Grayscale officially files opening brief in lawsuit against SEC—what’s next for spot Bitcoin ETFs?

TechFlow Selected TechFlow Selected

Grayscale officially files opening brief in lawsuit against SEC—what’s next for spot Bitcoin ETFs?

What impact will the approval of future spot Bitcoin ETFs have on the secondary market?

By 0xbread, TechFlow

In June 2022, the SEC rejected Grayscale's application to launch a spot Bitcoin ETF.

Today, Grayscale has officially filed its opening brief with the appellate court, and Craig Salm, its Chief Legal Officer, stated on Twitter that the SEC’s rejection was “arbitrary and capricious,” amounting to “unfair discrimination.”

The reason behind the SEC's rejection of spot Bitcoin ETF applications is no mystery—they have repeated the same justification for five years: they believe the BTC market is prone to fraudulent and manipulated trading. Yet, the SEC has approved futures-based Bitcoin ETFs that rely solely on Bitcoin.

This is precisely the crux of Grayscale’s argument against the SEC.

Grayscale argues that the SEC must explain why it applies stricter standards to spot Bitcoin ETFs while being more lenient toward futures-based ETFs. Without sufficient justification, this constitutes clear inequity.

This naturally raises the question: as the world’s largest digital asset management firm, why is Grayscale so determined to launch a spot Bitcoin ETF?

Before answering that, let’s first understand why GBTC has existed and maintained a positive premium since 2015.

GBTC was launched to help high-net-worth U.S. investors gain exposure to Bitcoin within the boundaries of local regulations—just like buying a mutual fund. Since October 28, 2014, GBTC has suspended its redemption mechanism, allowing only one-way deposits of BTC but not redeeming GBTC shares back into BTC.

GBTC currently holds 635,240 bitcoins, worth $12.8 billion at current spot prices. This means each of its 692,370,100 outstanding shares is backed by 0.00091723 BTC.

Clearly, GBTC offers investors exposure to Bitcoin without requiring them to directly hold or self-custody the cryptocurrency. Thus, during previous macroeconomic periods of monetary easing, GBTC became highly desirable. Individuals and institutions unable to directly hold BTC flocked to buy GBTC, contributing to its high positive premium of up to 20%.

The existence of a positive premium also created another flywheel—arbitrage. Crypto firms could simply buy BTC on the secondary market, deposit it into Grayscale, and after the GBTC lock-up period (six months), sell the shares at a higher price to traditional institutions eager to enter, capturing profit margins as high as 20%.

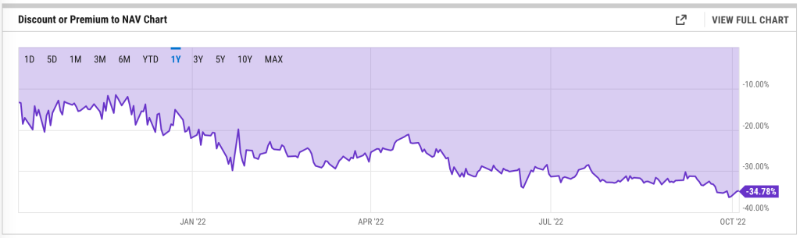

This model of sacrificing liquidity for returns thrived during bull markets. But what happened afterward is all too familiar: the collapse of Terra’s LUNA triggered a chain reaction across the digital asset market, delivering a devastating blow to an already fragile environment. Prior to that, the emergence of three Bitcoin ETFs in Canada had already caused GBTC’s positive premium to vanish rapidly, turning into a discount by March 2021. After the crash, institutions may have further sold off GBTC to meet margin requirements, deepening the discount relative to NAV (net asset value).

Therefore, the negative premium on GBTC can only disappear if Grayscale Investments successfully converts it into a spot ETF, or if investors once again become willing to pay a premium for GBTC’s non-redeemable Bitcoin holdings.

Will a spot Bitcoin ETF be approved in the future?

When it comes to successful ETF approvals, institutional investor interest likely plays a major role.

A survey conducted by Fidelity in September 2021 found that 52% of institutional investors held digital assets in their portfolios; however, 54% cited volatility as a significant barrier, and 44% said they lacked fundamental understanding of digital assets.

By April 2022, 80% of institutional investors expressed belief that digital assets might outperform traditional investment vehicles.

Then the Terra incident occurred, leading to bankruptcies of Celsius Network, Voyager Digital, and 3AC. Institutions that previously expressed interest in Bitcoin quickly changed their stance, saying they needed to reassess.

Given the profit-driven nature of institutions, it’s highly unlikely that Grayscale will receive SEC approval to return to a positive premium during a bear market.

However, as BTC and Web3 continue evolving and penetrating traditional sectors, more new and traditional institutions will embrace digital assets. When the next era of monetary easing arrives and investor confidence returns, GBTC—the Pac-Man-like vehicle that only takes in BTC—may once again become a bull market engine.

As previously mentioned, during bull markets, strong support from institutional investors greatly increases the likelihood of spot ETF approval. Yet even if approved, it would merely serve as a catalyst adding momentum to digital assets entering the next phase.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News