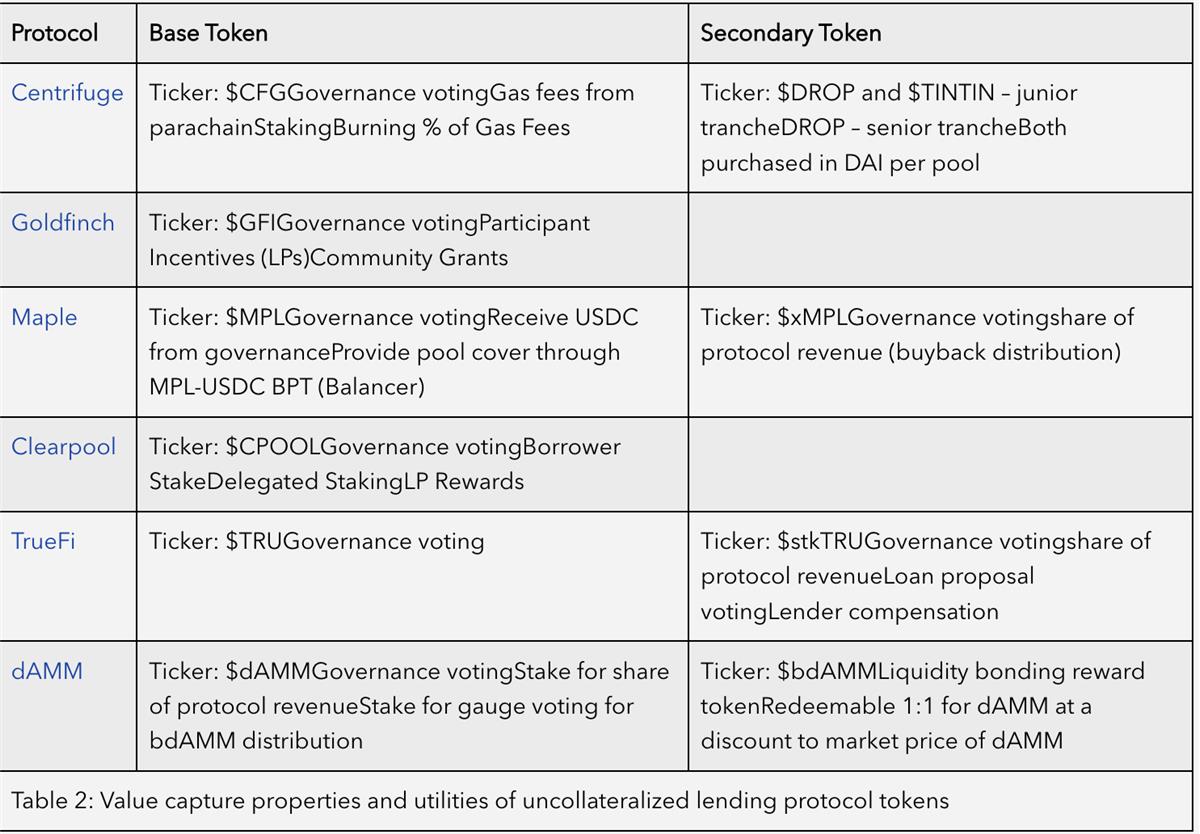

Table 2 presents an overview of value capture attributes and utilities from the top six protocols in Table 1. All tokens grant governance rights to holders and stakers.

Moreover, Maple, Centrifuge, and TrueFi utilize staking to issue secondary tokens. These secondary tokens are sometimes designed as vote-locked (ve) models and can also serve as tools to distribute fee shares to loyal supporters. In cases such as Centrifuge, Maple, TrueFi, Clearpool, and dAMM, fee shares are granted either directly or via distributed buybacks.

Goldfinch and Clearpool do not use auxiliary tokens but instead use their primary tokens directly as protocol incentive tools. All native protocol tokens accumulate value directly from product usage, whether through the aforementioned fee-sharing mechanisms, governance rights, or user benefits provided during token staking. This implies a certain level of correlation between all tokens and protocol adoption can be expected.

Token Metrics Relationships

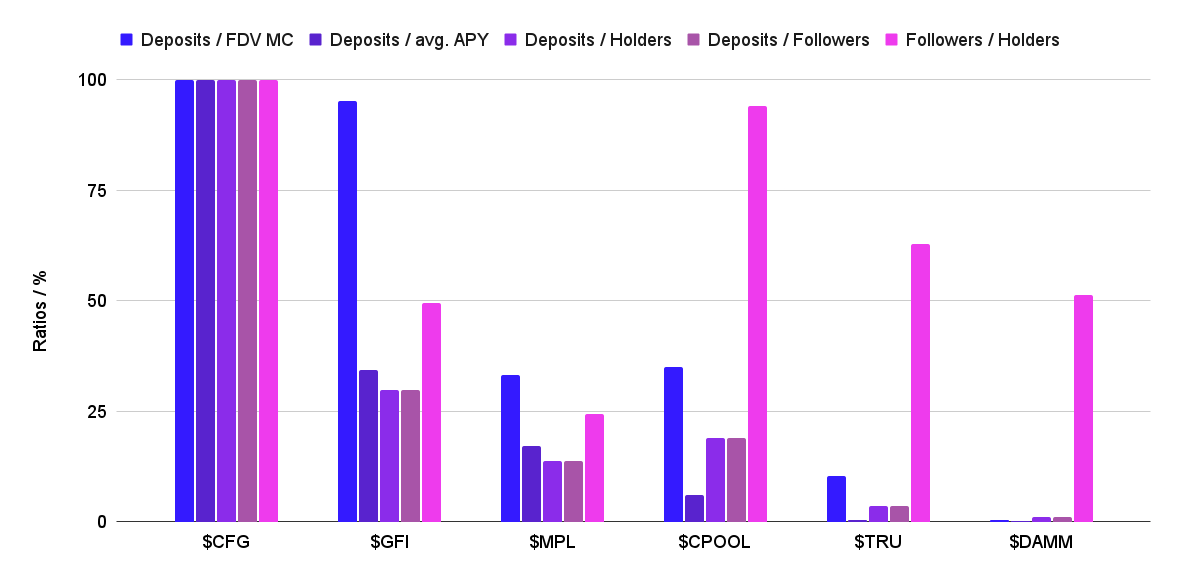

Figure 2 shows the relationship between protocol deposits (TVL) and various metrics such as FDV/MC, average lender APY, number of holders, and Twitter followers. These ratios are expressed as percentages of the highest value within each category.

-

The Deposit/FDV MC ratio reflects capital adoption relative to current market valuation. Note that these metrics only consider unsecured loans and staked deposits.

-

The Deposit/Average APY ratio serves as an indicator of capital adoption versus capital incentives.

-

The Deposit/Holders ratio indicates the average deposit value per native token holder and acts as a benchmark for actual user quality in terms of capital scale.

-

The Deposit/Followers ratio measures capital adoption per unit of marketing effort. Note that Twitter follower count does not necessarily correlate with actual product user adoption.

-

The Followers/Holders ratio reflects the relationship between actual user adoption of the native token and marketing efforts.

Data collection was completed in February, but due to rapid market changes, all data points require updating. In prior data collection, rankings across different categories varied significantly among protocols. However, currently, Centrifuge emerges as a clear leader across all categories, a direct result of its high TVL.

The reason for its success compared to other participants may lie in its innovative use of real-world assets (RWA) in tokenized form.

Normalized Historical Comparison of Token Market Value

The previous comparisons focused on recent values. Figure 3 displays the historical development of FDV/MC for different unsecured lending protocol tokens. These values are normalized against Ether’s FDV/MC to benchmark against the broader cryptocurrency market. The vertical axis uses a logarithmic scale to mitigate the visual impact of high volatility. From January 1, 2022, to May 19, 2023, all native unsecured lending tokens have declined relative to $ETH.

Possible reasons for their underperformance include:

-

Cryptocurrency market crash. Since November 2021, the entire cryptocurrency market has been in a downtrend, and unsecured lending protocols have not been immune. As crypto prices fell, so did the value of these protocols’ native tokens.

-

Concerns about sustainability of unsecured lending. Unsecured lending protocols are relatively new and untested concepts, raising concerns about their long-term sustainability. Some critics argue these protocols are inherently risky and believe it's only a matter of time before they collapse. Several protocols, including Centrifuge, Maple, and TrueFi, have already experienced partial incidents. Other lending and investment platforms have faced complete collapses, such as Celsius, Voyager Digital, and 3 Arrows Capital, potentially amplifying fears.

-

Availability of safer collateralized lending alternatives. Collateralized lending protocols are more popular because they offer lower-risk alternatives to unsecured lending. As more users shift toward collateralized lending, demand for unsecured lending decreases, exerting downward pressure on the value of these protocols’ native tokens.

Summary and Insights

Token designs of unsecured lending protocols exhibit diverse approaches and value accrual mechanisms. While all protocols offer governance rights through their tokens, not all provide direct revenue sharing via staking. Nevertheless, all token designs derive some form of value growth from product adoption.

Centrifuge is currently the most successful unsecured lending protocol in terms of FDV valuation and TVL. Despite facing issues with overdue loans, its strength lies in its innovative approach to RWA.

The overall valuation performance of all native unsecured lending tokens has been poor, failing to outperform the broader cryptocurrency market. The 2022 bear market saw too many partial or complete collapses, leading to reduced trust in the sector.

In terms of aggregate FDV/MC, the unsecured lending sector remains small relative to the entire DeFi ecosystem (0.7%) and the broader cryptocurrency market (0.03%).

Considering the significant role of unsecured lending in traditional finance and the trend toward optimizing capital efficiency, decentralized unsecured lending still holds substantial potential for growth and innovation. However, more time is needed to rebuild trust and drive innovation before this potential can be fully realized.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News