ETFs Are Just a Ticket to the Door: Bitcoin’s True Institutionalization Is Happening Where You Can’t See It

TechFlow Selected TechFlow Selected

ETFs Are Just a Ticket to the Door: Bitcoin’s True Institutionalization Is Happening Where You Can’t See It

Bitcoin is no longer just about ETFs—it’s the new infrastructure underpinning insurance reserves, rated bonds, and institutional collateral.

Author: Andjela Radmilac

Compiled by: TechFlow

TechFlow Introduction: ETFs only solve “how to buy Bitcoin”—but no one noticed that Wall Street is already using it for the same purposes it uses U.S. Treasuries and gold: collateralized lending, insurance reserves, and rated bonds. The February liquidation wave proved this system can withstand stress—but also exposed the fatal flaw of collective margin calls across leveraged chains.

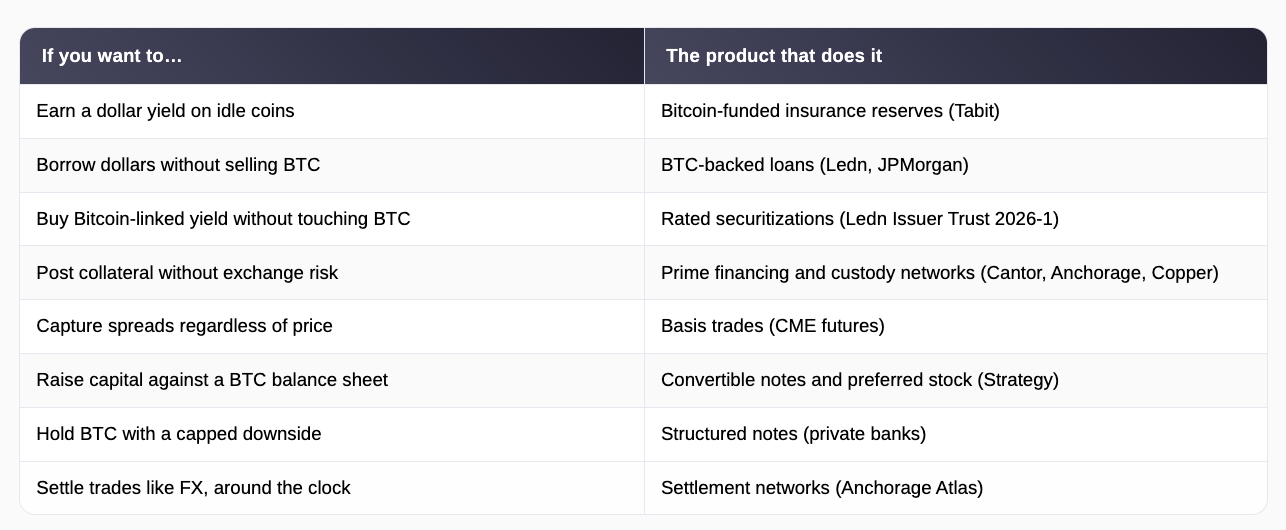

Everyone knows ETFs, yet almost no one realizes that, while ETFs absorb all the attention, dozens of institutional products built around Bitcoin are already live—from a $40 million insurance reserve in Barbados to S&P-rated bonds sold to Wall Street investors by Jefferies.

ETFs answer just one question: how can retail and institutional investors hold Bitcoin within a regulated wrapper? The products described in this article answer a different—and arguably more important—question: once you own Bitcoin, what can you *do* with it?

The answer is: exactly what finance has long done with U.S. Treasuries and gold. You can pledge it as collateral to borrow cash, use it as margin for trading, back insurance policies with it, or build corporate balance sheets atop it.

An asset capable of doing all these things simultaneously is sometimes called a *financial primitive*—a fancy term for “building blocks”: widely accepted, easily valued assets upon which the rest of the financial system stacks loans, bonds, and derivatives. Treasuries achieved this status because everyone agrees on their value—and on how to seize them if things go wrong.

Bitcoin is now undergoing the same test. Early results explain why some of the largest participants in this market truly, deeply don’t care about price movements.

Insurance Reserves, Consumer Credit, and the First Rated Bitcoin Bond

In March 2025, Tabit Insurance—a property and casualty insurer licensed in Barbados and founded by former Bittrex executives—capitalized its operations with $40 million fully funded in Bitcoin.

Essentially, Bitcoin holders deposit their coins to back real insurance policies covering storm damage and lawsuits against corporate directors. In return, they earn yields approaching 10% in USD. Policies and premiums remain denominated in USD, so customers never touch cryptocurrency—while Bitcoin sits as reserve capital, deployed to pay claims if needed.

Tabit holds a Class 2 license from the Barbados Financial Services Commission and operates as a segregated account company, meaning each investor’s fund pool is legally isolated from others—so losses in one account won’t deplete capital in another.

Regulators and auditors can verify reserves in real time on-chain—offering far greater transparency than traditional insurers provide in quarterly reports. CEO Stephen Stonberg notes the global reinsurance industry runs on roughly $800 billion in capital, while Bitcoin is a multi-trillion-dollar asset class; even a small fraction of that wealth flowing into underwriting would reverberate across the entire industry.

While insurance reserves represent a surprisingly novel use case for Bitcoin, lending is where money gets serious. Bitcoin-backed lending works simply: you pledge your coins to a lender, receive USD, and reclaim your coins upon repayment.

Holders do this because selling triggers taxable gains and forfeits exposure to future price appreciation—whereas borrowing against coins delivers cash without sacrificing either.

Platform trading volumes reached ~$2 billion in 2025. Toronto-based Ledn alone reports issuing over $9.5 billion since 2018. JPMorgan and other major banks have now launched similar offerings for their clients.

In February 2026, this lending business crossed into mainstream bond markets. Ledn completed a $188 million securitization—packaging 5,441 loans into a single pool and issuing bonds whose interest payments derive from borrower repayments.

The bonds were split into two tranches: a $160 million senior tranche, rated BBB− by S&P Global—the first-ever investment-grade rating granted to a digital-asset-backed security—and a $28 million junior tranche, rated B−, absorbing initial losses in exchange for higher yields.

By crypto standards, the underlying numbers are notably conservative. Of the 2,914 U.S. borrowers in the pool, outstanding debt totaled $199.1 million—but they pledged ~4,079 BTC, worth $356.9 million, yielding a loan-to-value (LTV) ratio of 55.8%. That means borrowers posted nearly $2 of Bitcoin collateral for every $1 borrowed.

Ledn CEO Adam Reeds says the structure creates a “direct pipeline” between liquidity-seeking Bitcoin holders and the world’s deepest institutional capital pools. Bitwise’s Head of European Research, Andre Dragosch, adds the deal proves traditional finance now views Bitcoin as legitimate—and even pristine—collateral.

The structure faced an immediate stress test—revealing both the model’s strength and fragility. From mid-January to February 2026, Bitcoin fell ~27%, pushing the pool’s aggregate LTV ratio upward and triggering margin calls—automated demands for borrowers to post additional collateral or risk forced liquidation.

Ledn ultimately liquidated roughly one-quarter of the loans originally intended for the transaction. Sales still closed successfully—partly because these automatic liquidations functioned precisely as designed, and partly because Ledn has never incurred losses when selling collateral due to defaults.

The reverse consequence to remember: when many lenders run identical triggers against the same volatile asset, sharp price drops force simultaneous sales—and those sales further depress prices, triggering more margin calls. The system passed its first true test—but also revealed precisely where it collapses under sufficient stress.

Collateral Networks, Arbitrage Trades, and Corporate Balance Sheets

Beneath these products, the market’s foundational mechanics are being rebuilt—resembling money and bond markets, where the firm holding your assets, the platform where you trade, and the system settling transactions are three distinct entities.

Anchorage Digital operates the only federally chartered crypto bank in the U.S. In April 2024, it launched its Atlas settlement network—enabling institutions to settle trades directly with each other, eliminating the need to park funds in custodial accounts or pre-fund exchanges.

By March 2026, Atlas had connected nearly 600 participants—four times its count a year earlier—and processed tens of billions in settlements. It has since expanded into collateral management: the bank now monitors loan positions on behalf of lenders, issues margin calls, and executes liquidations.

In March 2025, Cantor Fitzgerald selected Anchorage and Copper.co to play this role for its global Bitcoin financing business. Copper’s ClearLoop system lets trading firms lock coins with custodians while still trading across multiple exchanges—ensuring a repeat of the FTX collapse won’t sweep away client assets.

All this makes posting Bitcoin as margin as routine and secure as posting Treasuries—a prerequisite enabling every other development mentioned in this article.

The massive institutional capital flowing through this infrastructure holds *no view whatsoever* on Bitcoin’s price. Basis trading—one of the most popular institutional strategies since ETFs launched—exploits the fact that Bitcoin futures typically trade at a slight premium to spot: funds buy spot Bitcoin or ETF shares while simultaneously selling futures contracts at higher prices, locking in the spread regardless of subsequent price moves—gains on one leg offsetting losses on the other.

Once ETFs gave funds a simple way to hold the spot leg, hedge funds built record short positions in CME futures—open interest climbing from ~30,000 contracts in early 2024 to a peak near 45,000 by November.

This trade grew so large that unwinding it now moves markets independently: CME open interest dropped below $10 billion in April 2026 as paired positions closed, mechanically driving prices lower irrespective of sentiment.

CME continues building for this cohort: launching 24/7 trading in May 2026, then introducing Bitcoin Volatility Index futures in June—letting institutions bet on—or hedge—the *magnitude* of price swings, not their direction.

Corporate treasuries push this idea furthest. As of late May 2026, Strategy held 843,738 BTC. To fund its aggressive BTC purchases, it issued $6.7 billion in convertible notes—bonds convertible into stock if the share price rises—and $15.5 billion in preferred stock across five distinct instruments: fixed-dividend securities ranked between debt and common equity.

It raised $25.3 billion in 2025 alone—making it the largest U.S. equity issuer that year, accounting for ~8% of total issuance. It markets its preferred securities as “digital credit”—a full fixed-income product line whose dividends are ultimately serviced by its Bitcoin balance sheet.

Shareholders gain leveraged Bitcoin exposure via stock; dividend investors earn double-digit yields backed by Bitcoin—imitators like Tokyo-listed Metaplanet and Semler Scientific replicating Michael Saylor’s risk playbook.

Private banks run parallel assembly lines for wealthy clients—packaging structured notes that cap downside exposure to Bitcoin in exchange for surrendering part of its upside, letting conservative portfolios hold an asset otherwise deemed too volatile.

This brings us full circle to the opening paradox.

ETFs answered *how* institutions hold Bitcoin; the products described here answer *why*. An asset that simultaneously capitalizes Caribbean reinsurers, backs investment-grade bonds, secures CME derivatives, and services preferred dividends has long transcended speculative adoption—it’s embedded in finance’s operating machinery.

Historians of this market may ultimately view ETFs as the visible, first layer of institutionalization—while lasting change occurs deeper, within funding and settlement systems where Bitcoin fulfills the roles Treasuries and gold have performed for generations: serving as collateral, upon which everything else is built.

Risks are real—as the February liquidation wave demonstrated—and compound with leverage. But the direction appears set: Bitcoin’s most consequential institutional role may never appear on capital flow charts—because it’s becoming part of the machine itself.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News