Opinion | UNI is not a governance token, its value is severely underestimated

TechFlow Selected TechFlow Selected

Opinion | UNI is not a governance token, its value is severely underestimated

UNI is often mistakenly referred to as a "governance" token, and the market tends to believe that "governance has no value." However, in reality, UNI is a pass-thru token, meaning its revenue will be passed through to token holders. UNI token holders will receive a very substantial revenue stream starting in February 2021.

Original | Jeff Dorman

Translation | Overnight Porridge

Source | Bitmain

Bitcoin is surging ahead, while DeFi seems to be experiencing a winter! For example, Uniswap's token UNI has continuously halved, and the market has begun questioning its value. Governance tokens appear to have become a joke. In response, Jeff Dorman, Chief Investment Officer at New York-based investment management firm Arca, shared his thoughts on Twitter, arguing that UNI is severely undervalued. Below is the original text:

The investment case for holding ETH is that Ethereum is a clear market leader with strong growth and usage metrics, even though ETH token holders have not yet captured this value. The same logic actually applies to UNI.

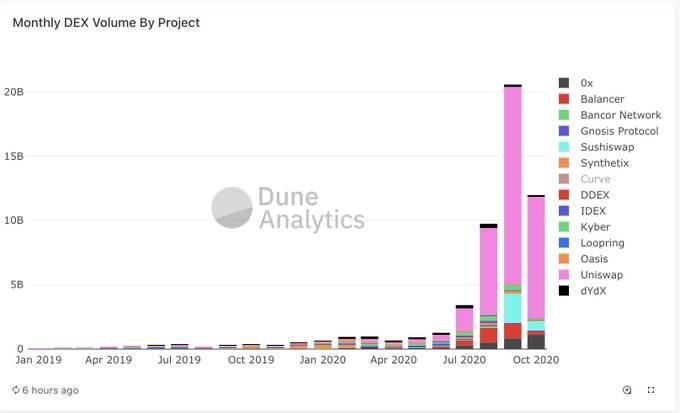

Uniswap holds a dominant lead in the DEX trading market, just like "Ethereum vs. other smart contract protocols." In the DEX space, no protocol comes close to Uniswap (analysis from @DuneAnalytics).

For ETH, EIP-1559 and Ethereum 2.0 have remained in the "future," but UNI's "fee switch" is almost certain—it will be activated on February 26, 2021 (180 days after governance began).

Then, UNI will join a small group of tokens such as HXRO, MKR, FTT, and BNB—tokens that derive real value from revenue.

Based on Uniswap’s average daily trading volume of $360 million and a 0.30% fee, the protocol is expected to generate $380 million in annual fee revenue. After the fee switch is flipped (with 1/6 of fees allocated to UNI token holders), UNI holders will receive $66 million in annual income, giving it a dividend yield of 13%. By comparison, the S&P 500 has a forward P/E ratio of 25x and a dividend yield of 1.7%.

I believe anything in DeFi (and digital assets in general) deserves higher multiples than an overextended stock market during an economic downturn.

Once market participants begin applying the same valuation standards to UNI and ETH, UNI will be seen as the cheapest asset among all digital assets.

Below are five reasons some people think you shouldn't hold UNI:

-

The selling pressure from liquidity mining exceeds demand, but only 770,000 UNI are actually released per day. Once the fee switch is turned on and generates yield (liquidity mining may end on November 18), value investors can easily absorb these releases;

-

You believe Uniswap won’t maintain its market leadership, that its trading volume will decline or lose competitiveness (like the so-called "ETH killers");

-

You don’t believe the "fee switch" will happen (or aren’t even aware of it);

-

You believe the fee switch will happen, but since there are still three months left, you're waiting for the best time to buy;

-

UNI is only part of DeFi, and DeFi is no longer popular;

Point 1 is valid, but points 2–5 seem extremely short-sighted.

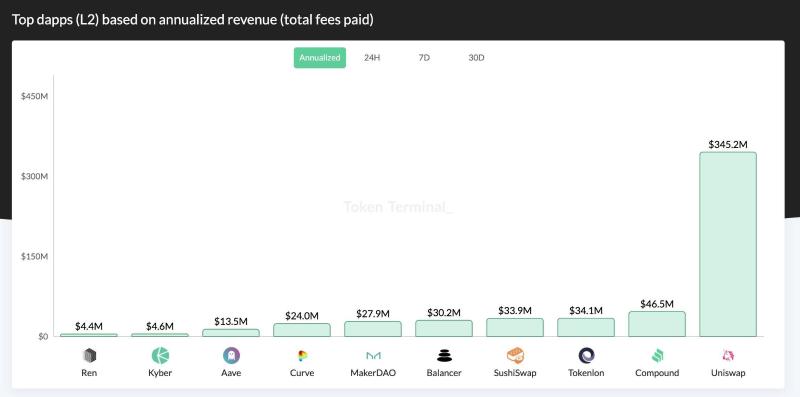

Uniswap is one of the few companies/projects in the digital asset space with real utility and product-market fit. Strangely, digital asset buyers continue chasing unproven future projects (L1 protocols) rather than investing in what already has tangible appeal today.

Investors in Uniswap (UNI) will also benefit from historical lessons.

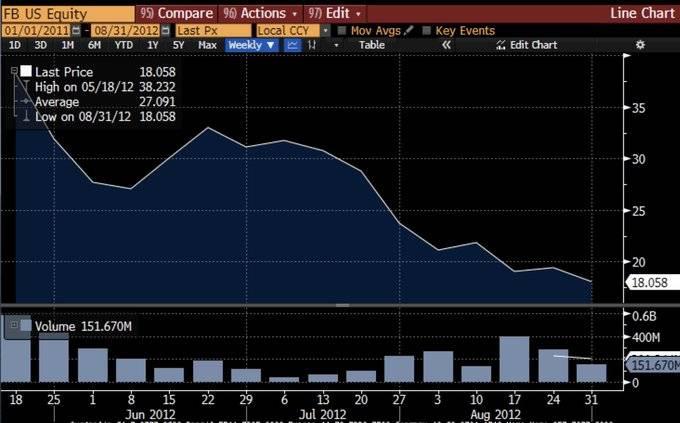

Remember Facebook’s failed IPO? It was priced at $40, then dropped below $20 after going public—everyone feared it was overvalued.

Smart investors don’t bet against market leaders.

UNI is often mistakenly called a "governance" token, and the market assumes "governance has no value."

But in reality, UNI is a pass-thru token—meaning its revenue will flow directly to token holders. UNI holders will gain access to a very substantial income stream starting in February 2021.

Ultimately, all governance tokens need to become value-bearing tokens—that's why voting matters so much: to direct cash flows.

In an industry where genuine growth is hard to achieve, being bearish on a project exhibiting such growth seems irrational.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News