More than ten Web3 unicorns see 50% decline in off-exchange valuations, signaling weakness in primary markets amid bear market

TechFlow Selected TechFlow Selected

More than ten Web3 unicorns see 50% decline in off-exchange valuations, signaling weakness in primary markets amid bear market

How can entrepreneurs survive and raise funds during a bear market?

Author: Julian

"If we had delayed investing in this Web3 company by two more months, the valuation would've been half as much—we're all blaming me for moving too fast," laughed Mark awkwardly after returning from the Polkadot Ecosystem Conference in Hangzhou.

In April this year, his Web3 fund invested in a GameFi project at a $45 million valuation. By May, the project proactively lowered its valuation to $35 million for further fundraising. Now, the project's public fundraising valuation has dropped to $25 million.

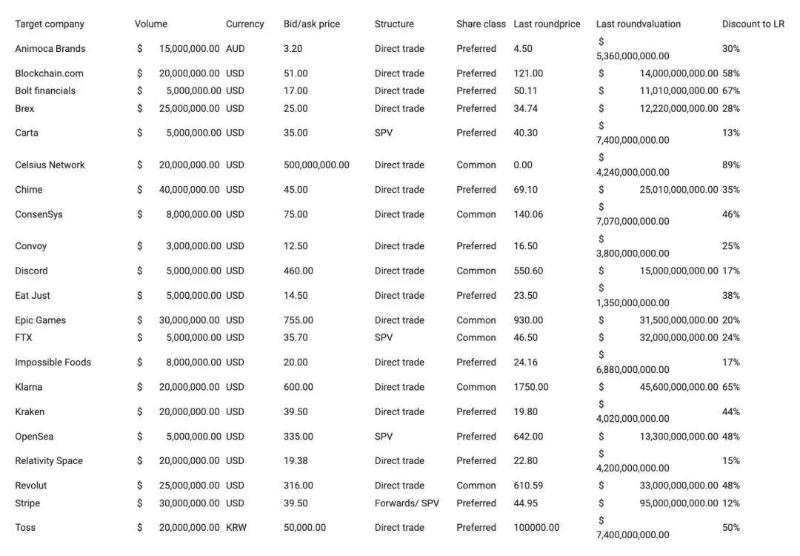

Under bear market conditions, most projects struggle to avoid first-tier valuation declines. Data compiled by Messari founder Ryan Selkis shows that over-the-counter trading prices for many Web3 unicorn investments are now significantly below their last funding round valuations—high-profile cases include OpenSea, FTX, and ConsenSys. More than 10 Web3 unicorns have seen valuations drop by around 50%, with some falling as much as 90%.

One extreme example is BlockFi. In March 2021, BlockFi raised $350 million at a $3 billion valuation. Later that same year, it reportedly raised funds at a valuation exceeding $5 billion. In June this year, The Block reported that BlockFi was seeking funding at a $1 billion valuation. Just over a year later, news emerged that FTX is acquiring BlockFi at a variable price of up to $240 million.

This reflects the real state of the Web3 primary market during the bear market: project valuations are declining, institutions are generally cautious and holding back, while major platforms accelerate industry consolidation through acquisitions.

Against the backdrop of a cooling Web3 primary market, G3 spoke with over a dozen Web3 investment firms and entrepreneurs to explore investment and entrepreneurial opportunities during the bear market.

Primary Market Begins Cooling Down

"We’ve been reviewing projects for the past three months but haven’t made any moves yet," said KiWi, an investor at a top-tier exchange. By the end of 2021, they detected rising risks in global capital markets. Monitoring new listings across exchanges, they noticed many projects suffering from inverted pricing between primary and secondary markets—indicating immediate post-IPO drops. They concluded the bear market would soon spread from secondary to primary markets and promptly hit the pause button on investments.

Since late last year, warnings about Federal Reserve rate hikes and inflation have echoed constantly. Yet many professional institutions, due to excessive momentum, failed to exit during this clearly cyclical downturn.

During bull markets, when profit effects are strong, both retail investors and institutions tend to abandon rational, long-term cash flow-based valuations for crypto startups. Instead, they rely heavily on comparable company analysis and peer benchmarking, causing project valuations to inflate rapidly.

For instance, the X-to-Earn trend earlier this year led many institutions to invest heavily in GameFi projects. According to crypto media Odaily, Q2 2022 saw 82 GameFi-related funding rounds, accounting for 16% of total market deals and $2.996 billion in funding—23.5% of the total market volume—making GameFi far outpace other sectors in both deal count and amount raised.

Now, as Federal Reserve rate hikes continue and broader risk assets decline, bear market pressures have caused X-to-Earn projects to collapse, likely dragging down valuations for many such crypto startups.

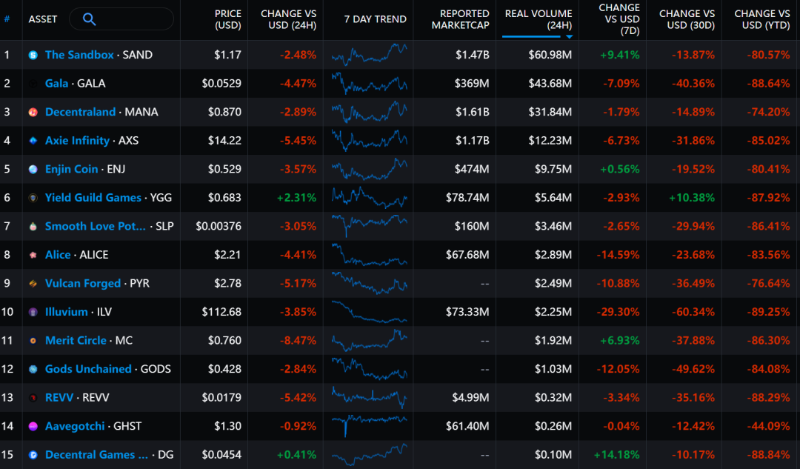

GameFi sector one-year performance. Data source: Messari

Take StepN, the leader in X-to-Earn: among hundreds of analyses, most overlook a key factor—Binance. StepN’s success hinged on Binance’s full-scale incubation and strategic support, combined with its clever Ponzi-style economic model, ultimately achieving a peak market cap in the tens of billions and fueling the entire X-to-Earn trend.

Treating such a uniquely timed and supported project as a standard benchmark and applying its valuation to similar projects in public markets inevitably leads to overpaying, resulting in misalignment between primary and secondary market valuations.

0xTodd, partner at Nothing Research, believes valuation inversion between primary and secondary markets is especially pronounced in the Web3 space. "The entire Web3 sector is still in the concept validation phase—characterized by minimal cash flows and user growth driven largely by subsidies. Under these conditions, success heavily depends on bull market narratives—essentially selling dreams. Once the bear market hits, data metrics immediately shrink by an order of magnitude, making secondary market performance hard to sustain."

Startups Face Increased Fundraising Difficulty

"Terra (LUNA and UST) collapsing was a clear turning point, causing many mainstream investors to lose interest and slow down venture investments in Web3," said a DeFi project lead. Several traditional VC firms, including top-tier dollar funds, were previously in talks with them—but paused negotiations after Terra’s collapse.

Due to lagging transmission effects from secondary to primary markets, Terra’s implosion and subsequent liquidations accelerated panic across the board, severely damaging market confidence.

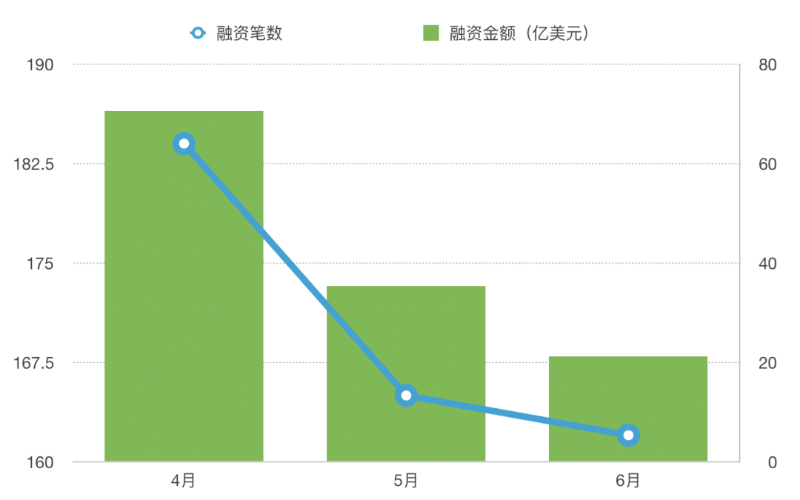

According to Odaily’s aggregate data, April 2022 saw 184 funding rounds totaling ~$7.05 billion. May recorded 165 rounds (~$3.54 billion), and June had 162 rounds (~$2.12 billion). Clearly, following Luna’s crash and negative institutional news, market sentiment remained depressed, capital erosion worsened, and both funding volume and value declined sharply.

Data source: Odaily

The cooling primary market directly impacts startups currently fundraising. Besides traditional VCs pausing talks, many Web3-dedicated funds are reducing per-deal allocations or demanding startups lower their valuations.

Compared to projects that have already secured partial or full funding, early-stage Web3 founders face even greater hurdles. When helping Web2 professionals transition into Web3 connect with investors, G3 found that without sufficient Web3-native experience or relevant resources, it's extremely difficult to raise funds—even with solid product and technical capabilities.

A project lead in the DID space within the G3 community shared that after six months refining their product, they began fundraising following a successful internal test in June. After engaging over ten VC firms, results were disappointing. They’ve since halted marketing activities and redirected spending primarily toward product development and R&D.

Some founders are now turning to vertical-focused events—industry conferences, hackathons, startup camps, accelerators—in hopes of gaining visibility, Web3-native endorsements, and grant funding.

A Web3 storage protocol lead said they participated in the June Polkadot Decoded conference—their first appearance at a major offline event—giving them rare direct access to industry players during the bear market.

Exchanges Expand Through Acquisitions Amid Downturn

Retail investors don't know whether institutions hold cash or tokens—and if tokens, whether they’re blue-chip or altcoins.

Thus, during bull markets, institutions leverage technical expertise, information asymmetry, and low entry costs, often using leverage to amplify capital advantages. They rotate aggressively between cash, major cryptocurrencies, trending altcoins, and even NFTs—generating massive volumes and volatility to extract profits.

But in bear markets, as retail activity and trading volumes dwindle, the market shifts to a zero-sum game among large holders. Institutions that over-leveraged during the bull run, accumulated large altcoin positions, or swapped cash for illiquid staked assets face severe risks—if they fail to exit in time, they risk blow-ups or liquidity crises.

Meanwhile, platforms that converted holdings into substantial cash reserves during the bull market can now begin investing and acquiring distressed, deeply discounted projects and firms—expanding their market share.

On July 1, Binance CEO CZ stated they currently hold significant cash reserves and are actively seeking to support struggling crypto companies, aiming to help those facing temporary liquidity crunches survive the cycle. They are currently negotiating acquisition deals with over 50 crypto firms.

"Currently, the biggest spenders in the market are still the major exchanges—they’re the main buyers in the bear market M&A landscape. Having accumulated substantial capital during the bull run and maintaining strong cash flow, they rarely engage in risky maneuvers that could backfire. While they may occasionally pay tuition in areas like reckless expansion or security lapses, they remain far safer than highly leveraged institutions," said 0xTodd.

Notably, some M&A activity also comes from DEXs (DeFi), such as Uniswap Labs recently acquiring NFT aggregator Genie.

Another major spender expanding aggressively is SBF of FTX. In April, FTX announced the acquisition of Japanese crypto exchange Liquid. More recently, FTX is set to acquire BlockFi at a variable price of up to $240 million. Reports also suggest FTX is open to acquiring battered crypto mining operations and continues pursuing acquisition opportunities with U.S. securities brokers to offer stock trading services to American customers.

Many foreign institutions, constrained by risk controls, are now struggling—objectively creating "bargain-hunting" expansion opportunities for dominant players like Binance and FTX. Alex Zuo, Investment VP at Cobo Ventures, noted: "Many U.S. (foreign) institutions aren’t as strong as we assume. They’re trying to use regulations and legal frameworks to retrace paths we’ve already proven unworkable—like ASIC lending or interbank borrowing. They focus heavily on compliance applications, license approvals, and attending Wall Street events, but neglect improving profitability and technical risk controls. Some even involve custodians misappropriating client funds—so recent crises were inevitable."

Final Thoughts: Timing the Bottom

Regarding when institutions should bottom-fish, how entrepreneurs can survive the bear market and fundraise, several investors offered insights.

Having lived through multiple cycles, Yang Linyuan, founder of Web3Vision, remains optimistic: bear markets offer the best window for primary market investment. Truly outstanding founders are forged through market trials, and quality assets become reasonably priced. At the bottom of the last bear market, few institutions competed for early high-quality projects—making them easier to invest in.

"There are promising follow-on projects we missed at seed or early stages. During mid-to-late bear markets, due to cash flow issues, they may loosen their stance on valuation in new funding rounds—I believe this presents excellent investment opportunities," said Iren, investment lead at Miji Jike. If favored projects reduce valuations during the bear market, they consider joining or increasing their stakes.

Iren also advises cash-strapped teams to endure this bear market at all costs. It would be tragic to collapse just before dawn—a fate that, based on historical patterns, affects no small number. Securing funding at a reduced valuation and surviving is already a win.

0xTodd agrees: "Most high-potential projects actually emerge from bear market bottoms. Historically, about 90% of projects fail during bear markets. For investors, we prefer lean teams capable of operating in 'low-power mode,' using raised funds wisely for solid development and execution—only then can they survive. For founders, simply enduring and staying alive means you've already outperformed 90% of your peers."

"Investing goes against human nature, so we never try to guess the bottom. Usually, when nobody cares anymore—that’s the bottom. The ideal left-side timing is nearly impossible to predict. I believe we need to wait for clear right-side indicators in the broader market before the second-best time to buy arrives," said 0xTodd.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News