Reviewing the Subtle Changes and Future Development of NFT Trading & Aggregation in 2022

TechFlow Selected TechFlow Selected

Reviewing the Subtle Changes and Future Development of NFT Trading & Aggregation in 2022

In recent years, the NFT sector has attracted significant attention from many investors, with top-tier CEXs such as Binance, Coinbase, and Kraken announcing their entry into the NFT space.

1. Introduction

In recent years, the NFT sector has attracted significant attention from many investors. Leading centralized exchanges (CEX) such as Binance, Coinbase, and Kraken have all announced their entry into the NFT space. In the past, DeFi took only about a year to establish a complete ecosystem encompassing DEXs, lending, stablecoins, oracles, derivatives, and cross-chain bridges, continuously evolving toward value aggregation based on traffic. In 2022, the NFT market further accelerated its pace of ecological convergence, trending toward maturity with ongoing developments ranging from policy reviews and royalty reforms to brand collaborations and platform consolidations.

Against the bear market backdrop of 2022, key NFT metrics experienced significant fluctuations, with overall market data declining steadily since the second half of the year. This led some voices within the ecosystem to claim that NFTs were entering a period of decline. However, NFT price movements can often serve as early indicators of broader market trends and reflect underlying value logic in industry development—such as the consolidation activities we examine here in the aggregation segment. The NFT market is now transitioning into a phase of stabilization and transformation, requiring time and sustained effort to deepen its foundations.

This article begins with an overview of NFT origins and fundamental concepts, summarizes key historical milestones in the NFT space, analyzes the current state of the NFT market, and discusses recent merger and acquisition activity at the trading layer. It also compiles updates on platform policies and shifts in royalty handling approaches, provides an in-depth look at recent technological advancements, and offers a comprehensive outlook on the trajectory and future direction of the entire sector.

2. NFT Basics

When people think of NFTs, they most commonly associate them with digital images or profile pictures (PFPs) on social media. However, what we now consider traditional NFTs actually existed before 2021—though few truly understood them at the time.

What Is FT?

Fungible Tokens (FTs) are interchangeable, uniform, and nearly infinitely divisible tokens.

A good example of fungibility is currency—because of their uniformity, one $5 bill can be easily exchanged for another $5 bill. As fungible tokens, dollars are simple to exchange; even if serial numbers differ, identical denominations hold equal value regardless. These items are interchangeable because they are defined by value rather than uniqueness.

What Is NFT?

NFT stands for non-fungible token. Non-fungibility is a defining characteristic of NFTs.

Unlike fungible tokens, NFTs cannot be mutually substituted. They are unique data units stored on blockchains, capable of representing one-of-a-kind crypto assets like artworks. Each NFT carries a distinct identifier that differentiates it from others, serving as proof of authenticity and ownership in the digital realm.

There are multiple frameworks for creating and issuing NFTs. The most popular ones are ERC-721 and ERC-1155 on the Ethereum blockchain. Without the owner's permission, an NFT cannot be copied or transferred—even by its issuer.

History of NFTs

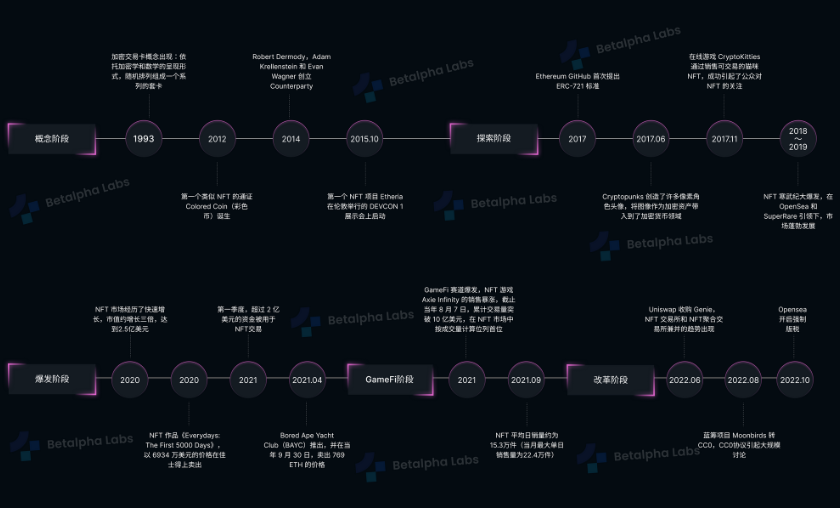

The concept of NFTs can be traced back to "Crypto Trading Cards" in 1993 and "Colored Coins" in 2012. "Crypto Trading Cards" introduced the idea of collecting digital cards generated through mathematical transaction models, while "Colored Coins" extended Bitcoin’s utility and served as an excellent experiment in off-chain asset mapping.

Subsequent explorations, explosive growth, and stabilization phases gradually brought NFTs into wider public awareness. Today’s NFTs look vastly different from their original conceptual forms, yet it is precisely through repeated innovation attempts that today’s crypto landscape has emerged.

Figure 1: Five Major Milestones in NFT Development

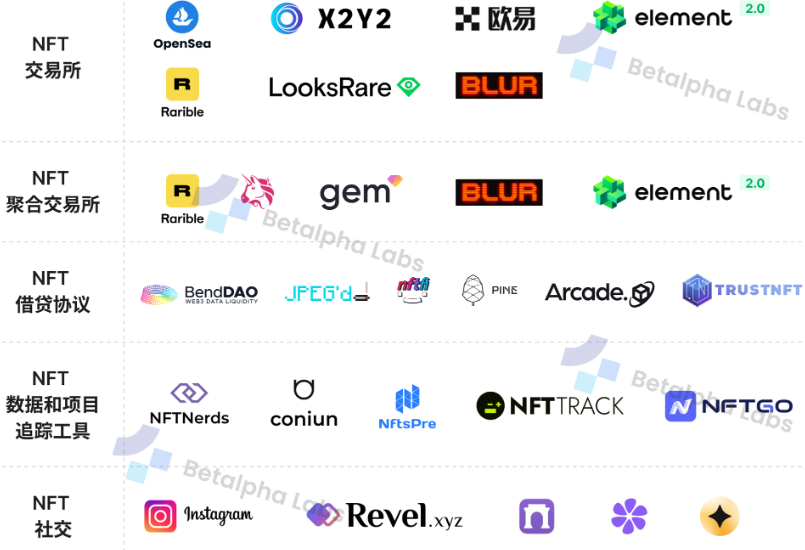

NFT Sector Classification:

Classifying NFT markets by protocol functionality, platforms can be divided into five main categories: trading, aggregation, lending, data tracking, and social.

Figure 2: NFT Sector Breakdown

3. Overview of NFT Market Landscape & Policy Updates

3.1 Trading Platforms

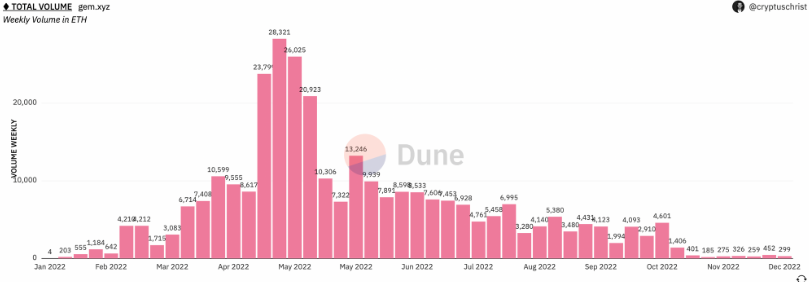

According to data from CoinMarketCap, total trading volume across 14 NFT platforms surged from $85.7 million in 2020 to $19.6 billion in 2021—an increase of nearly 23,000%. 2021 was undoubtedly a year of unimaginable growth for the NFT space.

Figure 3: Trading Platform Data

However, 2022 proved to be a difficult year for the NFT sector. From the collapse of Luna in early 2022 to FTX’s bankruptcy at year-end, despite continued emergence of new projects and exploration efforts, the broader downturn in the crypto ecosystem dragged the NFT market into a bear cycle.

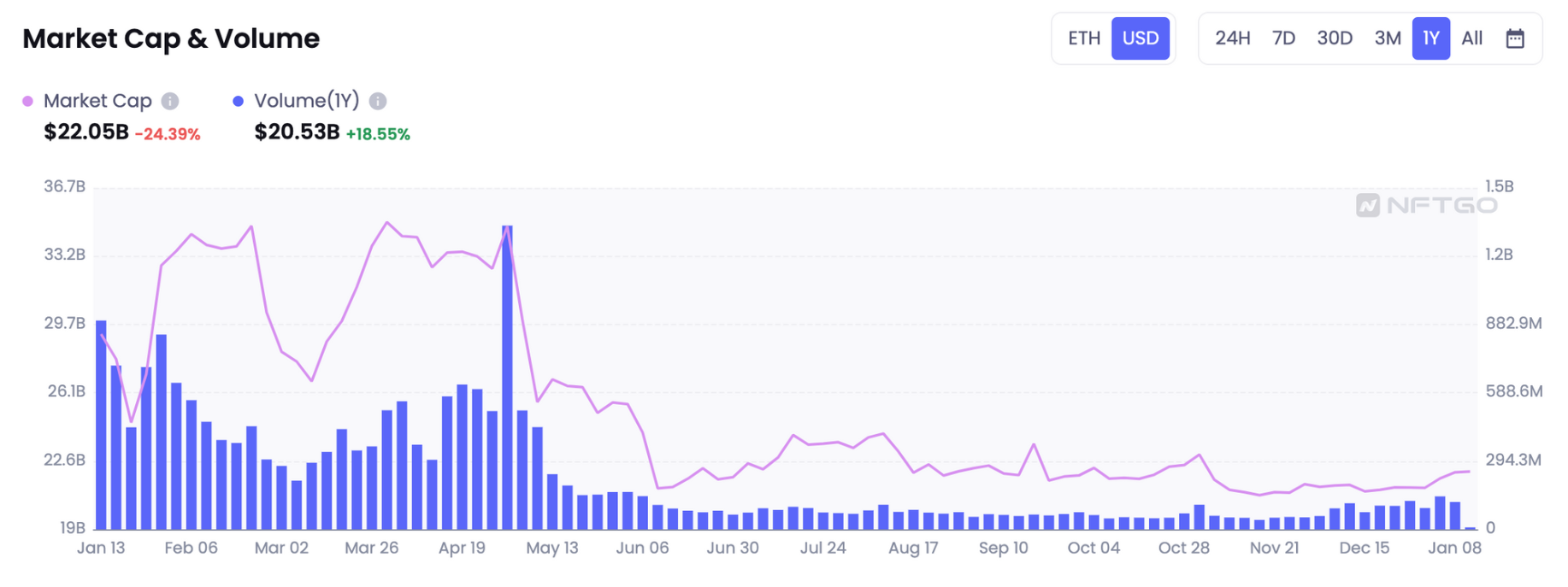

The total market capitalization of the NFT market peaked at $34.96 billion in March but declined thereafter, remaining between $21–23 billion until reaching a low of $20.82 billion in November—a 40.5% drop.

Figure 4: Market Cap & Volume

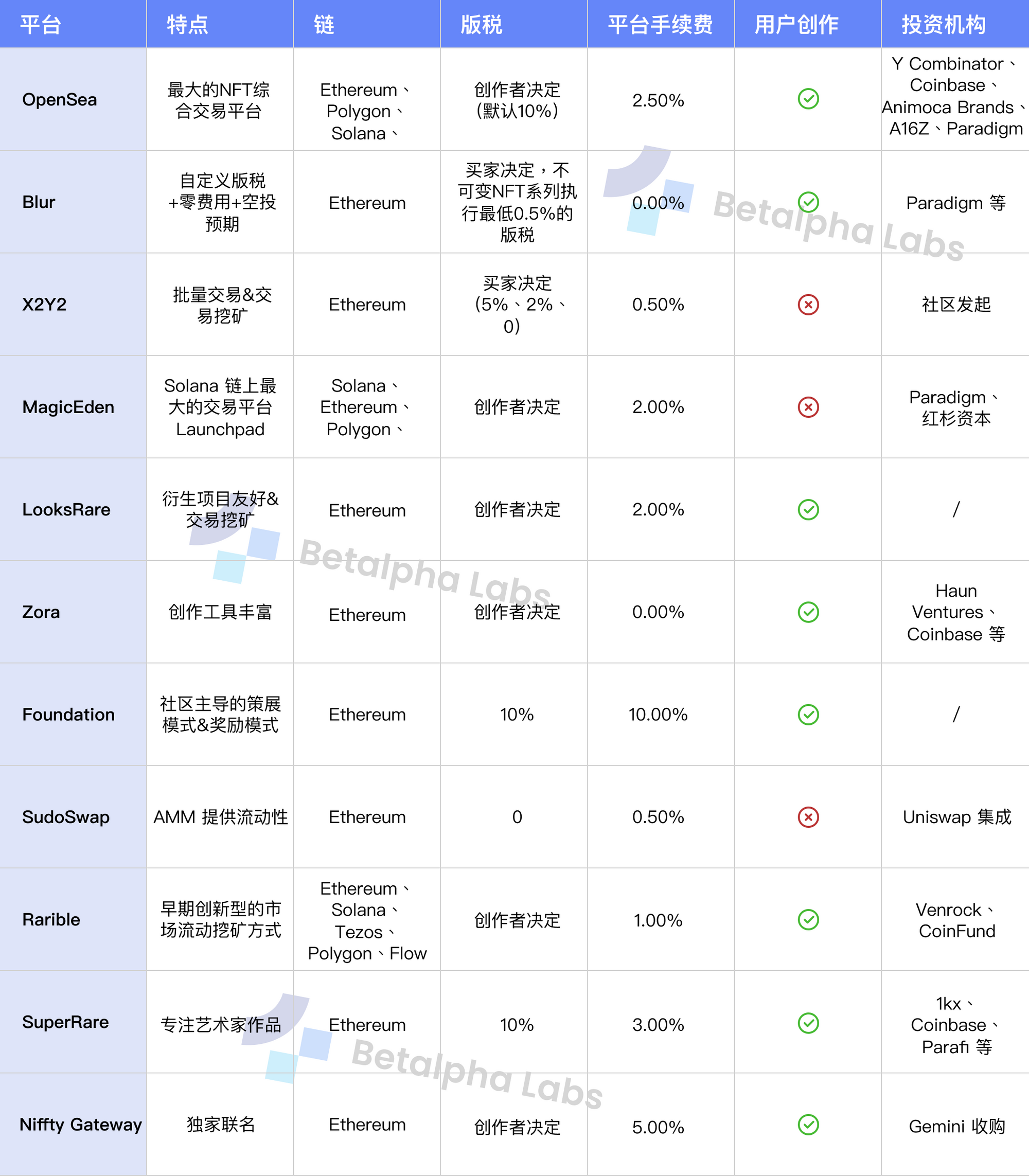

OpenSea

Founded in 2018, OpenSea is a blockchain-based global marketplace for buying and selling digital items and has long been the leading project in the NFT trading space. Positioned as the premier decentralized exchange, OpenSea facilitates peer-to-peer (P2P) trading of non-fungible tokens (NFTs).

In 2022, OpenSea focused more on copyright protection. In June, it launched an updated NFT copyright protection program, introducing multiple measures to enhance and safeguard NFT owners’ rights. Additionally, OpenSea rolled out a new verification system to better distinguish genuine accounts and content.

In November 2022, OpenSea announced it would introduce an on-chain royalty enforcement tool. Under this mechanism, NFT projects wishing to collect royalties on OpenSea must use OpenSea’s mandatory royalty contract. However, this contract blacklists any platform offering custom royalty settings. If an NFT project refuses to blacklist other marketplaces, OpenSea will reduce all royalties generated on its platform for that project to zero.

Magic Eden

As the NFT trading platform with the highest volume on Solana, Magic Eden expanded its supported blockchain list by integrating Polygon. Gaming-related NFTs remain Magic Eden’s strength. In December, it hosted several Polygon-based projects on its Launchpad. According to Polygon, once the Polygon Launchpad goes live, Magic Eden users will be able to trade NFTs using MATIC.

Magic Eden also made updates regarding royalty protection. In December, it officially launched a new protocol mandating royalties for all newly released collections opting into the tool. The open-source Open Creator Protocol (OCP) allows creators launching collections to choose whether to protect royalties. For creators not adopting OCP, royalties remain optional on the platform.

Additionally, Magic Eden introduced a discount and rewards system, allowing users to earn benefits based on their platform activity. It is collaborating with ecosystem partners to add features like referral codes and trading analytics tools.

Despite OpenSea adding Solana support in April 2022, Magic Eden continues to lead in trading volume on the Solana chain.

3.2 Aggregation Platforms

Aggregation platforms are increasingly emerging in the market. Many professionals believe that changes in the NFT market landscape won’t come from heavyweight crypto exchanges, nor from early token adopters like Rarible, or art-focused platforms like SuperRare and Foundation—despite their potential, these platforms target relatively niche audiences.

Rather, real disruption to OpenSea’s dominance comes from teams leveraging tools and aggressive token incentive mechanisms—platforms like GEM and Element, aggregators, and reward-driven models like Looksrare, along with newer entrants like Blur that quickly gained prominence.

Traditionally, aggregators primarily serve data aggregation purposes—collecting information across multiple sites and presenting it in a unified interface tailored to user needs. At their core, they function as search engines, compiling useful information while filtering out irrelevant noise.

With technological advancement, certain aggregators now use machine learning to generate valuable metrics derived from processed data.

Professional NFT aggregators gather transaction data from various public chains and consolidate them onto a single platform. This delivers a seamless trading experience and improves efficiency.

Compared to traditional marketplaces, NFT aggregators offer clear advantages:

- Highly aggregated information—users can view, trade, and purchase NFTs across all markets via a single platform, accessing comprehensive data including volume, floor price, transaction prices, quantities, top holders, and top buyers.

- Improved trading efficiency—users can easily browse listings across exchanges and select optimal pricing.

- Diverse payment options—in theory, users can pay with any preferred token on an NFT aggregator and save gas fees through batch transactions.

Overall Market Overview of Aggregation Platforms

NFTs have clearly become one of the hottest topics not only in the broader crypto economy but also in fintech and entertainment sectors. Similar to large-block trades in traditional finance, demand for easier basket purchases or bulk trading of NFT assets is growing steadily.

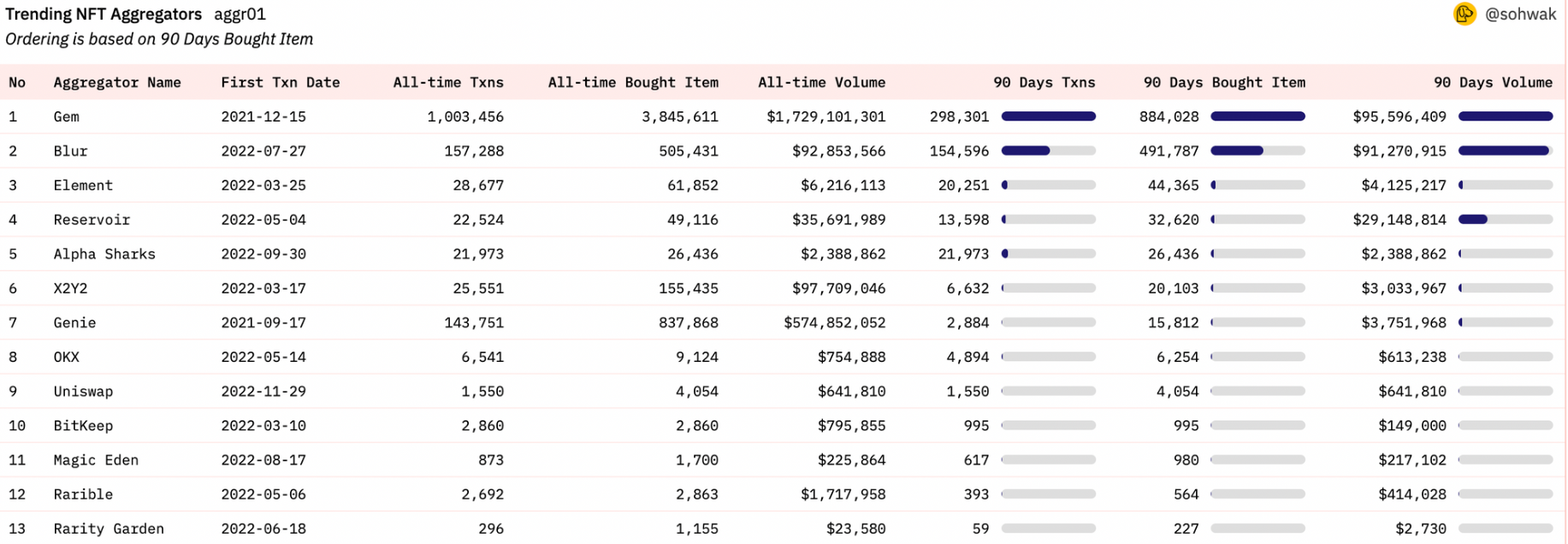

It’s evident that more and more platforms are turning their focus toward the NFT aggregation space through acquisitions or upgrades, making bulk NFT trading a clear market trend.

Figure 5: Trending NFT Aggregators

From the data above, Gem maintained strong momentum after launching its beta version on December 28, 2021, ranking first in total trading volume. In April 2022, it was officially acquired by OpenSea but continues operating under its independent brand.

However, in October 2022, Blur disrupted Gem’s dominant position. Through its model of “customizable royalties + zero fees + airdrop incentives,” Blur rapidly attracted a large user base, quickly becoming the largest on-chain NFT aggregation marketplace by trading volume and placing unprecedented pressure on existing platforms.

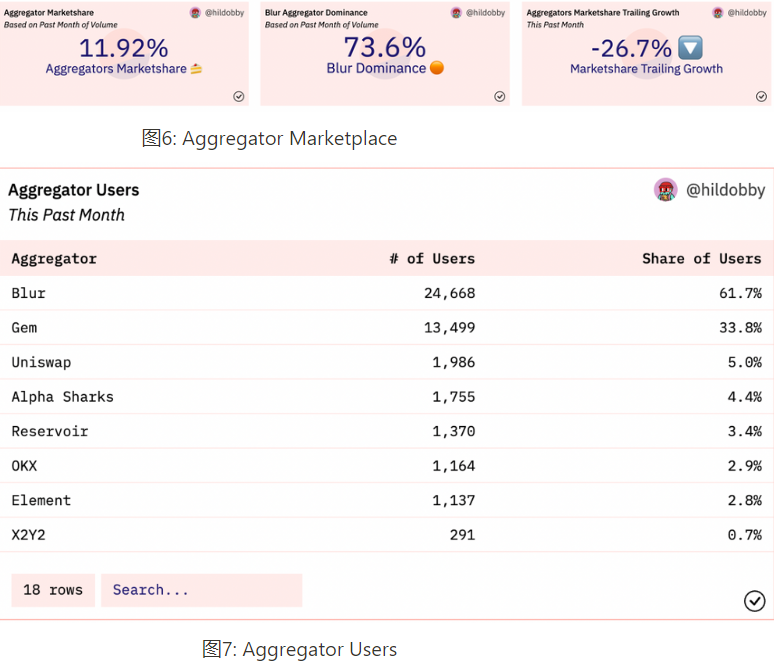

Recent data shows that aggregators accounted for only 11.92% of total NFT trading volume, down 26.7% month-over-month amid general market stagnation during the bear market, indicating a shift toward stability without explosive growth. Within this segment, Blur alone captured a staggering 73.6% share—more than half of the entire aggregation market—and firmly holds the top spot. In terms of user count, Blur reached 61.7% in the latest monthly data, followed by Gem (33.8%) and the newly launched Uniswap Aggregator (5%). Other aggregators lag far behind in usage compared to Blur and Gem.

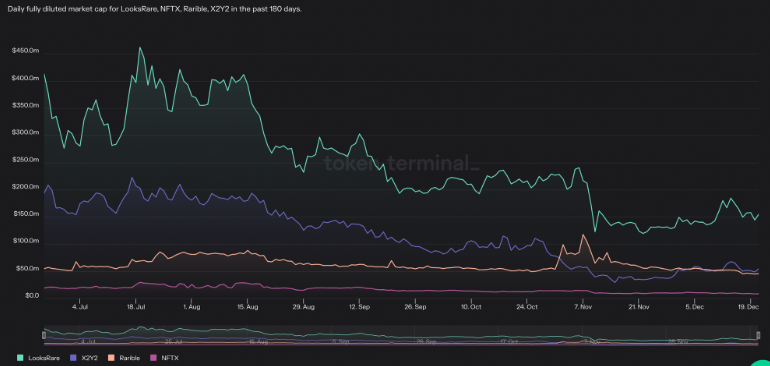

Looking at other platforms, aside from Blur and Gem, X2Y2 and Looksrare show relatively stable performance, with daily fully diluted market caps around $55M and $150M respectively—Looksrare’s figure being roughly three times that of X2Y2. From a revenue perspective, X2Y2’s recent average daily revenue is ~$18K, down 24.4% over the past 30 days but up 70.2% compared to 180 days ago. Looksrare’s average daily revenue is ~$90K, down 15.3% over the past month and 96.2% lower than six months ago, suggesting it has hit a bottleneck.

Figure 8: Daily Fully Diluted Market Cap

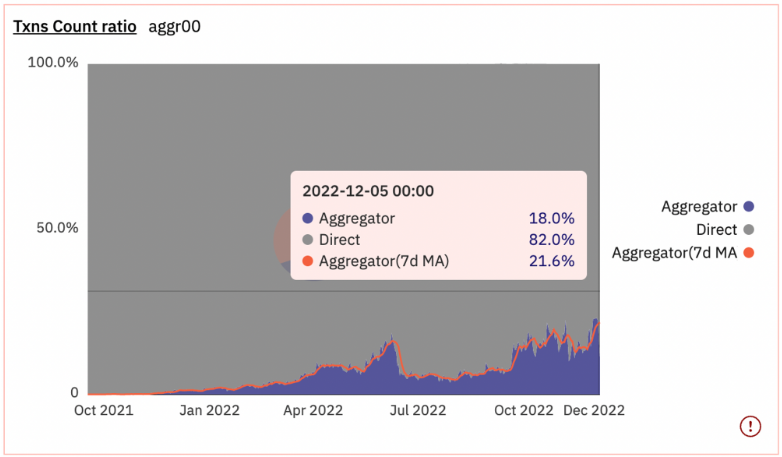

Overall, direct transactions on NFT marketplaces account for 82% of trading accounts, while aggregation platforms make up 18%. The chart clearly shows the last notable surge in aggregation platform usage occurred in October 2022—the same month Blur launched—indicating a strong correlation and impact.

Figure 9: Transaction Count Ratio

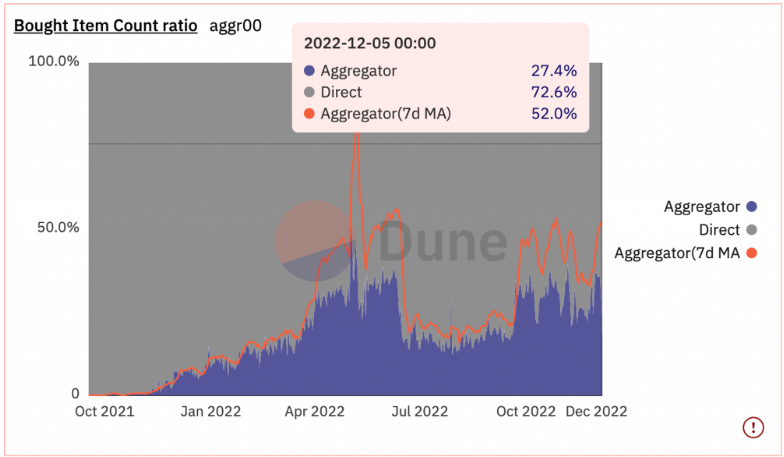

Regarding NFT purchase volume, 72.6% of NFTs are bought directly on marketplaces, while 27.4% are purchased via aggregators. The peak in aggregated purchases occurred on May 6, when aggregated volume reached 37.2% and MA peaked at 84.2%. That day marked the opening of Azuki’s Beanz Official airdrop, driving increased demand for blue-chip NFTs on aggregation platforms.

Figure 10: Bought Item Count Ratio

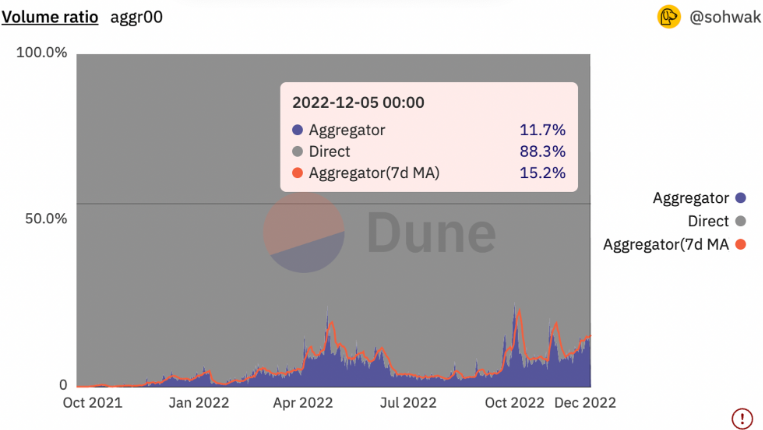

Finally, looking at transaction value, aggregators currently account for 11.7% of total market volume—about 16 percentage points below their purchase volume share (27.4%). We can reasonably infer that most aggregated trading volume comes from lower-priced NFTs. Users tend to use aggregators to bulk-buy undervalued or promising assets, whereas for blue-chip NFTs, especially without promotional events, users still prefer established platforms like OpenSea to minimize risk.

However, the long tail should not be underestimated. Companies like Amazon and Netflix built massive scale through long-tail effects before achieving breakout success. Similarly, the NFT aggregation market may experience its own surge as the broader NFT ecosystem evolves.

Figure 11: Volume Ratio

Trends in Aggregation Platforms – Detailed Analysis

- Blur

Blur stands out as the standout newcomer, rapidly capturing market share upon launch and sparking widespread discussion across platforms. Like Uniswap, it prioritized early promotion and emphasized a smooth user interface and robust backend supporting bulk NFT purchases. After its first airdrop in November, Blur already accounted for about 15% of Ethereum NFT trading volume.

Following a second airdrop in early December, by December 19, Blur’s monthly NFT trading volume surpassed OpenSea’s, capturing approximately 33.02% of the entire NFT market share and becoming the largest on-chain NFT aggregation marketplace.

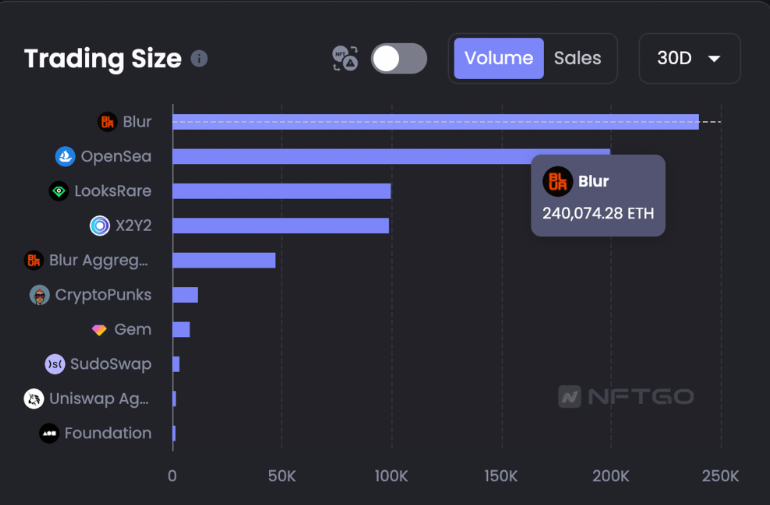

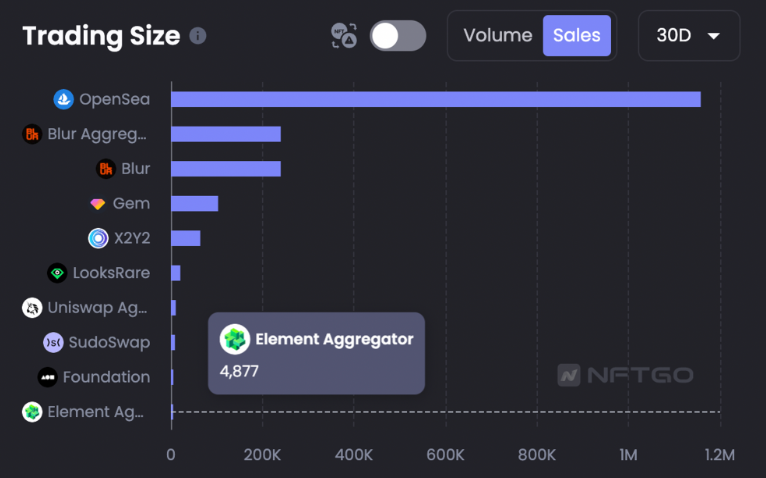

Data from NFTGo shows that Blur’s trading volume reached 240k ETH in just one month—surpassing OpenSea’s cumulative volume in merely three months since launch.

Figure 12: Trading Size

Blur also employs unique operational strategies. While most on-chain airdrops aim to attract traffic, Blur captured attention early with its first airdrop and openly stated that the second round would be tied directly to user interactions on the platform—this transparency helped build a loyal user base actively listing and trading.

Blur’s royalty mechanism differs significantly from most NFT marketplaces. Here, traders can set their own royalty rates—including choosing zero. This means original creators receive no income from secondary sales. Conversely, incentives favor traders who do pay royalties. For instance, those paying higher royalties receive larger airdrop allocations.

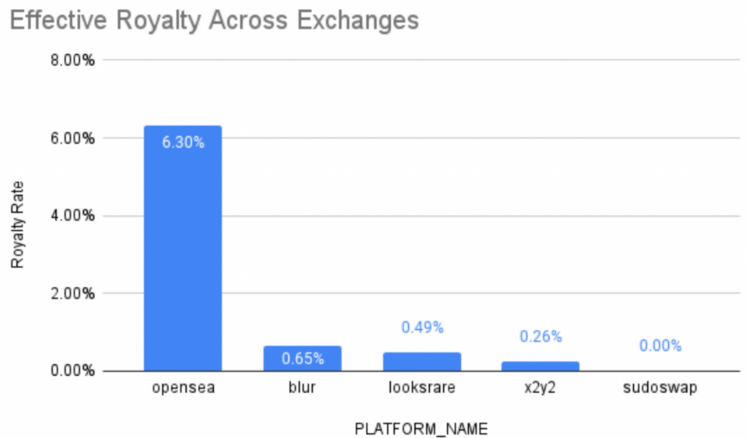

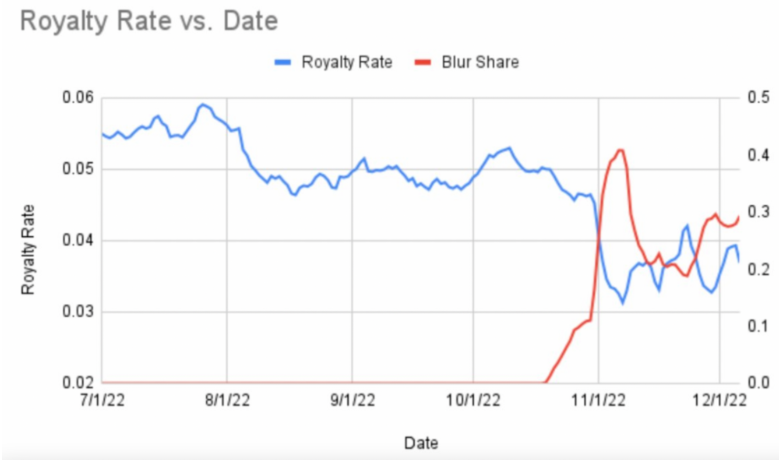

During the second airdrop, users setting higher royalties earned greater loyalty scores and thus larger rewards. For users migrating from zero-royalty platforms like Sudoswap, setting their royalty to match Sudoswap’s platform fee (0.5%) allowed them to maintain profits while qualifying for enhanced airdrops. However, post-airdrop data indicates these incentives failed to prevent low or zero-royalty behavior—Blur’s average effective royalty rate stands at just 0.65% (Figure 13), contributing to a broad decline in NFT market-wide royalty rates (Figure 14).

Figure 13: Effective Royalty Across Exchanges

Figure 14: Royalty Rate vs. Date

As for how long the “custom royalties, zero fees” model will last, Blur states it will wait until its token launches before community governance votes determine final royalty and fee structures. Until then, Blur will not earn any revenue.

Unlike Element, where buying one or multiple NFTs incurs similar gas costs, Blur charges increasing gas fees for larger batch purchases. This may explain why bulk NFT purchases on Blur almost never fail.

- Looksrare

Looksrare is a community-centric NFT trading platform that actively rewards all users. Upon launch, it was heavily marketed with slogans like “100% of trading fees shared among LOOKS stakers,” “massive airdrops,” and “By NFT people, For NFT people.”

Leveraging its native token LOOKS, Looksrare distributed airdrops to any NFT user who traded at least 3 ETH on OpenSea within the previous six months. The airdrop had nine tiers—the more trades a user completed on OpenSea, the more LOOKS tokens they could claim.

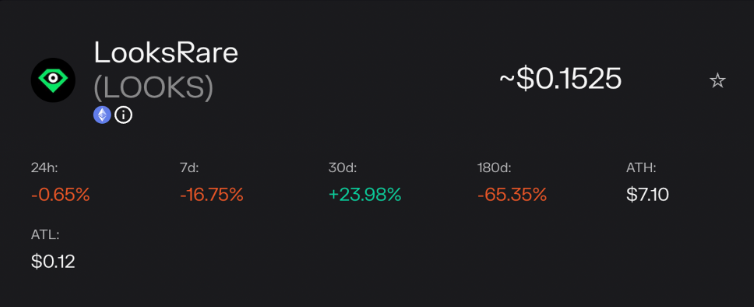

According to the latest data from Token Terminal, the price of its native token LOOKS dropped 65.35% over 180 days. Although it rose 23.98% in the past month, this rebound does little to offset earlier losses.

Figure 15: $LOOKS

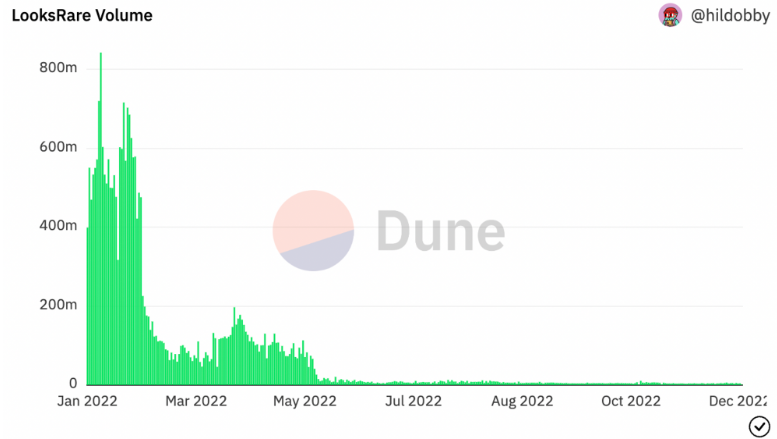

Since May, Looksrare’s trading volume has plummeted dramatically.

Figure 16: Looksrare Volume

Still, Looksrare distinguishes itself in key ways, particularly in platform fees. Since launch, Looksrare has charged a 2% trading fee, slightly lower than OpenSea’s 2.5%, and promises to distribute 100% of fees to users staking $LOOKS tokens—a move that drove significant early staking participation.

Looksrare also takes a different stance on derivative NFT projects. Unlike OpenSea, which exercises absolute control over listings and has delisted high-profile derivative works, Looksrare generally refrains from removing or freezing derivative projects unless malicious intent is involved. Naturally, opinions within the community vary—some argue such derivatives shouldn’t exist, while others believe restricting them contradicts Web3 principles.

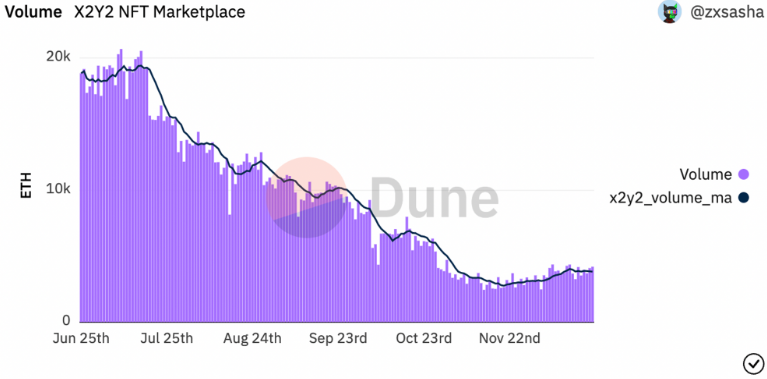

X2Y2

X2Y2 is a comprehensive NFT marketplace built on Ethereum. It used token airdrops to perform a vampire attack on OpenSea and introduced listing rewards, gas fee rebates, and trading mining incentives to capture market share. While trading mining was an effective early user acquisition tactic, it fails to create sustainable competitive moats. Charging only 0.5% in fees, X2Y2 adopted a low-price strategy to attract users but faced accusations of wash trading.

Initial listing rewards failed to draw users, and the April gas subsidy campaign did not boost trading volume. However, once trading mining launched, platform volume surged rapidly, peaking at 20,000 ETH weekly. After accumulating sufficient user base and visibility, data stabilized for a period. According to Dune Analytics, cumulative trading volume reached 1,689,188 ETH. However, since June, trading volume has sharply declined.

Figure 17: X2Y2 Volume

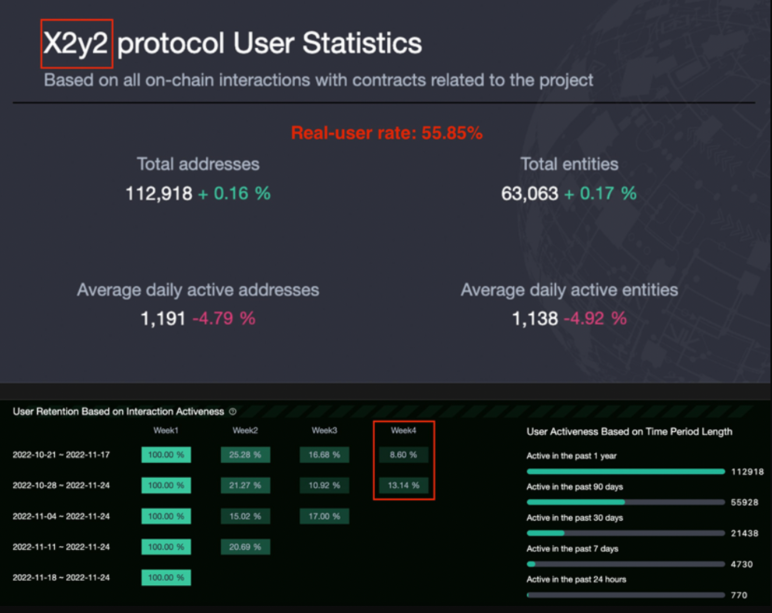

Pure on-chain data from 0xScope Insight reveals X2Y2’s real user rate (entities per address) is only about 55.85%, the lowest among OpenSea (64.23%), Looksrare (66.15%), and Blur (67.72%). This implies that among every 10 user addresses, only around 6 represent genuine users—highlighting serious wash trading issues.

Figure 18: X2Y2 Protocol User Statistics

One method involves users selecting NFTs without creator fees and conducting self-trades to earn trading mining rewards. Another exploits the platform’s peer-to-peer feature to frequently transfer NFTs between two addresses for rewards. Neither adds liquidity to the market and both discourage genuine user participation.

Unless these fake trading practices are addressed, X2Y2’s future growth will face severe constraints.

- Rarible

In October 2022, Rarible introduced aggregation features to enhance user experience. Its aggregator helps users find the best NFT prices across markets and chains, without charging additional fees on these external transactions. The tool includes filters to narrow down NFT projects by multiple criteria. Users can browse NFTs across blockchains including Ethereum, Solana, Tezos, Flow, Polygon, and Layer 2 solutions like Immutable X.

In September, Rarible expanded its gaming NFT offerings through a partnership with Immutable X, enabling buying and selling of game-related NFTs. On November 11, a proposal to build a zero-fee Apecoin marketplace failed to pass, receiving 85.65% opposition votes—possibly a missed opportunity for strategic expansion.

- Element

Element differs from other aggregators by operating its own trading marketplace and supporting multi-chain transactions.

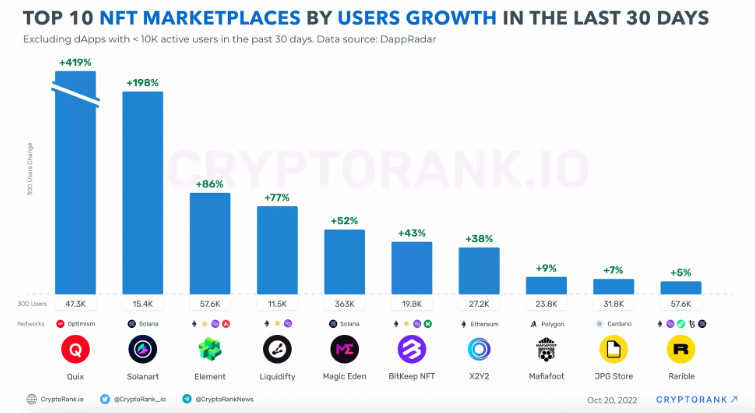

In October, Element ranked third in user growth among all-chain NFT markets, with an 86% increase and 57,600 total users over 30 days. Over three months following July 15, it achieved 70,124 unique users, over 170,000 transactions, and nearly $150 million in trading volume—an impressive record.

Figure 19: User Growth

However, its decline has also been stark. Over the past two months, as new platforms launched, Element’s trading volume steadily decreased, with three months’ volume falling short of the recently launched Uniswap Aggregator.

Markets evolve rapidly—many projects unable to secure market share quietly exit the competition.

Figure 20: Element Trading Size

4. Mergers and Consolidation at the Trading Level

4.1 Opensea & Gem

As monopolistic firms often do, OpenSea acquired Gem—widely seen as a highly centralized move aimed at eliminating a rising threat.

Although Gem will continue operating as an independent product separate from OpenSea, OpenSea plans to integrate more Gem features into its NFT marketplace over time.

Gem’s performance as an aggregator was outstanding. By the acquisition date, Gem had accumulated over 246,000 ETH in trading volume—double that of Genie, which launched earlier. Gem’s rapid rise stemmed largely from deeper market integration, aggregating major NFT platforms like OpenSea, Looksrare, and X2Y2 earlier than Genie, which for a long time focused mainly on OpenSea and smaller markets. Genie didn’t integrate Looksrare until early April 2022. Moreover, Gem incorporated advanced analytics dashboards from Dune Analytics and included anti-snipe bot features, giving it a technological edge over Genie. Despite strong metrics, NFT aggregators don’t charge platform fees and are still exploring viable monetization models—making acquisition inevitable.

Figure 21: Gem Total Volume

Before acquiring Gem, OpenSea emphasized improving community experience—aiming to serve more experienced professional users and offering flexible service tiers for NFT buyers of varying expertise. This suggests OpenSea’s strategy is forward-looking, and Gem is not just an NFT marketplace aggregator but also a portfolio management platform—precisely meeting OpenSea’s needs.

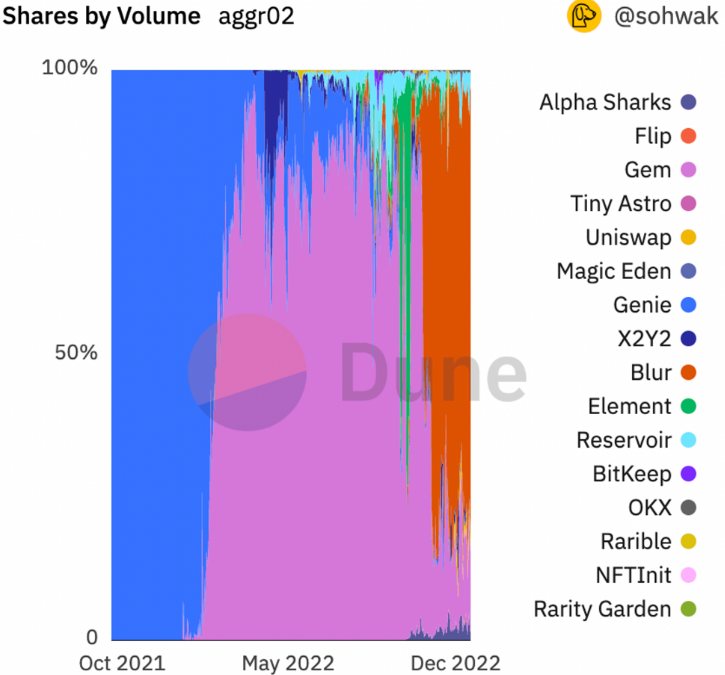

Previously, many speculated OpenSea and Uniswap would follow similar paths. But now, Uniswap appears to be pursuing a different strategy, focusing on bridging FT and NFT ecosystems. Gem, continuing as an independent brand, dominated the aggregation space until Blur’s aggressive entrance.

Since Blur’s launch, Gem’s top position in aggregation has been broken—within days, Blur captured much of Gem’s market share, rendering its prior advantages nearly obsolete.

Figure 22: Shares By Volume

Recent data shows most Gem users are collectors listing NFTs for sale, while actual buyers are comparatively fewer—suggesting declining market activity and shifting preferences among collectors.

Figure 23: Traders

4.2 Uniswap & Genie

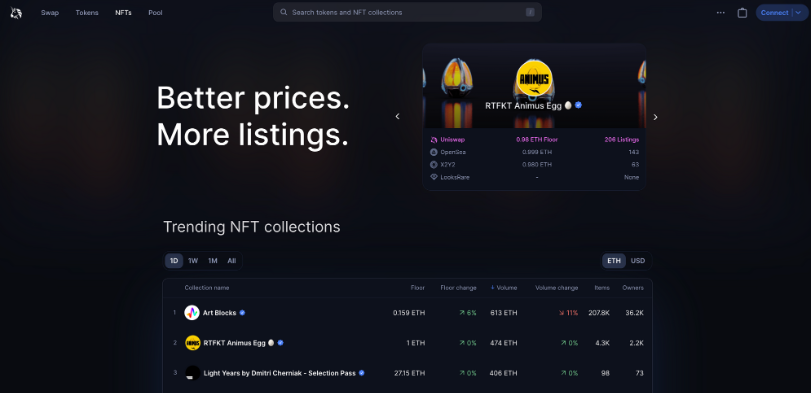

Uniswap Labs began integrating NFTs into its ecosystem in June 2022 by acquiring the NFT aggregator Genie, announcing plans to allow NFT purchases through its web app.

However, after Genie’s acquisition was announced in June, it remained largely silent. Nearly five months later, Uniswap finally launched its NFT aggregation platform—but perhaps failing to meet expectations, it generated limited discussion. The product offering was minimal and lacked standout features.

Figure 24: Uniswap Aggregator

Uniswap’s interface resembles other aggregators, displaying most essential data metrics for user reference.

Compared to Gem, Element, or even Genie itself, Uniswap NFT lacks analytical charting capabilities. Data dashboards are standard on other platforms, yet Uniswap NFT omitted this crucial component—especially surprising given its acquisition of Genie, suggesting insufficient commitment.

But this may align with Uniswap’s broader vision—it likely doesn’t intend to remain just an NFT aggregator. Instead, it aims to build an ecosystem that seamlessly connects FT and NFT trading.

Bridging FT and NFT trading isn’t trivial. Though ERC-20 tokens and NFTs operate largely as separate ecosystems, both are vital to digital economy development. Launching NFT functionality on Uniswap represents its first step toward interoperability and improved user experience.

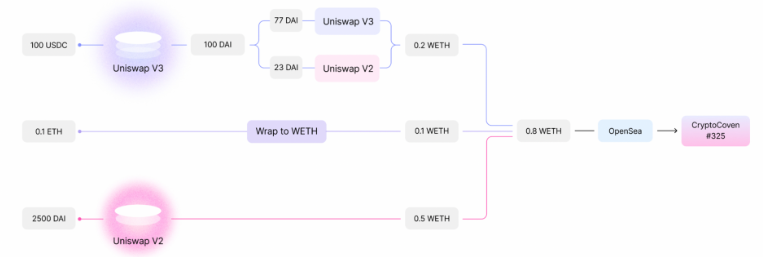

Moreover, Uniswap’s next-generation routing system, “Universal Router,” unifies ERC-20 and NFT swaps within a single router. Integrated with Permit2, it enables users to swap multiple tokens and NFTs in a single transaction, saving gas fees.

The entire process can execute as one transaction:

Figure 25: Flow Chart

Historically, FTs and NFTs were perceived as entirely separate experiences. Uniswap NFT introduces a new perspective—both are digital assets aiming to democratize ownership. They’re simply two different methods of unlocking value in the digital world, not inherently incompatible.

As the leading DEX, Uniswap can provide superior pricing options at the end of this workflow. Redefining the aggregator role enhances overall user experience and offers faster services—not by fighting for dwindling NFT market share, but by bridging FT and NFT ecosystems.

Within just two months, Uniswap attracted 864k unique addresses—an enormous footprint across the blockchain universe. Its ambitions clearly extend beyond mere aggregation. While Gen

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News