Crypto VC Rat Race: A Hunger Game with No End

TechFlow Selected TechFlow Selected

Crypto VC Rat Race: A Hunger Game with No End

Embrace change; what defeats you has never been your opponent, but possibly the era itself.

Crypto VCs Are Everywhere

Attending blockchain week events in Shanghai recently, the biggest impression was that crypto VCs are everywhere—anyone without an investment title seems almost embarrassed to be part of the scene.

It’s understandable. In the current regulatory environment, mining, exchanges, and project teams are all considered politically sensitive and must keep a low profile. Only crypto VCs can step into the spotlight. Secondly, this bull market has lasted long enough for some people to accumulate significant capital. With FOMO (fear of missing out) rampant, fundraising has become easier—and the barrier to entry for crypto VCs is extremely low. Whether you have hundreds of millions or just tens of thousands of dollars, you can still call yourself a "Crypto Fund."

Exchanges, projects, KOLs, communities, media... everyone is becoming a VC.

1. Exchange-affiliated VCs

Major exchanges either invest under their own name or set up dedicated capital brands. Some even act as LPs (limited partners) for other VCs—it's clear they're well-funded.

For example, one exchange runs Ventures, Labs, and Grants divisions—all involved in investing, leading to internal competition from the start.

Another trend involves exchange employees leaving to launch their own funds while maintaining close ties with their former employers.

Overall, however, aside from top-tier players like Binance Labs, exchange-linked capital is seeing declining influence. Top-tier projects often avoid early-stage entanglements with exchanges.

2. Project-affiliated VCs

A common trajectory in crypto: mint tokens → build personal fame/influence → move into investing.

After earning initial profits from a successful project, founders go on to capitalize further—building personal influence, gaining more voice, and launching funds either individually or under the project’s brand.

Sometimes, project teams raise large sums specifically to form a VC arm. Timing it right during a bull market, they make broad investments and earn huge returns—then list their own token on exchanges for additional profit. One fund, two purposes.

Additionally, major projects—especially public chains—are launching increasingly massive ecosystem funds.

3. Traditional/Outside Capital

In bear markets, crypto is called a scam; in bull markets, it's hailed as revolutionary. Attracted by rising prices, traditional VCs and old money are flooding back in, driven by FOMO and joining the competitive fray.

When Sequoia leads the charge, other dollar-denominated funds feel compelled to follow—investing both capital and personnel to explore the space.

That said, Sequoia has restructured its fund architecture to directly invest in crypto, removing institutional barriers. Most traditional VCs still operate under conventional structures, limited to equity investments in large projects—with few options available. More importantly, they lack methodologies for deploying LP capital in such a volatile sector—and suffer from a severe talent shortage.

Behind the scenes, outside players are far more deeply involved than most realize. Funds backed by external LPs—from big tech firms, listed companies, traditional gaming studios, financial institutions, even media conglomerates—are sprouting up rapidly. After all, no one turns down profit.

Of course, nobody openly says “we’re investing in crypto”—too crude. The proper phrasing is: “We’re investing in Web3, the metaverse, the next-generation internet.”

Truthfully, many elite traditional VCs look down on crypto folks, seeing them as scammers who got lucky (imagine Wang Xiaochuan looking at Sun Yuting). Every industry has this bias—but disruptive innovation often emerges precisely from these underestimated corners. That’s the narrative of Web3: bottom-up transformation. Weakness and ignorance aren’t survival threats—arrogance is.

Conversely, those within crypto view traditional VCs as opportunists—arriving in bull markets and fleeing faster than anyone when bears return. To some, Shen Nanpeng is just another Xu Xiaoping. (Poor Mr. Xu, whose offhand comment years ago—"the blockchain revolution has arrived"—has turned him into a lasting meme in the crypto world.)

Ultimately, the community prefers crypto-native players over so-called elites and authorities.

When global Sequoia changed its Twitter bio to include DAO-related tags and started saying "GM," people found it awkward—“like middle-aged folks trying too hard to use youth slang to fit in.” On December 9, Sequoia reverted its bio—a moment dubbed “One-Day Reform.”

*Note: This categorization of “outsiders” isn’t entirely accurate. Firms like Sequoia and IDG have long been active in crypto—IDG was even an early pioneer. We’ll cover this separately later. This is just a rough classification.

The VC Dilemma: Money Without Brand

With VCs everywhere, internal competition is inevitable. When everyone has money, the real question becomes: What else do you offer besides capital?

VCs are increasingly becoming service providers. Some help get projects listed on exchanges; others inject millions to boost TVL; some write press releases, manage PR, build communities—turning themselves into hybrid media and PR agencies.

Many VCs now love to claim they have “deep incubation capabilities”—which usually means they’ll introduce a few contacts or publish an article. The bar for “incubation” keeps dropping.

But in my view, for any VC, brand is the ultimate and most valuable asset.

Having money but lacking brand recognition is the core dilemma facing many small-to-mid-sized crypto VCs today.

There’s a prevailing consensus (and bias) in the industry that truly high-quality projects are overseas-based. Hence, building a strong international brand is crucial for VCs today.

Some investors discriminate against Chinese-founded projects, and vice versa—some Chinese projects look down on domestic capital.

For instance, a Chinese team secures funding from top-tier Western investors, then raises its valuation exponentially before letting domestic investors in. Or a project takes local capital first, then raises from global funds—and later demands to fully or partially remove the earlier domestic investors: “Your brand just doesn’t cut it.”

Thus, the key challenge for VCs is: Beyond capital, how do you define and cultivate your core competitiveness? How do you build a global brand?

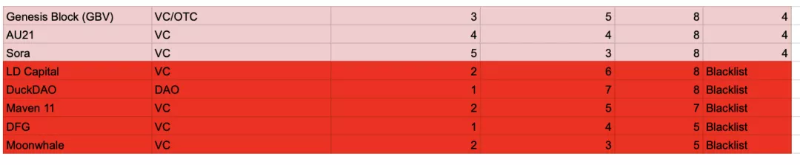

One case worth studying is LD Capital.

Due to past controversies, older community members often hold negative views toward LD Capital, frequently associating it with “harvesting韭菜 (retail investors).” There was even a viral VC ranking chart circulating online, falsely attributed to the well-known overseas community LobsterDAO, which placed LD Capital on a blacklist.

On this issue, LD Capital may have been unfairly treated.

Here’s what happened: The list existed long before, with unknown origins. Someone posted it in LobsterDAO’s Telegram group; Defiprime reposted it on Twitter citing LobsterDAO; Chinese media picked it up and republished it domestically as “LobsterDAO’s crypto VC ranking.” But the community later clarified it had no connection to the list.

Whether one accepts the list is purely subjective.

I know many in the industry dismiss LD Capital, calling their strategy blind spraying—attributing any success to luck. But setting aside bias, examining their portfolio reveals solid achievements, especially in blockchain gaming, where they’ve profited enormously this year.

Looking closer: Illuvium bought at $3, peaked at $2,000; Star Atlas at $0.00045, hit $0.26; Alien Worlds at $0.003, reached $7—multiple projects generating over $100 million in paper gains.

So the question arises: How did a VC with questionable reputation manage to back so many star projects?

I asked someone at LD Capital, and got a vague answer: “CEO Yi Li has great vision, our partners are outstanding, and the team collaborates well.”

To elaborate: Founder Yi Lihua delegates extensively, giving team members autonomy and room to grow. Key partners bring in most quality deals through personal networks. LD Capital emphasizes post-investment support, with the entire team serving portfolio companies.

Very official—but correct. The core driver is exceptional individuals (partners).

Yet this also highlights a bottleneck for LD Capital and similar VCs: Once scaling up, brand matters. You can't just hire more people to chase deals—you need projects to come to you. A strong brand makes investing effortless. Otherwise, bigger size means heavier workload and fiercer internal competition.

Just as Tencent defined its mission in 2005 as “becoming the most respected internet company,” crypto entrepreneurs should also think big—earn money, yes, but cherish their reputation and aim for the global stage.

As a fellow in the industry once said, “If you make a fortune but lack respect, people will only see you as a coal tycoon from the crypto world.” I couldn’t agree more.

Downgrade Strike: Big Capital and Their Inner Circles

The reality of crypto inflation: polarization and capital clustering.

While small-to-mid VCs fight tooth and nail over $10K allocations, top-tier VCs wield both capital and brand power to dominate the landscape—and they stick together.

a16z, the standard-bearer of Web3, has partners tirelessly writing essays on Twitter to evangelize Web3 and capture mindshare.

Want to understand Web3? Visit a16z’s website and read Future (their media platform). Want to know top Web3 projects? Check a16z’s portfolio. That’s exactly the effect they aim for—seizing话语权 in the Web3 era.

Paradigm raised $2.5 billion for its latest fund. Money helps, but what’s truly formidable is Paradigm’s first-class research, innovation, and execution—they can build innovations from scratch.

On November 25, Paradigm appointed Georgios Konstantopoulos as CTO. At the top of the blockchain food chain: technology + capital. I believe this is the future norm for Tier-1 crypto VCs: technically fluent, and technically capable.

Cutting-edge theoretical innovation? Paradigm has it. Hardcore tech? Paradigm has it. Capital? Paradigm has plenty. So much so that Paradigm can turn mediocrity into magic—just look at how Uniswap was nurtured step-by-step by Paradigm.

In traditional VC circles, Lightspeed and Sequoia are expanding into crypto at rocket speed—and building their own exclusive networks.

This reflects another major trend in crypto VC: capital consolidation, growing ever more closed-off.

Each blockchain ecosystem has its own circle of VCs. You’ll often notice the same few names backing top projects—Polkadot, Solana, etc. Even Ethereum’s star projects are largely divided among inner circles.

Terra’s ecosystem was particularly closed—mostly controlled by Do Kwon and his allies. Delphi Digital, for example, directly incubated projects and designed economic models, leaving little room for outsiders.

It’s logical—why share a project with 99% profit certainty with outsiders when you can keep it for yourself or your close collaborators?

Self-reliance breeds strength across the board.

The Future of Crypto VCs

Back to basics: How do you back winning projects?

The answer boils down to two things: finding great projects, and getting in. Most VCs fail at the second step.

Long-term, crypto VCs must develop unique core competencies to strengthen their brand.

In my opinion, a promising approach is building influence in a vertical niche.

You can’t catch every opportunity. Instead of casting a wide net, focus deeply on one area—crowded spaces are rarely rewarding.

Take Animoca Brands and its parent Everest Ventures Group (EVG)—both深耕 gaming for years. With the rise of blockchain games like SANDBOX, they’ve shot to fame.

In the early hours of December 9, Animoca founder Yat Siu shared their 2021 performance:

1. Investment and digital asset revenue grew to ~$529.6 million in the first nine months of 2021, holding over $600 million in liquid digital assets (BTC, ETH, USDC, AXS, FLOW, etc.).

2. Digital asset reserves within Animoca’s product and platform ecosystem (including REVV, SAND, TOWER, GMEE, and other proprietary tokens) rose from ~$2.9 billion at end-September 2021 to ~$15.9 billion by end-November.

Multicoin Capital’s success primarily came from Layer1 bets—especially Solana and THORChain (which I define as 'cross-chain L1').

Secondly, embrace change: You’re not beaten by competitors, but by shifts in the times.

In Jin Yong novels, Jinlun Fawang spends 16 years mastering his martial arts—only to be defeated instantly by Yang Guo, who breaks all conventions. It wasn’t camera rivals that killed Kodak, but smartphones. The future threat to crypto VCs may not come from existing peers.

This is an era where everyone is media, and everyone is a VC.

Here are a few emerging VC organizations and models I believe could rise:

DoraFactory: I noticed this group because a friend at a major crypto VC told me, “DoraFactory is way better than us at landing top projects.”

Simple reason: DoraFactory is backed by DoraHacks, which has hosted over 100 global blockchain hackathons—where star projects like Matic originated.

Think of DoraHacks as the first caregiver for groundbreaking projects—nurturing them early and securing privileged access to investment opportunities.

As new blockchains enter a Warring States era, hackathons have become battlegrounds for talent. Gitcoin represents Ethereum’s camp—while neutral DoraFactory occupies a critical cross-chain ecological position.

Next, DAO VCs—or venture DAOs. I see them as unions of super individuals, deconstructing and disrupting traditional VC models.

Currently, they haven’t disrupted traditional crypto VCs—but the wind is blowing, stirring waves.

Metacartel, for example, includes founders of Aave, Nexus Mutual, Ocean Protocol, and Axie Infinity—and has incubated Rarible, Gelato Network, and DAOHaus.

Venture capital has long been concentrated in Silicon Valley—both capital and talent localized. But DAO-based VC funds can invest globally and recruit talent worldwide. In DAO models, carry and fees can be embedded directly into smart contracts.

The road ahead is long—but change is underway.

*Finally, if you're involved in or interested in Web3 investing, feel free to add TechFlow01—we might have something to discuss.

*TechFlow is a community-driven deep content platform committed to delivering valuable insights and thoughtful perspectives.

Community:

WeChat: TechFlow01

Twitter: @TechFlowPost

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News