Which Projects Can Survive Bull and Bear Markets? Three Types to Watch Out For

TechFlow Selected TechFlow Selected

Which Projects Can Survive Bull and Bear Markets? Three Types to Watch Out For

Warning signs to keep in mind when researching a project.

Written by: Ben Giove

Translated by: TechFlow intern

Bear markets are full of opportunities. As valuations compress and bull market bubbles burst, projects with strong fundamentals and professional teams capable of surviving the crypto winter will not only survive but thrive—offering investors a significant opportunity.

Even during the 2018–2019 bear market, a few standout projects delivered outsized returns after the major crash. For example, in the relatively sluggish market of 2019, Chainlink (LINK) and Synthetix (SNX) surged 486% and 2,924%, respectively.

Picking winners is extremely difficult, but investors can significantly improve their odds not only by focusing on high-quality projects but also by training themselves to identify what to avoid. Let’s examine some red flags to keep in mind when researching a project, so your bear market portfolio won’t hold too many surprises.

Red Flag #1: Excessive Supply

Tokenomics is about supply and demand. While no token can fully escape the relentless selling pressure brought by a bear market, differences in token allocation and supply schedules can help investors better understand where structural selling pressure might come from.

The most critical factor when examining a token’s supply dynamics is the percentage of its supply that is currently in circulation. Many tokens—especially in DeFi—launch with shallow depth or low circulating supply. This often leads to a significant discrepancy between a project’s market cap and its fully diluted valuation (FDV), as new tokens are typically pulled to unreasonable valuations shortly after launch due to retail investors competing for a small pool of tokens.

While this varies by token, those with low circulating supply—particularly if they have high valuations—are more likely to face sell-offs during a bear market as holders cash out to survive. Tokens with a higher proportion of supply already circulating in the public market may be better equipped to withstand bearish conditions.

Selling pressure from these low-circulation tokens typically comes from two sources:

● First is internal unlocks, as many tokens allocate a large portion of supply to team members and investors. There's usually a time buffer—some period between launch and the start of vesting schedules, followed by a gradual release over time.

Although it's uncertain whether insiders will immediately sell their tokens upon unlocking, these events do introduce selling pressure, especially since early investors may have acquired tokens at a cost basis far below the current price—even amid weak market conditions.

● Another uncertainty is that private funding round valuations are rarely disclosed, putting current and future token holders at an informational disadvantage.

Despite this information asymmetry, savvy investors can use tools like Dove Metrics, Unlocks Calendar, and Nansen to gather more insights into these rounds and monitor whether insiders are selling their holdings.

In addition to unlocks, many tokens also face structural selling pressure from miners. Even in this bear market, numerous protocols currently run active liquidity mining programs, incentivizing miners with their native tokens.

Moreover, many protocols have recently shifted toward inflationary ve-token models. These models increase emissions of the native token to incentivize liquidity across various pools.

Regardless of the distribution mechanism, as miners sell these tokens for profit, this inflation exerts downward pressure on price.

Selling pressure from unlocks and inflation increases the likelihood that a token will continue to depreciate throughout the bear market. But as we’ll see next, this selling pressure can also erode a protocol’s capital base, reducing its chances of survival through a long winter.

Red Flag #2: Treasury Concentrated in Native Token

Another sign that a project may struggle to survive a bear market is a lack of diversified funding.

According to DeepDAO data, DAO treasuries hold over $8.1 billion in liquid and vested assets. Of that, only $1.0 billion (12.3%) consists of dollar-pegged stablecoins such as USDC, USDT, DAI, FEI, and FRAX. An additional $391.8 million (4.8%) is held in crypto reserve assets like ETH.

This data reveals something important: it shows that many protocols are undercapitalized and lack the necessary funds to survive long-term in a bear market. The lack of diversification also confirms that many DAO treasuries are heavily concentrated in their own native tokens.

This creates a problem because it ties a protocol’s self-sustaining ability directly to the value of its own token—exactly what we’re seeing now.

Furthermore, it suggests that in order to pay contributors and cover other operating expenses, DAOs may be forced to sell their own tokens into increasingly illiquid markets at depressed prices. This not only exacerbates selling pressure on the token, further depleting treasury value, but could also spark internal conflict within the community, increasing friction with holders, damaging morale, and making life harder for all stakeholders.

A non-diversified treasury may force a protocol to seek alternative financing. For instance, to secure enough funds to survive, a DAO might be compelled to turn to over-the-counter (OTC) deals, selling locked tokens at a discount to VCs or institutions.

These deals are generally not in the best interest of the protocol, as they don’t represent the interests of token holders. While DAOs may soon gain access to more sophisticated financial tools—such as bond and debt issuance via protocols like Porter Finance and Debt DAO—this infrastructure is still in its infancy and introduces new risks and obligations that many protocols may not be equipped to handle.

Although centralized companies dedicated to protocol development (e.g., Uniswap Labs) may possess sufficient funding, investors and token holders cannot verify this, as their financials are almost never publicly disclosed.

It’s prudent for investors to examine the composition of these treasuries, ideally avoiding projects whose funding is overly allocated to their native token.

Red Flag #3: Poor Governance

Unfortunately, we are still in the early stages of Web3, and DAO governance is largely a mess. That said, investors should pay attention to particularly poor examples of governance as warning signs.

During bear markets, tensions rise, stakes are high, trust is scarce, and governance can make or break a project. Decisions made through governance—and how they are executed—can have massive implications for a protocol’s long-term health and legitimacy.

Since DAOs are still nascent, the industry has yet to reach consensus on governance and organizational structures. Combined with surging token-holder voting—which can easily lead to governance chaos and short-term value maximization—many DAOs fall into one of two extremes of decentralization.

● On one hand, some DAOs find themselves overly decentralized. While highly centralized power causes problems, a complete lack of hierarchy brings its own issues. Overly decentralized DAOs are extremely inefficient, unable to make fast, timely decisions. Additionally, these organizations may suffer from infighting and power struggles, leaving them unable to execute their roadmap.

● On the other hand, many DAOs are DINO: Decentralized in Name Only. Despite claiming to be DAOs, these organizations remain highly centralized due to several factors. For example, many DINO DAOs have token supplies heavily concentrated among insiders, with oversized allocations to investors and team members.

Often, these team members are the only entities capable of implementing proposals, allowing insiders of these "DAOs" to completely ignore or bypass their stated governance processes, staging "governance theater" to pursue their own agendas.

Just in the past week alone, we’ve seen several such examples.

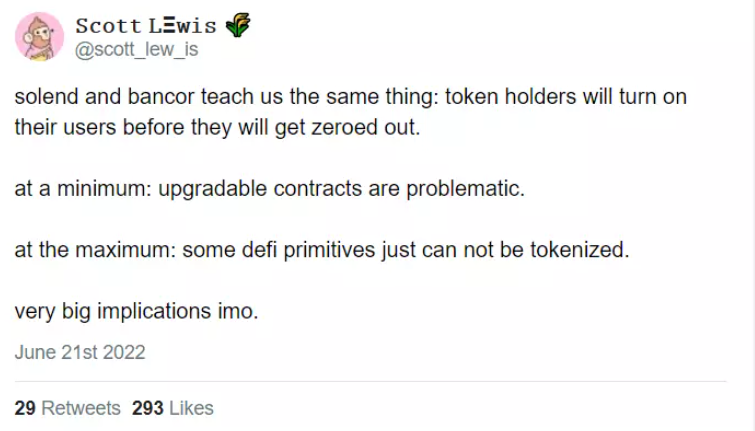

For instance, the decentralized exchange Bancor unilaterally decided to suspend impermanent loss protection, a key component of its value proposition for providing liquidity on the DEX—all without going through governance or notifying participants in advance.

Another example is Solend, a lending market that activated its on-chain voting system and then immediately proposed seizing funds from a whale whose large position faced liquidation risk. While the whale’s position posed a potential threat to platform stability, and the team later walked back the move, both Solend and Bancor may have severely damaged trust with users and the broader community.

Investors would be wise to avoid protocols that disregard governance and instead look for those actively working toward effective, balanced governance.

Conclusion

To find the next bear market winner, investors must not only know what to look for but also be able to recognize warning signs to avoid certain projects.

These signals include excessive token supply that faces continuous structural selling pressure from insiders and miners, DAOs with undiversified treasuries heavily weighted in their native token, and protocols with poor governance.

Bear markets are both crisis and opportunity—will you seize it?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News