a16z: 30% of Fortune 500 companies have already paid for AI—code generation and customer service are the first use cases to go live.

TechFlow Selected TechFlow Selected

a16z: 30% of Fortune 500 companies have already paid for AI—code generation and customer service are the first use cases to go live.

This 23,928-word report, based on internal data, reveals which AI use cases genuinely deliver value—and which remain mere conceptual hype.

Author: a16z

Translation & Compilation: TechFlow

TechFlow Intro: MIT claims that 95% of enterprise generative AI pilots fail to convert—but a16z counters this assertion directly with first-party data from its portfolio companies. 29% of Fortune 500 and 19% of Global 2000 companies are already paying customers of leading AI startups; programming tools boost top engineers’ productivity by 10–20x. This 23,928-word report—grounded in internal data—reveals which AI use cases truly deliver value, and which remain conceptual hype.

There is much speculation about how far AI has progressed within large enterprises—but most existing information consists only of self-reported AI usage or surveys capturing qualitative buyer sentiment rather than hard data. Moreover, the few existing studies asserting poor AI performance in enterprises—including MIT’s widely cited claim that 95% of generative AI pilots fail to convert—are largely anecdotal.

Based on our internal data and conversations with enterprise executives, we find this statistic implausible. We have closely tracked where AI adoption is highest and where ROI is clearest—and compiled hard data on what actually works in enterprise AI.

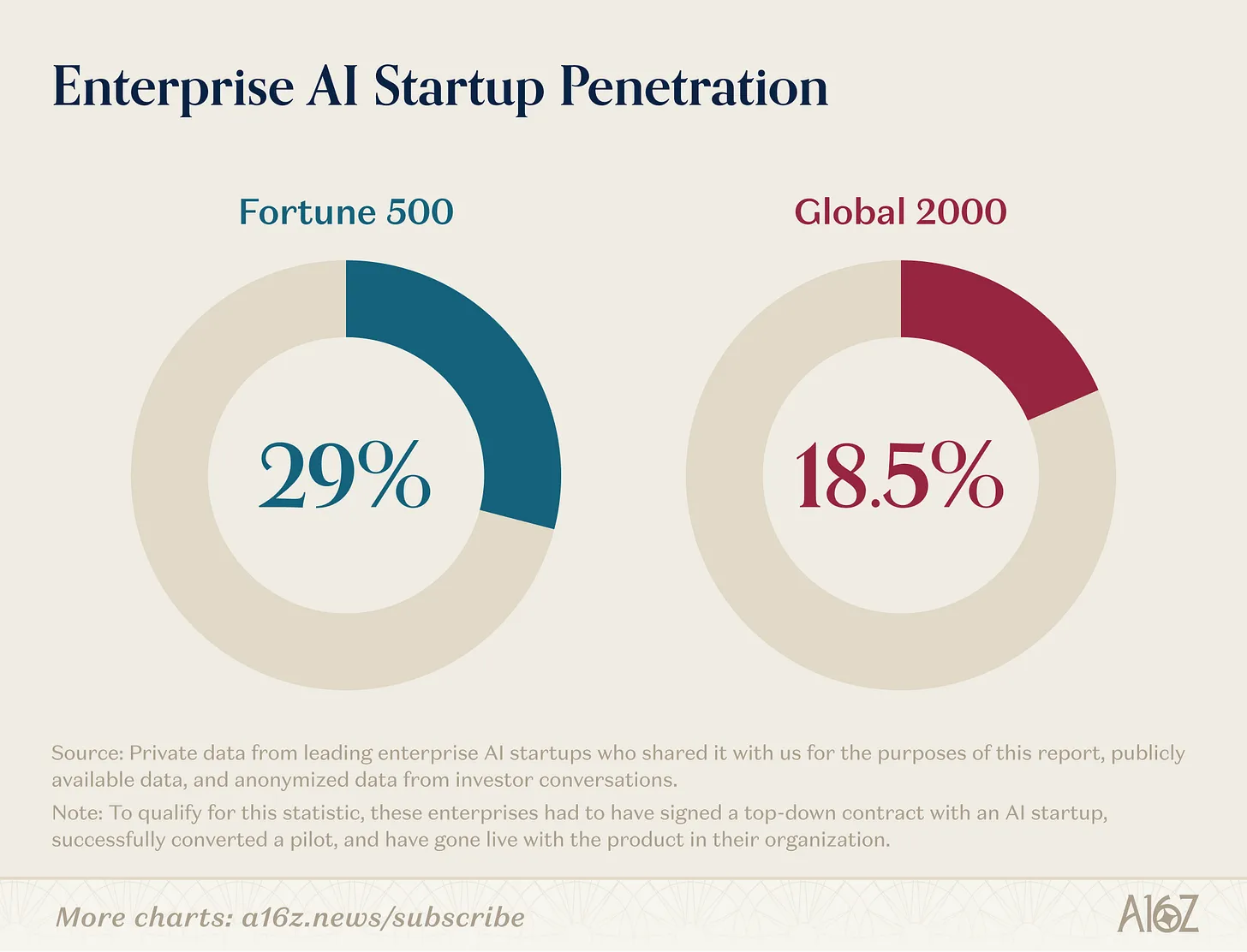

AI Penetration in Enterprises

According to our analysis, 29% of Fortune 500 companies and approximately 19% of Global 2000 companies are active, paying customers of leading AI startups.

To qualify for this statistic, these enterprises must have signed top-down contracts with AI startups, successfully converted pilots into production deployments, and launched the products across their organizations.

Achieving this level of penetration in such a short time is remarkable—Fortune 500 companies are not historically known as early technology adopters. Historically, many startups had to first sell to other startups to gain early traction; it often took years before they secured their first enterprise contract—and even more time and revenue before landing Fortune 500–scale customers.

AI has upended this norm. OpenAI launched ChatGPT in November 2022, instantly demonstrating AI’s potential to both consumers and enterprises. This triggered an unprecedented surge of interest in AI—one no prior generation of technology has ever sparked—making large enterprises more willing than ever to bet on new products earlier. The result: just over three years later, nearly one-third of Fortune 500 and one-fifth of Global 2000 companies have real, production-grade enterprise AI deployments.

What Works in Enterprise AI

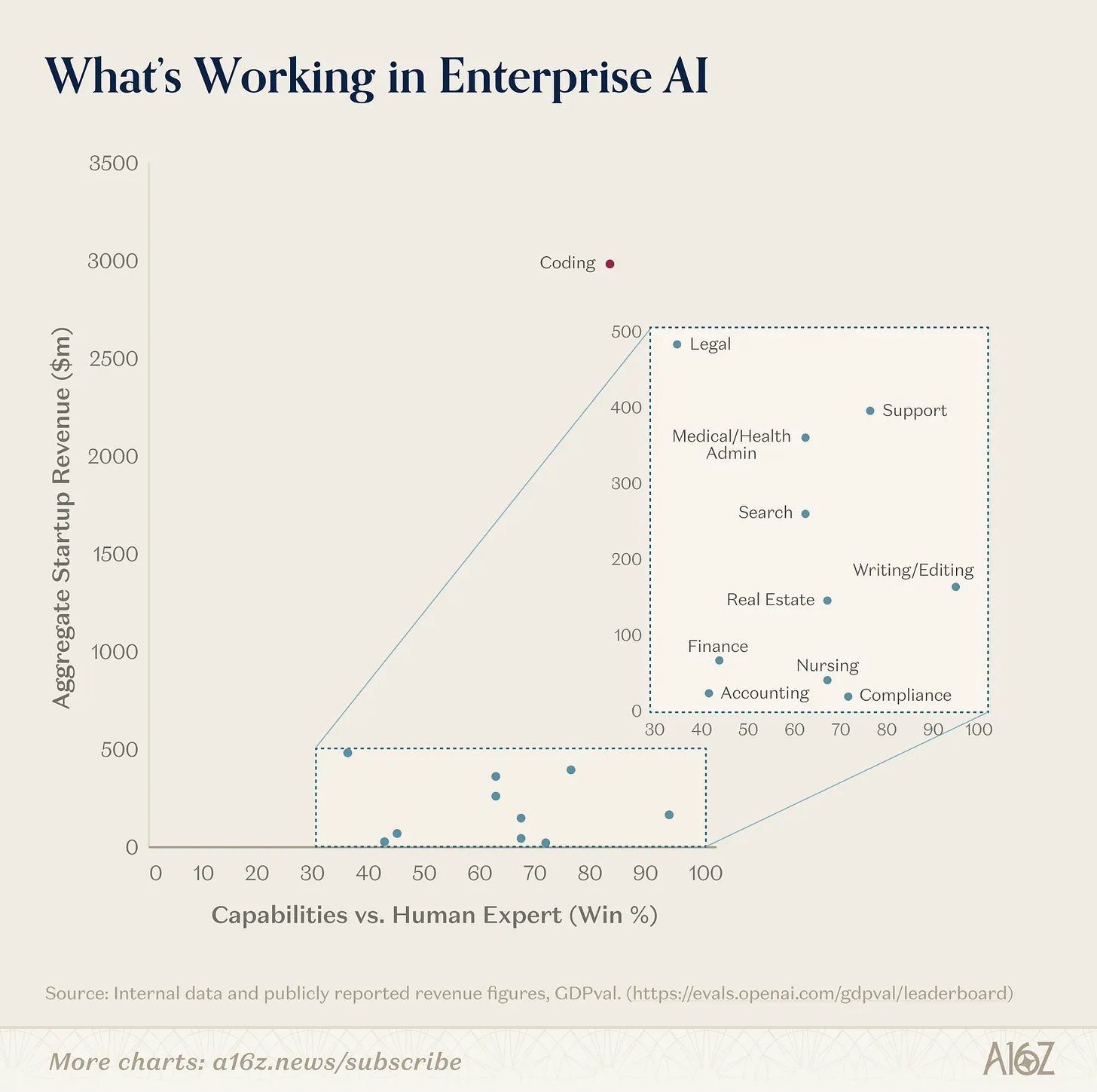

Where is adoption happening fastest—and how does it map to what models are inherently better at doing?

We find the most telling analytical approach is to overlay revenue momentum across use cases onto models’ theoretical capabilities—as defined by GDPval, a well-known OpenAI benchmark evaluating model performance on economically valuable real-world tasks. For us, these two dimensions collectively capture both how capable models can be—and how much value they demonstrably deliver today. That makes them highly informative about where AI adoption stands today, where it may go next—and where adoption remains stalled despite advancing model capabilities.

Where Does Enterprise AI Deliver the Most Value Today?

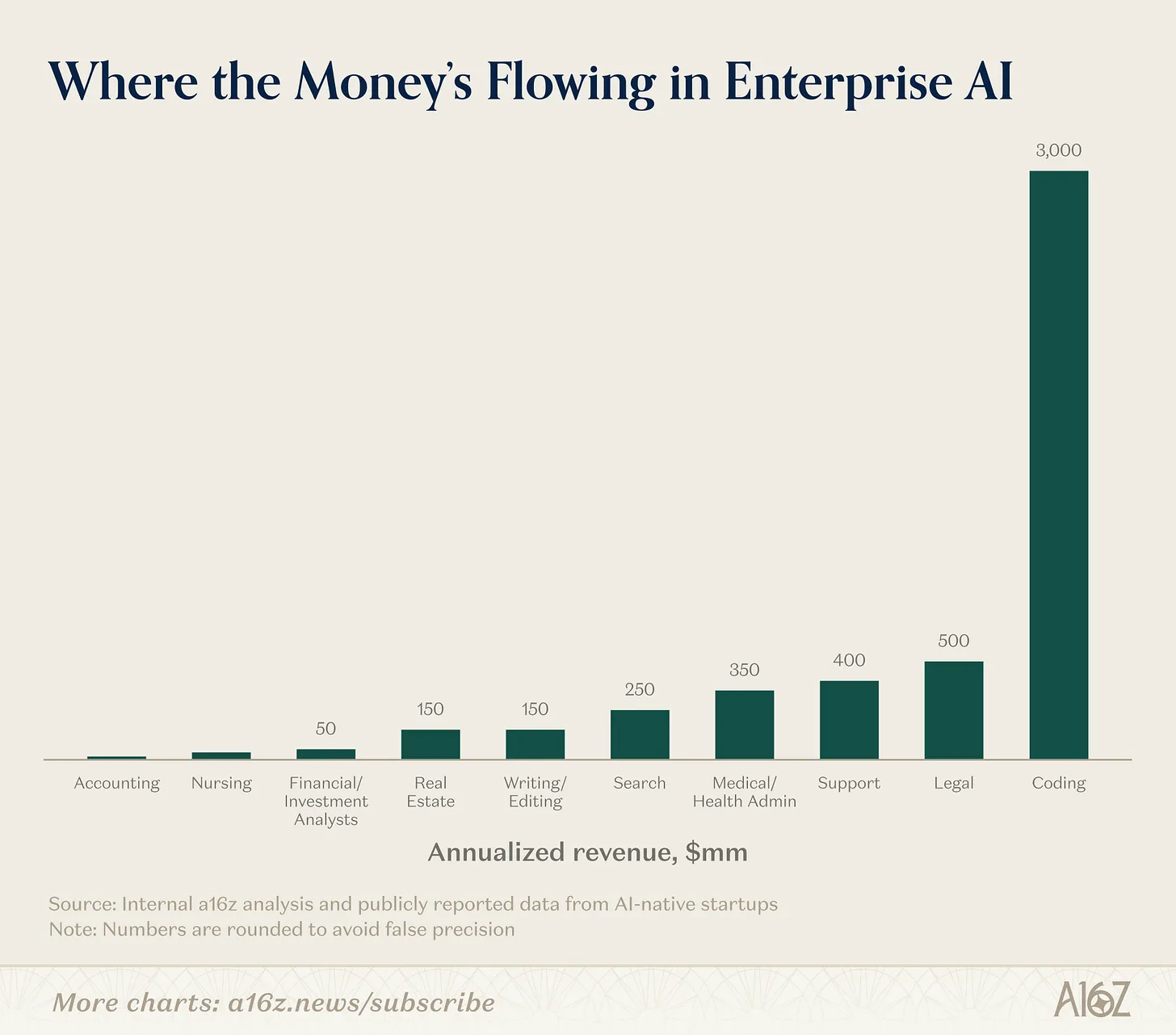

In terms of revenue momentum, enterprise AI adoption is led by a distinct set of use cases and industries. Programming, support, and search dominate so far (with programming standing out as an order-of-magnitude outlier), while technology, legal, and healthcare sectors are the most eager adopters.

Programming: Programming is the dominant AI use case—by nearly an order of magnitude. This is evident in explosive growth reported by companies like Cursor and hyper-fast adoption of tools like Claude Code and Codex. These growth rates have exceeded even the most optimistic forecasts—and to date, the vast majority of Fortune 500/Global 2000 AI tool adoption occurs in coding.

In many ways, programming represents AI’s ideal use case—both technically and commercially. Code is data-rich, meaning high-quality code is abundant online for model training. It is text-based, making it easy for models to parse. It is precise and unambiguous, with strict syntax and predictable outcomes. Crucially, it is verifiable: anyone can run it and immediately know whether it works—creating tight feedback loops for model learning and improvement.

Commercially, it’s also a strong fit. Our portfolio companies consistently report that AI coding tools increase the productivity of their best engineers by 10–20x. Since hiring engineers is difficult and expensive, any productivity uplift delivers clear ROI—creating massive incentive for adoption. Engineers are also often early adopters of best-in-class tools, because programming is a relatively solitary task compared to most enterprise work—making it easier for them to independently identify and adopt superior tools without being slowed down by the coordination overhead and bureaucracy that burden many other enterprise functions.

Moreover, programming tools need not complete tasks end-to-end at 100% accuracy to deliver value—any acceleration (e.g., bug detection, boilerplate generation) still saves time and proves useful. Because programming involves tight human-in-the-loop workflows, developers still supervise the development process today; these tools accelerate output while leaving ample room for human review, editing, and iteration. This both increases enterprise confidence and smooths the adoption path.

Programming capability is improving exponentially—with every major lab explicitly prioritizing “winning code” as a core use case. This has enormous implications. Code underpins all other applications—it is the foundational building block of all software—so AI’s acceleration of coding should compound across every other domain. Lowering the barrier to building in those domains unlocks new opportunities to solve problems with AI—but the same accessibility makes building durable competitive advantage for startups more critical than ever.

Support: Support sits at the opposite end of the spectrum from programming. While software engineering typically receives the most investment and attention within organizations, support is often overlooked. Work in support organizations tends to be back-office, entry-level, and frequently outsourced to offshore providers or business process outsourcing (BPO) firms—because companies perceive managing it internally as too cumbersome and complex.

AI has proven exceptionally effective at managing this work—for several reasons. First, most support interactions are time-bound and have constrained intent (e.g., issuing a refund), giving agents clearly defined problems to solve. Support is also one of the few functions where tasks involved are explicitly codified. Support teams are large and highly turnover-prone, requiring rapid, standardized onboarding of new representatives. To achieve this, they rely on clearly articulated standard operating procedures (SOPs) guiding each representative’s actions. These SOPs create explicit rules and guidelines that AI agents can readily mimic—setting support apart from most other enterprise functions, which tend to be longer-duration, less clearly defined, and involve more stakeholders beyond customer and agent.

Support is also one of the enterprise functions where ROI is clearest. Support operates on quantifiable metrics: tickets resolved, customer CSAT (satisfaction) scores, and resolution rates. Any A/B test comparing the status quo to AI agents yields favorable results for AI: it resolves more tickets, improves resolution rates, and lifts customer satisfaction—all at lower cost. Since most support is already outsourced to BPOs, adopting AI solutions requires minimal change management—making adoption smoother.

Support also doesn’t require 100% accuracy to be useful—it has a natural escalation path to humans (e.g., “I’m escalating you to a manager”). This allows sales cycles to move faster and makes piloting AI support agents relatively low-risk; in the worst case, 100% of cases simply escalate to humans for resolution.

Finally, support is inherently transactional. Customers don’t care who—or what—is on the other end, meaning support doesn’t require the interpersonal qualities that AI struggles to replicate. These characteristics explain why companies like Decagon and Sierra are growing so rapidly—and why vertical-specific support players like Salient and HappyRobot are flourishing.

Search: The final horizontal category with clear enterprise market pull is search. ChatGPT’s primary use case is itself search—so search’s impact may be deeply embedded in ChatGPT’s revenue and usage metrics, possibly significantly underestimated here.

AI search is so broad a category that it has spawned numerous independent, large-scale startups. One of the top pain points inside many enterprises is enabling employees to easily locate and extract relevant information across disparate internal systems. Glean has thrived as the leading startup provider for this use case. Many large industries also operate on highly specific internal and external information—companies like Harvey (originally focused on legal search) and OpenEvidence (originally focused on medical search) have flourished by building core products around this exact need.

Industries

Technology: The most common industry adopting AI so far is technology. ChatGPT itself reports that 27% of its commercial users come from tech—and many early customers of companies like Cursor, Decagon, and Glean are tech firms. Given that tech is almost always an early adopter—and the very industry that catalyzed the AI wave—this is entirely unsurprising.

More surprising is that markets historically not considered early adopters have proven highly eager this time.

Legal: Legal is surprisingly among the earliest industries embracing AI. Historically viewed as a difficult software market—characterized by long sales cycles and buyers less fluent in technology—legal has become receptive due to AI’s unique value proposition.

This is because traditional enterprise software delivered limited value to lawyers: static workflow tools failed to accelerate the unstructured, nuanced work lawyers actually do. But AI clarifies technology’s value proposition for lawyers. AI excels at parsing dense text, reasoning over large volumes of text, and summarizing or drafting responses—all core activities for lawyers. AI now commonly acts as a co-pilot to boost individual lawyer productivity—but it’s beginning to expand beyond that: in some cases, it’s generating revenue by enabling law firms to handle more cases (as with Eve, a plaintiff-side firm).

The results are striking. Harvey reported ~$200M in annual recurring revenue (ARR) within three years of founding; companies like Eve now serve over 450 clients and reached a $1B valuation this fall.

Healthcare: Healthcare is another market responding to AI in ways traditional software never could. Companies like Abridge, Ambience Healthcare, OpenEvidence, and Tennr are experiencing rapid revenue growth based on discrete use cases—such as clinical note-taking, medical search, or back-office automation of the Byzantine rules governing how healthcare is delivered and reimbursed.

Healthcare has historically been a slow-adopter of software because: 1) high-skill, complex work maps poorly to problems addressable by traditional workflow software; and 2) the dominance of EHR systems like Epic squeezes out new software vendors. With AI, however, companies can target discrete manual labor—replacing administrative roles (e.g., medical scribes) or augmenting higher-value work doctors perform—bypassing legacy system constraints. This work is sufficiently distinct that it doesn’t require ripping and replacing EHRs, allowing these companies to scale quickly without displacing incumbent software vendors.

Notes on the Analysis

These estimates represent our best judgment. They may underestimate revenue generated in each category—and overestimate model capabilities.

We may underestimate revenue because:

• Revenue analysis focuses solely on departments and use cases mature enough to sustain large, independent enterprise AI businesses—excluding the long tail of use cases other startups are pursuing.

• Many of these markets also include sizable non-startup participants generating significant revenue (e.g., Codex/Claude Code in coding; Thomson Reuters’ CoCounsel in legal)—but our analysis centers on independent startup players.

• Many of the work tasks outlined in our analysis may be embedded within model companies’ core products (e.g., ChatGPT and OpenAI’s search functionality) but are not broken out and included here.

• This analysis focuses exclusively on enterprise business—not consumer or prosumer business. Successful businesses (e.g., Replit and Gamma in app generation and design) serve substantial commercial user bases—but primarily target consumers or prosumers today. Since this analysis focuses on enterprise AI and where enterprises derive value, we exclude consumer-led businesses.

On the capability side, measuring AI’s impact across economic sectors is extremely difficult—though many economists are trying. Work is inherently ill-defined and long-tailed, making full automation exceptionally challenging. It remains unclear how much value enterprises derive from partial automation—if AI handles only 50% of a human task, the importance of the non-automatable portion may rise, as it becomes the bottleneck and thus increases in relative value. Therefore, we may overstate current capability—since each incremental 1% capability gain does not translate linearly into 1% economic value. Still, tracking relative capability—and how it evolves with each new model release—remains highly informative.

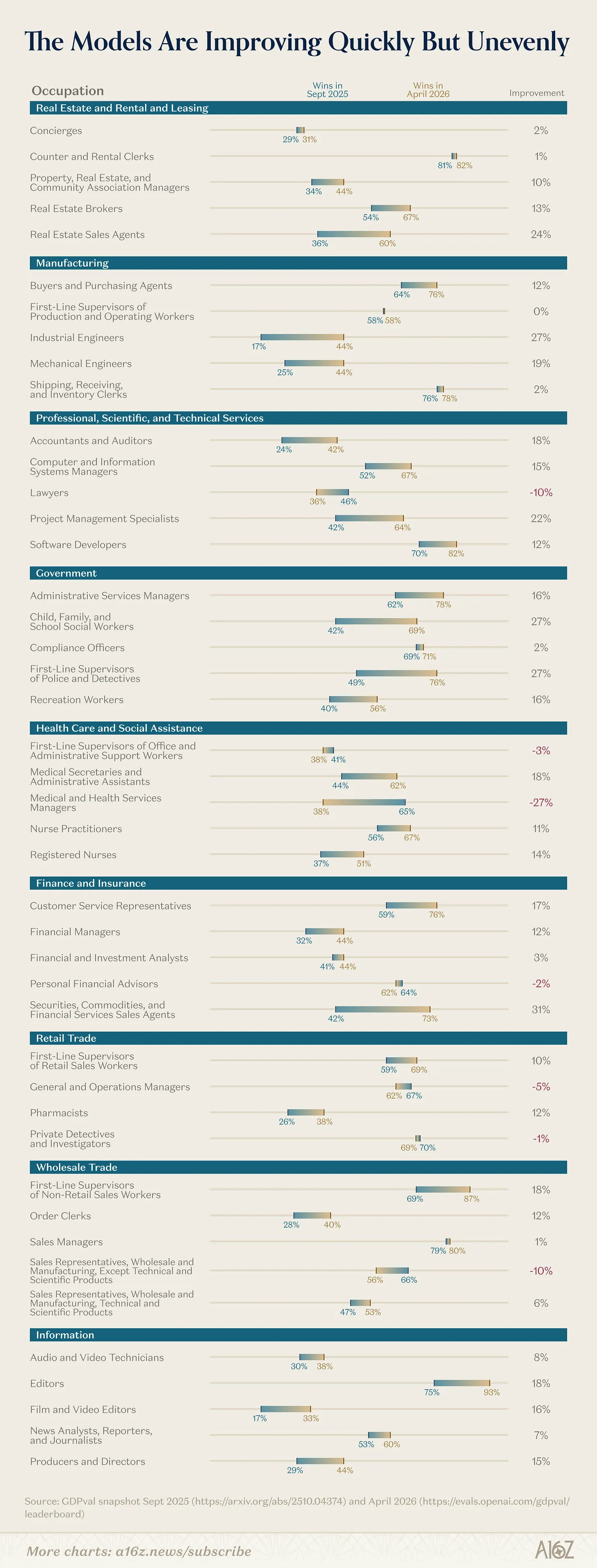

AI Is Entering Every Market

This analysis measures top-evaluated models’ win rates against human experts on economically valuable tasks, per the GDPval benchmark. Based on this, it’s clear that since fall 2025, models have become significantly stronger on economically valuable work.

So why haven’t all industries scoring highly on this evaluation shown comparable revenue momentum?

The industries enthusiastically adopting AI share several traits: they’re text-based; involve mechanical, repetitive work; feature natural human-in-the-loop involvement to inject judgment; face limited regulation; and produce clearly verifiable outputs (e.g., runnable code, resolved support tickets). Many industries lack these attributes—they either operate in the physical world, rely heavily on interpersonal dynamics, incur high coordination costs across multiple stakeholders, face regulatory or compliance barriers, or lack verifiable outcomes. While revenue momentum and model capability are clearly correlated, even in domains where models currently hold sub-50% win rates against humans (e.g., legal), companies like Harvey can still rapidly gain market share via co-pilot products enhancing individual legal work—and continuously improve their core offerings as models evolve.

The most notable finding here is the rapid pace of capability improvement. Several domains show dramatic gains over the past four months—accounting and auditing jumped nearly 20% on GDPval, and even fields like policing/detective work improved nearly 30%. We expect these jumps to catalyze compelling new products and companies in their respective domains. Moreover, model companies have explicitly announced plans to strengthen core capabilities for economically valuable work—focusing on spreadsheets and financial workflows, using computers to tackle legacy systems and industry-specific challenges, and meaningfully improving performance on long-horizon tasks—opening up an entire new class of work that cannot easily be sliced into short, digestible fragments.

Implications for Builders

Understanding where enterprises derive value—and how they assess ROI—as well as which sectors show clear demand versus which are emerging, helps clarify where AI builders’ opportunities lie.

Serving buyers in technology, legal, and healthcare is clearly fertile ground today—but we don’t believe there will be a single “winner” in each category. In legal, for example, there are many types of lawyers—corporate counsel, law firms, patent attorneys, plaintiff-side attorneys—each with distinct workflows and needs that different companies can address. Similarly, healthcare’s fragmented landscape of physician specialties, facility types, and payer structures creates parallel opportunities.

Beyond these sectors, another productive lens is identifying areas where capabilities are strengthening—but no breakout company has yet emerged in revenue terms. Many current businesses were built before model capabilities fully unlocked their product potential—but they’ve already established sufficient technical infrastructure and customer/market awareness to be best positioned when that unlocking arrives.

Finally, it’s critical to track where labs are concentrating their latest research efforts—specifically on economically valuable work. As long-horizon agents improve rapidly, computer-use capabilities receive heavy investment, and reliable interfaces for modalities beyond text (e.g., spreadsheets, presentations) advance, a whole new cohort of startups will soon possess the enabling infrastructure needed to deliver meaningful enterprise value.

Data Methodology: This data is aggregated from leading enterprise AI startups—including private data shared with us for this report, publicly available data, and anonymized insights drawn from thousands of conversations between a16z and startups and large enterprises.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News