Howard Marks' Latest Memo: How to Escape Before the Market Crashes

TechFlow Selected TechFlow Selected

Howard Marks' Latest Memo: How to Escape Before the Market Crashes

The greatest investor behavior should be "what the wise begin, fools end."

Translation: Zhu Xueying, Zhao Ying, Bu Shuqing

For a century, the stock market has risen and fallen in cycles without ever stopping—countless cycles have streaked across the sky of history like brilliant meteors.

Why do cycles exist, and why do investors pour so much effort into the ongoing battle against market fluctuations? Because their investment psychology continually shapes market direction. As long as humans participate in investing, we will see these patterns repeat themselves over and over again.

In this latest memo titled "Bull Market Rhymes", Howard Marks, co-founder of Oaktree Capital, analyzes the regularities of bull market cycles and points out that investor behavior can signal which phase the market is currently in—and help exit before a market crash.

Driven by dreams of wealth, investors in a bull market frenzy often lack appropriate fear, and this surge of irrational exuberance signals that risk is near.

Marks emphasizes that investors must recognize when "bull market psychology" becomes dominant and maintain necessary caution. "Bull market psychology" is not a compliment—it implies complacency and high risk tolerance. Investors should feel concern, not encouragement:

It is risk aversion and fear of loss that keep markets safe and rational.

Marks notes that asset prices depend on fundamentals as well as how people perceive those fundamentals. High returns during bull markets make people more inclined to believe in new developments, low-probability events, and optimistic outcomes. When investors become fully convinced of the value of such things, they often conclude there’s “no such thing as an expensive stock.” At this point, new entrants flood in, keeping stock prices elevated. Caution, selectivity, and discipline disappear precisely when they are needed most.

Marks illustrates with today's market dynamics:

On Wall Street today, news of rate cuts pushes stocks higher. Then expectations of inflation from lower rates pull stocks down. Next, the realization that rate cuts could stimulate a depressed economy lifts stocks again. Finally, fears that overheating may lead to renewed rate hikes cause stocks to fall.

Marks openly states his belief in timeless investment maxims, making the following quote one of the greatest principles for investors: "What begins as wisdom ends as folly."

Full text of the memo:

Although I use many quotes and proverbs in my memos, only a few make it onto my personal favorites list. One of my all-time favorites is Mark Twain’s saying:

History doesn’t repeat itself, but it rhymes.

It is well documented that Mark Twain said the first four words in 1874, though there is no solid evidence he actually uttered the full sentence.

Over the years, others have expressed similar ideas. In 1965, psychoanalyst Theodor Reik wrote an article titled "Faraway," conveying the same sentiment. He added several lines of his own, which I believe offer the best formulation:

Cycles recur—up and down—but the process remains largely the same, with minimal variation. Some say history repeats itself, but that may not be accurate. History merely rhymes.

Past investment events don't replay exactly, but their core themes do reappear—especially those tied to investor behavior—which is precisely what I study.

Over the past two years, the kind of cycle Reik described has once again unfolded, drawing significant attention. What strikes me most is the recurrence of classic behavioral patterns, which will be the focus of this memo.

I should clarify upfront: this memo does not attempt to predict the market’s future direction. For example, bullish sentiment began when markets bottomed in March 2020. Since then, serious internal (inflation) and external (Russia-Ukraine conflict) economic problems have emerged, along with major adjustments. No one—including me—can know how these factors combined will shape the future.

My purpose in writing this memo is simply to place recent events in historical context and uncover underlying lessons. This is crucial because we must go back 22 years—to the bursting of the tech-media-telecom bubble in 2000—to witness the true beginning of a bull market and the end of the preceding bear market. Many readers started investing too late to have experienced that period firsthand.

You might ask: “What were market returns like before the 2008–2009 global financial crisis and the 2020 pandemic-driven market collapse?”

In my view, prior to both crises, markets rose gradually rather than parabolically. The increases weren’t driven by狂热 emotions, prices didn’t soar to absurd levels, and high valuations weren’t the cause of either crisis. The 2008–2009 crisis stemmed from the housing market and subprime mortgage securitization, while the 2020 crash was due to the pandemic and government-mandated economic shutdowns.

Regarding the term “true bull market,” my definition differs from Investopedia’s:

A sustained increase in asset or security prices over time.

Markets typically rise 20% after falling 20% in stocks.

The first definition is too bland, failing to capture the core investor sentiment during a bull market. The second offers false precision—bull markets shouldn’t be defined by percentage price changes. For me, it’s better described by how it *feels*, the underlying investor psychology, and resulting investment behaviors.

(I began investing before numeric standards for bull and bear markets were established, and I find them meaningless. Does it really matter whether the S&P 500 falls 19.9% or 20.1%? I prefer the old-fashioned definition of a bear market: nerve-racking.)

01 Overreach and Correction

My second book is Mastering the Market Cycle: Getting the Odds on Your Side. As is well known, I am both a student and believer in cycles. Over decades as an investor, I’ve lived through several important cycles (and been educated by them).

I believe understanding where we stand in the market cycle can provide clues about what comes next. But halfway through writing that book, I had a thought I’d never considered before: Why do cycles exist?

For instance, since its inception in 1957, the S&P 500 has delivered an average annual return slightly above 10%. Why can’t returns just be 10% every year? To add to a question I raised in my July 2004 memo “The Middle Way,” why did the index return between 8% and 12% only six times in that period, and why was it far outside that range 90% of the time?

After some reflection, I believe the answer lies in what I call "overreach and correction."

If you imagine the stock market as a machine, it would be reasonable to expect it to run steadily over time. However, I believe investor psychology significantly explains market volatility.

When investors turn aggressively bullish, they tend to reach the following conclusions:

First, everything will rise forever; second, no matter how high a price they pay for an asset, someone else will buy it at an even higher price (“greater fool” theory), because optimism runs so high:

Stock prices rise faster than corporate earnings, pushing valuations well above fair value (overvaluation).

Then the environment disappoints, revealing the foolishness of paying high prices, causing prices to fall back to fair value (correction), and then further below.

Falling prices fuel pessimism, driving prices far below intrinsic value (overselling).

Eventually bargain hunters push depressed prices back toward fair value (correction).

Overvaluation leads to above-average returns for a time, while overselling results in below-average returns. Other factors may be at play, but I believe “overreach and correction” explain most of it. During 2020–2021, we saw excessive market gains, and now we’re seeing the correction unfold.

02 Bull Market Psychology

In a bull market, favorable conditions lift stock prices and boost investor confidence. That confidence fuels aggressive actions, which further drive up prices, leading to even greater optimism and continued risk-taking.

This upward spiral is the essence of a bull market, and its momentum appears unstoppable.

At the onset of the pandemic, we witnessed a classic asset price collapse. The S&P 500 hit a record high of 3,386 on February 19, 2020, then plunged one-third in just 34 days, bottoming at 2,237 on March 23. But soon, multiple forces drove a strong rebound:

The Federal Reserve cut interest rates to near zero and, together with the Treasury, announced massive stimulus measures.

These actions convinced investors that authorities would stop at nothing to stabilize the economy.

Lower rates sharply reduced expected returns on investments, altering their relative appeal.

Together, these factors pressured investors to accept short-term risks.

Asset prices then rose: by late August, the S&P 500 had recouped all losses and surpassed its February peak.

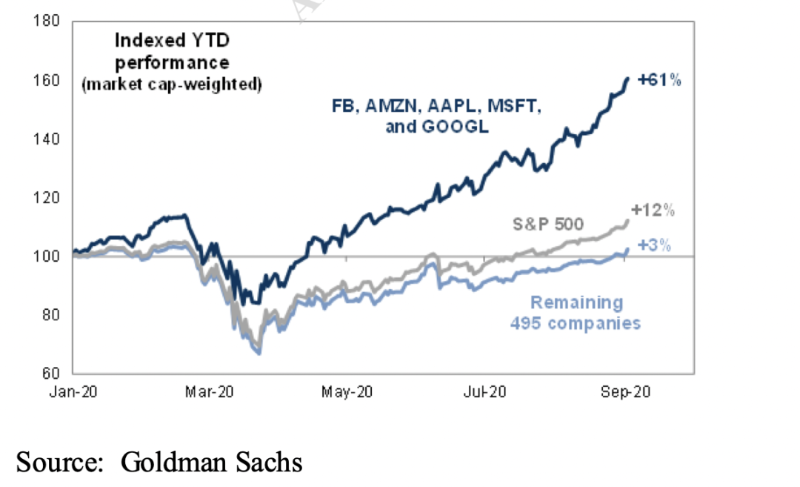

FAAMG (Facebook, Amazon, Apple, Microsoft, Google), software stocks, and other tech shares surged, propelling the broader market.

Finally, investors concluded that sustained stock market gains were likely—aligning with typical bull market thinking.

As in that last point, the hallmark of bull market psychology is that most investors see rising prices as a positive signal for the future, becoming increasingly optimistic. Only a few question whether this reflects overvaluation based on unrealistic expectations—unsustainable gains that will eventually reverse.

This brings to mind another favorite saying of mine—one I learned nearly 50 years ago—known as the "Three Stages of a Bull Market":

First stage: A few far-sighted individuals begin to bet on an emerging bull market;

Second stage: Most investors realize a bull market is underway;

Third stage: Everyone believes the bull market will last forever.

Interestingly, although the Fed’s actions quickly transformed the market from depressed lows in March 2020 to a boom by May, skepticism remained widespread. The most common question I heard was:

With such terrible conditions—pandemic raging and economic stagnation—how can stocks possibly rise?

Back then, optimists were hard to find. Many investors became what my late father-in-law called “handcuffed buyers”—they bought stocks not because they wanted to, but because they felt forced to, given negligible cash returns. Once stocks began rising, fear of missing out pushed them to chase higher prices.

Thus, the rally seemed driven more by the Fed’s manipulation of capital markets than by strong corporate performance or genuine investor optimism. It wasn’t until the end of 2020—after the S&P 500 had risen 67.9% from its March low and gained 16.3% for the year—that investor sentiment finally caught up with soaring prices.

Few bull markets truly progress through the first stage; even fewer experience the second. Many investors leapt directly from deep despair in late March to extreme optimism later on.

Today, this serves as a good reminder: while core themes of history do rhyme, expecting precise repetition is a big mistake.

03 Optimistic Rationales, Super Stocks, and Novelty

In frenzied bull markets, investors become hysterical. In extreme cases, their thoughts and behaviors detach from reality. This requires elements that excite the imagination while suppressing caution.

Thus, certain recurring elements appear in every bull market: new developments, inventions, and rationales for stock price increases.

By definition, bull markets feature prosperity, surging confidence, gullibility, and willingness to pay high prices for assets—all of which later prove excessive. Historical experience shows that keeping these tendencies in check is vital. Hence, the rational or emotional justifications fueling bull markets often stem from novelty—something unprecedented and untested by history.

History repeatedly shows painful consequences when markets exhibit bullish behavior, valuations soar, and investors blindly embrace novelty.

Everyone knows (or should know) that after parabolic rises, stocks typically fall 20%–50%. Yet, as I learned in high school English, the “willing suspension of disbelief” causes these behaviors to persist and recur.

Here’s another favorite quote of mine:

Financial euphoria is, and always has been, little known. Financial memory is short, leading to quick forgetting of past crises.

When similar or nearly identical situations reoccur—even within a few years—they are hailed by young, supremely confident newcomers as great discoveries in finance and economics. Few industries treat past experience with such irrelevance as finance.

To some extent, history becomes mere nostalgia—a refuge for those unable to appreciate the current spectacle.

—John Kenneth Galbraith, A Short History of Financial Euphoria, 1990

Over the past 30 years, I’ve shared this quote many times because I believe it perfectly summarizes key insights. But until now, I haven’t explained my interpretation of the described behavior.

I don’t think investors forget. Rather, on one side of the scale sits knowledge of history and prudent caution; on the other, the dream of wealth—and the latter always wins. Memory, caution, realism, and risk aversion only hinder the pursuit of riches. Thus, when a bull market begins, investors naturally lack appropriate concern.

Instead, they seek justifications for valuations exceeding historical norms. On October 11, 1987, Anise Wallace published an article in The New York Times titled “Why This Time Isn’t Different,” describing this phenomenon. Back then, people were optimistic and rationalizing unusually high prices. But Wallace argued this reasoning was flawed:

Seventy-four-year-old mutual fund manager John Templeton pointed out that the four most dangerous words in investing are “this time it’s different.” During market highs and lows, investors use this rationale to justify emotionally driven decisions.

In the coming year, many investors may repeat these four words to defend high prices. But they’d better adopt the attitude of “the check’s in the mail” toward bull markets—no matter what brokers or fund managers say, bull markets don’t last forever.

It took less than a year—just eight days—for the world to experience “Black Monday,” when the Dow Jones Industrial Average crashed 22.6% in a single day.

Another explanation for bull markets is investor belief in certain companies’ bright futures. This applied to the “Nifty Fifty” growth stocks in the late 1960s; semiconductor makers in the 1980s; and telecom, internet, and e-commerce firms in the late 1990s. Each development was believed to change the world, freeing investors’ imaginations and appetites from past business realities. And indeed, they did change the world. Yet, the high valuations once deemed justified did not endure.

In many bull markets, one or more groups become what I call “super stocks,” whose rapid ascent fuels growing optimism. Rising optimism pushes valuations higher—a hallmark of past market cycles. This positivity and elevated valuation spread to other securities (or all securities) via relative value comparisons and improved overall sentiment.

Looking back at 2020–2021, FAAMG topped the list of exciting companies, with unprecedented market dominance and scale. Their stellar 2020 performance captured investor attention and supported broad bullish trends.

By September 2020 (within six months), these stocks nearly doubled from March lows and rose 61% from年初. Notably, these five stocks carried heavy weight in the S&P 500, lifting the index overall—diverting attention from the poor performance of the other 495 stocks.

FAAMG’s extraordinary success created broad positive sentiment toward tech stocks. Demand for tech soared, and as in any market, strong demand stimulated supply. A notable barometer was IPO activity among unprofitable companies.

Before the late 1990s dot-com bubble, IPOs of unprofitable firms were rare, spiked during the bubble, then declined. In the 2020–2021 bull market, unprofitable IPOs surged again, fueled by investor appetite for tech scale-ups and biotech drug trial funding.

If promising companies power a bull market, novel innovations can amplify the rally. SPACs (special purpose acquisition companies) are a recent example. Investors provided blank checks to newly formed entities, redeemable with interest if no acquisition occurred within two years or if shareholders disapproved of a proposed deal.

This seemed like a “sure thing” (one of the most dangerous phrases in investing). SPAC numbers jumped from 10 in 2013 and 59 in 2019 to 248 in 2020 and 613 in 2021. Some delivered huge profits; others returned principal plus interest. But due to insufficient skepticism toward untested innovations and fueled by bull market psychology, too many SPACs were created—by both competent and incompetent sponsors—who earned large fees upon completing *any* acquisition.

Today, SPACs that completed acquisitions and exited since 2020 trade at an average of $5.25, down from their $10.00 offering price. This clearly shows that novelty isn’t as reliable as investors thought—they’ve again paid dearly for something they believed “couldn’t happen.”

SPAC supporters argue they’re just another path to going public and dismiss concerns about their role. My focus is on how readily investors embraced an unproven innovation during a hot market.

Another dynamic involving innovation deserves mention, showing how “novelty” contributed to the bull market:

Robinhood Markets began offering commission-free trading in stocks, ETFs, and cryptocurrencies years before the pandemic. Afterward, with casinos and sports betting shut down, it encouraged millions to enter the stock market.

Millions of employed individuals received generous fiscal subsidies, increasing disposable income during lockdowns. Social platforms like Reddit turned investing into a “stay-at-home social activity.”

As a result, legions of inexperienced retail investors flooded the market, many lacking basic investment knowledge.

Novices became excited by celebrity endorsements, declaring “stocks only go up.”

Consequently, many tech and “meme stocks” (retail抱团stocks) soared in price.

Another notable novelty was cryptocurrency. Bitcoin supporters cite its utility and limited supply relative to potential demand. Skeptics counter that Bitcoin lacks cash flows or intrinsic value, making fair pricing impossible. Regardless of who’s right, Bitcoin exhibits characteristics that benefit from bull markets:

Bitcoin is relatively new (though 14 years old, it only gained attention in the past five).

Its price surged dramatically, from $5,000 in 2020 to a peak of $68,000 in 2021.

Per Galbraith, it’s surely something previous generations “could not appreciate.”

In all these aspects, it fits Galbraith’s description of being “enthusiastically embraced by a new, young, and supremely confident generation as a great financial innovation.”

Now, Bitcoin is down over half from its 2021 peak, while thousands of other cryptocurrencies have fallen even more.

The remarkable performances of FAAMG, tech stocks, SPACs, meme stocks, and cryptocurrencies intensified the infatuation and amplified general investor optimism. It’s hard to imagine a full-blown bull market without something previously unseen or unheard of. Belief in the “new new thing” and “this time it’s different” are recurring hallmarks of bull markets.

04 The Race to the Bottom

Another recurring theme in cycles is the detrimental impact of bull market trends on the quality of investor decision-making. Simply put, when cool-headed rationality gives way to burning optimism:

Asset prices rise

Greed overtakes fear

Fear of loss turns into fear of missing out

Risk aversion and prudence fade away

Remember: it is risk aversion and fear of loss that keep markets safe and rational. These developments typically buoy markets while eroding caution and rational thinking, turning them into dangerous places.

In my 2007 memo “The Race to the Bottom,” I explained that when investors and capital providers have too much money and are eager to deploy it, bidding for securities and lending opportunities becomes overly aggressive. Intense competition drives down expected returns, increases risk, weakens safeguards, and reduces margin for error.

A cautious investor insists: “I require 8% interest and strong covenants.”

A competitor counters: “I’ll take 7% with weaker covenants.”

The least disciplined party, unwilling to miss out, says: “I’ll accept 6% with no covenants.”

This is the “race to the bottom”—why people say “the worst loans come in the best times.” This couldn’t happen when people are still hurting from recent losses and afraid of more pain. Following the Fed’s massive response to the global financial crisis came over a decade of record economic recovery and stock market gains, accompanied by:

A wave of IPOs from unprofitable companies

Record issuance of junior securities (high-risk CCC-rated bonds)

Heavy debt issuance by volatile sectors (tech and software)—industries typically avoided in cautious periods

Rising valuation multiples in M&A deals

Persistently low risk premiums

Favorable conditions also encourage greater leverage. Leverage magnifies both gains and losses, but in bull markets, investors believe gains are guaranteed and ignore the possibility of losses. Under these circumstances, few see reason not to borrow, as interest costs are negligible and borrowing boosts returns on successful investments.

But adding debt at high prices late in the cycle isn’t a recipe for success. When conditions deteriorate, leverage turns against you. Investment banks issuing debt near market peaks often get trapped. Debt lingering on bank balance sheets often acts as the “canary in the coal mine,” signaling danger ahead.

Since I believe in timeless investment maxims, it’s fitting here to quote what I consider the greatest principle of investor behavior: “What begins as wisdom ends as folly.” Those who bought stocks in the first stage of a bull market, when widespread pessimism (like during the 2008–09 global financial crisis or early 2020 pandemic) kept prices low, could earn rich returns with minimal risk—the main prerequisites being capital and courage.

But as the bull market heats up, attractive returns fuel investor optimism, and the traits rewarded become desire, credulity, and risk-taking. In the third stage, new entrants flood in, keeping stock prices elevated. Caution, selectivity, and discipline vanish precisely when they’re needed most.

Notably, investors who gain confidence and reward for risk-taking often stop differentiating among investment opportunities. They not only believe certain “new things” are bound to succeed, but eventually conclude the entire field is promising, making differentiation unnecessary.

For these reasons, “bull market psychology” is not a compliment. It signifies unguarded behavior and high risk tolerance. Investors should feel concern, not encouragement. As Buffett said, “Be fearful when others are greedy, and greedy when others are fearful.” Investors must recognize when bull market psychology dominates and remain appropriately cautious.

05 The Pendulum Effect

Bull markets don’t emerge from nothing. Winners in each bull market succeed for simple reasons grounded in reality. However, as I noted, bull markets exaggerate stock values, pushing prices to dangerously high levels—and upward swings don’t last forever.

In my January 2016 memo “On the Couch,” I wrote: “In the real world, things usually oscillate between ‘pretty good’ and ‘not too hot.’ But in investing, expectations swing between ‘hope’ and ‘despair.’” Exaggeration is a key feature of investor behavior. During bull markets, investors believe difficult, improbable, and unprecedented things are certain to work.

But in less favorable times, positive economic news and “beat-and-raise” quarters fail to trigger buying, and rising prices no longer make underexposed investors regret their positions. We see people quickly abandon suspended disbelief, turning negative fast.

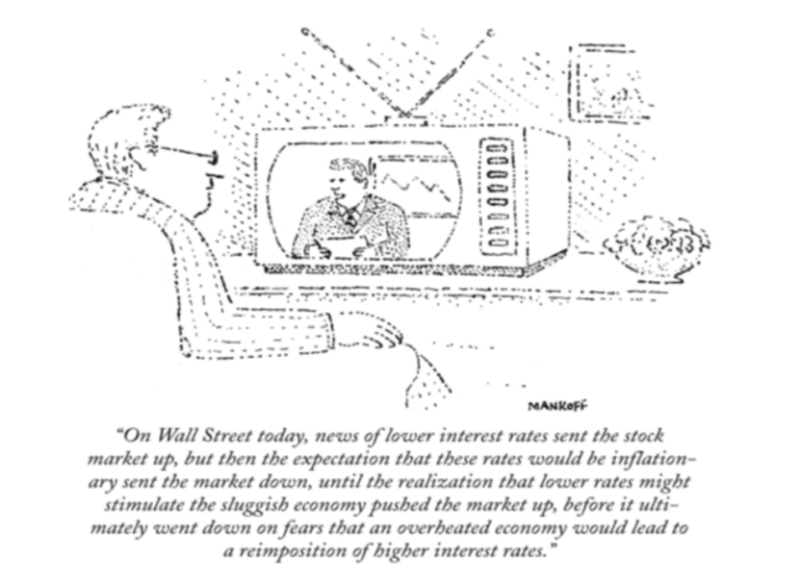

Investors can interpret almost any news positively or negatively depending on framing and mood—this is key. (The cartoon below, one of my longtime favorites, was published decades ago—note the antennas and TV cabinet depth—but clearly, the caption speaks directly to this moment.)

“On Wall Street today, news of rate cuts lifts stocks, but then expectations of inflation from lower rates push stocks down. Next, realizing rate cuts could stimulate a depressed economy lifts stocks again. Finally, fears that overheating may lead to renewed rate hikes cause stocks to fall.”

Reversing this narrative reveals the earlier-mentioned shift “from hope to despair.” While bullish arguments have merit, when things go well, investors treat them as certainties. But when flaws emerge, they deem the entire thesis wrong.

In happier times (a year ago), tech bulls said: “You must buy growth stocks—earnings are likely to grow for decades.” Now, after a sharp decline, we hear: “Investing based on future potential is too risky. You must hold value stocks—you can verify their current worth, and they’re reasonably priced.”

Likewise, during booms, investors in unprofitable IPOs said: “There’s nothing wrong with reporting losses—spending to scale makes sense.” Now, many say: “Who invests in unprofitable companies? They just burn cash.”

Those who haven’t watched markets long might think asset prices depend solely on fundamentals, but that’s false. Asset prices depend on fundamentals *and* how people perceive them. Therefore, price changes reflect changes in fundamentals *and/or* changes in perception.

Fundamentals are theoretically subject to “analysis,” maybe even forecasting. But perceptions are subjective, immune to analysis or prediction, and change faster and more violently.

Some sayings capture this idea:

Balloons deflate faster than they inflate.

Things take longer to happen than you think, but when they do, they happen faster than you imagine.

On the latter point, from experience, we often see positive or negative fundamentals accumulate over time with no price reaction. Then, at a tipping point—fundamental or psychological—everything suddenly reflects in prices, sometimes excessively.

06 Then What Happens?

Bull markets don’t lift all sectors equally. As discussed, optimism concentrates on certain stocks—like “novelties” or “super stocks.” These rise the most, symbolize the bull market, and attract further buying. Media attention prolongs the cycle. From 2020–2021, FAAMG and other tech stocks exemplified this.

It’s obvious, but worth stating: investors holding large positions in leading bull market stocks performed exceptionally well. Some fund managers, smart or lucky enough to focus on these stocks, achieved top returns amid prevailing optimism and graced newspaper and cable TV headlines. In the past, I’ve said our industry is full of people famous for consecutive correct calls. For those who increased exposure to leading sectors, fame may double.

Yet, stocks that rise most in up years often fall hardest in down years. Relevant real-world sayings apply: “Success has many fathers, failure is an orphan,” “What goes up must come down,” and “The higher they climb, the harder they fall.”

A tech fund rose 157% in 2020, going from obscurity to fame. But it fell 23

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News