a16z Invests $500 Million in One Month, Small Funds Line Up to Shut Down: Where Is Crypto VC Capital Flowing?

TechFlow Selected TechFlow Selected

a16z Invests $500 Million in One Month, Small Funds Line Up to Shut Down: Where Is Crypto VC Capital Flowing?

Let's break down what TVPI and DPI actually mean, what GP and LP will respectively face in the second half of 2026, and who the real winner is.

Author: Ben Lakoff, CFA

Compiled by: TechFlow

TechFlow Editor's Note: The title of Carta's latest report is "VCs Are Back," but what's recovering is just paper valuations (TVPI); cold hard cash (DPI) hasn't returned to LPs yet. This monthly financing report breaks down the situations of GPs and LPs in 2H 2026: who's making money, who's holding on, and what this logic looks like applied to crypto VC. Author Ben Lakoff is a licensed CFA focusing on early-stage crypto investment, with direct views and high data density. All crypto financing deals and hackathon results for June are attached at the end.

Gm!

Welcome to the June Deal Flow Digest, a snapshot of all the crypto financing I tracked last month.

This month's feature article digs into VC fund performance. Carta released the 2026 Q1 VC Fund Performance Report, with the headline "VCs Are Back." But paper value returns much faster than cash. Let's break down what TVPI and DPI actually mean, what GPs and LPs will face respectively in the second half of 2026, who the real winners are, and what this logic looks like specifically for crypto VC.

Remember to check that table at the end; all June transactions are in there, along with recent hackathon and Demo Day results (in the links).

Carta tracked 2,775 funds holding approximately $119.3 billion in assets. The data shows that median fund valuations have risen for almost every recent vintage (referring to the year the fund was established), fundraising pace has accelerated, and the overall outlook for VC has improved significantly.

From 2017 to 2024, the median TVPI for almost every vintage has been climbing, for six consecutive quarters. TVPI (Total Value to Paid-In) measures what a fund is worth now, including unrealized book value. The valuation reset in 2022 and 2023 that wiped out everyone's paper value is basically over.

This is good news. But the key to the story is: paper value is back (paper gains), cash is not.

VC is recovering, but only unrealized book value (TVPI) is rising

Let's start with the truly positive part. The median TVPI for the sample has started moving up and to the right again for basically every recent vintage. Valuations stopped falling and then started rising, and funds holding these assets mechanically became more valuable.

Note: Median TVPI for vintages has risen for six consecutive quarters

Source: Carta 2026 Q1 Report

Who is pushing it up? Mostly the top tier.

The 90th percentile valuations for every stage are soaring, and most of it comes from one sector. Carta's Private Markets Companion Report shows that AI ate up a record share of every dollar VC invested. If your fund has AI exposure, the book looks healthy. If you're running an infrastructure-type "pick-and-shovel" business, or betting on something outside the narrative, your "recovery" is much weaker.

So this tide hasn't lifted all boats. It basically only lifted (significantly) the few boats carrying foundation models. Not surprising.

This determines how you should read that number in the headline. High TVPI does not equal a good fund. It is a snapshot, reflecting what someone somewhere is theoretically willing to pay, not money actually wired into LP accounts.

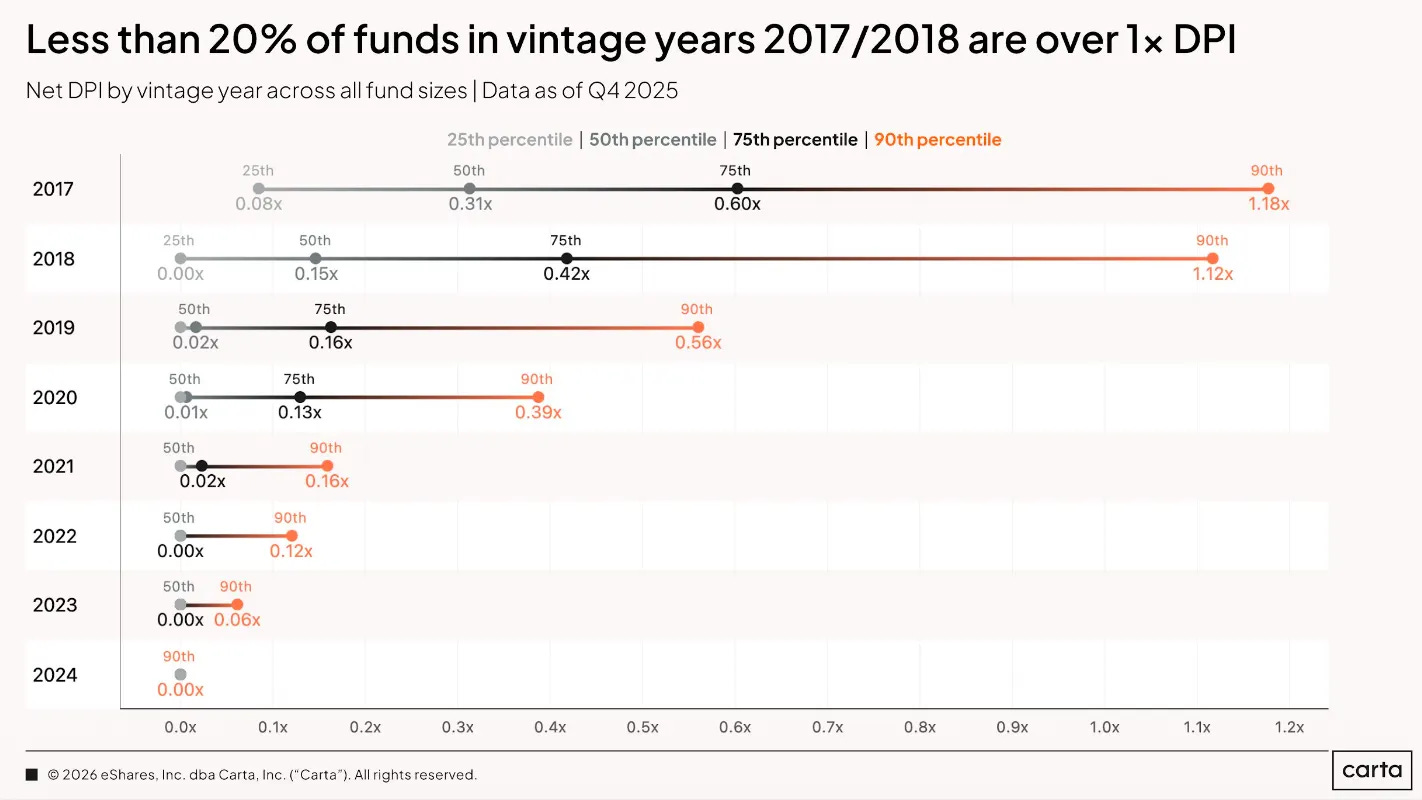

No one is actually getting paid (DPI)

This is the part the recovery story skips. DPI (Distributions to Paid-In) is the cash a fund actually returns to LPs, and this number is still very low.

For 2019 and 2020 vintages, the median DPI is only slightly above zero, and more than half of the funds haven't returned a single cent to LPs. These are funds that were established five or six years ago.

Note: Median DPI for 2019 and 2020 vintages is only slightly above zero; over half have not returned any cash

Source: Carta 2026 Q1 Report

The older batch should be better, but results are worse. 2017 and 2018 vintages are nearly ten years old, in the latter half of their lifecycle, when distributions should be appearing. Yet less than 20% of funds have touched 1x DPI, meaning returning the money LPs initially invested.

The problem is the J-curve refuses to complete its second half. Early in a fund, money goes out and IRR turns negative, then as valuations rise and exits land, the curve should bend upward. Now valuations are rising (TVPI has proven that), but exits aren't landing. The IPO window has only cracked open for a few names, M&A is picky, and the rest are marked at high prices, stuck there unable to move.

PitchBook, Preqin, NVCA, Wellington, judgments on 2026 all point to the same thing: liquidity is the bottleneck, plain and simple. The remedy everyone is sizing up is the secondary market, continuation vehicles, GP-led deals, LPs selling stakes for cash rather than waiting for traditional exits. This will quickly move from niche to more common.

For GPs, the signal read is uncomfortable but simple. A fund with beautiful TVPI and DPI near zero will start getting asked ugly questions in the next 12 to 18 months. LPs were patient throughout the reset period. Before they reinvest, they want to see cash. Whoever can proactively manage a liquidity path (partial exits, secondaries, continuation funds) will have an advantage over those who just keep issuing beautiful paper numbers.

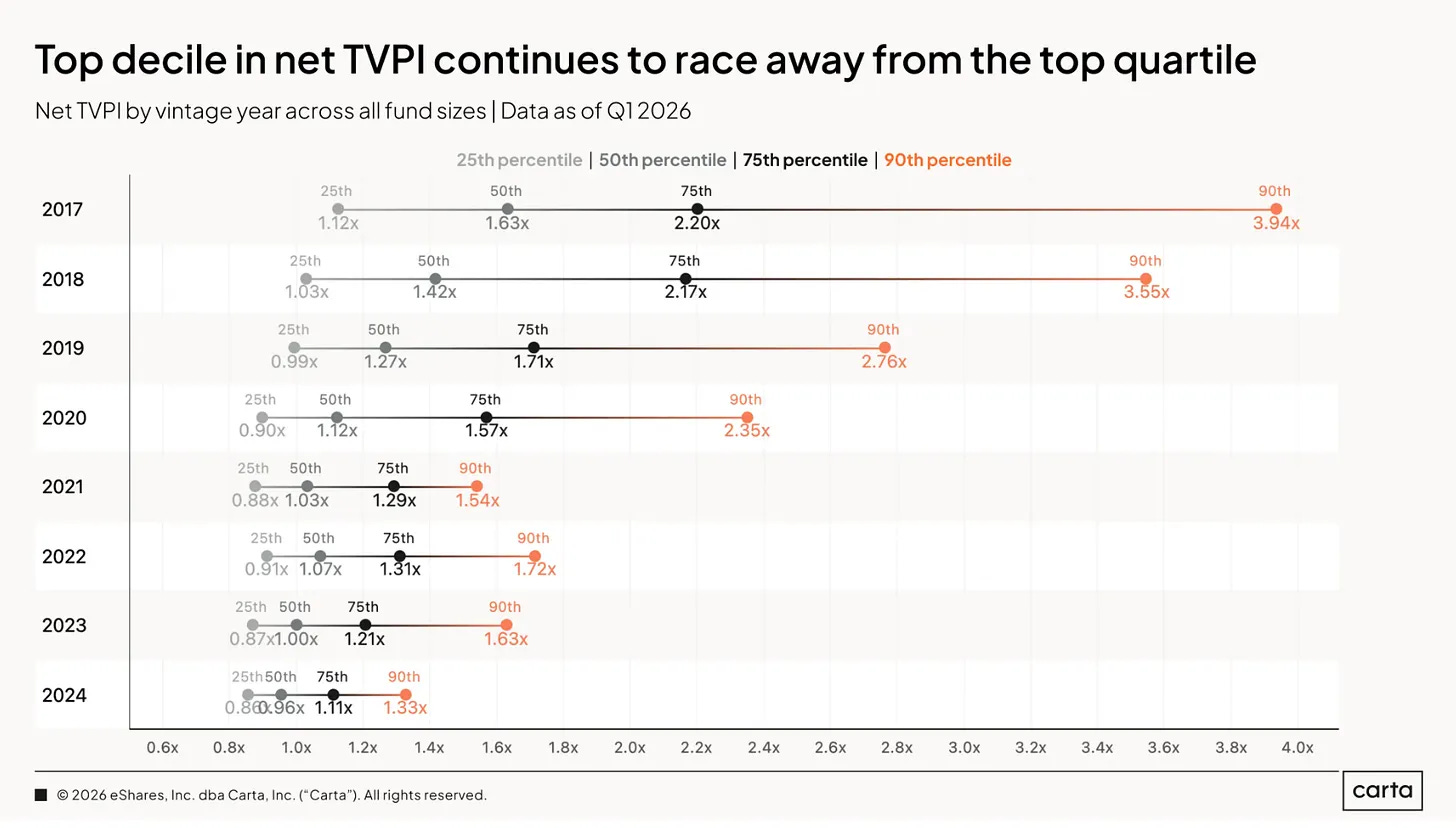

VC is a power law game, and the gap is ridiculously large

Regardless of recovery, dispersion is the permanent feature inside VC.

For almost every vintage, the 90th percentile net IRR is over 20%, while the 75th percentile is still below 15.5%. The distance from "top quartile" to "top decile" is huge. Most funds are crowded in the "okay" tier.

And the gap compounds. For reference: 10 years of 20% annual growth is 6.2x, 10 years of 10% annual growth is 2.6x.

Note: Net IRR distribution for vintages, 90th percentile generally over 20%, huge gap with 75th percentile

Source: Carta 2026 Q1 Report

VC is not just the asset class with the highest returns, it is also the one with the highest dispersion.

Translation for LPs: Choosing a manager is not one of many inputs, it is the input. Indexing the entire asset class, you get the median, and the median VC fund is at best a slow, illiquid 2.6x.

The middle layer is being squeezed out

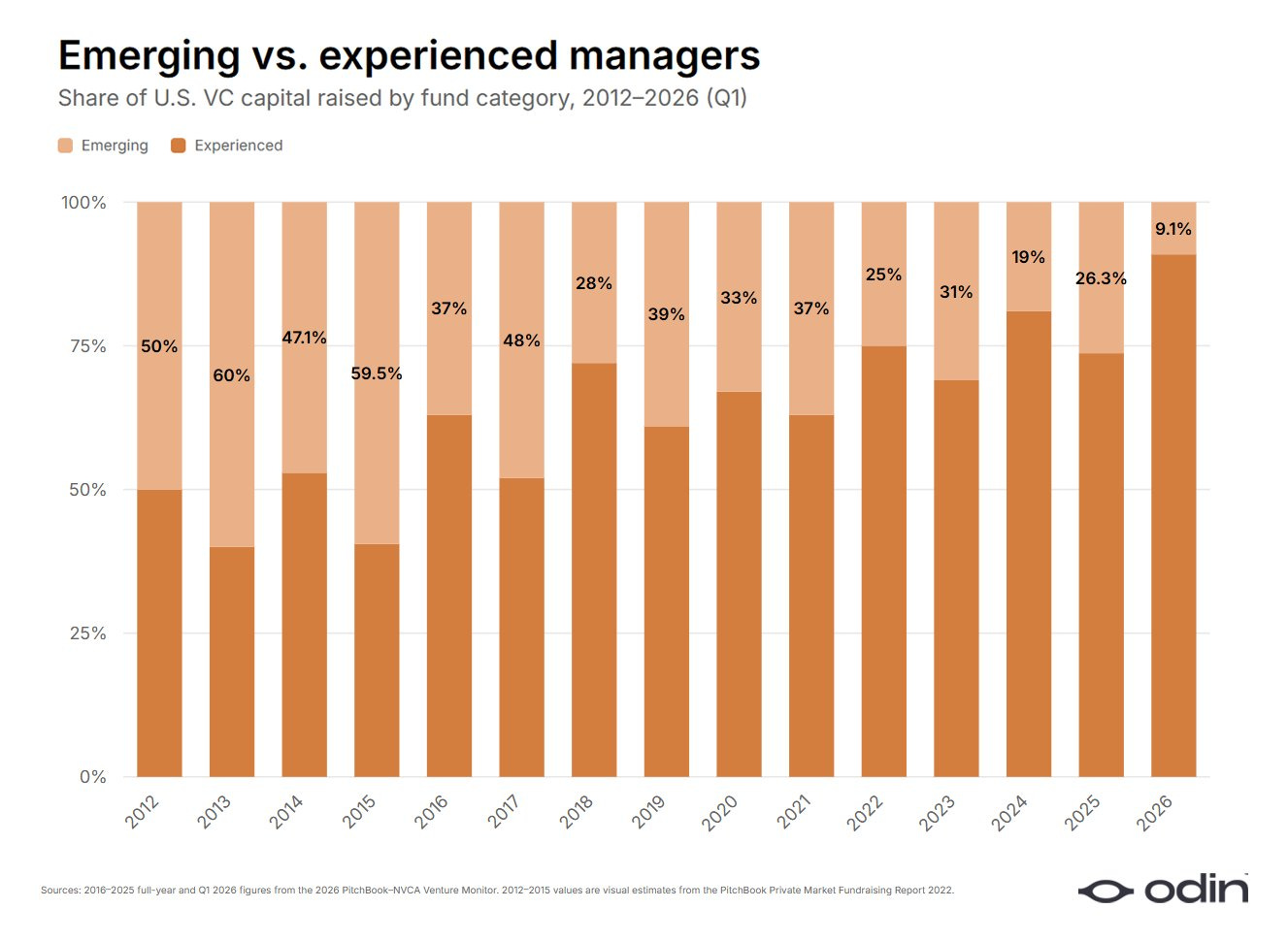

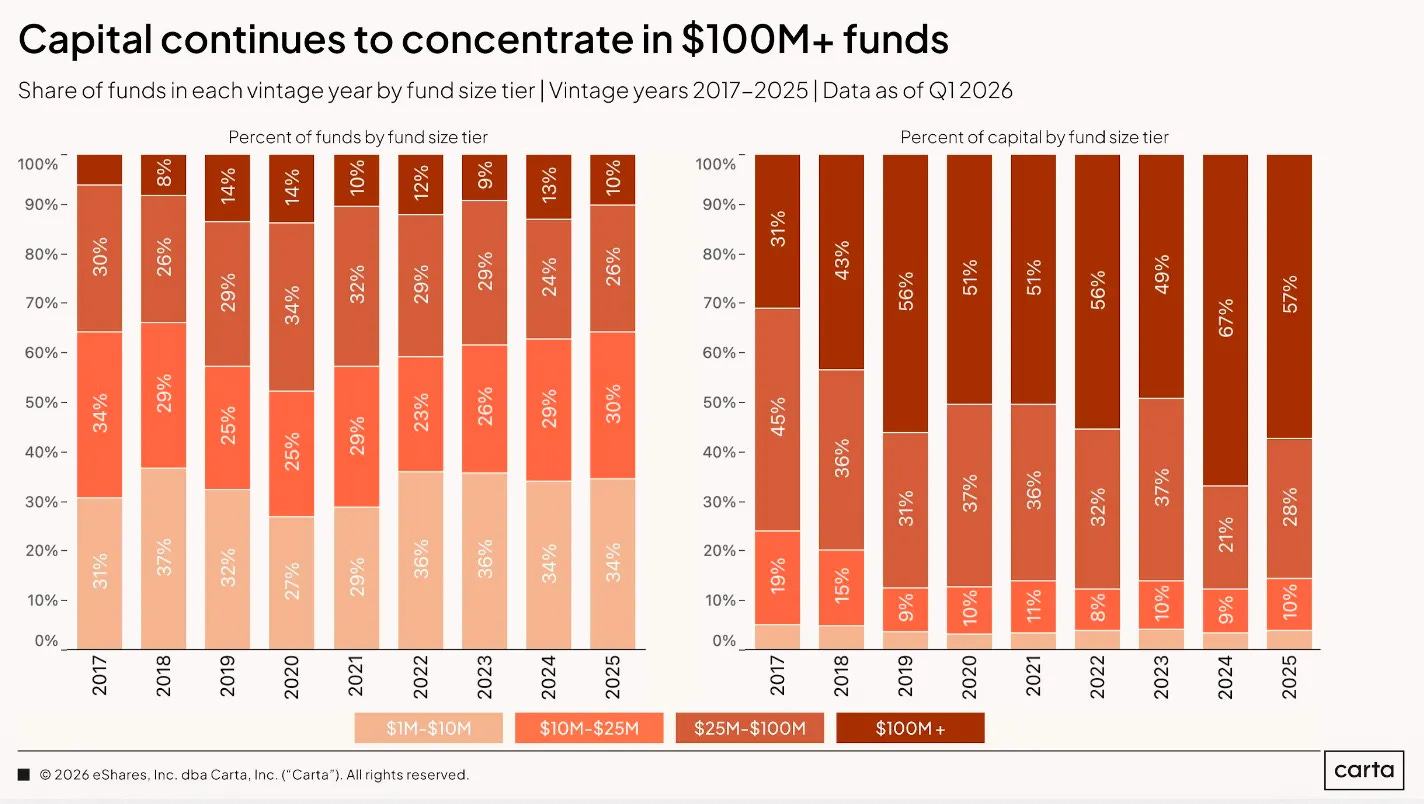

The last piece, perhaps the most structural one, and a theme I've repeated in recent articles: capital is concentrating.

Note: Capital is concentrating towards top-tier funds

Source: Carta 2026 Q1 Report

Funds over $100 million took 57% of all VC fundraising in 2025. Eight years ago this number was 31%. Most newly established funds are still small funds under $25 million, but the share absorbed by large funds is growing every year.

Note: Number of small funds under $25 million still dominates, but total fundraising tilts towards large funds

Source: Carta 2026 Q1 Report

This is a dumbbell structure. Super-large funds raise via balance sheets and brands. Truly differentiated micro funds raise via edge strategies. The undifferentiated middle layer is where fundraising goes to die. Hobbyist VC managers are heading home. The crossover and generalist capital that flocked into private tech at the 2021 peak is retreating to its old lanes.

Overall fundraising is stabilizing (Carta Q1 recorded 86 new funds, $3.9 billion, the strongest start since 2022), but "stabilizing" does not equal "evenly distributed." This money is going to people with track records, leaving everyone else.

My key takeaways

Broken down to the simplest, just four points:

Paper recovered, cash did not. TVPI is a story about sentiment, DPI is the only number LPs can spend.

Power laws are alive. A few funds win big, most are mediocre, the distance between the two is the whole game.

Liquidity is the next dominant logic. Funds that can create distributions, not just report paper gains, will win the next round of fundraising.

The trend of capital concentration. Either be big, or be sharp, don't get stuck in the middle.

Carta doesn't break out crypto separately, so none of the above are "our" numbers. But the physics are the same, just louder in crypto.

Crypto VC is more dispersed, more concentrated, and more reflexive than the broader market. Hobbyists ran here earliest and hardest. This suits me fine: at the pre-seed stage, the only lasting advantage is picking the right person before the crowd shows up. Data keeps confirming this, the median is a trap, the work is all in the tails.

Okay, next is the rest of June crypto and Web3 financing :)

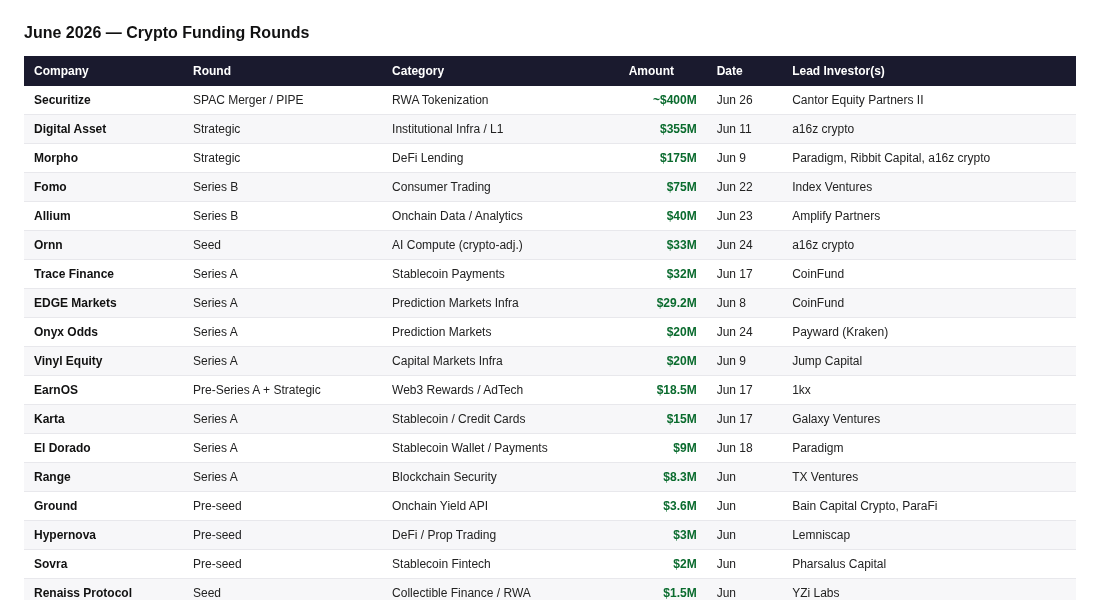

Top 10 Crypto Financings in June

Securitize | SPAC Merger / PIPE | RWA Tokenization | ~$400 million | 2026-06-26

This BlackRock-backed tokenization leader is listing on the NYSE via merger with Cantor Equity Partners II (ticker SECZ), gross raising approximately $400 million, including an oversubscribed $225 million PIPE. Clients include Apollo, KKR, Hamilton Lane, and VanEck; Securitize is also helping the NYSE build its own tokenized securities platform. This is a public listing rather than a private VC round, so it tops the list with an asterisk, but it is also the cleanest milestone this year for "tokenization going mainstream." The transaction is expected to close around July 1.

Digital Asset | Strategic Round | Institutional Infrastructure / L1 | $355 million | 2026-06-11

a16z crypto led this month's truly largest crypto financing, valued at $2 billion, with a co-investor list reading like a Wall Street roll call: Citadel Securities, Abu Dhabi Investment Authority affiliates, BNP Paribas, HSBC, Apollo, Optiver, Tradeweb, CME Ventures, S&P Global, SBI, SoFi, Coinbase Ventures, and Polychain. Digital Asset builds Canton, a privacy-enhancing public L1 chain for regulated capital markets, supporting approximately $6 trillion in tokenized asset issuance, with users including JPMorgan, DTCC, and Visa. If you want a data point for "TradFi choosing rails," this is it.

Morpho | Strategic Round | DeFi Lending | $175 million | 2026-06-09

Paradigm, Ribbit Capital, and a16z crypto co-led, with Apollo Funds, Circle's VC arm, and VanEck co-investing, valuation up to $2 billion. Reportedly the largest DeFi round to date. Morpho allows anyone to "build their own Aave," creating customizable lending markets. Its client list (Coinbase, Kraken, Anchorage, Galaxy) explains why institutional capital suddenly dares to underwrite on-chain credit. The thesis "DeFi is the backend of FinTech" got funded.

Fomo | Series B | Consumer Trading | $75 million | 2026-06-22

Index Ventures led $75 million, valuation $550 million, with Union Square Ventures and angels Mark Pincus, Kevin Hartz, Humam Sakhnini, etc. co-investing. Fomo is a non-custodial social trading App, abstracting away wallets, gas, and bridging. Onboarding, depositing, and buying a token takes about 30 seconds, with leaderboards and social flow added on top. 625,000+ users, $4 billion in trading volume, the brightest consumer financing this month.

SignalPlus | Series B | Institutional Derivatives Infrastructure | $50 million | 2026-06-02

HashKey Capital led, valuation $500 million, BlockBooster ($10 million cornerstone) and AppWorks co-invested, Goldman Sachs acted as advisor. SignalPlus is an institutional-grade options and derivatives terminal, understandable as the Bloomberg terminal of crypto options, serving Cumberland, FalconX, and Galaxy Digital. Platform trading volume reached $16 billion in Q4 2025 alone, with a quarterly compound growth rate of 74% since 2023. The options market is crypto's next liquidity layer, this is a dominant infrastructure bet within it.

Allium | Series B | On-chain Data / Analytics | $40 million | 2026-06-23

Amplify Partners led, Kleiner Perkins and Theory Ventures co-invested. Allium cleans and structures on-chain data across 150+ chains for institutional clients, reportedly with Visa, Federal Reserve, a16z, and Coinbase on the client list. This is a "pick-and-shovel" bet on institutional crypto adoption, with a clear second act waiting for "agent" buyers to appear.

Trace Finance | Series A | Stablecoin Payments | $32 million | 2026-06-17

CoinFund led, Coinbase Ventures, Haun Ventures, Jump Capital, Paxos, and Chainlink Labs co-invested, angels include Solana's Anatoly Yakovenko. This Brazil-headquartered company stitches local bank channels, FX, compliance, and stablecoin settlement into cross-border payment infrastructure, having processed over $10 billion in institutional trading volume, this round valuation is approximately 10x the 2022 seed round. The "stablecoins as payments" thesis is landing where it truly changes lives.

EDGE Markets | Series A | Prediction Market Infrastructure | $29.2 million | 2026-06-08

CoinFund led again, Indicator Ventures, Mantis VC, StepStone Group, and Bullpen Capital co-invested. EDGE builds the pipes underneath regulated prediction and betting markets: EDGE Pro is a high-throughput deposit account for market makers, covering CFTC-regulated venues; EDGE Connect is a real-time payment channel, cutting costs by over 70%. It's the unglamorous layer the prediction market boom can't expand without.

Onyx Odds | Series A | Prediction Markets | $20 million | 2026-06-24

Kraken parent Payward led $20 million, valuation $220 million. Onyx Odds is a sports-oriented prediction market App; as part of the deal, it will integrate Payward Services (Kraken's B2B infrastructure) and add crypto trading inside the App. This is Kraken spending money to squeeze into the prediction market land grab, standing on the other side of the Kalshi/Polymarket arms race.

Karta | Series A | Stablecoins / Credit Cards | $15 million | 2026-06-17

Galaxy Ventures led a $15 million equity round, part of a larger $140 million financing, including a $125 million credit facility from Community Investment Management. Karta issues US credit cards operated via WhatsApp for global travelers and high-net-worth non-residents, stitched underneath with stablecoin infrastructure and an AI concierge. 2025 revenue and payment volume grew 10x, Q1 2026 grew another 4x.

El Dorado | Series A | Stablecoin Wallet / Payments | $9 million | 2026-06-18

Paradigm led, Coinbase Ventures and Verda Ventures co-invested, El Dorado cumulative financing approximately $12 million. This peer-to-peer stablecoin wallet does cross-border payments for underserved Latin American markets, expanded to enterprise payments on the Tempo blockchain, connected to 100+ enterprise clients (including merchants importing EVs from China). Small check, betting exactly on the right end of the stablecoin thesis.

Click here to see all June financing transactions: Spreadsheet Link

June Crypto VC Fund Fundraising Announcements

Two new fund announcements this month, both expanding mandates from pure crypto to AI / Agent themes.

Variant | Variant 4|$222 million|June 2026

Variant raised $222 million for its fourth early-stage fund,围绕 an "autonomy" thesis: any application that gives users more agency, spanning permissionless finance, crypto infrastructure, and agent AI. Its framework is that crypto is the "pipe" that makes products run (e.g., Uniswap, Morpho), not the product itself. (First close and final close sizes undisclosed.)

Framework Ventures | Framework Fund IV|$400 million|June 2026

Framework closed an oversubscribed $400 million fourth fund (FIV), approximately half deployed. Single checks range from $1 million to $50 million, covering pre-seed to Series A, mandate now extends from crypto (stablecoins, tokenization) to AI, robotics, energy, and FinTech. LPs are primarily institutional, anchored by an Ivy League endowment, sovereign wealth funds, and fund of funds.

Reminder, if you are interested in learning about Bankless Ventures Fund II, please fill out this form, and we will contact you!

Hackathons

Starting Soon

ETHGlobal Lisbon 2026|July 24-26, 2026

Lisbon, Portugal, offline. Pragma Lisbon runs concurrently with the hackathon. (Unfortunately I'm not in town :()

ETHOnline 2026|September 4-16, 2026

Online asynchronous hackathon. ETHGlobal's flagship remote event.

Colosseum Fall Hackathon|September 28 - November 2, 2026

Online. Next session of Colosseum's Solana ecosystem competition, following the record-breaking Frontier Hackathon.

Ongoing

Colosseum "Eternal"|Rolling

Online. On-chain competition Colosseum runs regularly between flagship hackathons, outstanding teams are considered for pre-seed financing and accelerator inclusion.

Demo Day

Starting Soon

Colosseum Accelerator Demo Day|Summer 2026 (Date TBD)

Private Demo Day, for the top ~10 teams in the Frontier Hackathon accelerator batch (8-week program, first two weeks in San Francisco), pitching to top crypto VCs. (Exact 2026 dates not yet announced.)

Alliance DAO Demo Day|Approx. August 2026 (Date TBD)

Tied to the ALL17 batch starting in May. Dates not officially confirmed.

Accelerator Open Applications

Alliance DAO (ALL18)|Open / Rolling

Online plus offline retreat. ALL18 batch starts September 7, 2026, interview results out about 2 weeks after application, rolling throughout the year. Acceptance rate approx. 5%; median graduating team raises $3.5 million at $25 million post-money valuation. Program is free; takes $500,000 at founder-friendly terms.

Colosseum Accelerator|Rolling (via Eternal)

2 weeks in San Francisco plus 6 weeks remote-friendly. Main entry points are Frontier Hackathon (closed) and the always-on Eternal competition. Each startup gets $250,000 at founder-friendly terms.

Outlier Ventures Base Camp|Open / Rolling

Online plus offline. 12-week, token-design-focused accelerator, accepting early applications for 2026 batch, directions covering DeAI, DeFi, RWA, and DePIN.

Techstars Web3|Open

Online plus offline. Reportedly 2026 applications are open; standard Techstars terms.

That's it for June!

Thanks, and good luck out there!

Ben Lakoff, CFA

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News