How to Build an Innovative Economic Model for Web3 + Gaming?

TechFlow Selected TechFlow Selected

How to Build an Innovative Economic Model for Web3 + Gaming?

Strong player social dynamics and network effects are key to surviving the volatility of the crypto market.

Organization Introduction

About 2DAO3

The founding mission of 2DAO3 is simple: to organically bridge "2" and "3", helping more people who wish to transition from Web2 to Web3 become active participants, and supplying higher-quality talent to the Web3 ecosystem. We don't see Web2 and Web3 as binary opposites—Web3 isn't built by belittling Web2. We welcome more like-minded Citizens to join us and co-build the future together.

Linktree: https://linktr.ee/2dao3

About W Labs

W Labs is an institution focused on the blockchain gaming vertical. Currently centered on original content creation, it also provides research analysis, modeling, and operational consulting services for blockchain gaming projects. In the future, W Labs aims to become a one-stop infrastructure service platform for blockchain games, incubating various products related to blockchain game services.

Linktree: https://linktr.ee/Wlabs

Event Recap

On July 23, 2022, 2DAO3 hosted its second private roundtable discussion. Co-organized by 2DAO3 and W Labs, the event welcomed Jeffrey from RCT, Aiko from Folius Ventures, and Kluxury from W Labs, focusing on how to build innovative economic models for Web3 + gaming. The following is an edited excerpt from the event, with some content revised for clarity.

1) Overall, what are the similarities and differences between Web2 and Web3 games in terms of business models?

@Jeffrey

The business models of Web2 games generally fall into several categories: paid downloads, subscriptions, DLC/skin microtransactions, and in-game advertising. For Web3 games, we currently mostly see land sales, item sales, and transaction fee commissions from marketplaces.

From the perspective of fundraising and liquidity, Web3 games have significant advantages over Web2. This model is indeed disruptive to traditional gaming, but many Web3-focused games today ultimately turn into Ponzi schemes. Both founders and users end up focusing on trading volume rather than the game itself or new content releases.

Traditional game companies sell users gameplay content—the sale of items is only part of their revenue. As long as the content is good, players will spend money—buying monthly passes to grind, opening loot boxes for skins, or spending time watching ads. These behaviors are all consumption based directly on game content, and traditional Web2 players do not earn any financial returns from them.

From this angle, Web3 founders should first consider how to get players to naturally re-engage with the game ecosystem—not how to design economic incentives that drive frenzied purchases, or how treasury buyback mechanisms can extend profit timelines. Without compelling gameplay to attract users, even the most sophisticated tokenomics will eventually collapse into Farm & Dump cycles. There are many proven Web2 business models that Web3 hasn’t yet adopted—and these could be leveraged effectively.

2) Compared to Web2 games, what key factors are currently limiting the development of Web3 game business models? (Delphi’s article points out that the capital structure of blockchain games harms the experience of loyal players.)

@Kluxury

My perspective comes largely from that of a Web3 player, so some of my views may differ from other panelists.

To answer the first question briefly: compared to Web2, current Web3 games lag significantly in gameplay, content, and visual quality. Issues like off-chain games with on-chain interactions are commonly criticized. From a technological standpoint, I don’t think these gaps can be closed in the short term.

Even if we could perfectly migrate traditional game experiences onto the blockchain (tokenizing in-game currencies, NFTizing items, etc.), liquidity of tokens and NFTs remains a critical and highly restrictive factor.

A major distinction between Web2 and Web3 business models lies in tradability. In Web2, in-game items are one-time purchases without resale value—like skins bought or pulled in Honor of Kings or Genshin Impact, which cannot be traded externally. While this benefits publishers in the short term by enabling continuous monetization events, it may not be optimal for the long-term health of the industry. In contrast, tradability and liquidity are core features of Web3. Game companies typically earn recurring fees from secondary market transactions. When a project gains traction, this can generate extremely high-frequency revenue—for example, STEPN's transaction fees were astonishingly high. If Web3 games flourish in the future and cross-game item interoperability becomes possible, it would undoubtedly benefit the entire industry.

Liquidity is crucial. Limited liquidity restricts both game development and player experience. Randomness and gambling mechanics—such as gacha pulls, mystery boxes, refining, forging—are integral to many games. In traditional Web2/3 games, these easily create addictive loops due to frictionless, scalable purchases.

In Web3 games, however, players must first acquire tokens via LP (liquidity provider) pools before depositing them into the game—requiring deep liquidity. Current GameFi projects typically allocate only 10–20% of their tokens to LP pools. Even if a game is fun, insufficient liquidity limits spending by whales. The market simply can’t absorb large transactions. Farmers World stood out largely because it attracted significant capital from the SZ Ponzi scheme, allowing high capital absorption and accommodating big investors.

To address this, I have some initial ideas—such as integrating lending or Lego-like composability—to solve the Ponzi problem caused by lack of real-world utility. Recently, a guild project won an award at the Ethereum New York Hackathon, aiming to build a guild aggregation platform featuring NFT sharing: ownership remains with you, but usage rights can be delegated to others.

3) How should one balance traditional business models with crypto-native ones?

@Aiko

Let me first address previous questions:

First, the issue of capital scale:

Making large capital feel comfortable aligns with DeFi logic—good liquidity allows big money to enter. But within gaming logic, large investments naturally expect large returns—a double-edged sword. Games inherently lack external liquidity. Now, if we demand not just liquidity, but *high* liquidity, that seems excessive.

Second, guild-based leasing, lending, and asset sharing:

Guilds exist because of Play-to-Earn—they represent a tech tree branch of blockchain/Web3 gaming, raising awareness and fueling popularity. However, beyond the top three guilds, most have small market caps and little pricing power. Without flagship games, lower-tier guilds hold no leverage. Building lending systems atop such weak foundations is unwise. Moreover, developers often dislike rentals—leasing economies are delicate. You need non-paying players to enjoy benefits while landlords don’t lose money. Balancing these interests requires intricate rules and fine-tuned mechanics.

Regarding balancing traditional and crypto business models—it depends entirely on the project team’s product traits and goals. There’s no absolute right or wrong—everything hinges on the team’s revenue expectations: Do they want cash flow or tokenomic growth? They must clearly define their target user ecosystem.

Business models can be divided into five tiers:

The most traditional is Legend 4.

Legend 4’s token crashed hard. Yet Wemade’s WEMIX token held up well, and Wemade’s stock tripled. Because their revenue sources differ, so do their strategic options.

The second tier is “chain-modding.”

Some mid-tier studios unable to secure licenses domestically attempt to “blockchain-enable” existing games—adding tokens or NFTs and launching INOs/ICOs. But users and VCs must evaluate whether the token captures real value.

The third tier combines traditional payment methods with Web3 benefits.

For instance, enabling open secondary markets or letting players cash out via tokens—many games aim here. Traditional gamers aren’t used to crypto workflows, so they prefer credit card payments and fiat on-ramps. Charging via subscriptions or playtime makes sense—but exiting poses challenges: Can tokens be exchanged for equivalent fiat-value goods? Could a floating exchange rate or oracle determine prices?

The fourth tier leans toward DeFi-style games.

Take League of Kingdoms (an MMO strategy game where players buy NFT land; landowners harvest 5% internal resources and receive 10% net profits in xDAI). Later, they raised funds and found many users couldn’t grasp SLG mechanics—it was too complex. Last year, they launched Drago Sticker NFTs—three dragons fighting together. Game designers may compromise on gameplay or token design depending on whether they’re targeting DeFi yield-seekers or mainstream gamers.

The fifth tier is fully on-chain games.

These resemble Fomo 3D, borrowing Bancor’s mechanism. During DeFi Summer, fully on-chain gambling games emerged—if they innovate at the contract or gameplay layer, they might become the next breakout. Another type, like Dark Forest, encodes all logic on-chain. But Dark Forest isn’t a strong economic vessel—it rewards players with xDAI each round, relying on stablecoins, and the community must organize competitions manually. An ideal version would be a full-chain game with a coherent world-building framework and intuitive mental model. Project teams are still refining such designs.

@Mike

Fomo 3D mechanics are already widely reused—one module in our current project uses it, akin to a grand博弈. It’s quite engaging and well-suited to amplify FOMO under current market conditions.

On balancing traditional and crypto models—I’ve spoken with project leads and traditional game executives. Their top priority is cash flow. Many successful projects today have already recouped costs through IDOs.

This resembles a high-leverage model—like China’s property developers previously using 99% leverage, funded by banks or trusts, then pre-sold to buyers with mortgages. In growing industries, higher leverage amplifies returns. Thus, traditional game publishers eyeing blockchain games likely favor financialized “operational leverage” models.

4) How should a team determine product positioning based on its inherent strengths (which types of games are better suited for blockchain)?

@Aiko

Markets evolve with user habits. Today’s players have only 5–10 minutes of fragmented time—they can’t be forced back into the MMO era.

Many Web3 developers abroad now study mobile gaming’s “monkey data” business model, believing it better drives in-game spending. This approach should also apply to crypto games.

Games like Genshin Impact or character-collection card games require massive content depth, demanding exceptional operational stamina and rich character pools.

If referring to pure Hearthstone-style card games, Skyweaver offers an example. It uses AMM cards—prompting questions: Do cards really need such high liquidity? How to ensure value and match efficiency? Skyweaver has strong industry reputation, starting in 2018, carefully studying player demand for secondary market liquidity and per-match rules like drop rates. Their next version will introduce a token and sticker-skin rewards, with rigid monetization structures. But their team isn’t game-first—they prioritize technical layers (wallets, AMMs)—so player-centric thinking is weaker.

Match-3 casual games: consider Gamee ($GAMEE), popular earlier in India on Polygon. Players earn small cash rewards per level. Traditional Web2 does similar things, but perceived value is weaker in crypto, and entry barriers are higher—making user acquisition harder.

Some try building mini-games for NFT communities, but these use cases often just sell NFTs—usage drops after a month, because NFT communities don’t actually need the game.

SLG genres are favored by Western institutions like Delphi Digital. SLGs naturally feature warfare and resource consumption—do current players understand this? Also, from a go-to-market perspective, if the user base isn’t balanced between Web2 and Web3 players, but purely Web3-native, it’s no different from today’s Ponzis—just internal competition and zero-sum games.

An interesting auto-battler example: Arrivant’s economic model. For instance, levels 1–100 each unlock specific resource access—Level 1 gets Resource A, Level 2 gets B, Level 3 gets C. Guild members recruit others; as they level up, teammates gather complementary resources. I doubt this model works—player time investment must correlate with XP, progression, and level. Calculating server-wide distributions (how many 20-level vs. 60-level players) and allocating resources accordingly is impractical. Gameplay appears tower-defense-like (where players place turrets to stop enemies), but it’s fast-paced—five enemy waves in five minutes, requiring tactical adjustments every minute, sometimes involving small roadblocks or randomized outcomes. Arrivant blends SLG, tower defense, and partial card mechanics, with cost systems.

5) What support can VCs offer startups or transitioning companies? (What should teams ask of VCs?)

@Aiko

I’d emphasize: as a project team, what should you demand from institutions? Ask directly—don’t hesitate. If they refuse, that’s their problem.

Some foreign developers are experts themselves and don’t need VC guidance. Always maintain critical thinking when evaluating advice.

Strong founders early on may access institutional networks or FA referrals. This space is mixed in quality—as I said, it depends on your own expectations. If you aim to build great games with novel mechanics targeting Web2 players, you might lean toward Flow or Solana ecosystems. But if your FA specializes in low-tier Ponzi schemes, you’ll need to be cautious in selection.

First, ask them to map developer and user ecosystems across chains—what support can they connect you with from your chosen chain’s ecosystem? Negotiate these early.

Second, conduct due diligence on your VC. Just because they know many people doesn’t mean you should accept all introductions blindly.

Third, regarding fundraising—don’t limit yourself to VCs. Sometimes partnering with established projects brings greater value: technical collaboration, ecosystem integration, or funding. Game teams should reach out to guilds early, even during seed rounds.

6) For Web2 companies wanting to transition, should they pursue [evolving games into the metaverse] or [embedding blockchain games within metaverse environments]?

@Kluxury

-

Card games: Whether Skyweaver or earlier Splinterlands (long dominating DappRadar’s user rankings), they rely on offline tournaments to sustain interest. Card games don’t suit current P2E models—without revolutionary new designs, breaking through in GameFi will remain difficult.

-

SLG Strategy: I believe this is currently among the hardest genres to blockchain-enable. SLGs start with solo progression, but later shift to intense PvP conflict with escalating resource consumption. Undeniably appealing to high-spending players, but their slow-burn pace clashes with crypto’s fast-in, fast-out rhythm.

-

MMORPGs: Not promising in the short term—too challenging and costly. But as a long-term vision, once foundational frameworks exist, MMORPGs could find their niche. Traditional PC MMORPGs have stagnated—players still engage with titles from 2014 or earlier, while studios mostly tell stories. This reflects broader trends—fragmented player time. Still, many gamers deeply desire a “Ready Player One” scenario given the chance.

[From Games to Metaverse]: Originally just making games. Once a game reaches maturity, transition into storytelling—launch sequels, then integrate into a unified platform. Projects like Axie or RACA now pitch their “metaverse phase” to users.

[Embedding Games Within Metaverse]: Build the environment first, then populate it with games. Artiverse plans to release Endless this December, with more to follow. Gala wants its own full ecosystem, though progress is slow.

Many Web2 game companies aspire to build game ecosystems. Projects entering via gaming platforms—like Gala or P12, aiming to be blockchain Steam—seek to attract games. Others, like Ultiverse, build vast worlds first, then develop large-scale RPGs like Endless. From a Web3 user perspective, none of these resonate strongly. The core issue? Insufficient interconnectivity. Beyond NFT sales and cross-NFT collaborations, there’s little meaningful linkage. True in-game composability—a key user expectation—is missing. Projects like Sandbox, centered on land ownership, currently emphasize social or IP creation aspects, which I exclude from this broader ecosystem discussion.

Personally, the entry point doesn’t drastically affect overall ecosystem development—only impacts entry difficulty and risk levels. Single-game entry is easier, but due to lifecycle constraints and “new over old” market sentiment, reviving declining interest becomes extremely difficult.

Web2 companies hold major advantages in game resources and teams over most Web3 projects, yet actual results often disappoint. A key reason? Their mindset remains traditional. For example, taking outdated games from databases, making minor blockchain tweaks, hyping IPs, selling PFPs—users aren’t convinced. Worse, single-game “chain mods”—gold becomes a child token, diamonds a parent token, mystery boxes become NFTs in a one-click trifecta.

Web3 players aren’t pure gamers. The economic model is equally crucial. Narratives must be logical and backed by executable roadmaps. Web3 users care less about corporate pedigree and more about roadmap execution—this builds community confidence and fosters decentralized consensus.

7) As the GameFi sector evolves, does W Labs have concrete ideas for economic model design?

@Kluxury

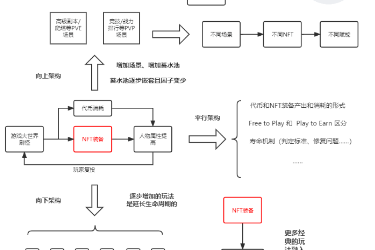

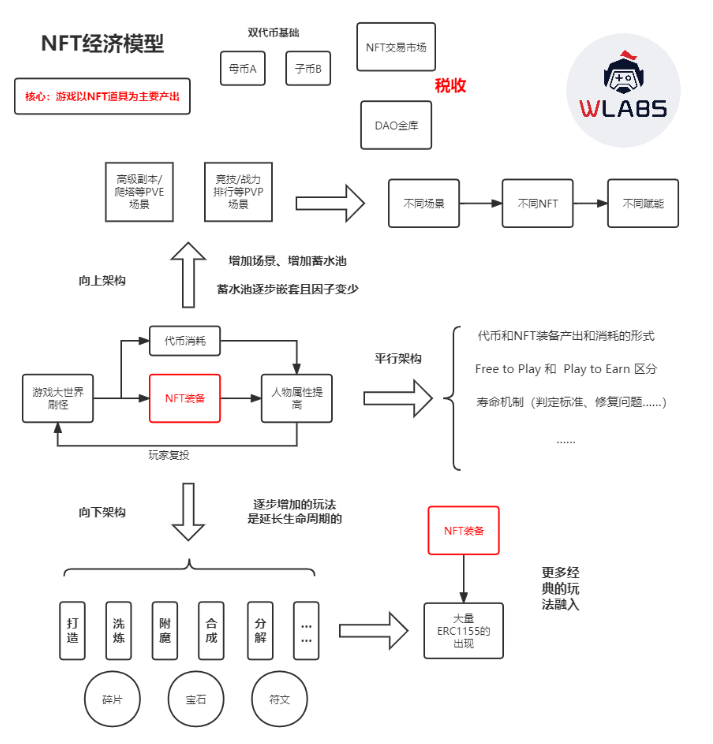

We already have several frameworks. NFTs will inevitably play a central role in GameFi. Let me briefly explain using an NFT template:

Core premise: games primarily produce NFT items.

Foundation: Dual-token model. This is currently the most stable system, validated by the market. So we adopt it for now.

NFT Marketplace: Must be proprietary, not third-party. At least for now, marketplace taxes are the primary revenue source for the project team.

DAO Treasury: Still largely narrative-driven at this stage.

Scenario 1 represents a typical Ponzi-like GameFi 1.0 setup—latecomers continuously fund early entrants. Often, teams offload token selling pressure onto NFTs; when the NFT “reservoir” overflows, death spirals begin.

Extending upward: Most projects offer players too few choices—99% of entrants follow a单一“play-to-mine-and-dump” path. We propose adding diverse scenarios and reservoirs—PvE, PvP—with distinct characteristics, empowering users through varied incentives and consensus-building. Of course, these unfold across different phases.

Horizontally: Enrich core mechanics—token and NFT generation/consumption, Free-to-Play vs. Play-to-Earn differentiation, lifespan determination, and repair mechanisms.

Downward extension differs from upward: vastly increasing item quantities. Diversified gameplay prolongs project lifespans. This area is where traditional games excel.

Key takeaways:

-

Web2 and Web3 users currently differ significantly in attributes and acquisition strategies

-

Ponzi dynamics are acceptable initially—the key is whether later stages can absorb prior bubbles

-

Project revenue should primarily come from taxes, not just latecomer capital

-

Building consensus isn’t hard—especially with strong IP—but maintaining it is. Community is paramount.

-

If a team has full confidence in its gameplay, mechanics, visuals, etc., success is assured—whether in Web2 or Web3—as long as the game is truly fun.

@Mike

Eventually, any system must rest on taxation. When a society forms, people can “seize the tyrant’s wealth.” But as it matures, institutional stability and consistent taxation become essential. I hope to explore this further with the audience.

8) RCT’s practical experience and challenges transitioning from Web2 to Web3 (Mirror World, Delysium, etc.)—covering fundraising, product, and users

@Jeffrey

Since 2018, RCT has provided AI algorithms, NPC design, and scene-generation technology to traditional game developers. Leveraging our AI and game algorithm expertise, we create interactive NFT assets—an aspect often missing in the NFT narrative.

Now, we aim to combine our AI strengths with traditional game development experience to create multiplayer shooters familiar to Web2 gamers. Our ultimate goal is to provide in-game editors so users and publishers can create custom scenes and items, incorporating interactive digital assets.

We began Mirror World in September last year, continuing RCT’s original vision of creating interactive meta beings. Within a month, we developed AI NFTs while building community content and gathering feedback. By November, we pivoted toward GameFi, aiming to build a digital world with cross-game asset interoperability.

Currently, NFT transaction ecosystems fail to fully capture value—users often need multiple platforms to complete one trade. In Web2, purchasing takes just a few clicks—experience gaps are huge. We’re starting with mobile casual games. A multi-game interoperable Game Matrix can improve UX and solve fragmented liquidity issues. On top of this, we’ll provide mobile SDKs for developers to create new content. Ultimately, we envision a closed-loop ecosystem where all players and editor users coexist. We recently joined Solana’s ecosystem—including their hardware phone—and hope to see more developers embrace Web3 mobile apps.

With nearly 200 developers on product, I’m highly confident in our transition. Stay tuned for updates. Trinity: The team has a strong artistic flair, excelling in abstract and philosophical thinking. RCT’s official WeChat articles are excellent. Underlying AI and game engine capabilities are robust. Mid-layer commercialization includes deep GameFi understanding and UX expertise.

9) How can Web3 games appeal to Web2 gamers? What user needs must be met?

@Jeffrey

First, gameplay. The fundamental purpose of any game is entertainment. Many high-volume Web3 successes aren’t really games—they’re gold-farming or mining operations. In traditional gaming ecosystems, gold farming is marginal. A healthy gold economy requires both whales and a solid base of casual gamers.

Second, price sensitivity. Over half of Web2 game revenue comes from free-to-play titles. Even premium hits like Call of Duty charge only $70 per copy, while development costs exceed $300 million. Expecting Web2 players to pay hundreds for a game with tens of millions in dev cost—just to farm gold—is unrealistic.

Third, user experience. In traditional mobile games, a microtransaction takes two or three taps—barriers are extremely low. In Web3 games, users must compare exchange fees, preload wallets, switch platforms—entry barriers are prohibitively high for traditional gamers. Multi-platform external trading causes game developers to miss out on value capture. Most teams end up reverting to selling land and items.

Finally, for Web3 games, strong player socialization and network effects are key to survival during crypto market downturns. While many Web2 games lack strong social features, in P2E, assets live on-chain and liquidity ties directly to crypto markets. All Web3 players exist in an open PvP ecosystem. When your NFT legendary weapon halves in price, you can still show it off in your guild or carry your random teammates. These moments give NFTs intrinsic value. When markets crash and whales dump, these interactions and embedded values become the reason users HODL.

Q&A

Some respondents were audience members attending the event.

1) From a financial regulatory perspective—especially macroprudential oversight—how should we view the impact of in-game tokens and stablecoins on the broader financial system?

@Ken—Partner, PwC China Financial Institutions Services

Economic design involves many principles closely tied to finance. From my view, two key issues stand out:

First, establishing trust. People transact with centralized markets under asymmetric information—systems must build user trust and align expectations. Everyone should perceive asset value similarly. Users anchor NFT and crypto prices to assess value, but directly tying asset value to a currency symbol risks systemic resonance effects—dangerous in any financial system. That’s why Terra collapsed—many security tokens lacked proper mechanisms because expectations weren’t hedged.

Thus, in designing NFT or mining mechanisms, different users should derive different value. Some profit from going long NFTs, others from shorting. Simulate financial market expectations to form organic pricing—not just universal appreciation leading to Ponzi dynamics. Early stages can use Ponzi mechanics to establish asset value, but if the entire system relies on it, massive bubbles emerge. Without self-correcting mechanisms, herd behavior dominates.

Second, cross-game trading mechanisms should mimic financial exchange rate formation. At the ecosystem level, we need valuation mechanisms reflecting divergent user expectations—creating differential valuations. To resolve trust issues, relatively neutral intermediaries are needed, along with socially constructed value bases—some contribute labor, others gain from asset appreciation (e.g., land sales). This creates hedges, reducing overall macro risks.

Lastly, when forming consensus mechanisms, incorporate diverse rule designs to ensure long-term, stable operation—the foundation of trust. Without this, users act shortsightedly, preventing systemic stability.

@Mike

From a player’s view, we’ve observed that if all players believe they’ll break even in 30 days, the game’s death spiral accelerates dramatically. If the model is complex enough that ROI estimates vary across a range, the game lives longer. Layering nested mechanics and副本 increases volatility beneficially.

@Ken—Partner, PwC China Financial Institutions Services

When designing macro ecosystems for regulators, this point is crucial: First, how to build collective trust—achieved through diversification. Second, fostering divergent expectations—which strengthens trust formation.

2) In-game DeFi and NFTfi (stablecoins and lending): How do they compare to DeFi stablecoins? What lessons can be drawn?

@mindao—Founder of dForce

DeFi’s three pillars: stablecoins, lending, swaps. On the NFT side, lending is most integrated. Many wonder whether GameFi needs a dollar-pegged or otherwise stable in-game currency.

Decentraland, one of Ethereum’s earliest Metaverse games, prices land in MANA—but friction is high.

Another trend emerging: fiat-backed stablecoins or native system stablecoins may soon become core components of GameFi. There are clear advantages. Decentralized stablecoins in DeFi have already proven viable—via over-collateralization. This model is validated.

GameFi is a crypto-native economy with organic demand for transactions and lending—more fundamentally sound than DeFi, where most demand stems from yield farming and leverage, which are highly cyclical. For GameFi, stablecoins offer obvious benefits.

Metaverse games need economic interaction with other games—value spillover enhances significance. Stablecoins serve as natural bridges, frictionlessly connecting external worlds and other game economies.

Stablecoin monetary policy should be managed by GameFi operators, enabling controlled economic expansion. Currently, GameFi stablecoin thinking is limited—likely due to developmental stage. For example, STEPN built its own DEX because swapping is their biggest use case. Stablecoins may come next. As lending expands—NFTs being borrowed, leveraged—the need for stablecoins will grow organically. I believe one to two years from now, GameFi projects will launch native stablecoins.

Ideally, design stablecoins into GameFi economic models early. Earlier implementation makes liquidity easier to bootstrap. Games can control liquidity supply—providing their own liquidity for lending markets and DEXs—greatly benefiting adoption and value capture.

@Mike

DeFi will eventually become foundational infrastructure—like blockchain itself, a financial hub. Many GameFi projects now integrate DeFi elements, like Defi Kingdoms. I believe DeFi fundamentals are indispensable to GameFi.

3) How to design a mechanism encouraging users to trade NFTs on the game’s built-in platform instead of external ones like OpenSea?

@Mike & Kluxury

Two methods:

First, set lower fees on the in-house platform than OpenSea;

Second, code into the smart contract that while external trading isn’t banned, post-trade there’s a cooldown period—e.g., 12 hours during which the item can’t be used. This incentivizes use of the internal marketplace.

Additionally, this touches anti-cheating measures. When designing models for clients, fairness is often critical. Many games are ruined by bots—script farms outperform regular players significantly, undermining fairness. We aim to solve this via in-game NFT platforms: by setting transaction thresholds and fees, transferring NFTs externally and then farming becomes economically unviable.

From a player’s view, most wouldn’t use OpenSea anyway. OpenSea serves all NFT projects, but game NFTs are highly specialized. Native platforms offer better filtering and convenience.

Game aggregators acting as GameFi trading systems. Currently, individual games have short lifespans, so no aggregator breaks out. But if games persist for six months to a year with steady pipelines, such aggregators will multiply (STEPN had such plans earlier).

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News