Cobo Ventures: Looking at the Future of NFTFi from the Current Market

TechFlow Selected TechFlow Selected

Cobo Ventures: Looking at the Future of NFTFi from the Current Market

As NFTs become increasingly empowered, the applications of NFTFi should not be limited to the NFTs themselves. In the foreseeable future, NFTFi is highly likely to focus on extended use cases of empowerment and rights transfer, which is indeed the most exciting prospect.

This article is contributed by the Cobo Ventures team, authored by team members Alex Zuo, Ellaine Xu, Walon Lin, Caroline Li, and Yuwei Hou.

Cobo Ventures is the industry research and strategic investment division of Cobo, focusing on foundational Web3.0 infrastructure including public blockchains, cross-chain solutions, and scaling technologies. It also maintains a strong focus on application-layer sectors such as DeFi, NFTs, DAOs, and Social. Through deep research, Cobo Ventures aims to empower investments, incubation, and post-investment support, integrating upstream and downstream resources to build optimal strategic synergies and continuously inject new vitality into the industry.

Table of Contents

NFTFi Overview

-

Background

-

Market Size

-

Pain Points in the NFT Market

NFT Lending

-

P2P NFT Lending Protocols

-

P2Pool NFT Lending Protocols

NFT Liquidity Solutions

-

NFT Leasing Protocols

-

NFT Liquidity Pool Protocols

-

NFT Crowdfunding Protocols

NFT Aggregators

Special Pricing Mechanisms and Oracles for NFTs

-

Game Theory-Based NFT Pricing Models

-

Autonomous Computing Oracles for NFTs

NFT Derivatives

-

NFT Options Platforms

-

NFT Perpetual Contract Platforms

-

NFT Automated Market Makers

Conclusion

NFTFi Overview

Background

NFTs have become an indispensable chapter in the crypto world. Since the NFT Summer boom in 2021, Ethereum's largest NFT platform Opensea has reached a weekly trading volume in the billions of dollars, with over 300,000 unique wallets consistently active (Dune Analytics @hildobby, 2022).

However, due to their non-fungible and hard-to-price nature, NFTs suffer from low liquidity, leading to high capital thresholds and inefficient capital utilization. Beyond being forced to sell at lower prices during cash shortages or being unable to participate in blue-chip projects due to limited funds, NFT holders may also incur liquidity losses due to valuation difficulties. To address these issues, the market recently introduced the concept of NFTFi—leveraging financialization to enhance NFT liquidity, pricing, utility, and interoperability, aiming to improve user experience.

Market Size

Based on valuations of blue-chip NFTs, we can estimate the current size of the NFTFi sector.

Current value estimates of major blue-chip NFTs (using floor prices and assuming ETH at $2,000): BAYC ~$1.72 billion, Moonbirds ~$440 million, Azuki ~$237.4 million, CryptoPunks ~$953.2 million, totaling approximately $3.587 billion USD.

Land-based NFTs like The Sandbox, Arcade, and Decentraland were excluded due to clear rarity rankings that make floor price calculations inappropriate. Considering future growth potential, the total market cap of blue-chip NFTs could easily exceed $5 billion. Additionally, emerging projects in lending, leasing, liquidity, crowdfunding, and rights tokenization continue to emerge, making the overall value of the NFTFi space potentially limitless.

Pain Points in the NFT Market

-

Insufficient Liquidity

① High Entry Barriers

For ordinary collectors or consumers outside the ecosystem, current NFT marketplace entry barriers are too high. Even within the community, fragmented liquidity across different listing platforms remains an issue. Therefore, payment integration systems and NFT listing aggregation protocols represent important practical applications.

② Limited Trading Precision

Fungible tokens typically offer higher trading precision (e.g., 10^-18), but ERC721-formatted NFTs circulate only as whole units, creating liquidity thresholds. On one hand, requiring full purchases raises minimum transaction thresholds—sometimes hundreds of dollars—hindering NFT liquidity. On the other hand, market makers struggle to operate effectively without sufficient precision, especially given varying NFT rarities causing intra-series price spreads up to 10x, further impeding market-making and transaction experience.

③ Low Capital Utilization

Fungible tokens or equities can leverage mechanisms like collateralization, staking, and leverage to increase capital efficiency. However, the NFT space currently lacks similar tools. While BAYC has started exploring utility extensions via airdrops and whitelist allocations, most NFT investment returns still rely solely on capital gains from buying low and selling high. Widespread NFT derivatives remain absent, and investors often hesitate to enter or even exit the market due to fears of “selling too early” or mispricing assets, negatively impacting trading volume and frequency.

-

Flawed Pricing Mechanisms

① Difficulty Achieving Price Consensus

Unlike traditional securities pricing, NFTs’ uniqueness means their perceived value varies significantly among collectors and investors. This pricing ambiguity makes it harder for buyers and sellers to reach agreement during transactions, hindering improvements in liquidity and capital efficiency.

② Inadequate Price Discovery Mechanisms

Current NFT market price discovery methods—external price feeds and built-in oracles—fall short in timeliness, accuracy, and universality. Even when consensus pricing occurs on certain exchanges or auction houses, it’s difficult to propagate this data across broader markets or other platforms. Some exchanges may even experience temporary pricing failures due to insufficient liquidity or whale manipulation, affecting derivative applications. Thus, oracles and other price discovery mechanisms are critical NFT liquidity infrastructures—they not only help form price consensus but also enable more rational derivative operations, including constructing NFT liquidity pools and enabling scalable capital utilization.

Currently, ChainLink offers NFTBank.ai, a dedicated NFT oracle that captures floor prices from Opensea.

To address the above issues, this paper summarizes the following solutions and examines existing market cases:

-

Aggregators can solve high entry barriers. Currently, Genie and Gem are two major NFT marketplace aggregators, while wallet usage can be facilitated through intermediaries like Moonpay.

-

Low capital utilization can be addressed via lending and leasing. Current market examples include P2P lending protocol NFTfi.com, P2Pool lending protocol DROPS, and leasing protocol Doubles.

-

Precision issues can be solved through fractionalization. Projects like NFTx and Fractional exist today. From the demand side, secure crowdfunding platforms allow users to pool funds under multi-sig environments to collectively manage funded NFTs.

-

Ambiguous pricing and oracle-related issues require multi-layered design mechanisms and multiple data providers. This paper will focus on Banksea and Abacus.

-

Finally, regarding derivatives, this paper introduces current market attempts to improve capital efficiency, though due to immature oracle mechanisms, NFT derivatives remain in early stages.

NFT Lending

P2P NFT Lending Protocols

P2Peer refers to a lending method where lenders and borrowers directly agree on loan terms, allowing borrowers to use NFTs as collateral to obtain loans.

The benefit is customizable lending rules, but drawbacks include reliance on specialized lending knowledge and longer matching times due to manual pairing, limiting full liquidity release.

In principle, NFT assets are locked into the NFTFi smart contract until the borrower repays the loan. If the borrower fails to repay by maturity, the NFT asset transfers to the lender. Lenders can individually fund specific NFTs, setting repayment amounts (or interest rates) for borrowers to accept. This model aims to provide liquidity for high-value NFTs, but differing value assessments between parties may lead to prolonged decision-making.

NFTFi.com

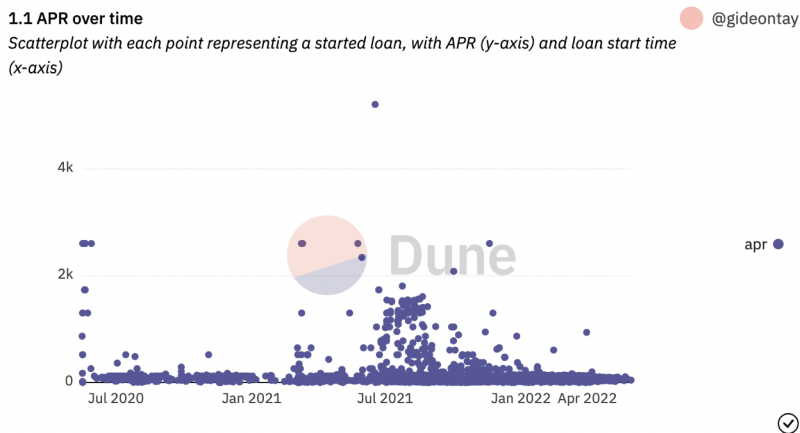

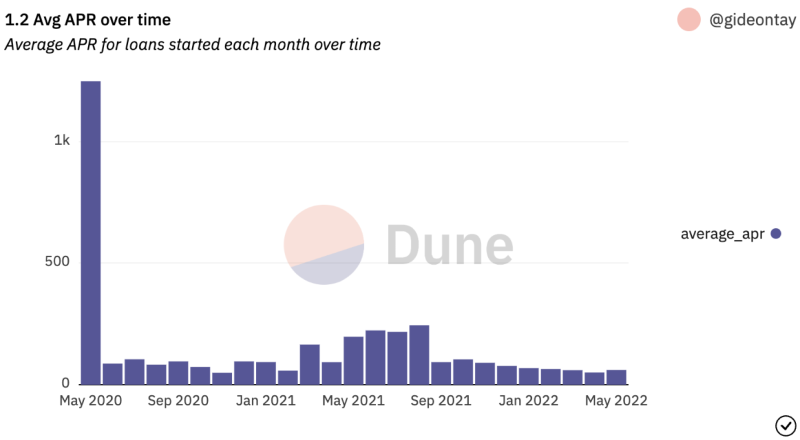

NFTFi.com is a mature auction-style P2P NFT lending platform where bidding, interest calculation, and timing are jointly determined by fund providers and NFT pledgers.

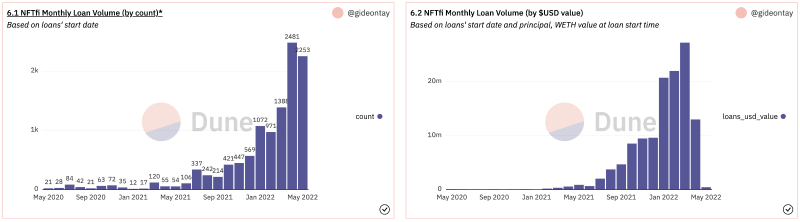

Source: NFTFi.com official website

NFTFi.com currently shows APR distribution ranging from ~30% to 110%, with average annualized yield around 60% in May 2022.

Source: Dune Analytics @gideontay

Source: Dune Analytics @gideontay

Monthly usage has grown steadily from over 20 transactions in May 2020 to approximately 2,253 (as of May 31, 2022), with transaction value exceeding $13 million—still less than 2% of blue-chip NFT market cap, but with a year-on-year growth rate of 300%.

Source: Dune Analytics @gideontay

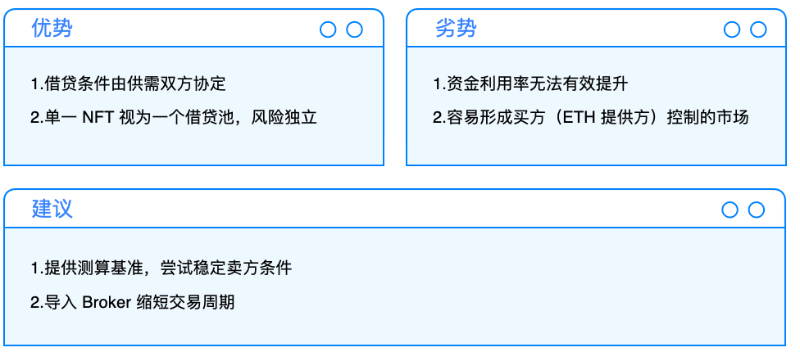

Advantages of P2P Model: Prices reflect equilibrium between supply and demand, and any NFT type can be listed without being affected by individual NFT price fluctuations.

Disadvantages of P2P Model: Lower NFT utilization due to long transaction cycles. The mutually agreed price may not reflect intrinsic NFT value, forcing cash-strapped NFT holders to sell at undervalued prices. This trade-off between liquidity and pricing shifts power toward buyers (ETH providers), creating an imbalanced market.

P2Pool NFT Lending Protocols

Another lending model is P2Pool. Analogous to DeFi protocols like AAVE and Compound, pricing typically relies on oracle feeds or time-weighted averages. Mechanically, lenders provide liquidity to the protocol, which allocates funds to borrowers using NFTs as collateral. This model usually depends on price oracles and algorithmic NFT valuation, thus only suitable for well-priced NFTs like CryptoPunks and BAYC, making permissionless pool creation difficult.

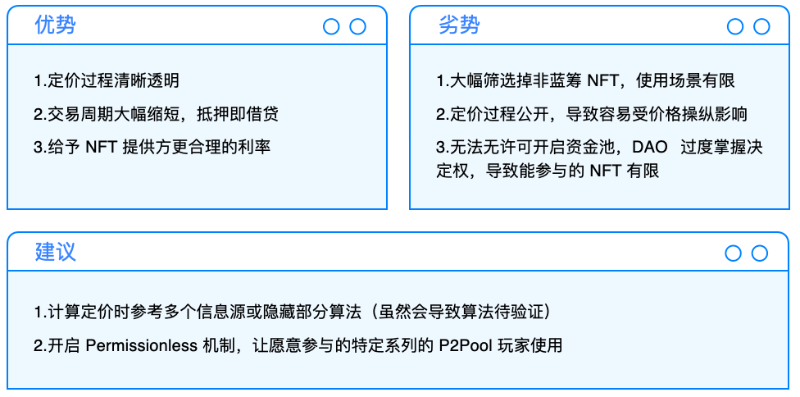

The advantage of P2Pool lies in significantly increased capital efficiency, offering more reasonable interest rates to NFT pledgers, and reducing pricing distortions caused by low-volume NFTs through series-based pooling.

However, P2Pool risks stem from largely transparent pricing models, making oracles critically important. Price manipulation (e.g., wash trading) or volatility could trigger liquidations. For instance, Azuki’s price fluctuated by about 10 ETH within days.

DROPS

DROPS' pricing model uses: 1) oracles, 2) time-weighting, 3) outlier removal, and leverages fractionalization (if available). However, this approach heavily filters out low-liquidity NFTs due to the need for extensive transaction data to eliminate noise, preventing illiquid collections from entering DROPS' calculation framework.

Pricing methodology (based on floor price):

1) Initial transaction screening: 25-block confirmation, one NFT sold, same Token ID not resold within 24 hours;

2) Remove outliers: After calculating floor prices from 100 transactions, exclude values below 5th percentile and above 95th percentile (e.g., if average floor price is 100E, exclude trades below 5E and above 950E);

3) Remove extreme possibilities: Exclude transaction prices beyond N standard deviations;

4) Price feed recorded every 4 hours;

5) If an index exists for the NFT series, it will be used as reference.

JPEG'd

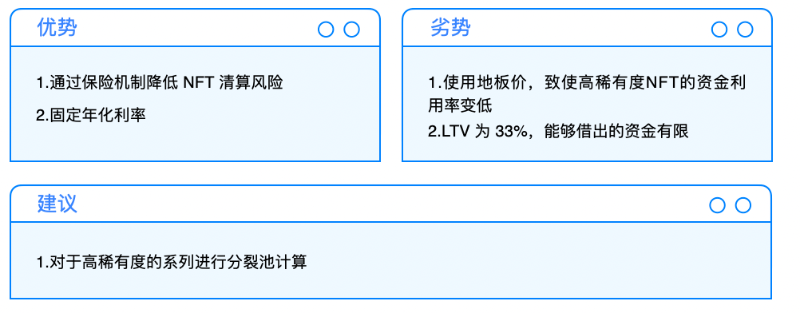

JPEG'd is an improved NFT P2Pool lending protocol. Initial borrowing rate is set at 2% annual interest plus a 0.5% withdrawal fee. Loan-to-Value (LTV) ratio is capped at 33%. For example: Alice pledges an NFT worth 10,000 PUSD and can borrow up to 10,000 × 32% = 3,200 PUSD. After deducting a 50 PUSD withdrawal fee, she receives 3,150 PUSD. When JPEG'd faces liquidation, users can use an early insurance mechanism to protect their NFTs. Alice must pay 1% as an insurance fund plus 25% of the debt value to the treasury to reclaim her NFT.

In terms of pricing, initially each APES is set at 2000 ETH (controllable by DAO), while other CryptoPunks prices are based on ChainLink-reported floor prices, defining the overall borrowing range. Currently, JPEG'd mainly supports CryptoPunks, relying purely on floor prices to reduce risk—keeping LTV at acceptable levels. JPEG'd currently holds NFTs valued at $8.46 million, comprising 73 NFTs.

Source: JPEG'd official website

This design limits capital efficiency improvement, with a 32% utilization ceiling. Although annual interest rates are lower than NFTFi.com, JPEG'd ultimately selects only blue-chip projects due to low pricing efficiency, increasing project safety but disadvantaging high-rarity NFT collectors.

Due to its liquidation mechanism, JPEG'd can purchase CryptoPunks into its treasury at 1/3 of market price and complete liquidation. On May 9, 2022—a highly volatile trading day—JPEG'd acquired 10 CryptoPunks at an average price of ~19 ETH, later selling them at 55 ETH (May 9, 2022 price), realizing a profit of 360 ETH.

Liquidation process:

NFT price drops sharply → Borrower’s LTV exceeds 33%, triggering liquidation → JPEG'd treasury buys back NFT at debt price (Floor Price × 1/3) → Finally, DAO disposes of treasury-held NFTs

BendDAO

BendDAO is also a non-custodial NFT lending pool. Once an NFT is pledged into the contract, users receive a corresponding BoundNFT receipt, retaining identical metadata so investors can still use BoundNFTs as PFPs.

Investors and users can pledge NFTs into lending pools to withdraw ETH. As of April 27, 2022, BendDAO was nearly the largest NFT collateral protocol holding BAYCs. Like most P2Pool protocols, only blue-chip NFTs are currently supported (BAYC, Azuki, CryptoPunks, MAYC, CloneX, Doodles), with expansion requiring voting by veBend holders.

Similar to JPEG'd, BendDAO features an insurance mechanism allowing pledgers to buy back collateral after liquidation. It provides a 48-hour grace period for debtors to redeem. If no redemption occurs, the NFT goes to auction.

BendDAO sources prices from Opensea floor prices (though DAO may change data sources later). Its biggest challenge is that liquidation prices may fall below debt prices, preventing liquidation, while when liquidation prices exceed debt prices, no one may want to buy back the NFT—leaving NFT scope restricted to blue-chip projects.

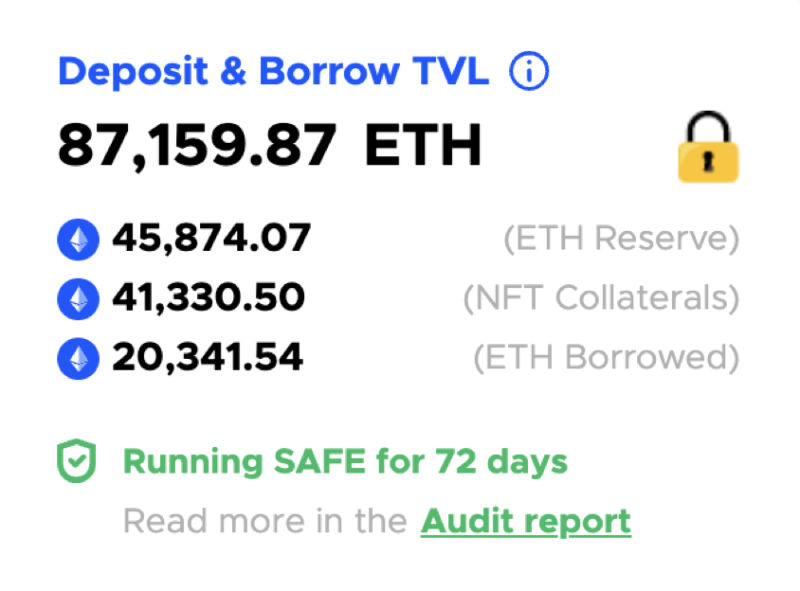

BendDAO’s total TVL is 87,159.87 ETH (~$174 million USD).

Source: BendDAO official website

Interest rates are voted by DAO for base rate and increment, then calculated based on NFT utilization. See chart below for reference.

Source: BendDAO Whitepaper

Current collateralization rate is 40%, liquidation threshold is 90%, indicating higher capital efficiency compared to JPEG'd.

Source: BendDAO Whitepaper

Summary

While P2Pool improves capital efficiency, it often leads to positions being liquidated and forced into auctions due to oracle flaws, pricing model inaccuracies, or extreme market moves. If auctions fail due to liquidity issues, problems arise in distributing liquidation proceeds. Based on current logic, P2Pool requires strict filtering of eligible NFTs for lending, limiting its audience.

In contrast, P2P models face NFT utilization challenges, but since terms are negotiated bilaterally, they resolve complex pricing and liquidation issues upfront. Despite buyer-market bias, P2P serves a near-universal audience, making it possibly more sustainable in the short term.

However, in the long run, as oracles and pricing models mature and gain precision, high-efficiency P2Pool models will likely dominate the market—the key variable being oracle maturity.

NFT Liquidity Solutions

NFT Leasing Protocols

Leasing protocols allow users to rent out NFTs to others or lease NFTs from others. This enables owners to earn income from idle NFTs without relinquishing ownership, while renters access NFT usage rights at lower costs, enhancing liquidity and capital efficiency.

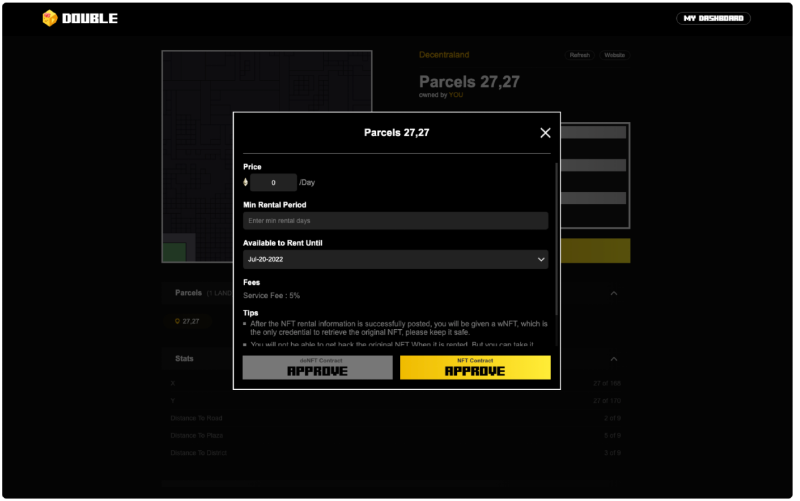

Double

Double is a leasing protocol attempting to separate usage rights from ownership. Unlike peers that lock NFTs in smart contracts with restricted usage, Double creates a doNFT type, pre-setting time and price at initiation, automatically destroying the doNFT upon expiry. This way, Double only unidirectionally locks the original NFT, minimizing restrictions on the doNFT borrower.

doNFTs feature multiple SDKs and APIs, along with non-transferable properties similar to POAP, enabling future integration into other game worlds and expanding circulation and usability across domains. Separating usage from ownership effectively addresses snapshot airdrop misjudgments, value overlap, and serves as vital GameFi infrastructure. With sustained SDK/API support, mapped NFT usage will better protect lessees’ rights. As of May 31, 98 NFTs have been onboarded.

Source: Double official website

NFT Liquidity Pool Protocols

Liquidity pools allow users to deposit their NFTs into a shared pool in exchange for n fungible tokens (vTokens). These vTokens can be traded on secondary markets, and interested parties can buy back equivalent vTokens to redeem any NFT from the pool. This groups NFTs of the same series together, allowing flexible redemption or pledging choices. Arbitrage opportunities arise when individual NFT values exceed the pool average—this is one method of price discovery. Liquidity pool trading offers faster execution for buyers seeking same-series NFTs, eliminating bidding or auction processes.

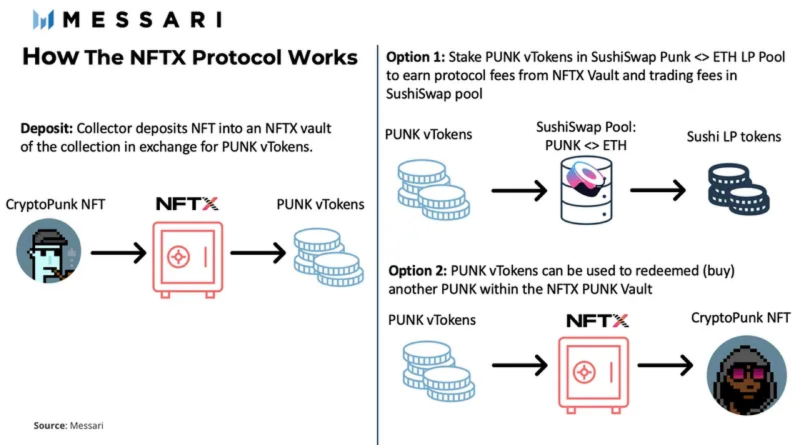

NFTX

NFTX focuses on floor-price NFTs, allowing users to deposit floor-tier NFTs into vaults and receive equivalent ERC20 vTokens, enabling partial investment in floor NFTs. For mid-to-high-tier NFTs of the same series, due to difficulty in valuation and equal vToken calculation, NFTX chooses to abandon this segment, focusing instead on directly benchmarkable NFT projects.

Unlike fractionalization models with governance conflicts, only those who purchase all fragments can redeem the underlying NFT. Currently, FloorDao employs OHM bonding mechanics to buy back NFTX’s ERC20 tokens into its treasury, creating its own ecosystem, providing index NFT space, and generating additional revenue for the NFTX treasury.

Source: Messari

Currently, NFTX achieves daily trading volumes of 143 ETH, with approximately $36 million TVL supporting protocol operations.

Source: Dune Analytics @nftx

Demand-side growth is rapid—up to ~1,100 NFTs minted into ERC20 vTokens in a single day, generating ~$1.2 million in fees within May.

Source: Dune Analytics @nftx

Overall, NFTX’s focus on floor-price minting encourages broad participation. Combined with FloorDao collaboration, sufficient vToken liquidity is created, forming a positive feedback loop.

NFT Crowdfunding Protocols

Crowdfunding protocols aim to pool capital and provide secure environments for NFT purchases, addressing the inability to split NFT ownership—enabling investors to diversify risk and enter the market with smaller capital.

Mesha

Mesha allows joint NFT ownership and enables proxy claiming of airdropped tokens or collective sale decisions, thereby boosting liquidity. It already integrates with Opensea, Looksrare, and gem.xyz. Additionally, Mesha offers chat and discussion features, combining community aspects to enable one-stop discussions for NFT collector teams. Most importantly, Mesha’s partnership with Moonpay enables in-app credit card payments, improving user experience.

Currently in early stages, users can earn XP tokens through tasks, exchangeable 1:1 for $MESHA in the future, and receive 50% fee discounts upon staking.

NFT Aggregators

Strictly speaking, aggregators don’t belong to NFTFi, but serve as crucial early-stage infrastructure that dramatically increases NFT liquidity and visibility—hence included here.

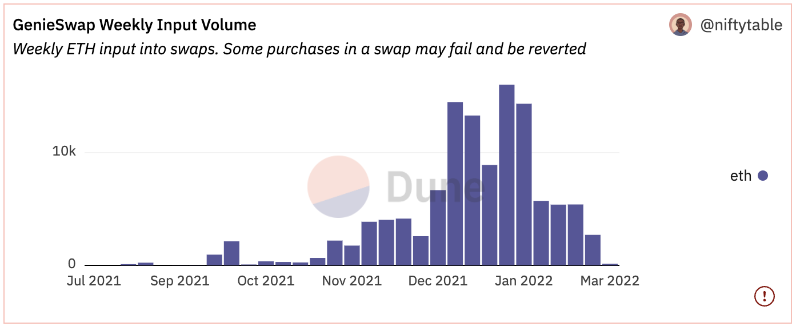

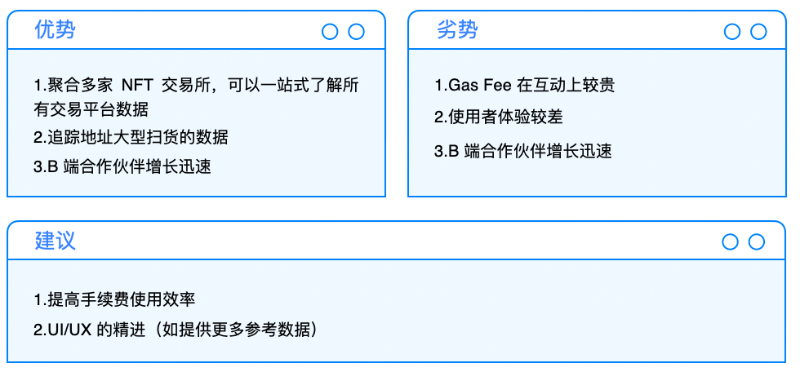

Genie

Genie emerged early in the NFT marketplace aggregation space, integrating OpenSea, Rarible, NFTX, NFT20, and others. It gained significant attention upon launch, accumulating ~$270 million in trading volume, with peak weekly users reaching ~3,600.

Source: Dune Analytics @niftytable

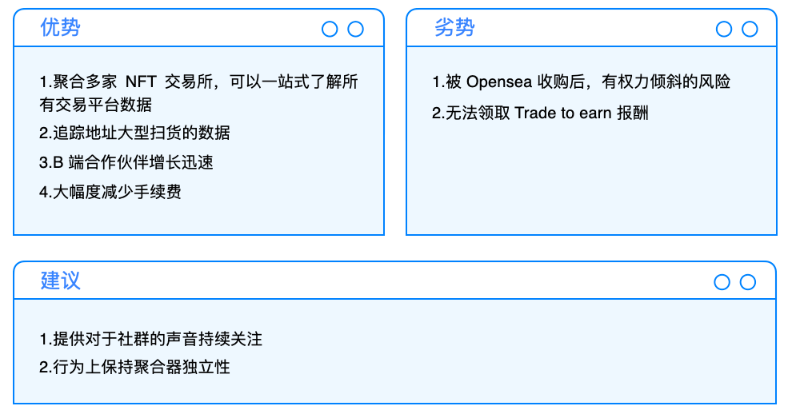

Gem.xyz

Over time, gas-efficient aggregator gem.xyz emerged. With significantly reduced gas fees and a more user-friendly UI, gem.xyz quickly eroded Genie’s first-mover advantage, achieving dominant leadership in the NFT aggregation race. Its daily usage is now nearly five times that of Genie (Dune Analytics @sohwak, 2022). Features like listing analytics and paying fees with any ERC20 token further boost user stickiness. Although Genie later partnered with Looksrare and others, users have already grown accustomed to gem.xyz.

In the NFT aggregation space, gem.xyz’s intuitive UI and substantial gas savings make it extremely difficult for Genie to catch up in user count and trading volume. This category has unified the fragmented NFT market, reducing search costs for NFT buyers.

Special Pricing Mechanisms and Oracles for NFTs

Game Theory-Based NFT Pricing Models

Abacus

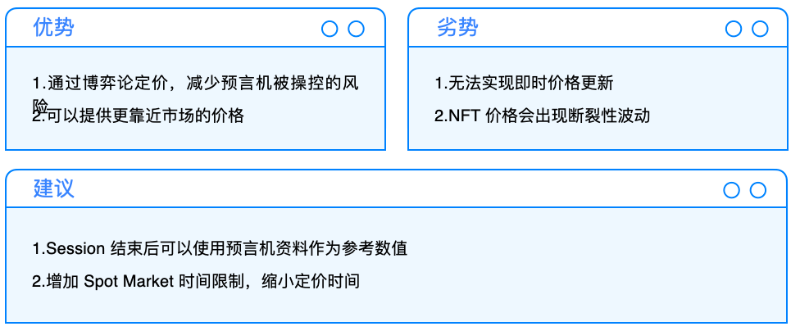

Abacus uses two pricing methods: first, peer-incentivized pricing; second, Spot Market pricing.

Peer-incentivized pricing requires users to pay a review fee (0.9%), incentivizing token stakers to discover value. Weighting is based on stake amount / minimum stake. Submitters whose final price falls within ±5% of the accepted price earn rewards. This incentive structure encourages broad participation in value capture.

Second, the Spot Market pricing model involves pool holders and traders. Pool holders initiate NFT pricing pools, setting initial price and quantity. For example, if Bob owns a CryptoPunk he values at 100 ETH and mints 1,000 xPunk tokens, each xPunk starts at 0.1 ETH, followed by a Dutch auction. The auction ends when the last xPunk sells, and the final sale price multiplied by total tokens represents the market-assessed value of Bob’s CryptoPunk. Closing the pool can occur via auction—if auction price exceeds pool price, the founder recovers principal and surplus ETH is distributed to traders; otherwise, the holder records a loss. Alternatively, the holder can exit and reclaim the NFT by paying 5% of the market anchor price to traders.

Under these dual mechanisms, traders are incentivized to push NFT prices toward liquid, fair valuations and engage in arbitrage via the AMM. Because traders don’t know whether the pool owner will close via auction or exit, they cannot easily manipulate downward pricing—otherwise, the owner would choose to exit and reclaim the NFT, reducing trader gains. This game-theoretic design, assuming sufficient trader participation, drives P2Pool prices toward market-consensus values.

Autonomous Computing Oracles for NFTs

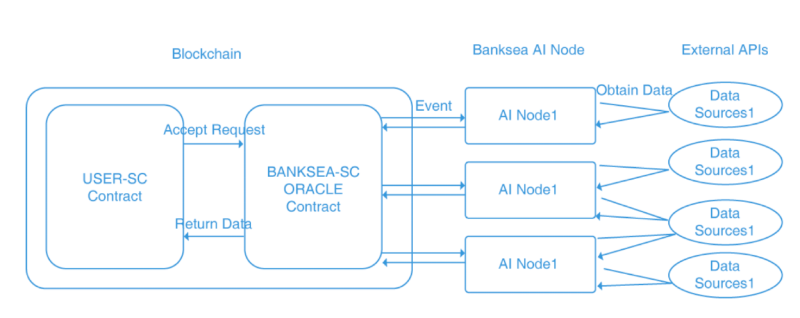

Banksea

Unlike typical lending platforms using ChainLink, Banksea operates its own data sources and built-in oracle system, producing a more suitable architecture for its native use cases.

Source: Banksea Whitepaper

Bank

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News